Sometimes, a single slide can explain more than a long report. Points and Figures is our way of breaking down what India’s leading companies are telling their shareholders and analysts. We comb through the decks, pull out the charts and data points that actually matter, and highlight the signals behind the numbers—whether about growth plans, margins, new markets, or risks on the horizon.

This is an extension of The Chatter. While The Chatter focuses on management commentary and earnings call transcripts, Points and Figures dives into investor presentations—and soon, even annual reports—to decode what companies are showing, not just what they’re saying.

We go through every major investor presentation so you don’t have to—bringing you the sharpest takeaways that reveal not just what the company is saying, but what it really means for the business, its sector, and the broader economy.

In this edition, we have covered 13 companies across 12 industries.

Healthcare

CORONA Remedies

Software Services

Coforge

Energy

Smarten Power Systems

FMCG

Devyani International

Sharat Industries

Chemicals

Responsive Industries

Auto Ancillary

Shigan Quantum Technologies

Engineering & Capital Goods

KSH International

Metals

Vibhor Steel Tubes

Retail

Logica Infoway Ltd.

Agriculture

Narmada Agrobase

Textiles

Monte Carlo Fashions

Financial Services

Emkay Global Financial Services Ltd.

Healthcare

CORONA Remedies | Small Cap | Healthcare

CORONA Remedies Ltd. develops, manufactures, and markets prescription and OTC medicines across therapeutic areas including cardiology, diabetology, gastroenterology, dermatology, respiratory care, neurology, pain management, and nutraceuticals.

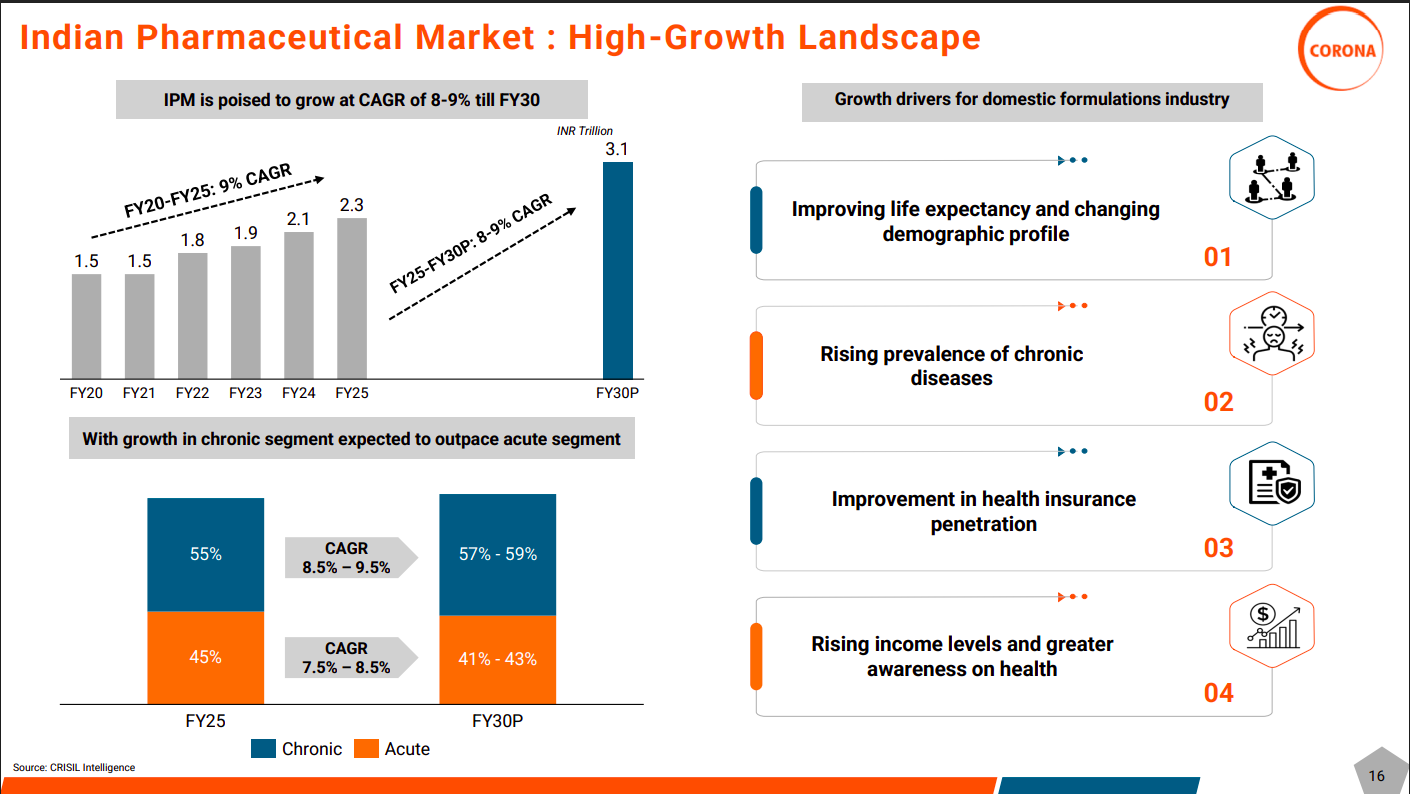

The Indian Pharmaceutical Market is expected to grow at 8–9% CAGR till FY30, led by chronic therapies outpacing acute segments. Structural drivers include rising life expectancy, higher chronic disease prevalence, better insurance penetration, and increasing health awareness.

