Sometimes, a single slide can explain more than a long report. Points and Figures is our way of breaking down what India’s leading companies are telling their shareholders and analysts. We comb through the decks, pull out the charts and data points that actually matter, and highlight the signals behind the numbers—whether about growth plans, margins, new markets, or risks on the horizon.

This is an extension of The Chatter. While The Chatter focuses on management commentary and earnings call transcripts, Points and Figures dives into investor presentations—and soon, even annual reports—to decode what companies are showing, not just what they’re saying.

We go through every major investor presentation so you don’t have to—bringing you the sharpest takeaways that reveal not just what the company is saying, but what it really means for the business, its sector, and the broader economy.

In this edition, we have covered 17 companies across 10 industries.

Engineering & Capital Goods

Gulf Oil Lubricant

CIE Automotive India

Metals

Hindalco Industries

Frontier Springs

Retail

Titan Company

FMCG

Hindustan Unilever Limited

Monika Alcobev

Jubilant FoodWorks

KRBL Limited

Agriculture

Narmada Agrobase

Media & Entertainment

Balaji Telefilms

MPS Limited

Chemicals

UPL

Captain Polyplast

Healthcare

Apollo Hospitals Enterprise Limited

Automobile

Mahindra & Mahindra Ltd.

Financial Services

Muthoot Finance Limited

Engineering & Capital Goods

Gulf Oil Lubricant | Small Cap | Engineering & Capital Goods

Gulf Oil Lubricants India Ltd (GOLIL), a part of the Hinduja Group, is a key player in the Indian Lubricants Industry. As a subsidiary of Gulf Oil International (GOI), it operates in Automotive and Industrial segments, serving OEMs and various B2B customers through a robust distributor network.

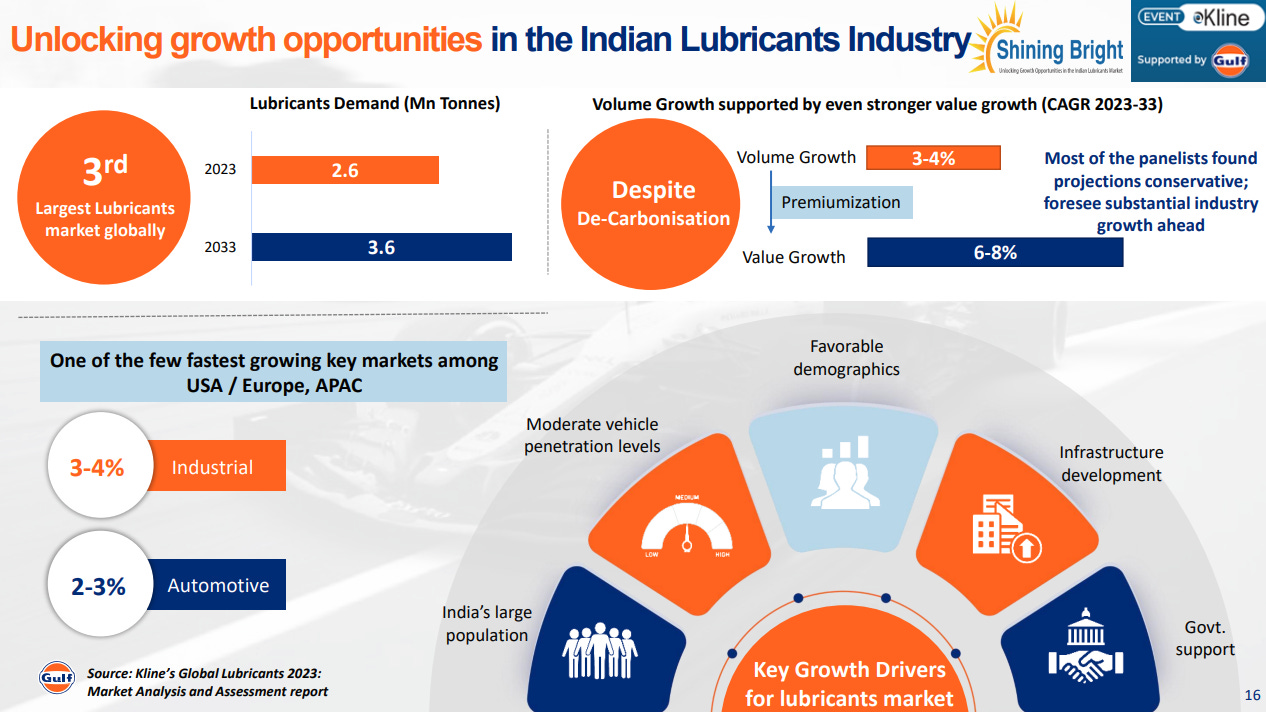

India is the 3rd largest lubricants market globally, with demand expected to grow from 2.6 million tonnes in 2023 to 3.6 million tonnes by 2033. Even with de-carbonisation, volume growth is projected at 3-4% CAGR and value growth at 6-8%, driven by premiumization. Favorable demographics, low vehicle penetration, infrastructure development, and government support make India one of the fastest-growing lubricant markets among the US, Europe, and APAC.

India’s auto market is still deeply under-penetrated with just 8% of households owning cars, and the middle class has more than doubled from 14% in FY05 to 31% now, projected to hit 60-63% by 2047. On top of that, the shift from older BS3/BS4 vehicles to BS6, growing SUV preferences, and stricter emission norms are all pushing demand toward pricier, premium lubricants. The market is quickly transitioning from volume to value.

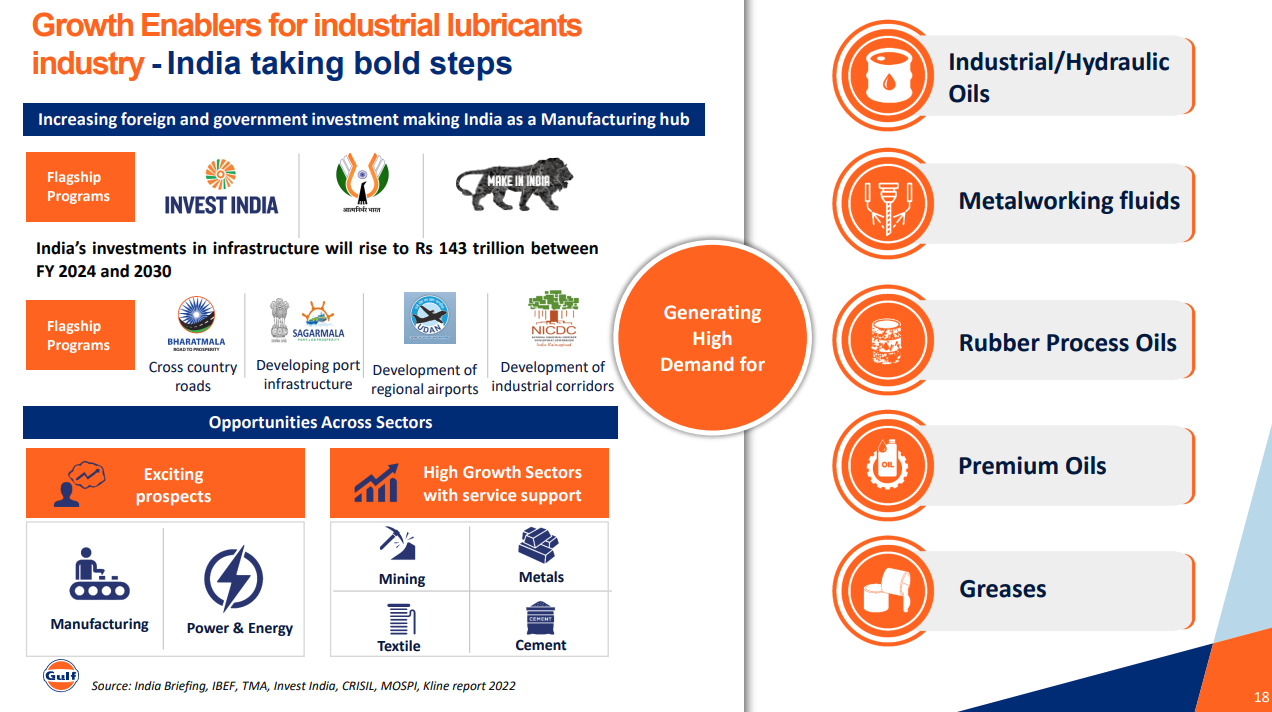

India’s infrastructure investments are expected to hit ₹143 trillion between FY24 and FY30, with flagship programs like Bharatmala, Sagarmala, UDAN, and industrial corridors driving activity. All of this is generating high demand for industrial lubricants across categories like hydraulic oils, metalworking fluids, premium oils, and greases. Sectors like manufacturing, power & energy, mining, metals, textile, and cement add further tailwinds.

CIE Automotive India Limited | Small Cap | Engineering & Capital Goods

CIE Automotive India is a diversified global auto-component manufacturer specializing in forging, casting, and stamping for major vehicle segments. The company maintains a strong geographic footprint in India and Europe, serving leading OEMs across passenger and commercial vehicle platforms.

Heavy European forging exposure tethers group performance to cyclical industrial shocks and volatile energy costs in the EU. India’s diversified product mix acts as the primary margin cushion, offsetting high-risk specialization in mature Western markets.

High customer concentration in India, with the largest client accounting for 32% of sales, ties financial performance closely to the success of specific OEMs. Strategic resilience depends on maintaining these anchor relationships while gradually diversifying the client base to mitigate potential market share shifts by lead customers.

The multi-year performance trend reveals a structural step-up in Return on Net Assets (RONA) compared to the pre-2021 period, despite recent margin volatility. Sustaining these higher return levels suggests the business has achieved a more favorable product mix and better cost control than in previous automotive cycles.

A massive 31.5% surge in tractor production during the final quarter indicates a strong rural recovery and potential inventory restocking. This sharp inflection point suggests that the cyclical bottom in the farm equipment segment is likely behind us and will drive volume growth in early CY26.

Long-term projections favor the two-wheeler segment with 7-9% growth, while the heavy truck market is expected to face structural stagnation due to rail competition. This shift in the internal product mix will require realigning manufacturing capacity to maintain margin stability over the next five years.

Metals

Hindalco Industries Limited | Large Cap | Metals

Hindalco is a global leader in aluminum and copper, serving as the flagship metals business of the Aditya Birla Group. The company integrates bauxite mining with downstream high-value manufacturing to serve automotive, packaging, and construction sectors worldwide.

Recycling bauxite residue into the cement and infrastructure sectors suggests a fundamental shift toward industrial symbiosis rather than simple waste disposal. This strategy reduces long-term environmental provisioning risks and improves local unit economics through lower waste-handling costs.

Deploying pumped storage for round-the-clock renewable energy signals a push to solve the intermittency problem of green power at a structural scale. This move locks in lower baseline energy costs and effectively hedges the business against future carbon-based trade barriers in key export regions.

Chinese supply caps and the green energy transition are creating a structural floor for aluminium prices. This setup allows Hindalco to maximize margins while global supply remains in a deficit.

Strong 9% growth in domestic aluminium demand, led primarily by the automotive sector, indicates a robust industrial cycle that is absorbing local supply. A higher domestic consumption mix typically allows for better realizations compared to the export market, strengthening the quality of the India business earnings.

Domestic demand and byproduct gains are insulating copper margins from weak global smelting fees. This stability secures a reliable cash engine regardless of volatile global market rates.

A sharp drop in copper EBITDA per ton reflects tightening global treatment and refining charges (Tc/Rc) alongside a less favorable concentrate mix. This highlights the copper segment’s vulnerability to global supply-side constraints for raw materials despite maintaining steady shipment volumes.

Frontier Springs | Small Cap | Metals

Frontier Springs Ltd is a global leader in manufacturing hot wound springs for various industries including transportation, industrial, and government applications. Their diverse product range includes a variety of springs such as Hot Coil Springs, Leaf Springs, and Industrial Springs for different applications like mass transit, railroads, pipe hangers, and power generators.

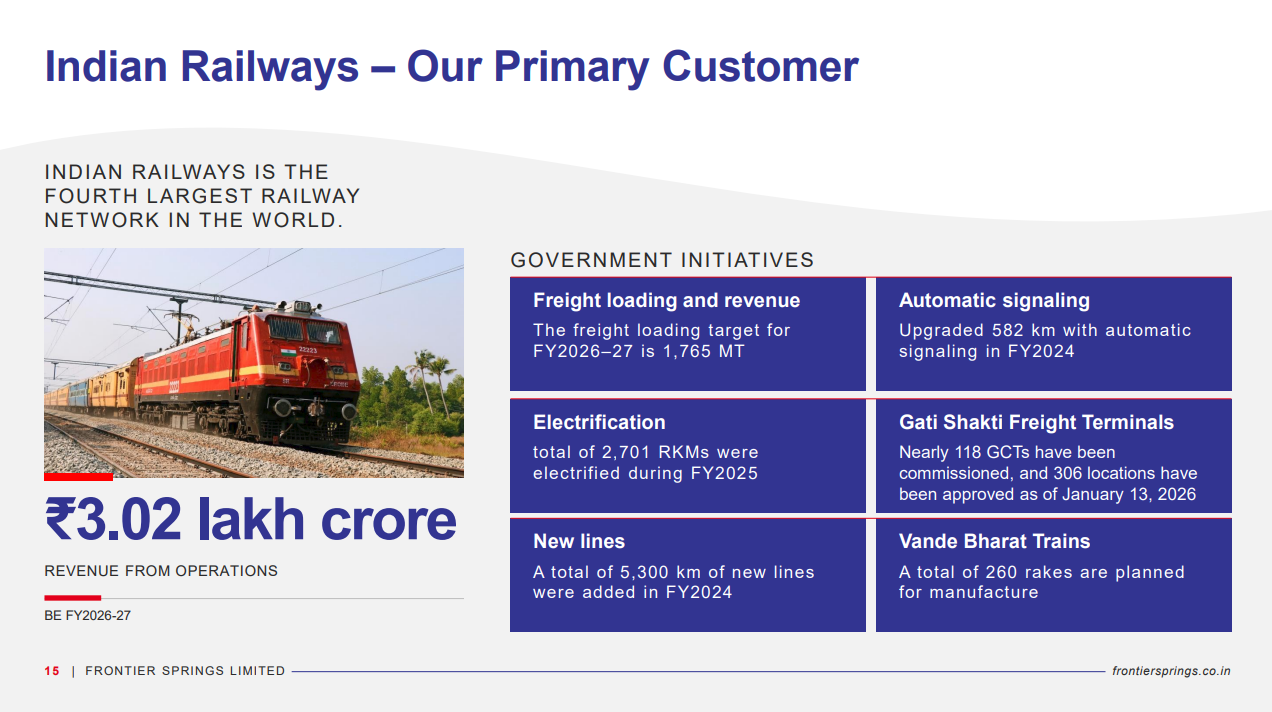

Indian Railways is Frontier Springs’ primary customer, with a budgeted revenue of ₹3.02 lakh crore for FY2026-27 and a freight loading target of 1,765 MT. The government is actively investing in electrification, new lines (5,300 km added in FY24), automatic signaling, Gati Shakti freight terminals, and 260 planned Vande Bharat rakes. For a springs manufacturer tied to railways, all of this translates directly into demand.

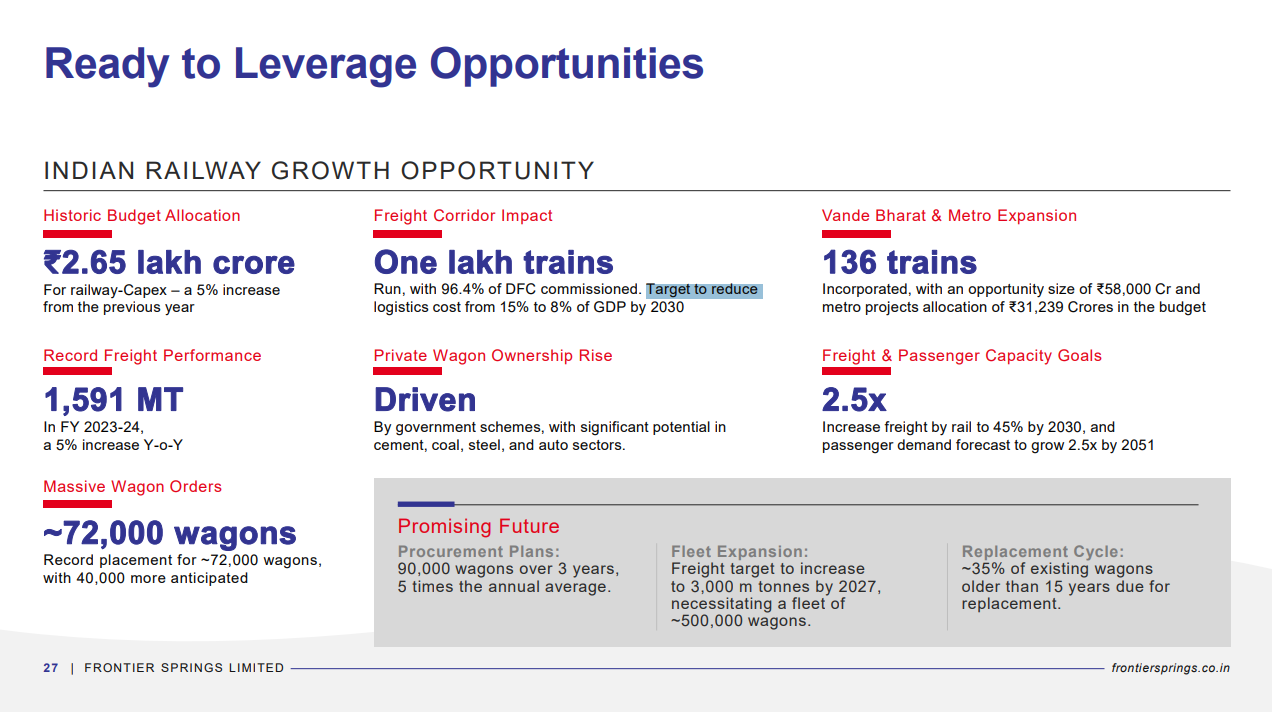

Railway capex stands at ₹2.65 lakh crore (up 5% YoY), with record wagon orders of ~72,000 and another 40,000 anticipated, plus a procurement plan of 90,000 wagons over the next 3 years. The freight target is to hit 3,000 MT by 2027 requiring a fleet of ~500,000 wagons, and ~35% of existing wagons are already over 15 years old and due for replacement. For Frontier Springs, this combination of new orders and replacement demand creates a strong growth runway.

Retail

Titan Company Limited | Large Cap | Retail

Titan is India’s leading lifestyle company with a dominant presence in organized jewellery, watches, and eyewear. The company operates a vast retail network across multiple brands, focusing on design-led consumer discretionary products and high-trust retail formats.

Revenue scaling from roughly ₹11,000 crore to over ₹57,000 crore in a decade reflects a masterclass in organized retail expansion. This trajectory validates the success of the multi-category lifestyle strategy and suggests high replicability as the company enters new segments like sarees and bags.

Low organized jewellery penetration of only 8% despite Titan’s dominance indicates a massive, long-term runway for growth driven by market formalization. High digital influence in sales confirms that the brand’s moat is evolving beyond physical presence to capture younger, tech-savvy consumer segments.

FMCG

Hindustan Unilever Limited | Large Cap | FMCG

Hindustan Unilever is India’s leading consumer goods company with a vast portfolio spanning home, beauty, and food categories. It maintains a dominant market share through an extensive distribution network that reaches millions of retail outlets nationwide.

Volume-led growth of 4% nearly matching sales growth confirms that demand is recovering without relying on aggressive price hikes. This shift toward volume suggests a healthier consumption environment and better long-term operating leverage compared to inflation-driven revenue spikes.

A 1400-basis point improvement in service levels for quick commerce shows a dedicated effort to own the fastest-growing urban channel. By institutionalizing quick-commerce capabilities, the firm protects its market share against digital-first brands while lowering fulfillment lead times by 20%.

Scaling premium acquisitions like Minimalist shows HUL is successfully transitioning from a mass-market giant to a luxury-niche competitor. This shift reduces reliance on price-sensitive consumers, protecting margins even when raw material costs for basic soaps rise.

Resilient 4% volume growth indicates pricing power is stabilizing as commodity volatility subsides across key categories. This suggests a structural shift toward volume-led market share gains rather than inflation-driven revenue growth seen in previous cycles.

Price-led growth masks a decline in core demand, suggesting consumers are trading down to cheaper regional brands. Margin durability now hinges on volume recovery rather than further price hikes which have likely peaked.

The exit from ice cream and full acquisition of OZiva signals an aggressive pivot toward high-margin wellness and digital-native categories. This portfolio pruning aims to improve capital efficiency by reducing exposure to capital-intensive and lower-margin seasonal businesses.

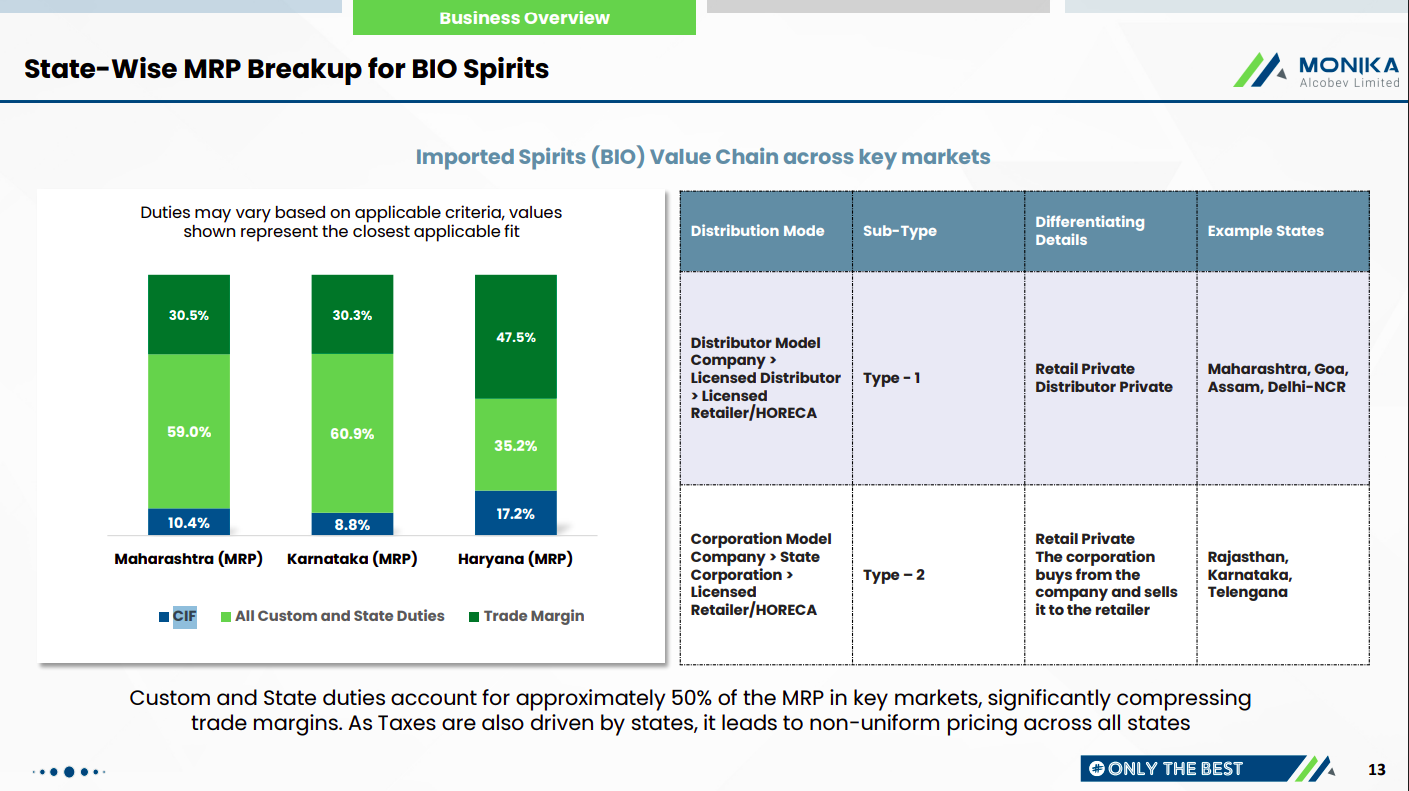

Monika Alcobev | Micro Cap | FMCG

Monika Alcobev is a prominent player in the imported liquor sector, focusing on premium and luxury alcoholic beverages. Specializing in importing, sales, distribution, and marketing of luxury spirits, wines, and liqueurs in India and the Indian Subcontinent, including Travel Retail Duty Free Shops.

Customs and state duties account for ~50–60% of MRP across key states like Maharashtra, Karnataka, and Haryana, significantly compressing trade margins. State-driven tax structures and distribution models (private distributor vs corporation model) lead to non-uniform pricing across India.

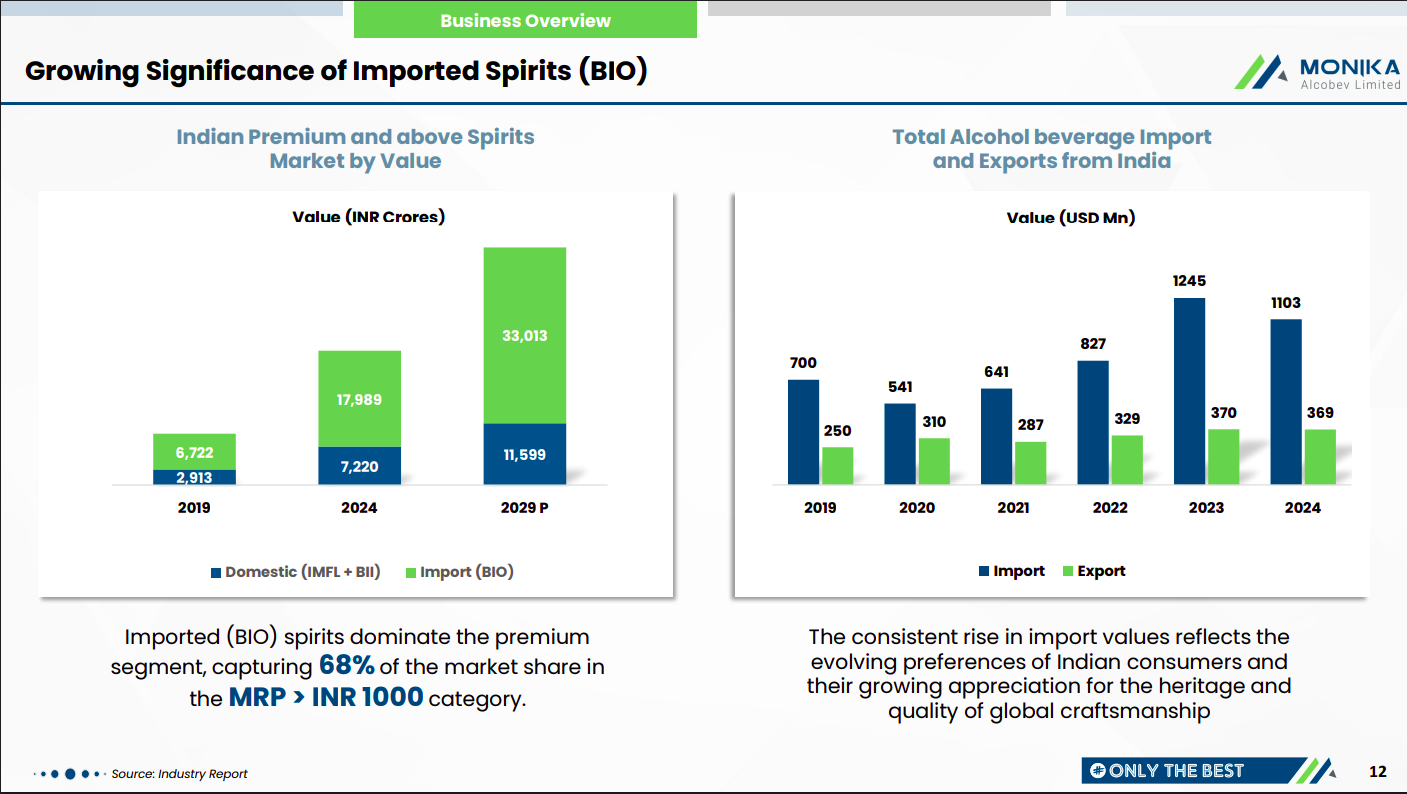

Imported spirits dominate India’s premium segment, capturing ~68% share in the MRP > ₹1,000 category. Rising import values reflect premiumization trends and growing consumer preference for global brands and higher-quality offerings.