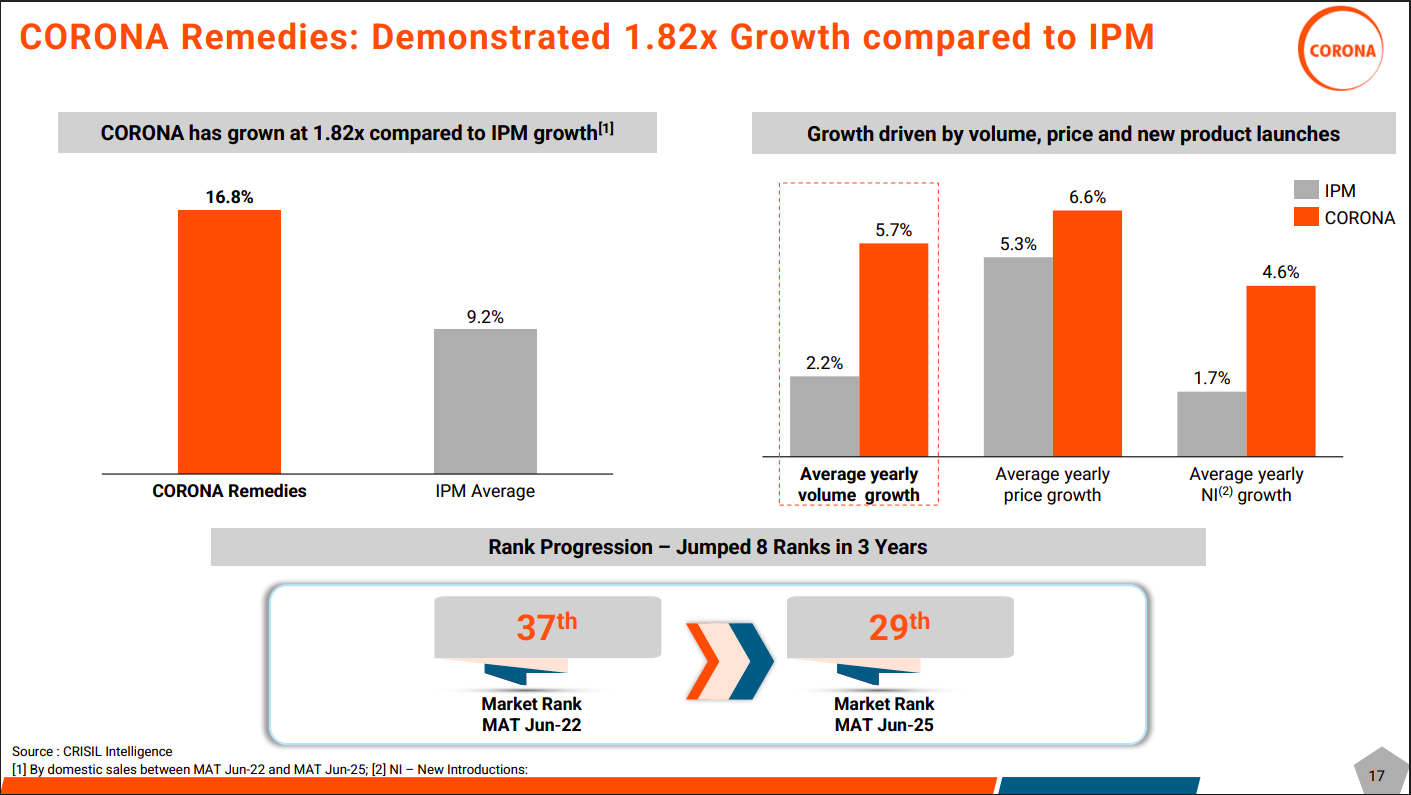

Corona Remedies has delivered 1.82× faster growth than the IPM average, driven by superior volume growth, pricing, and new product launches. Its market rank improved sharply from 37th to 29th over three years, reflecting consistent execution and portfolio strength.