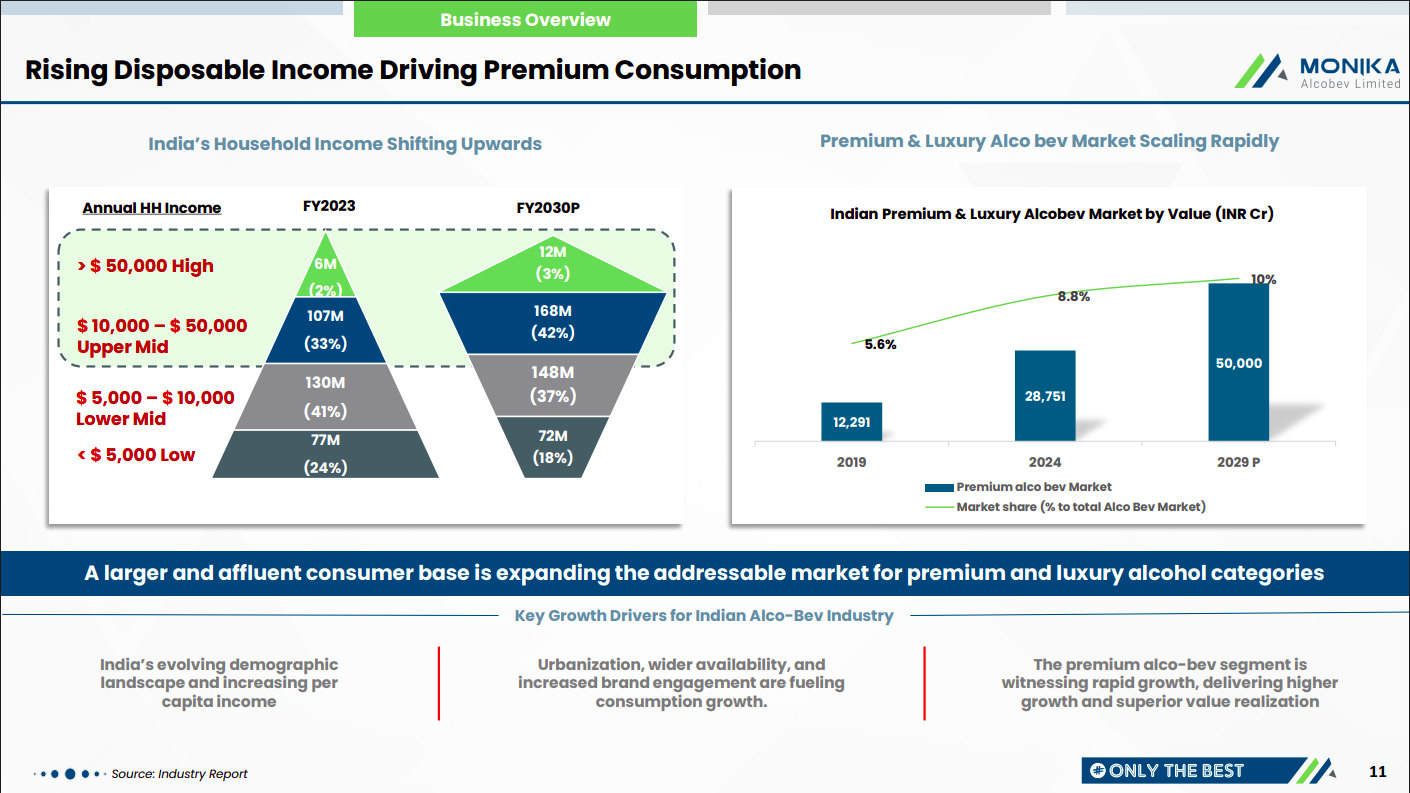

India’s upward income mobility is expanding the upper-middle and high-income segments, increasing the addressable base for premium and luxury alco-bev products. The premium segment is scaling rapidly, with market value projected to nearly double by 2029.

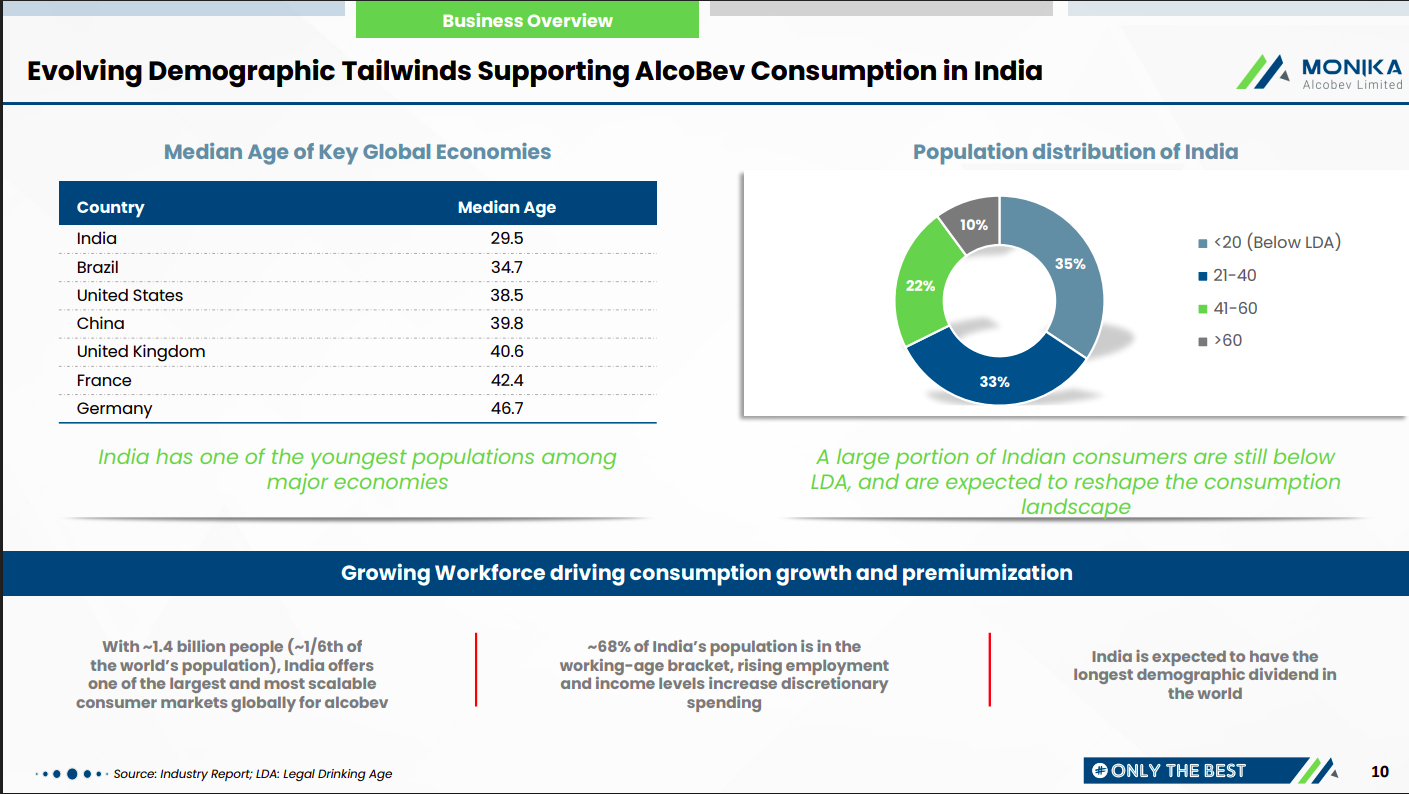

India has one of the youngest populations globally (median age ~29.5), with ~68% in the working-age bracket, supporting long-term consumption growth. A large young demographic below legal drinking age is expected to drive future premiumization and sustained demand expansion.

Jubilant FoodWorks | Mid Cap | FMCG

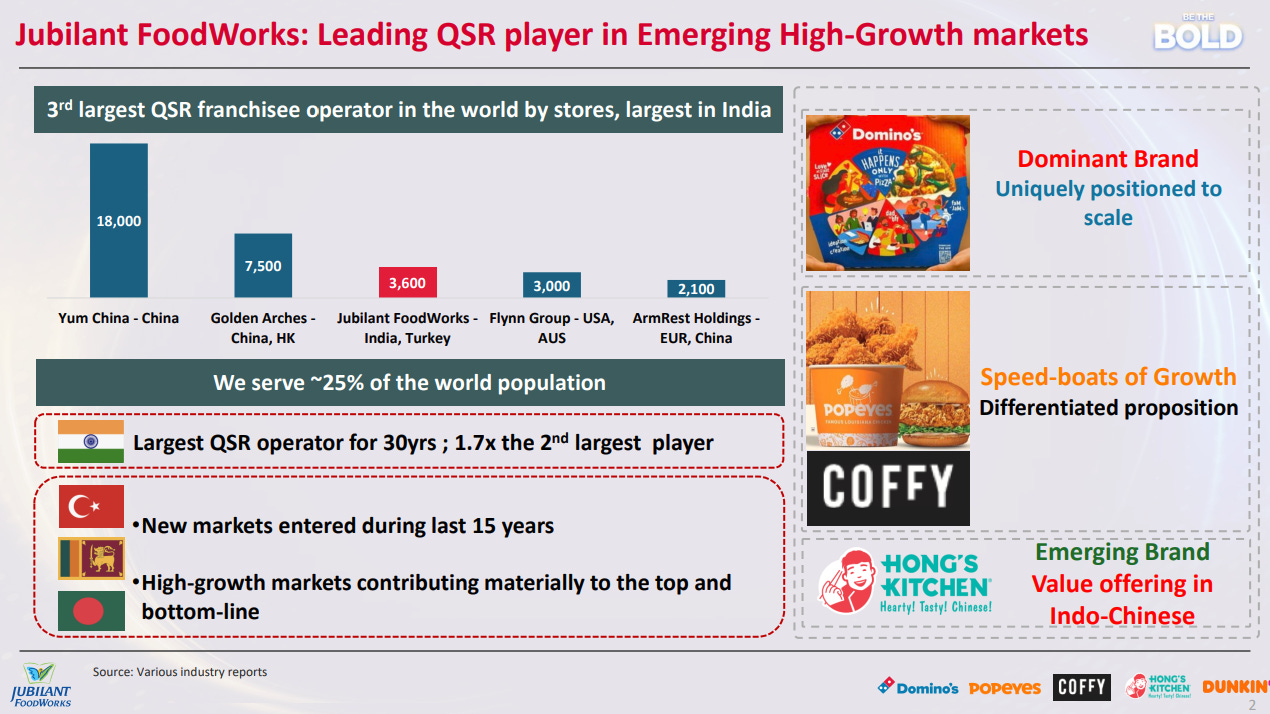

Jubilant FoodWorks Limited (JFL) is part of the Jubilant Bhartia Group and is one of the India’s largest food service Company. The company was incorporated in 1995 and initiated operations in 1996. It is India’s largest and fastest growing food service company. The company is a food service company and engaged in retail sales of food through two strong international brands, Domino’s Pizza and Dunkin’ Donuts addressing different food market segments.

Jubilant FoodWorks is the 3rd largest QSR franchisee operator globally with 3,600 stores, and the largest in India by a wide margin at 1.7x the second-biggest player. It serves roughly 25% of the world’s population across India, Turkey, Bangladesh, and Sri Lanka. Beyond the dominant Domino’s brand, it’s building newer bets like Popeyes, Coffy, and Hong’s Kitchen as independent growth drivers.

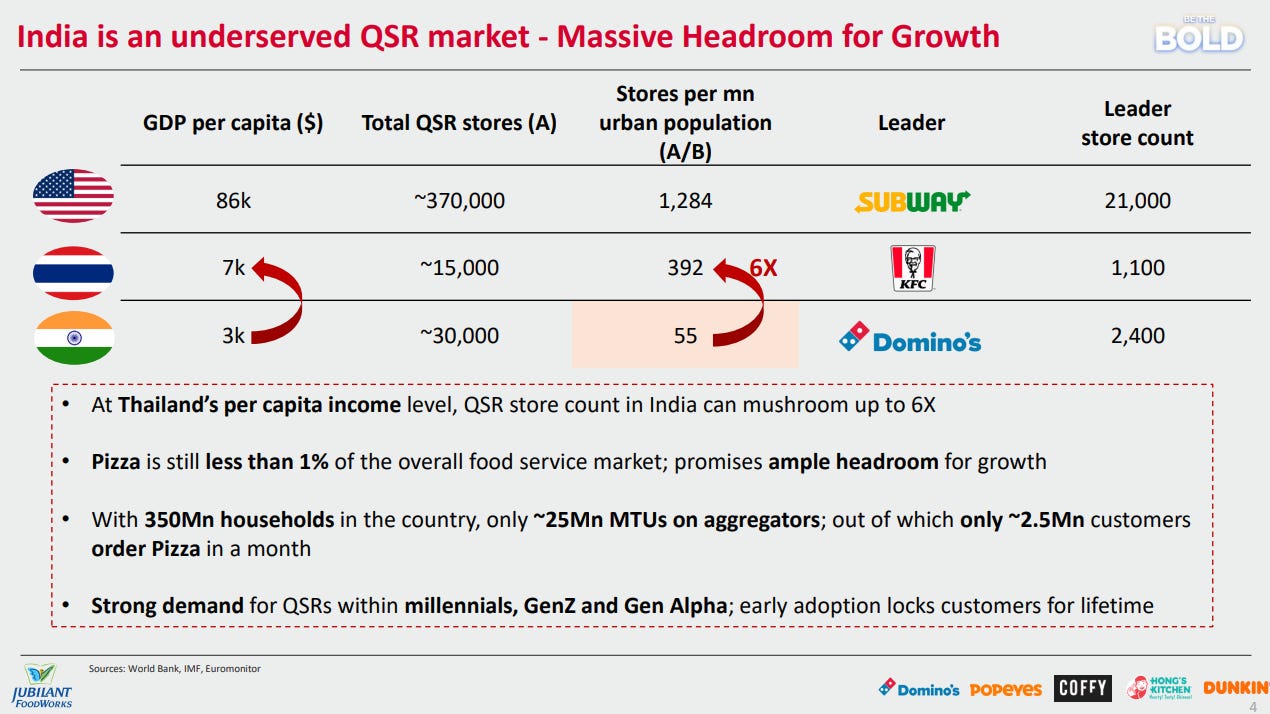

India has just 55 QSR stores per million urban population compared to 392 in Thailand and 1,284 in the US, and as incomes rise, store counts could grow up to 6x. Pizza is still less than 1% of the overall food service market, and only about 2.5 million out of 350 million households order pizza in a month. The penetration gap is massive.