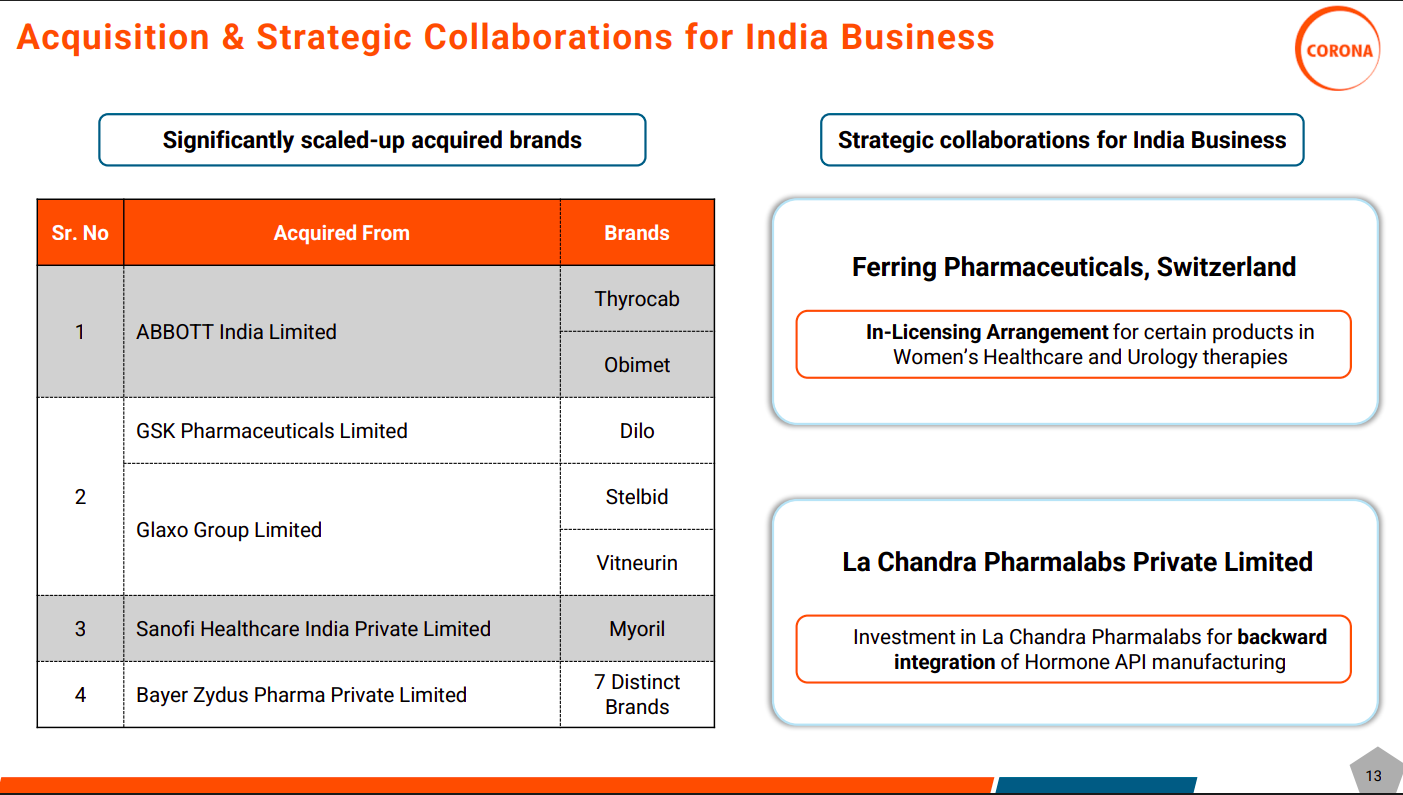

Corona Remedies has successfully scaled multiple acquired brands from Abbott, GSK/Glaxo, Sanofi, and Bayer Zydus, strengthening its domestic portfolio. Strategic partnerships with Ferring Pharma and La Chandra Pharmalabs enhance specialty presence and enable backward integration in hormone APIs.

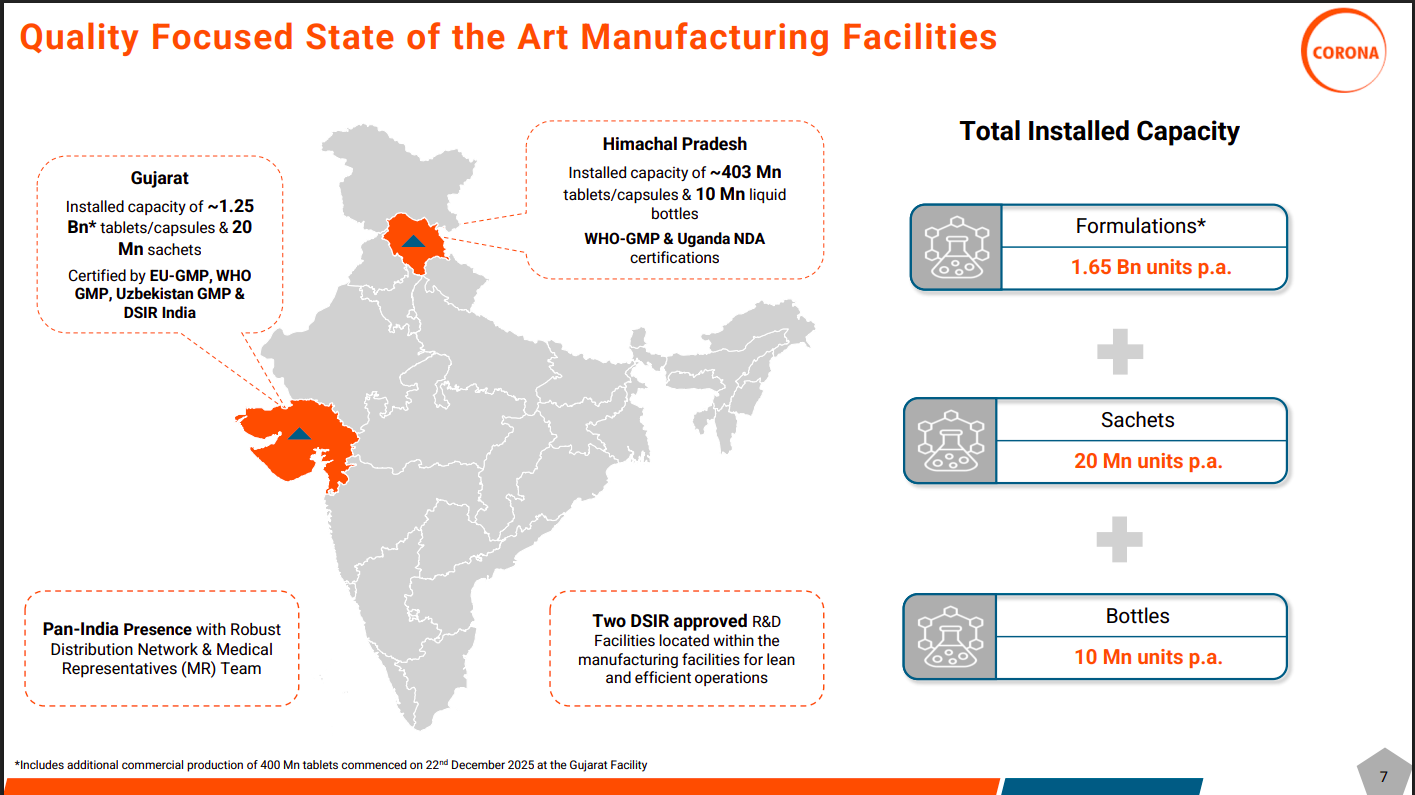

Corona operates state-of-the-art manufacturing facilities in Gujarat and Himachal Pradesh with strong global regulatory approvals (EU-GMP, WHO-GMP). The company has a total installed capacity of ~1.65 bn formulation units annually, supported by in-house R&D and a pan-India distribution network.

Software Services

Coforge | Mid cap | Software Services

Coforge provides IT/ITES solutions globally, specializing in Application Development & Maintenance, Managed Services, Cloud Computing, and Business Process Outsourcing. It serves sectors like Financial Services, Insurance, Travel, Transportation & Logistics, Manufacturing & Distribution, and Government, delivering tailored technology solutions to enhance business operations.