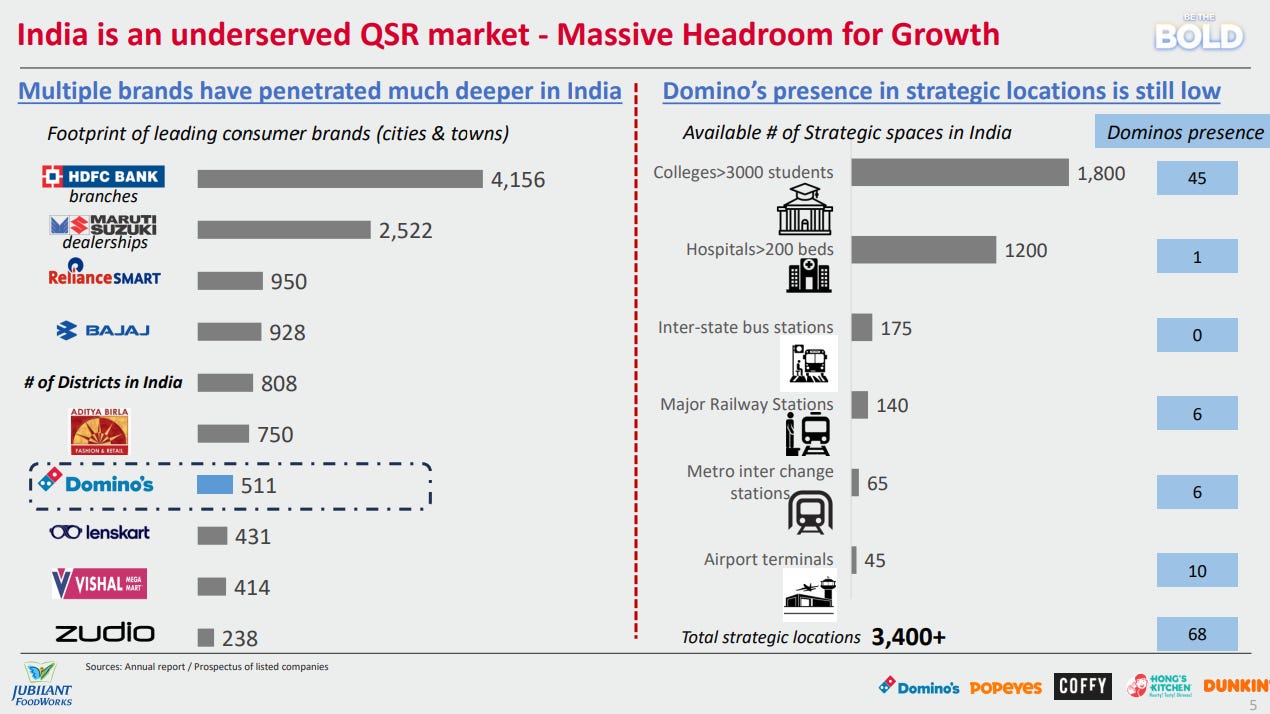

Domino’s is present in just 511 cities and towns, well behind brands like HDFC Bank (4,156) and Maruti Suzuki (2,522) that have gone much deeper into India. There are over 3,400 strategic high-footfall locations across colleges, hospitals, railway stations, and airports, but Domino’s is in only 68 of them. Even within its existing brand, there’s a lot of white space left before it hits any kind of saturation.

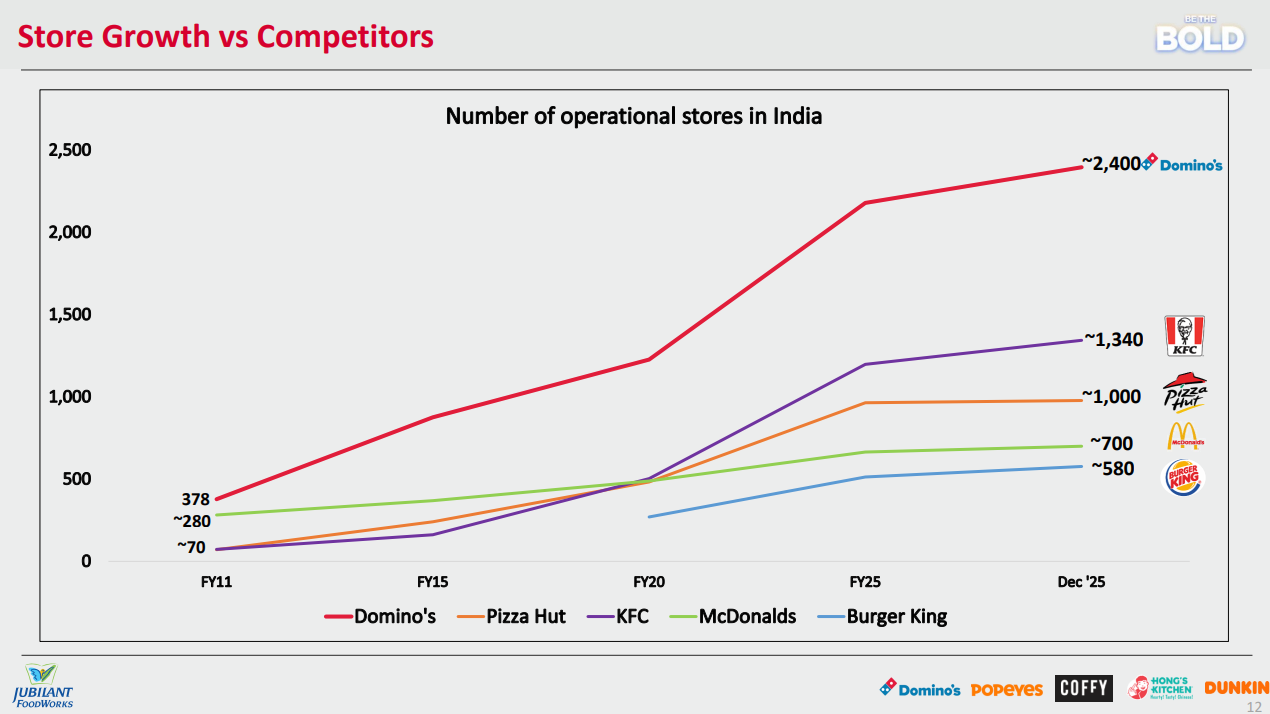

Domino’s has ~2,400 stores in India as of December 2025, nearly double the next biggest QSR player KFC at ~1,340. From 378 stores in FY11 to 2,400 now, it’s grown faster and more consistently than every major competitor including Pizza Hut, McDonald’s, and Burger King.

KRBL Limited | Small Cap | FMCG

KRBL Limited is India’s leading integrated rice miller and exporter, widely recognized for its flagship basmati brand, India Gate. The company maintains a dominant market share in both domestic and international markets through a robust distribution network and integrated processing facilities.

KRBL is the world’s largest rice miller and basmati exporter, with FY25 total income of ₹5,655 crore and a market share of 37.8% in general trade and 39.3% in modern trade. It reaches 12 million households in India and exports to over 90 countries. FY25 EBITDA margin stood at 13% with a PAT margin of 8.4%.

KRBL operates the largest rice milling plant in Punjab, has 850+ distributors across India, and runs the largest contact farming network for rice. The India Gate brand commands a significant premium over the industry average on basmati export realization per MT, reflecting strong pricing power. All of this is backed by a strong financial position with substantial internal accruals and minimal debt.

KRBL’s net worth has grown steadily from ₹3,693 crore in FY21 to ₹5,240 crore in FY25, with very low debt dependence throughout. Net bank debt has swung between small positive and negative figures, sitting at -₹405 crore in FY25, meaning the company is effectively net cash. It’s a clean balance sheet with minimal leverage.

India is the #1 rice exporter globally, holding 85% of the basmati export market with 16% volume growth expected in FY25. The Middle East alone accounts for 76% of India’s basmati exports by volume, with growing demand from the US and Indian diaspora markets adding further tailwinds. For KRBL, as the market leader in basmati, these export trends translate directly into opportunity.

Agriculture

Narmada Agrobase | Nano Cap | Agriculture

Narmada Agrobase is an ISO 9001:2015 certified company specializing in the manufacturing and processing of cotton seed meal cake, cattle feeds, and soya bean meal. Its high-protein products benefit cattle nutrition, while by-products serve industries like Textiles, Consumer Goods, and Paper.

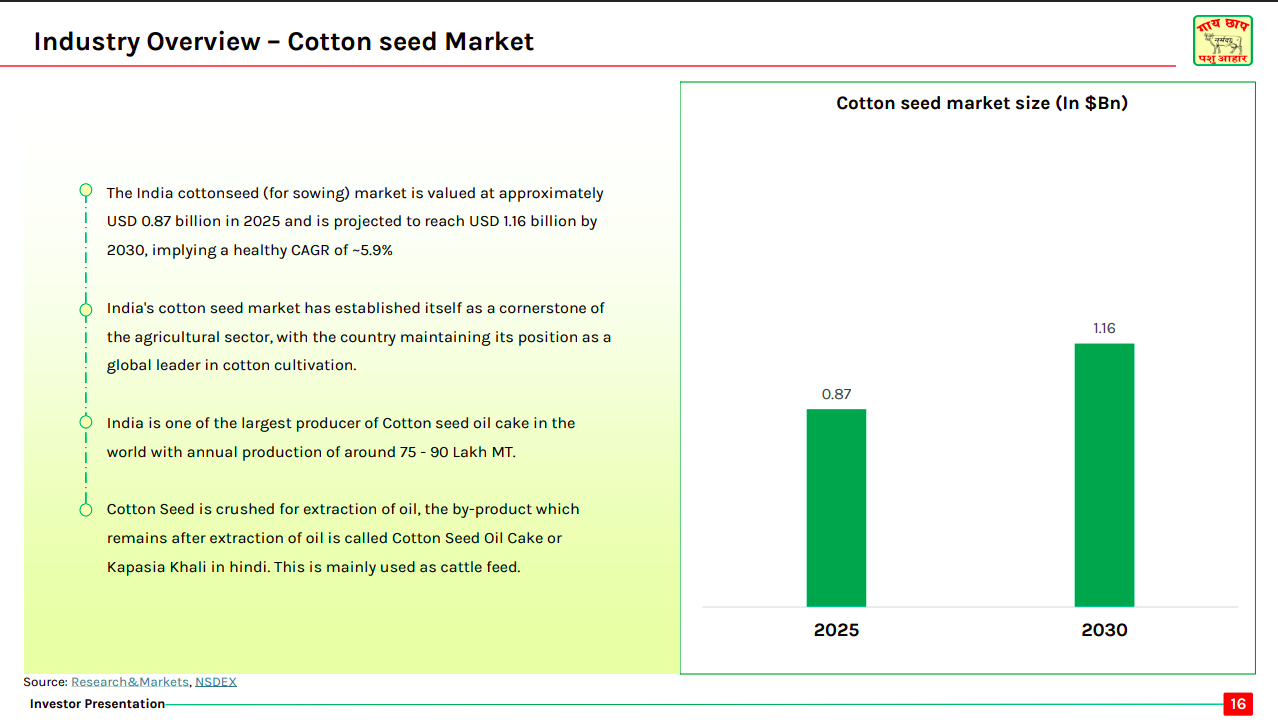

India’s cotton seed market is valued at ~$0.87Bn in 2025 and is projected to reach ~$1.16Bn by 2030, implying ~5.9% CAGR. India remains a global leader in cotton cultivation, with significant cottonseed oil cake production used primarily as cattle feed.

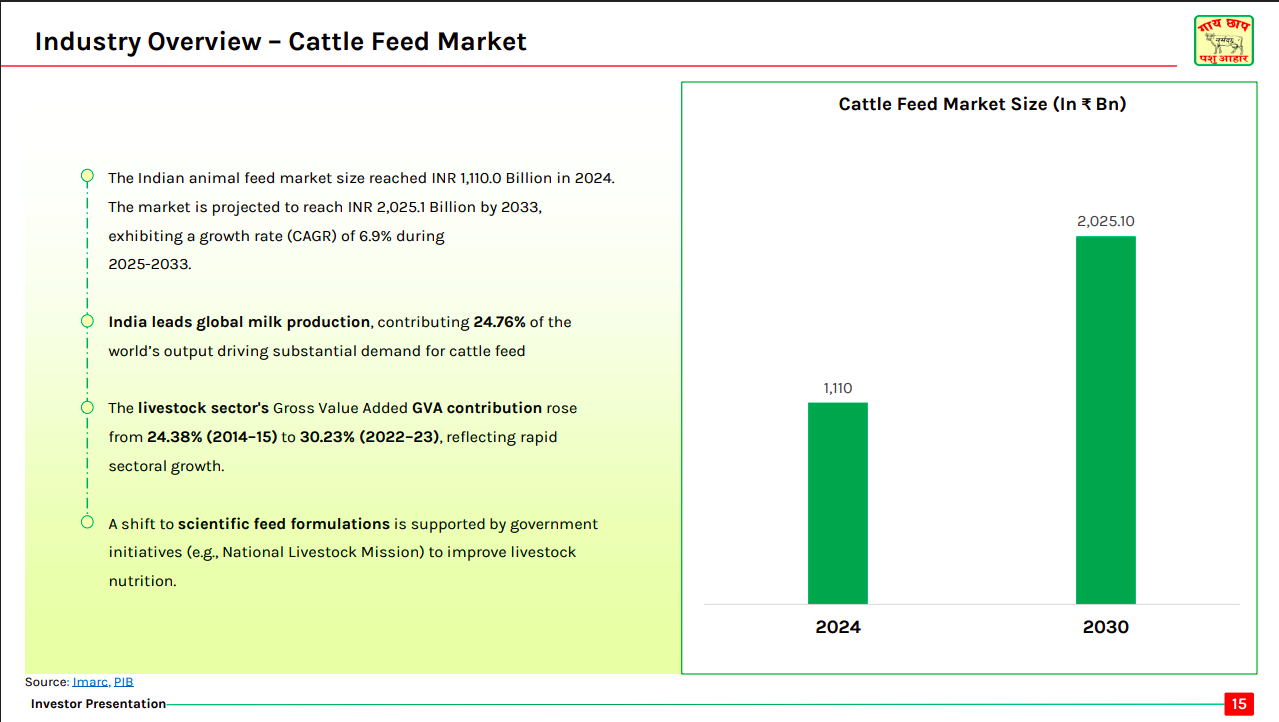

India’s cattle feed market stood at ₹1,110Bn in 2024 and is expected to grow to ₹2,025Bn by 2030+, driven by ~6.9% CAGR. Strong milk production leadership and rising livestock GVA contribution are fueling demand for scientific and nutritionally balanced feed.