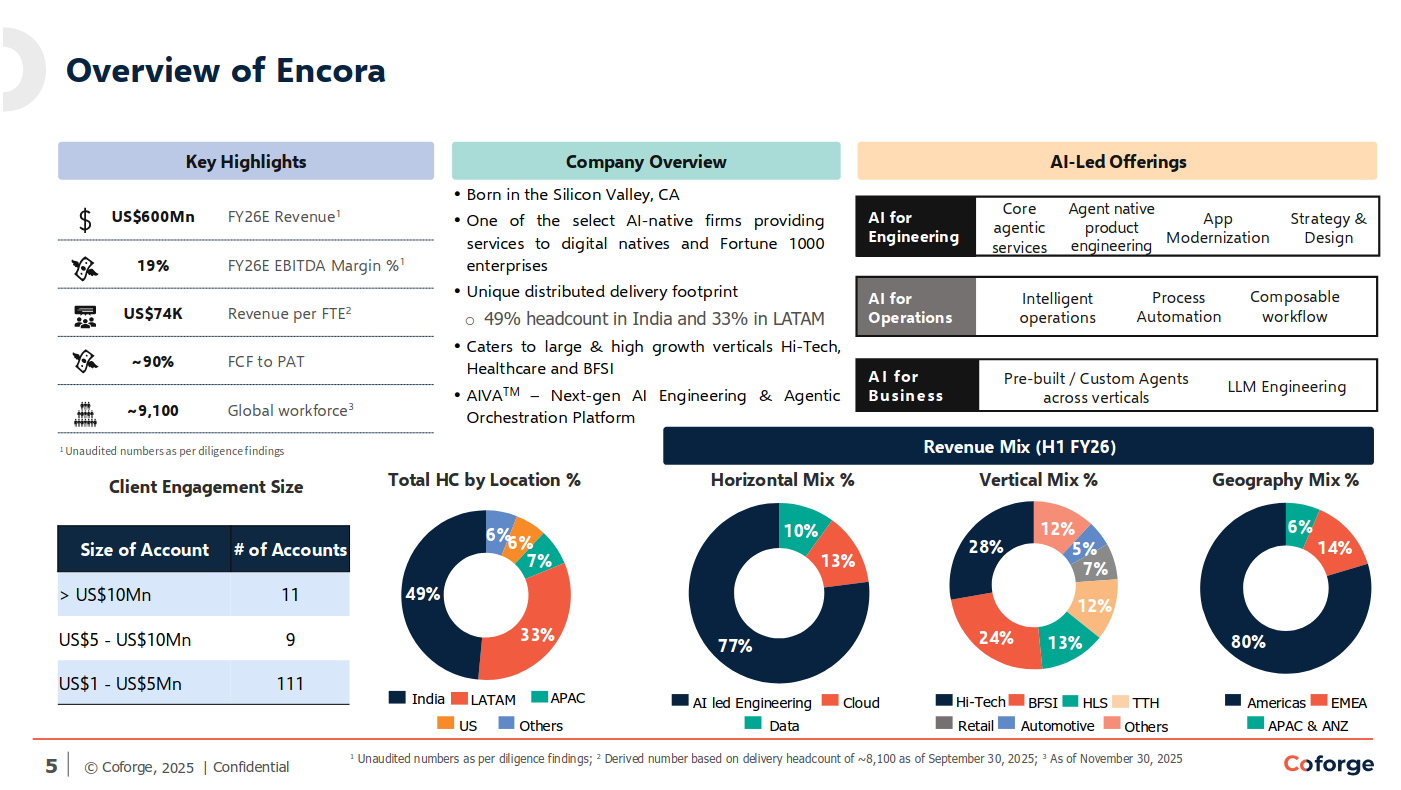

Encora is a Silicon Valley–born, AI-native digital engineering firm with ~US$600 mn FY26E revenue and ~19% EBITDA margins, focused on large digital-native and Fortune 1000 clients. Its AI-led offerings span engineering, operations, and business use cases, with a diversified mix across verticals, geographies, and long-tenure client relationships.