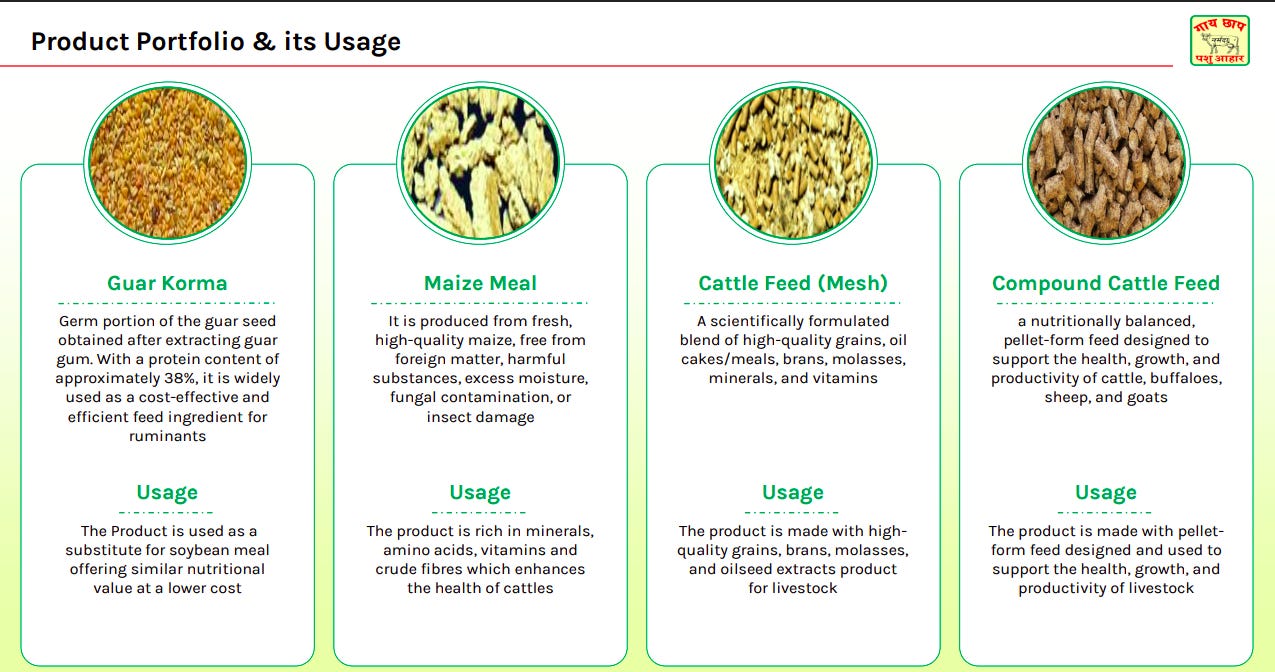

The company offers diversified feed products including Guar Korma, Maize Meal, Cattle Feed (Mesh), and Compound Cattle Feed. These products provide high-protein, mineral-rich, and nutritionally balanced solutions to enhance livestock health, growth, and productivity.

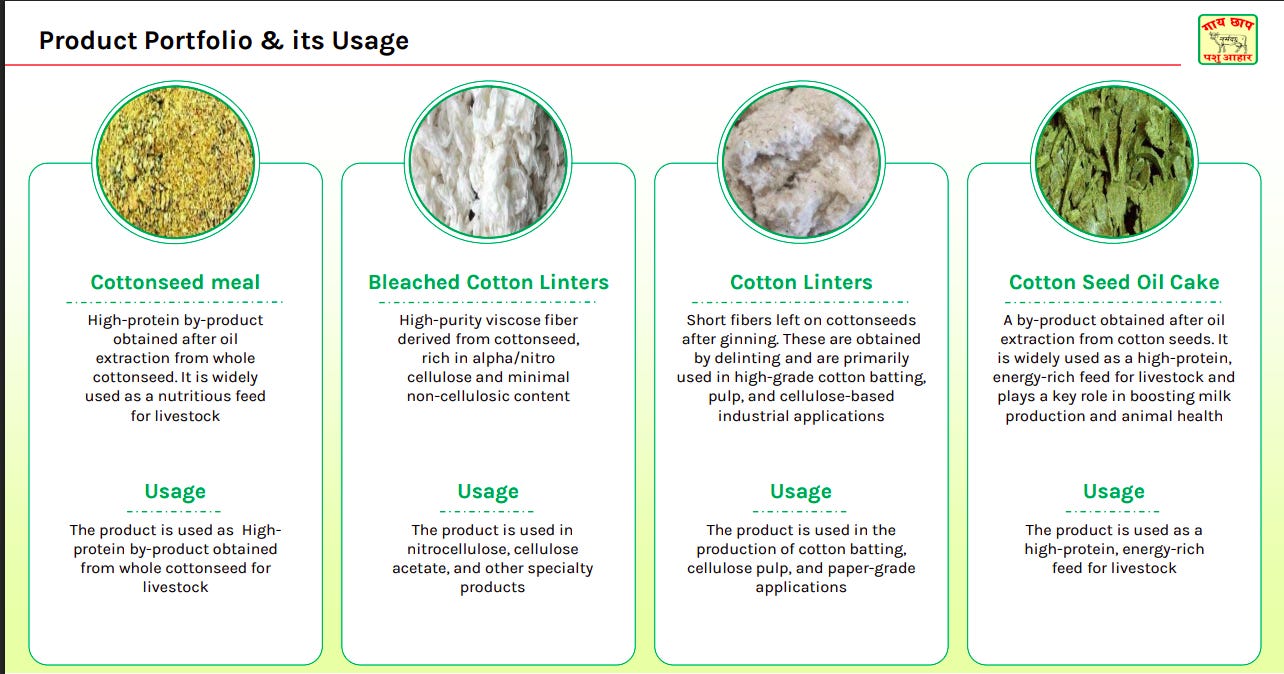

The portfolio includes cottonseed meal, cotton linters, bleached cotton linters, and cottonseed oil cake. While oil cake and meal serve as high-protein livestock feed, linters are used in cellulose, pulp, paper, and specialty industrial applications.

Media & Entertainment

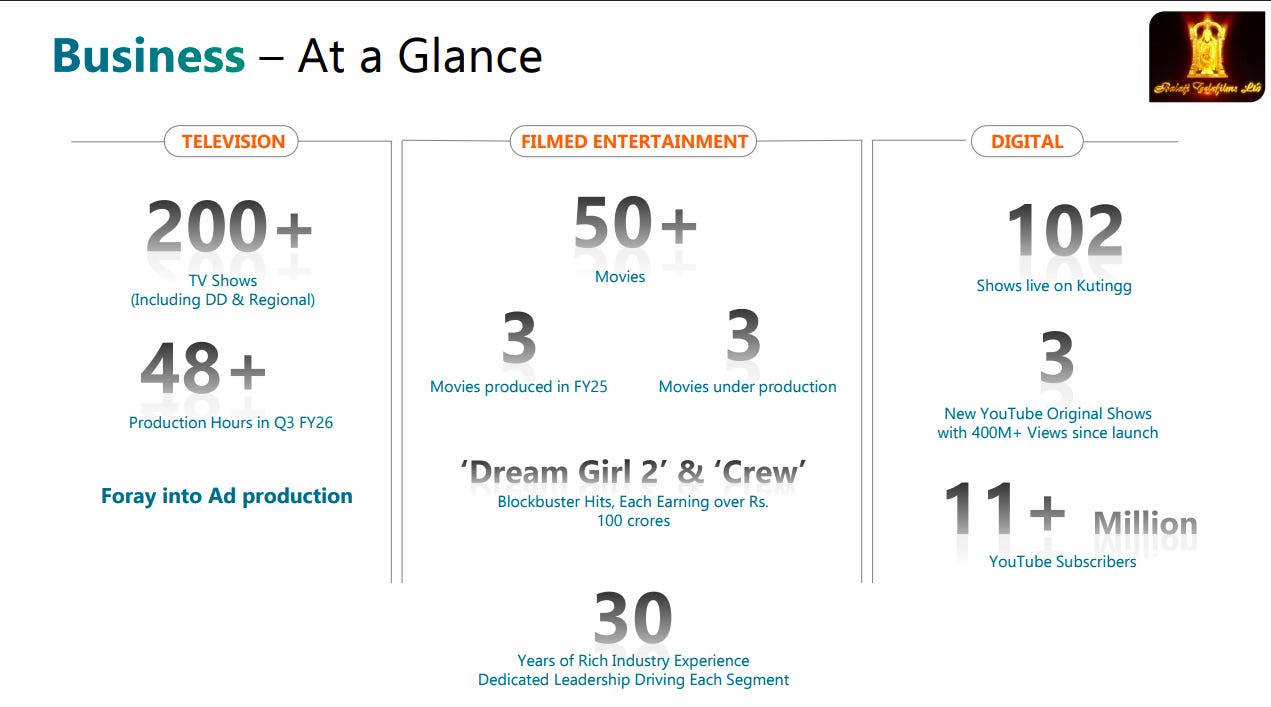

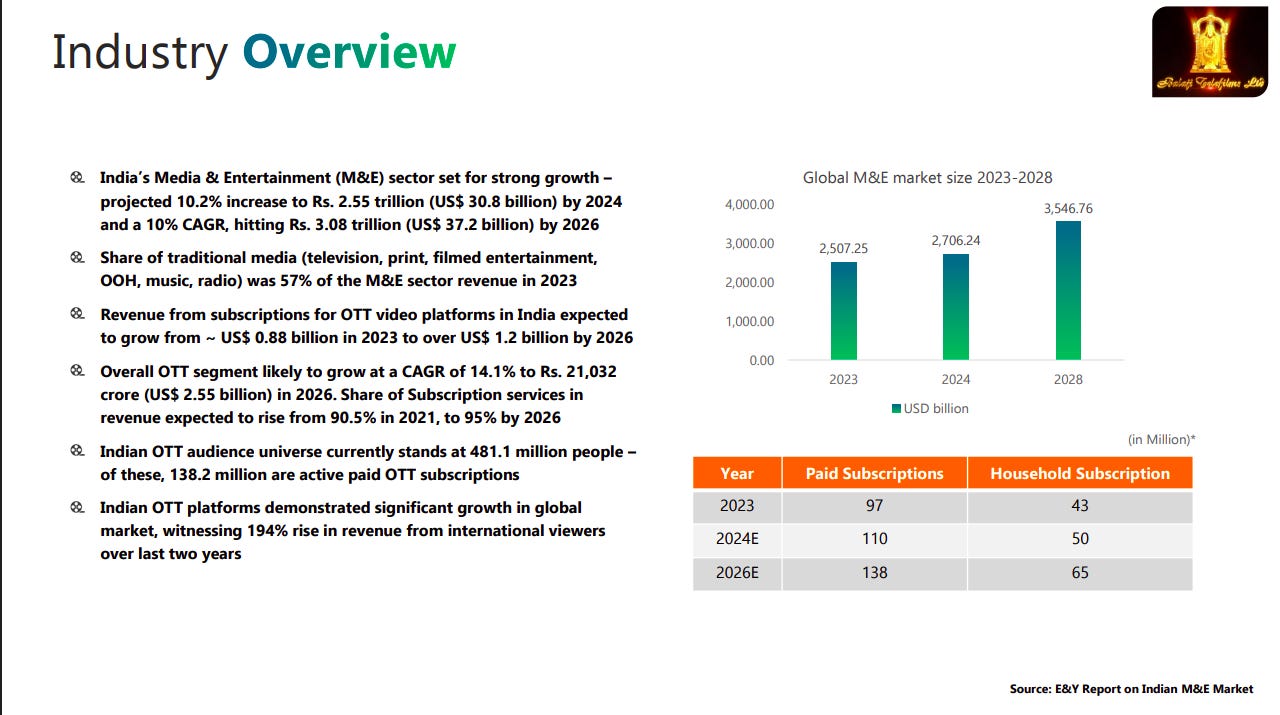

Balaji Telefilms | Micro Cap | Media & Entertainment

Balaji Telefilms Limited is a leading content production house in Asia and the Middle East, known for creating Hindi and regional content. It has made a significant impact on Indian television and expanded to producing movies through its subsidiary, Balaji Motion Pictures.

The company has a diversified presence across Television (200+ shows), Filmed Entertainment (50+ movies), and Digital (102 shows live). With 30 years of industry experience, it has delivered blockbuster hits and built a strong digital footprint with 11+ million YouTube subscribers.