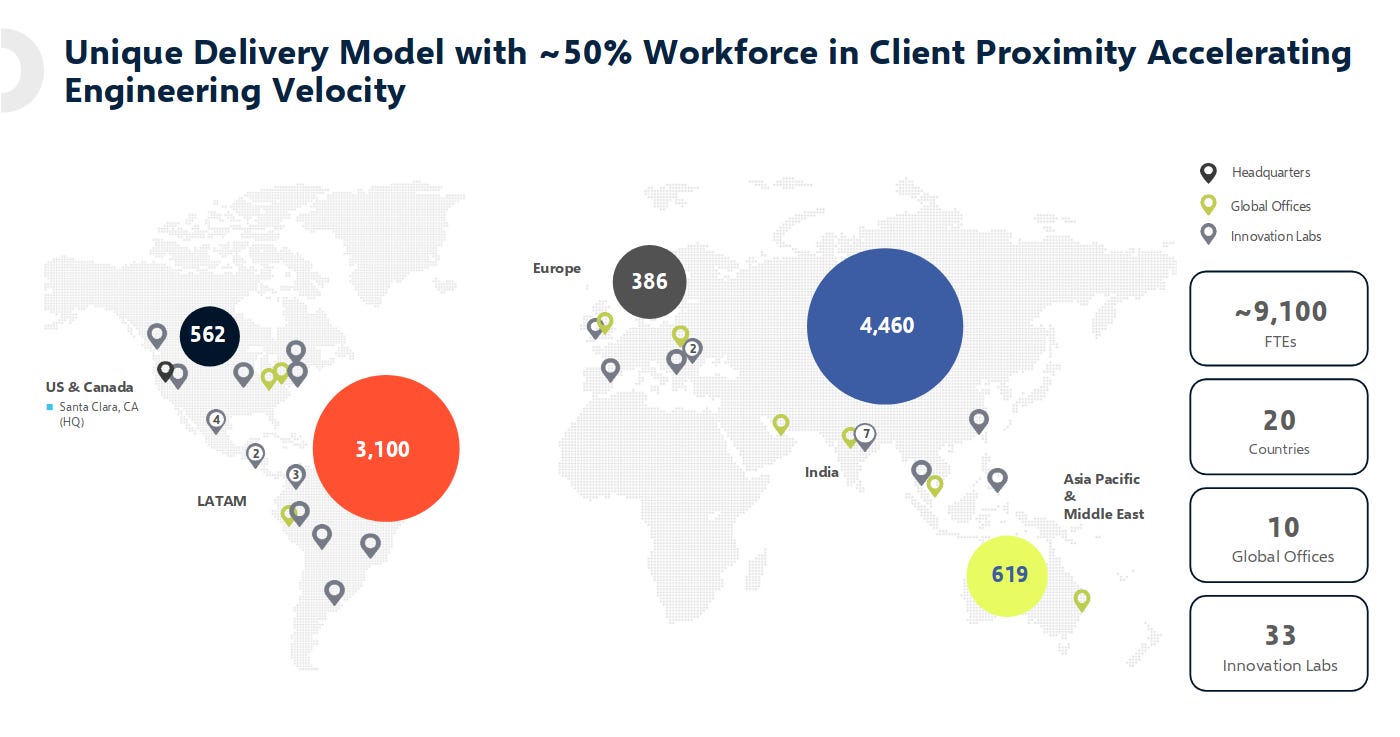

Encora operates a globally distributed delivery model with ~50% of its workforce located close to clients, accelerating engineering speed and collaboration. With ~9,100 FTEs across 20 countries, 10 global offices, and 33 innovation labs, India remains the largest talent base, complemented by strong presence in LATAM, Europe, and APAC.

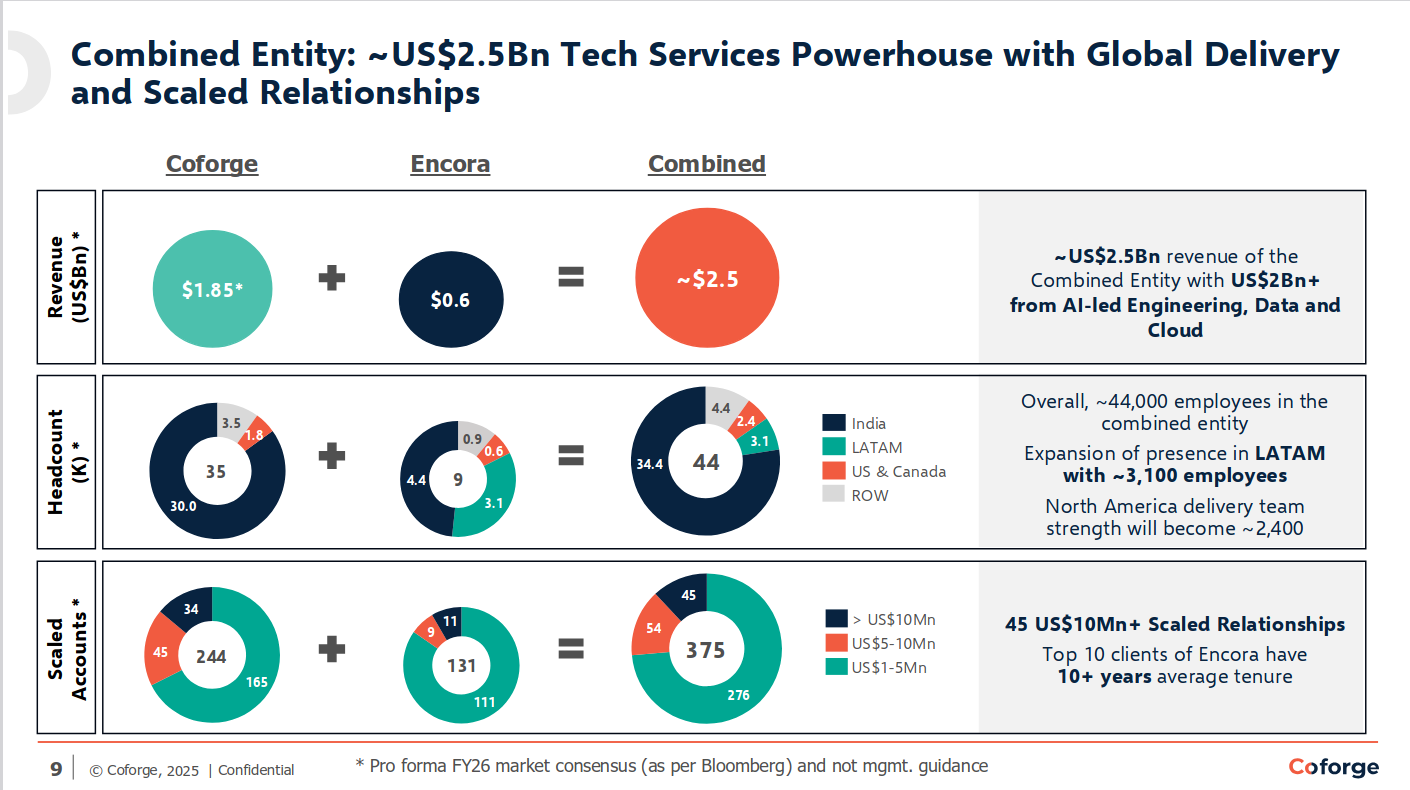

The combined Coforge–Encora platform creates a ~US$2.5 bn tech services powerhouse with ~44,000 employees and deep global delivery scale. The merger strengthens AI-led engineering, data, and cloud capabilities, expands LATAM and North America presence, and builds a larger base of $10 mn+ long-term client relationships.

Energy

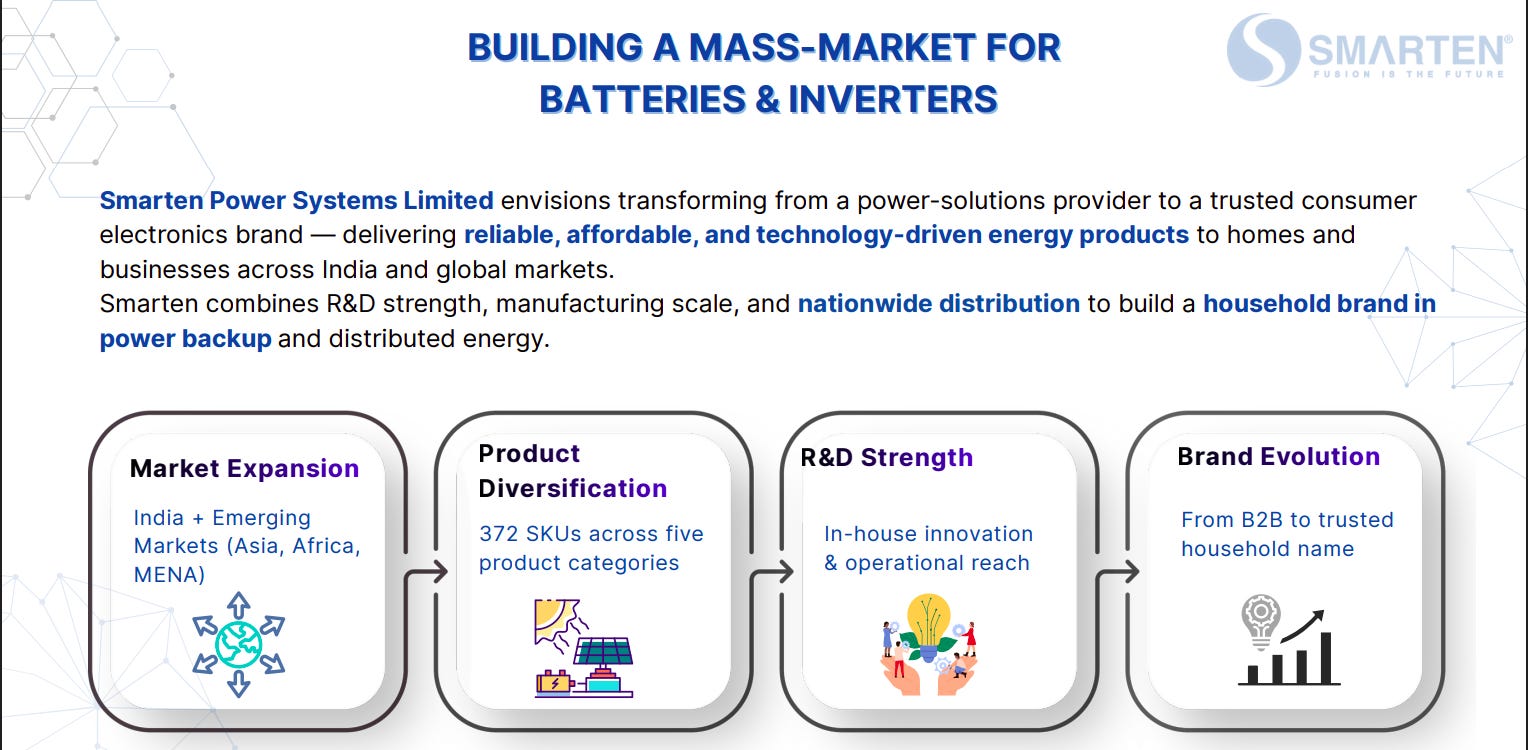

Smarten Power Systems | Nano cap | Energy

Smarten Power Systems Ltd designs and assembles power backup and solar products like home UPS, inverters, PCUs, and charge controllers. It also trade solar panels and batteries, sell via distributors in India, and export all products except solar panels.

Smarten is transitioning from a B2B power-solutions player to a trusted consumer brand in energy products. The strategy hinges on nationwide distribution, strong in-house R&D, a wide product range, and expansion across India and emerging markets.

The addressable market across inverters, solar charge controllers, solar PCUs, and lead-acid batteries is large and steadily expanding through 2032. Batteries stand out as the fastest-growing segment, while solar-linked products benefit from rising renewable adoption.

Smarten offers an integrated portfolio spanning UPS/inverters, solar charge controllers, solar PCUs, batteries, and solar panels. The range is designed for reliable power backup, efficient solar utilization, and scalable residential to rooftop applications.