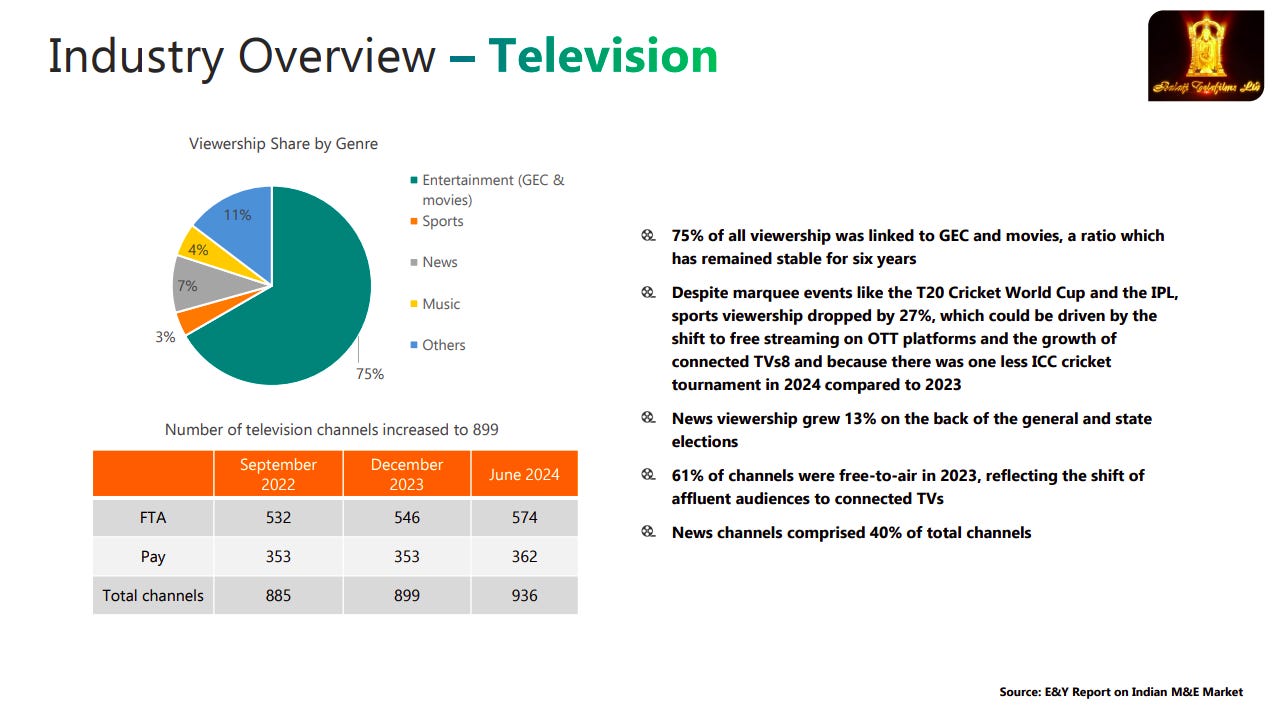

GEC and movies account for 75% of total TV viewership, a trend stable over six years, while sports viewership declined due to OTT migration. Total TV channels increased to 936 by June 2024, with 61% being free-to-air and news channels comprising 40% of the total.

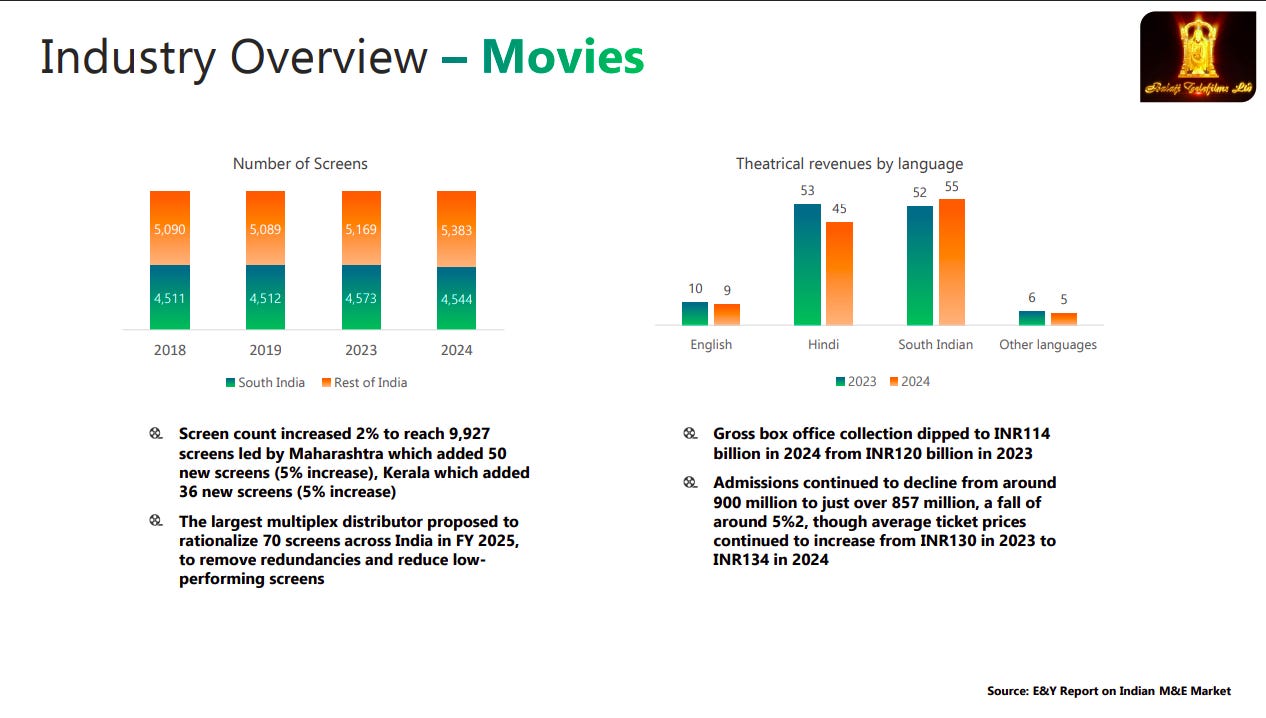

India’s screen count rose 2% to 9,927 in 2024, though box office collections dipped to ₹114 billion amid a 5% drop in admissions. Despite lower footfalls, average ticket prices increased, and rationalization of screens is expected in FY25 to improve efficiencies.

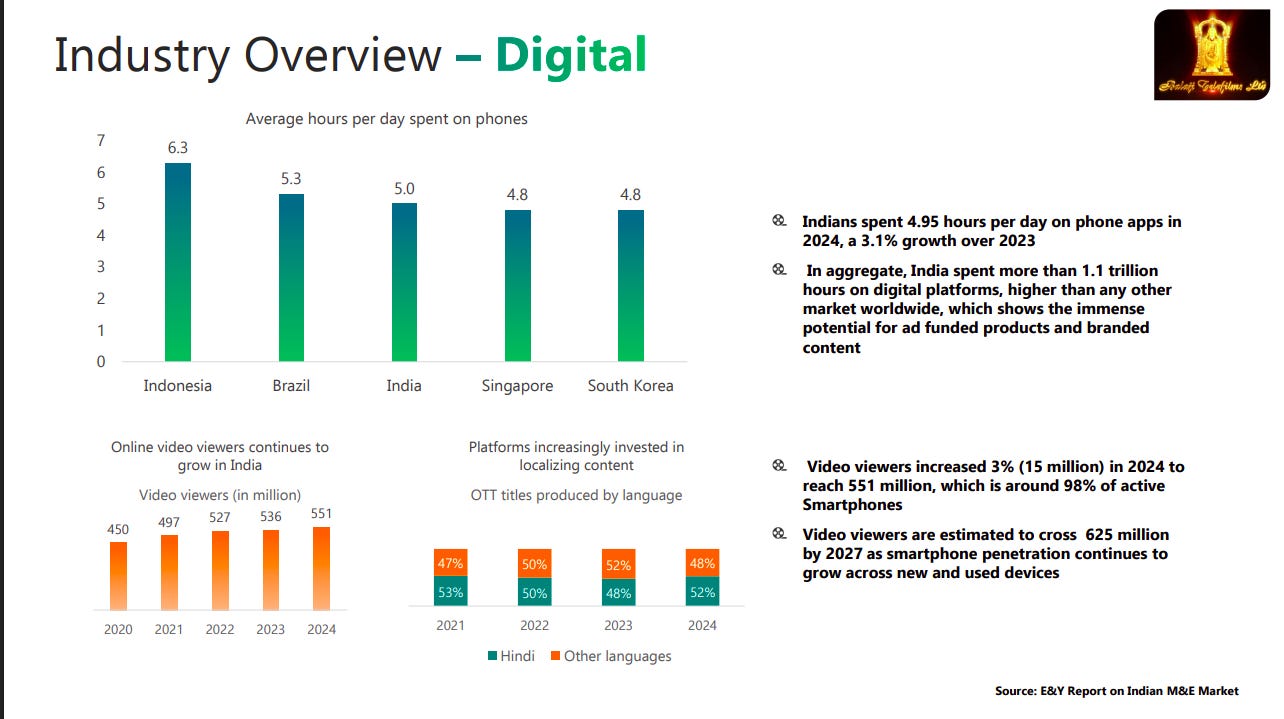

Indians spent 4.95 hours per day on phone apps in 2024, with digital video viewers rising to 551 million and expected to cross 625 million by 2027. India leads globally in total digital hours spent, highlighting strong monetization potential for OTT and branded content.

India’s M&E sector is projected to grow at ~10% CAGR, reaching ₹3.08 trillion by 2026, driven by OTT expansion and subscription growth. Paid OTT subscriptions are expected to rise from 97 million in 2023 to 138 million by 2026, with increasing household penetration.

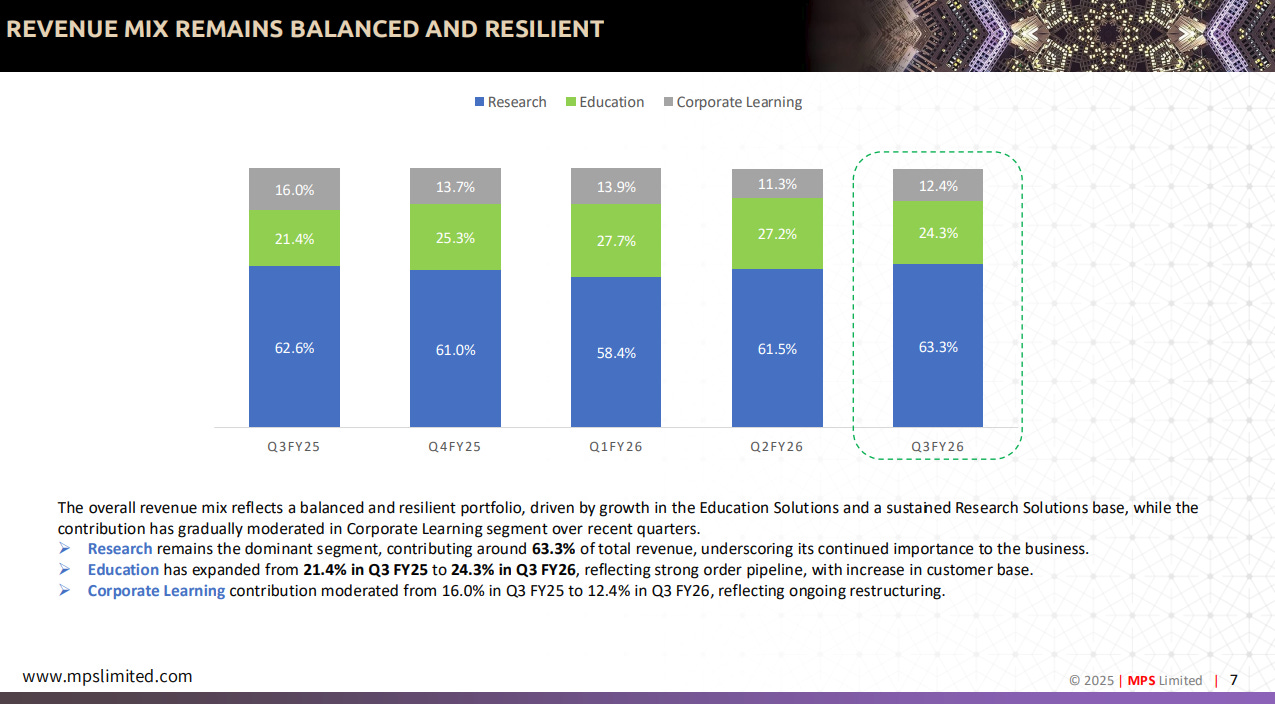

MPS Limited | Small Cap | Media & Entertainment

MPS Limited provides platform-led content, learning, and platform solutions to global publishers, enterprises, and educational institutions. The company operates through three main segments: Research Solutions, Education Solutions, and Corporate Learning.

Research remains MPS Limited’s dominant segment at 63.3% of revenue in Q3 FY26, holding steady over the last five quarters. Education has been the growth story, expanding from 21.4% to 24.3% over the same period on the back of a strong order pipeline. Corporate Learning, meanwhile, has moderated from 16% to 12.4% due to ongoing restructuring.

On a 9-month basis, Research still leads at 61.1% of revenue in 9M FY26, while Education has jumped sharply from 19.7% to 26.4% year-on-year. Corporate Learning has slipped from 16.5% to 12.5% as the segment undergoes restructuring. The mix is gradually tilting toward Education as the main growth lever.

Chemicals

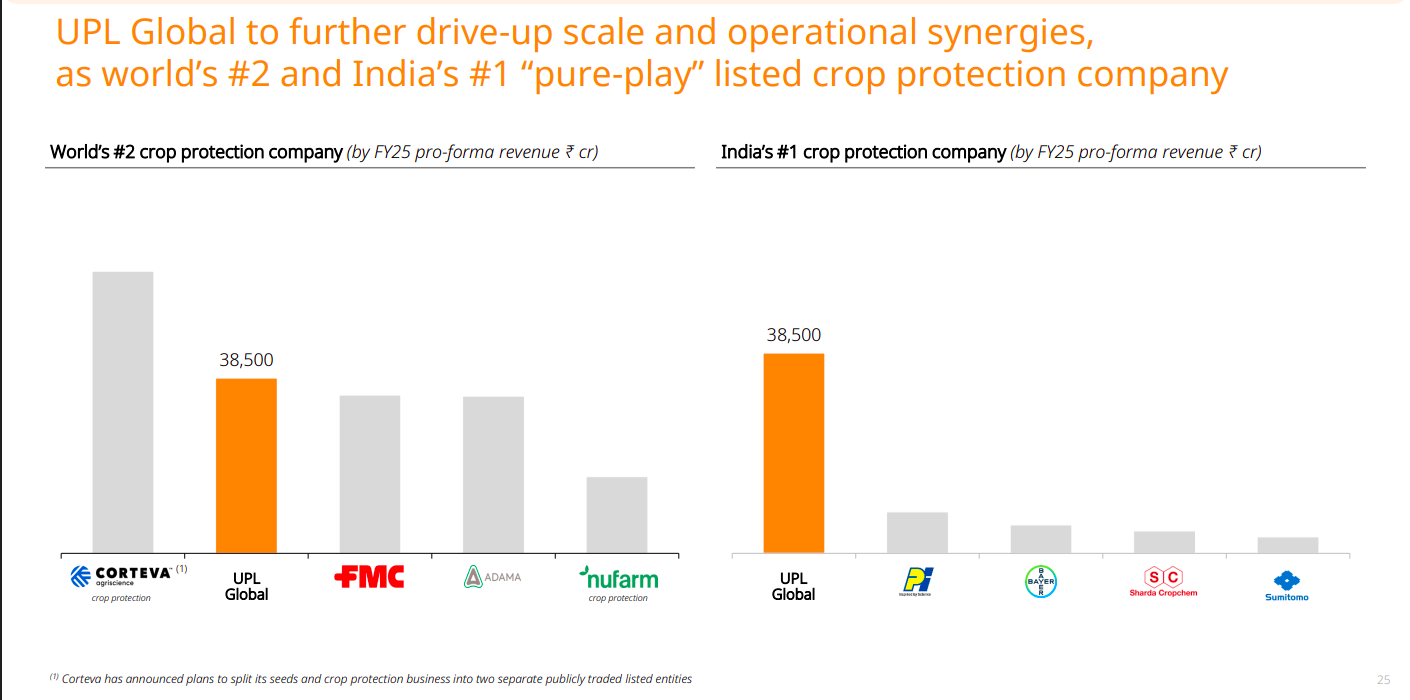

UPL | Mid Cap | Chemicals

UPL Limited is a global leader in agricultural solutions, operating in multiple countries. The company engages in the production and sale of agrochemicals, field crops, vegetable seeds, as well as industrial chemicals.