FMCG

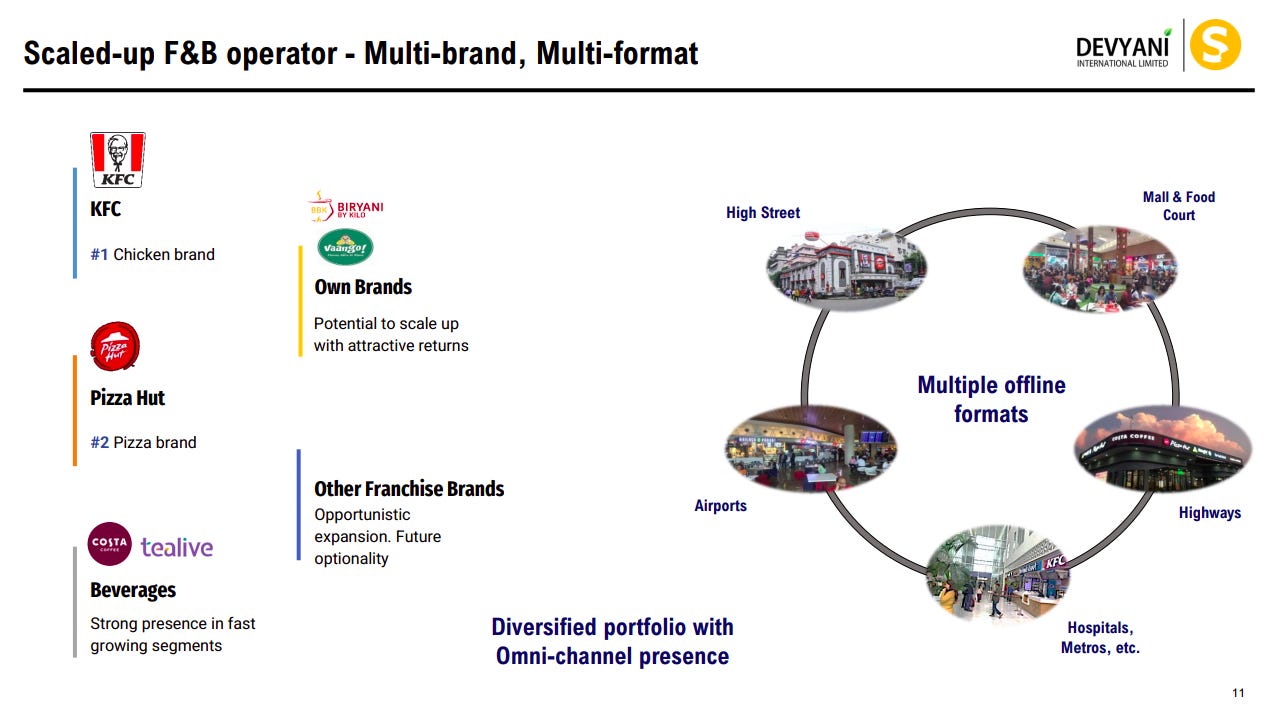

Devyani Internatl.| Small cap | FMCG

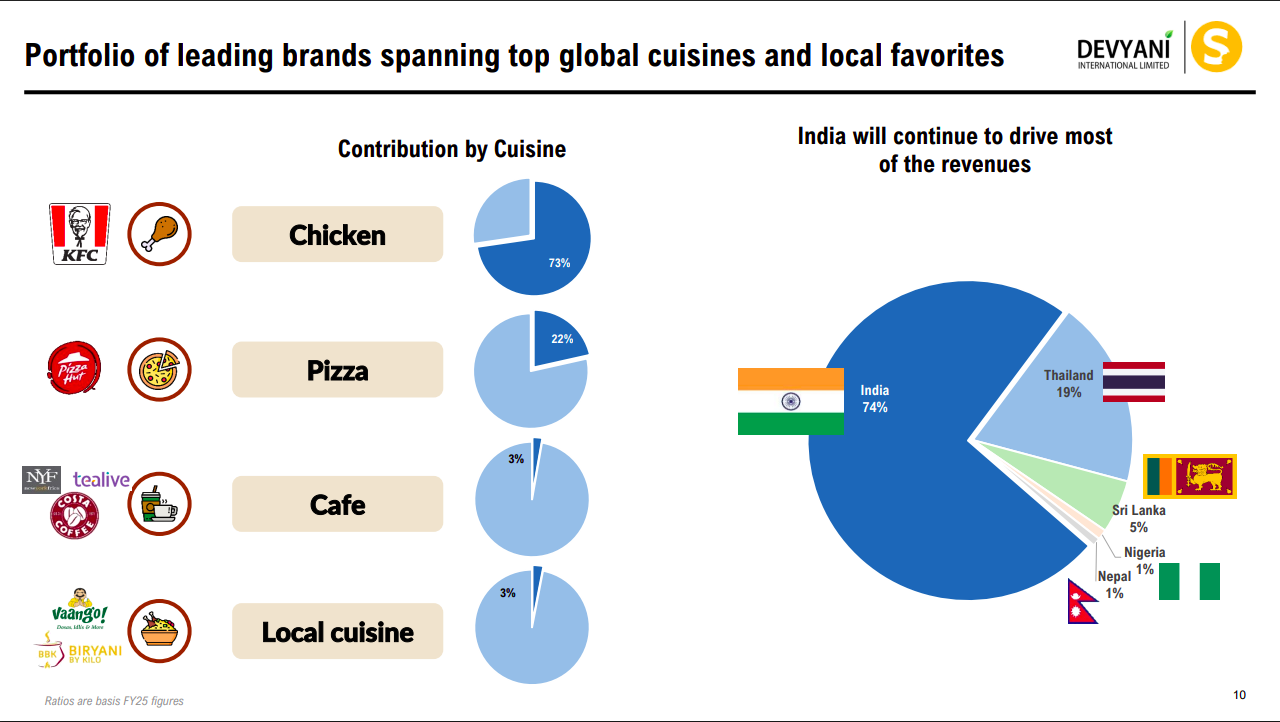

Devyani International Limited is the largest franchisee of Yum Brands in India, operating KFC, Pizza Hut, and Costa Coffee stores in the country as well as in Nepal and Nigeria. They also have their own brands like Vaango and Food Street, making them a major player in the food and beverage industry in India.

Devyani operates a diversified QSR portfolio led by KFC (#1 chicken) and Pizza Hut (#2 pizza), complemented by beverages and owned brands. The company runs multiple offline formats—high street, malls, airports, highways, hospitals—creating a strong omni-channel presence.