UPL positions itself as the world’s #2 and India’s #1 pure-play listed crop protection company based on FY25 pro-forma revenue (~₹38,500 crore). It ranks alongside global majors and leads the Indian market with significant scale advantages.

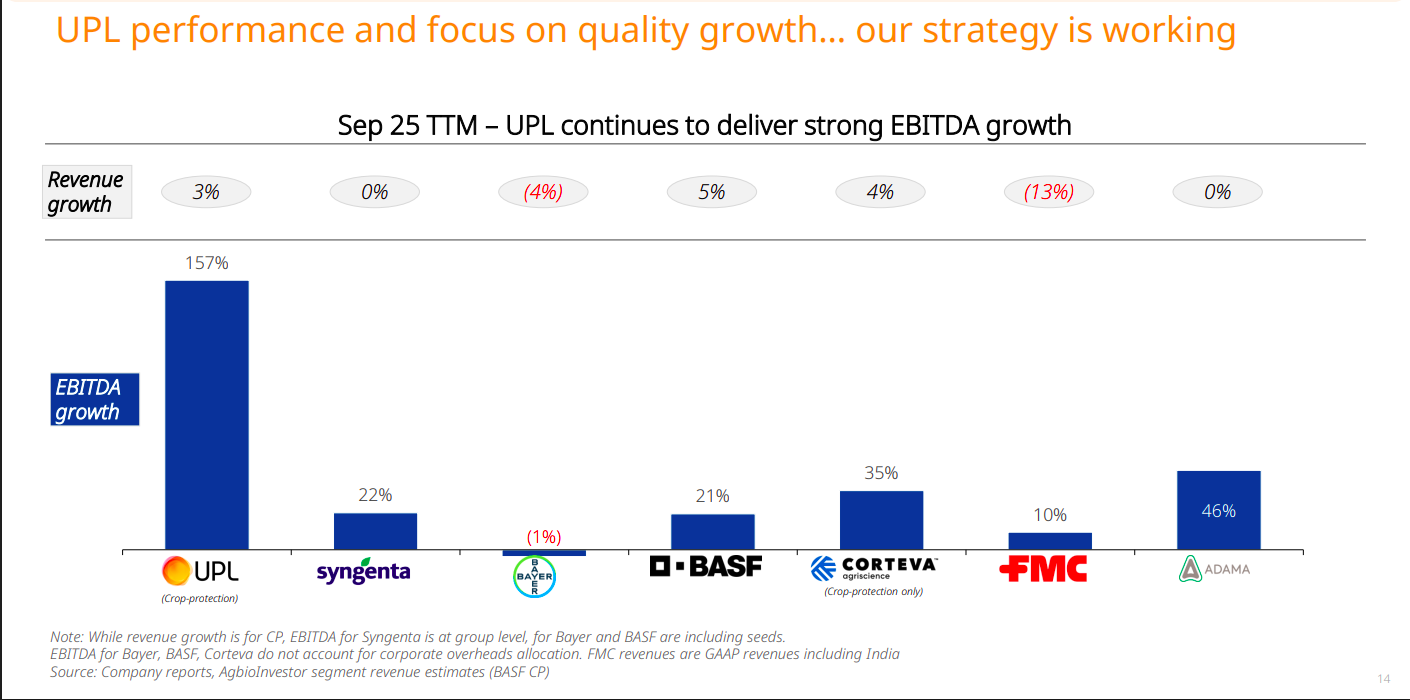

Despite muted revenue growth across peers, UPL delivered industry-leading EBITDA growth of 157% (Sep’25 TTM). This reflects strong operational execution and margin recovery compared to competitors like Syngenta, BASF, FMC, and Bayer.

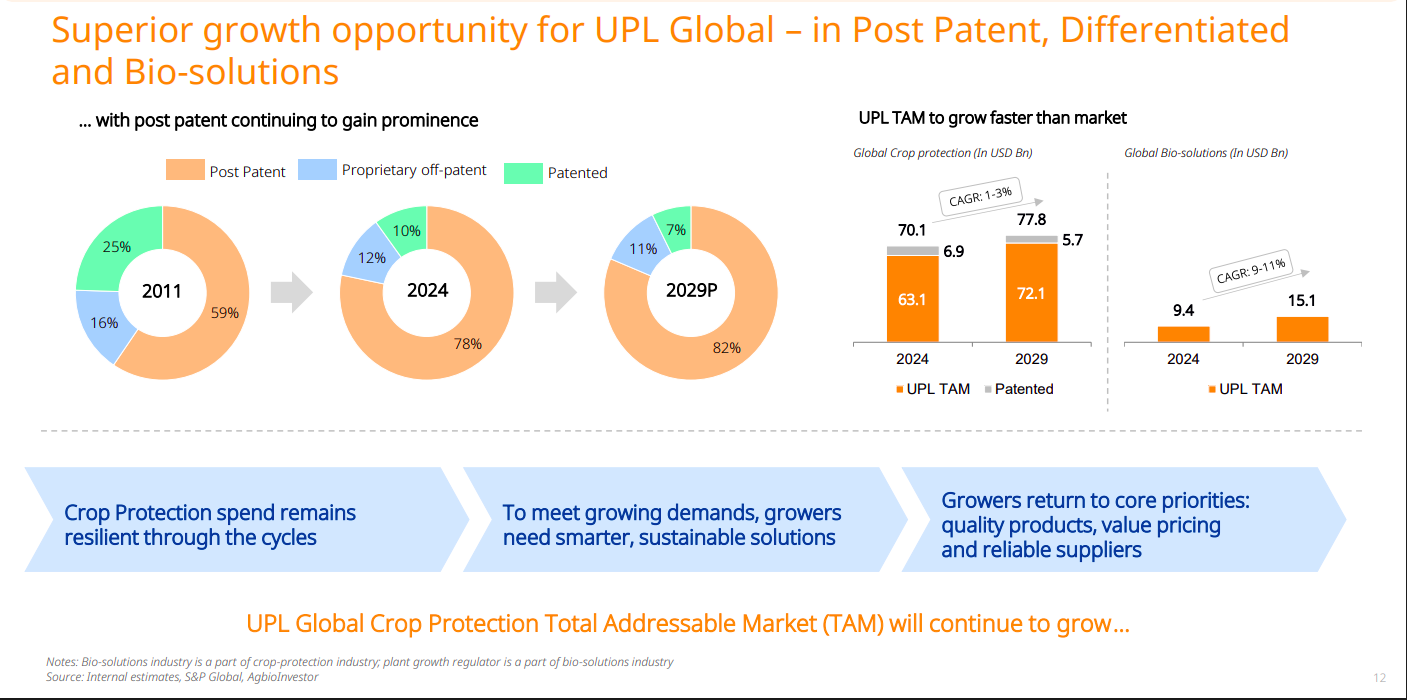

The crop protection mix is increasingly shifting toward post-patent products (59% in 2011 to 82% by 2029P). UPL’s total addressable market (TAM) is expected to grow steadily, with bio-solutions expanding faster (9–11% CAGR) than the broader crop protection market.

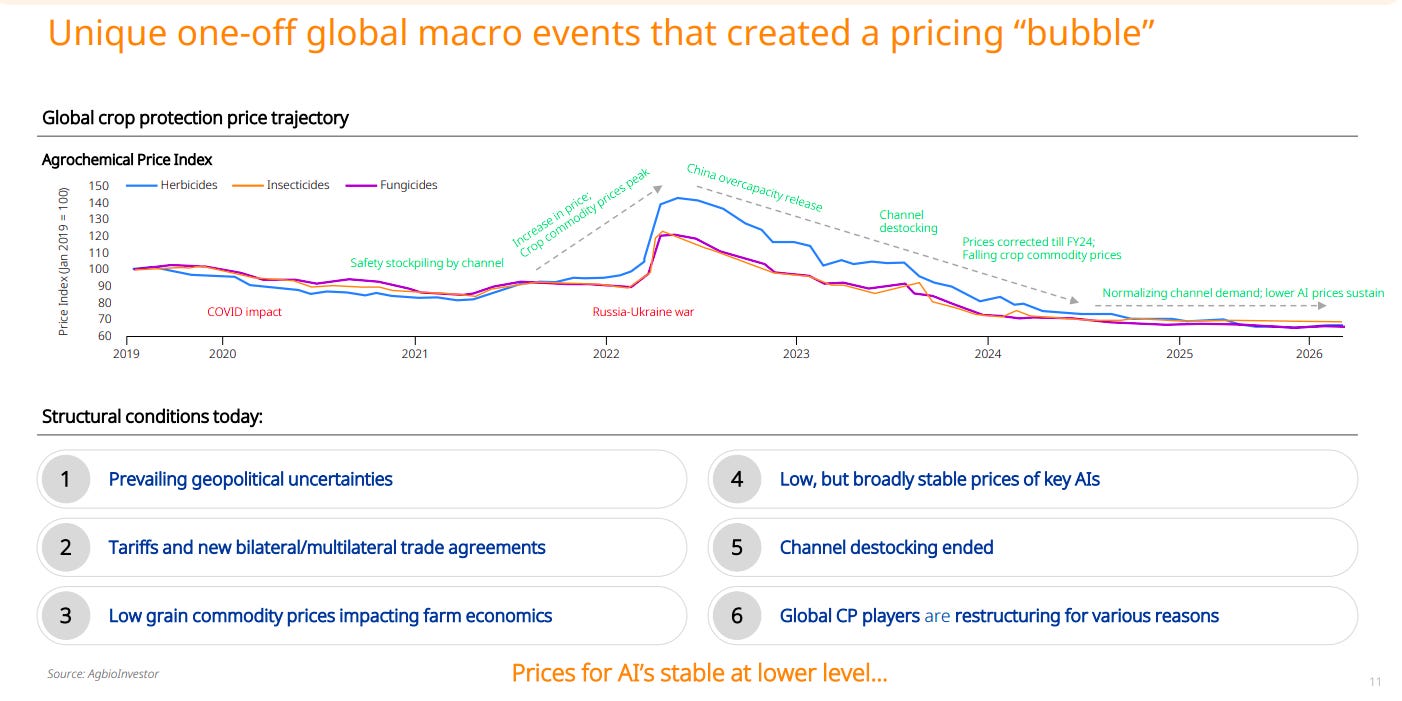

Agrochemical prices spiked due to COVID disruptions, supply chain issues, and the Russia-Ukraine war, creating a temporary pricing bubble. Prices have since corrected and stabilized at lower levels, with channel destocking largely complete and structural reset underway.

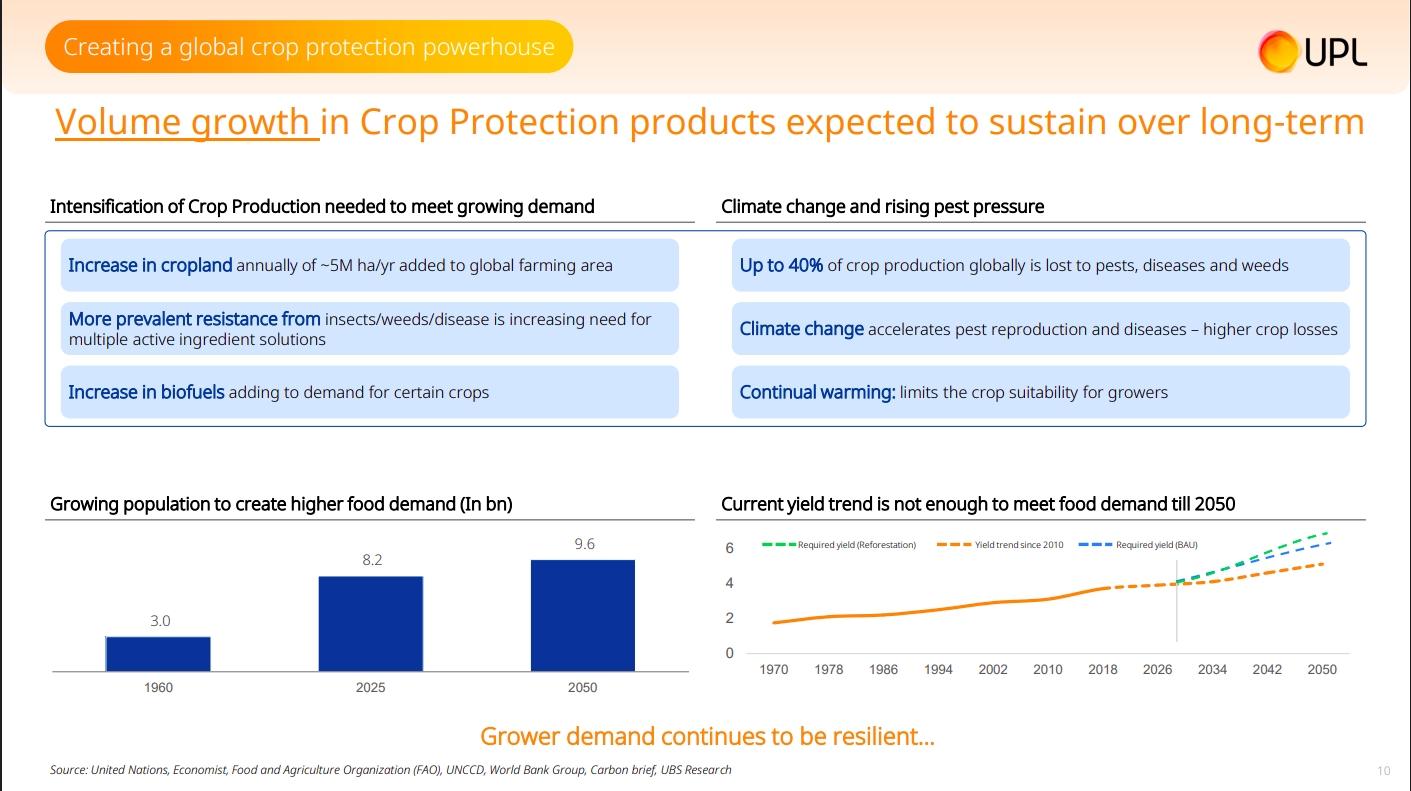

Structural demand drivers such as population growth (9.6bn by 2050), rising pest pressures, climate change, and yield gaps support sustained volume growth in crop protection. Increasing cropland, biofuel demand, and resistance management needs further reinforce long-term resilience in grower demand.

Captain Polyplast | Micro Cap | Chemicals

Captain Polyplast Limited is a leading manufacturer, exporter, and trading company specializing in top-quality HDPE Pipes and Irrigation Equipments such as Drip and Sprinkler Irrigation Systems, various Filters, Fittings, Valves, and more.

CPL offers a comprehensive portfolio across drip and sprinkler irrigation, including emitting pipes, inline/online emitters, lateral pipes, sprinkler pipes, and mini sprinklers. The diversified product suite positions the company to address water-efficiency needs across varied crop and farm applications.

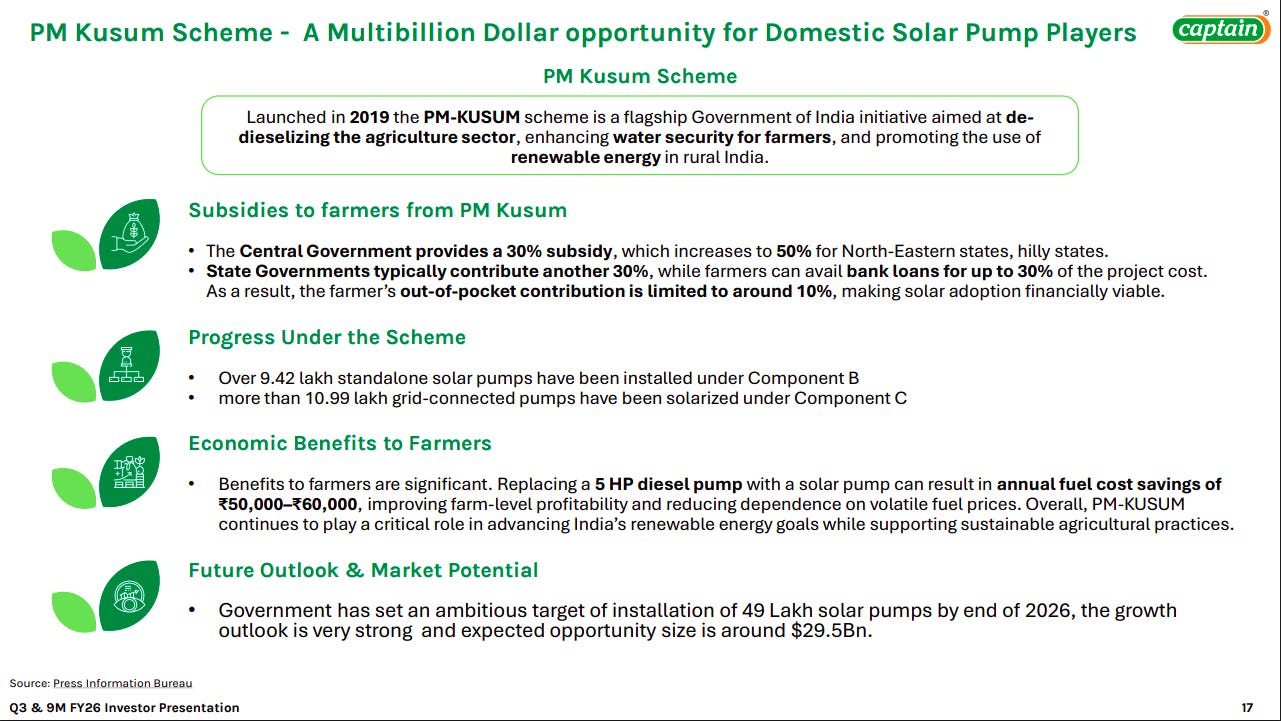

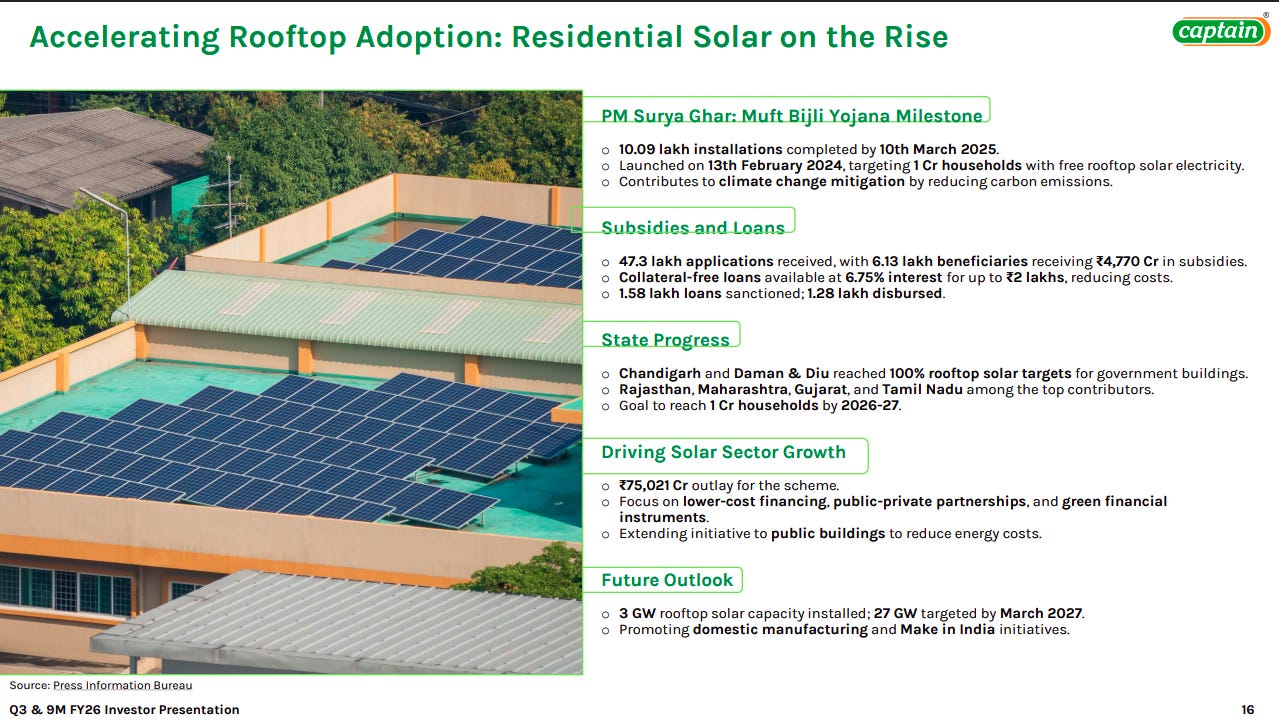

The PM-KUSUM scheme drives solar pump adoption through heavy subsidies (up to ~60% combined central and state support), limiting farmers’ out-of-pocket cost to ~10%. With ~49 lakh pump installation targets by 2026 and a ~$29.5Bn opportunity, the scheme presents a large structural growth runway for domestic solar pump players.

Under PM Surya Ghar, rooftop solar adoption is scaling rapidly with over 10 lakh installations and strong subsidy-backed financing support. With a 27 GW target by March 2027 and focus on domestic manufacturing, rooftop solar is emerging as a key driver of distributed renewable growth.

Healthcare

Apollo Hospitals Enterprise Limited | Large Cap | Healthcare Services

Apollo Hospitals is India’s leading integrated healthcare provider, operating a vast network of multi-speciality hospitals, pharmacies, and primary care clinics. The company combines physical infrastructure with a large-scale digital health platform to offer comprehensive clinical services across the country.

Significant EBITDA margin expansion in AHLL and HealthCo segments suggests these retail and digital units have reached a critical inflection point for operating leverage. If these units sustain current profitability trajectories, the consolidated bottom line will become less dependent solely on the core hospital segment.

An 11% increase in average revenue per inpatient despite stable occupancy indicates a deliberate shift toward more complex clinical cases and specialized surgeries. This improvement in case-mix strengthens the company’s competitive moat against smaller regional players and protects margins against rising medical inflation.

The rising share of private label and generic sales at 15.5% within the pharmacy distribution business points to a structural shift toward higher-margin product categories. This internal mix change is essential for funding the continued expansion of the 7,113-store physical footprint without diluting overall pharmacy returns.

A payor mix where 85% of revenue comes from self-pay and insurance patients provides superior cash flow predictability and shields the business from government pricing pressures. Focusing on high-end specialties like Cardiology and Oncology ensures the brand remains positioned as a high-end provider with significant pricing power.

Massive greenfield expansion in Tier-1 cities signals a pivot from asset-light growth to aggressive land-grab dominance. Investors should expect temporary return-on-capital dilution while these high-cost hubs reach critical occupancy levels.

A firm listing timeline indicates management’s commitment to stripping away the conglomerate discount from the core hospital business. Pure-play status will likely unlock higher valuation multiples for the fast-growing digital health and pharmacy divisions.

The complex web of subsidiaries and regional joint ventures reveals a capital-efficient expansion strategy that relies on local partnerships in key growth markets. Investors must monitor the share of profits attributable to minority interests as these regional hubs increasingly contribute to the total earnings mix.

Automobiles

Mahindra & Mahindra Ltd. | Large Cap | Auto Manufacturers

Mahindra & Mahindra is a leading Indian conglomerate with a dominant presence in the SUV and tractor segments. The company operates a diverse portfolio including financial services, information technology, logistics, and real estate through its various subsidiaries.

The divergence between operating PAT and reported figures across business units reveals that internal efficiency gains are currently being masked by specific non-recurring impairments. For investors, this suggests that earnings quality is improving and future quarters may see a sharp headline recovery as these one-time costs dissipate.

Logistics hitting profitability marks the transition of secondary investments from cash burners to self-sustaining assets. Diversifying income through real estate and services provides a critical hedge against the volatile automotive business cycle.

Maintaining a significantly higher revenue market share compared to volume share indicates a successful mix shift toward more expensive, premium SUV models. This trend suggests strong pricing power and brand desirability, which should lead to more resilient earnings compared to volume-led competitors.

Achieving positive EBITDA at the electric vehicle subsidiary (MEAL) during the early ramp-up phase marks a critical inflection point for unit economics. It demonstrates that the new EV platform can be financially viable at lower volumes, reducing the risk of permanent margin dilution during the multi-year technology shift.

Outpacing industry growth in the truck and bus segment indicates a successful scale-up of commercial operations beyond their traditional core. Higher volumes in these heavy categories improve operational efficiency and provide a broader base for long-term service-led revenue.

Sustaining 20% margins through industry downturns reveals structural pricing power that competitors cannot easily disrupt. This operational resilience de-risks the stock against rural economic shocks and provides capital for aggressive EV expansion.

The automotive division has emerged as the primary earnings engine, offsetting relatively stagnant growth in the core farm equipment segment. While the services spike appears large, much of that boost stems from one-off gains and investment income rather than recurring operations.

Financial Services

Muthoot Finance Limited | Large Cap | Financial Services

Muthoot Finance is India’s largest gold loan NBFC providing credit secured by gold jewelry across a vast branch network. The company also operates diversified subsidiaries in housing finance, microfinance, and insurance brokerage to broaden its financial service offerings.

Profit growth outpacing loan expansion reveals superior pricing power and the ability to extract high margins from a fixed network. This efficiency allows the company to fund aggressive branch expansion using internal cash rather than taking on expensive new debt.

The explosive 168% growth in vehicle finance contrasted with a decline in microfinance AUM reveals a deliberate strategic shift toward asset-backed lending. While this rebalancing diversifies the book, it also introduces different credit risk profiles that require a move away from the simple gold-only underwriting model.

Significant losses in the microfinance subsidiary during a record-breaking period for the parent company highlight the stark performance gap between secured and unsecured portfolios. This divergence reinforces the view that gold loans remain the group’s primary engine of stability and high-quality earnings compared to other segments.

Profit after tax grew by 91% while interest income rose 57%, a divergence primarily driven by a sharp 58% reduction in impairment costs. This suggests current earnings quality is heavily influenced by credit cost moderation, which may be a cyclical rather than permanent tailwind.

Muthoot is folding its underperforming vehicle loan business into its core gold-backed model to stop persistent credit leakage. This retreat signals a strategic priority on capital safety over pursuing high-risk growth in specialized lending markets.

Muthoot Money has achieved a massive turnaround, growing AUM by over 100% year-on-year while simultaneously slashing the Stage III ratio from 1.37% to 0.60%. This scale-up indicates that the subsidiary is now a meaningful contributor to group profitability and has successfully stabilized its credit underwriting processes.

A significant contraction in premium collections and policy volumes within the insurance brokerage unit points to a major shift in distribution strategy or a loss of momentum in third-party product sales. The resulting swing from profit to a marginal loss in this segment underscores the difficulty of scaling capital-light fee businesses compared to the core lending book.

That’s it for now! Your feedback will really help shape how Points and Figures evolves. Drop it down in the comments below!

Quotes in this newsletter were curated by Meher, Vignesh & Kashish.

Disclaimer: We’ve used AI tools in filtering and cleaning up the quotes from the images so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Points and Figures is run by the same team that creates The Daily Brief and Aftermarket Report.