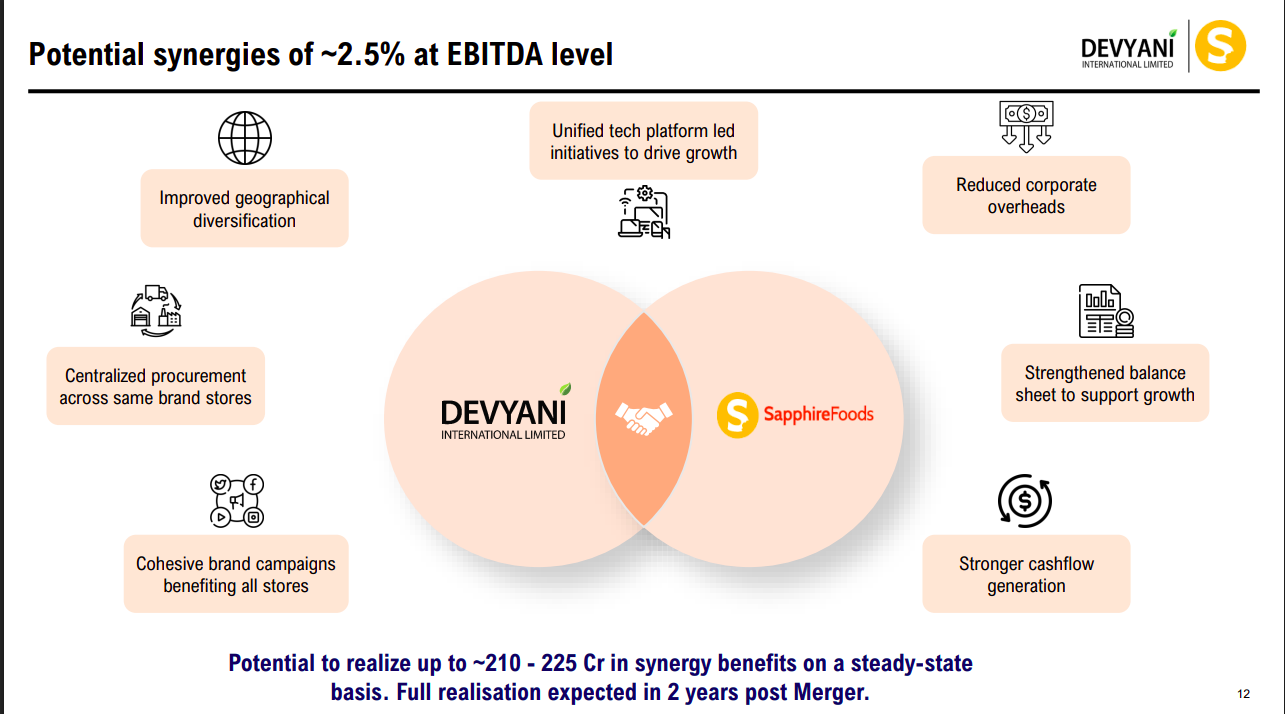

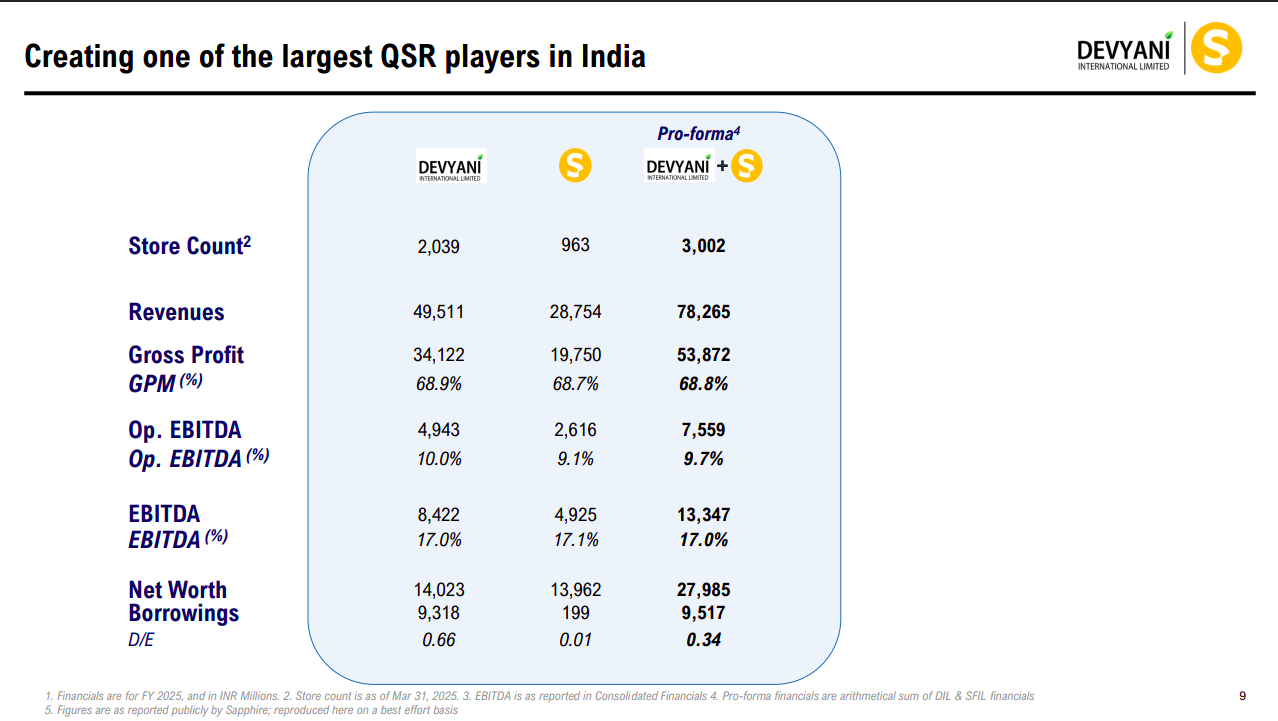

The Devyani–Sapphire Foods merger unlocks ~2.5% EBITDA synergies via centralized procurement, unified tech platforms, and reduced overheads.Steady-state synergy benefits of ₹210–225 Cr are expected within two years, alongside stronger cash flows and balance-sheet resilience.

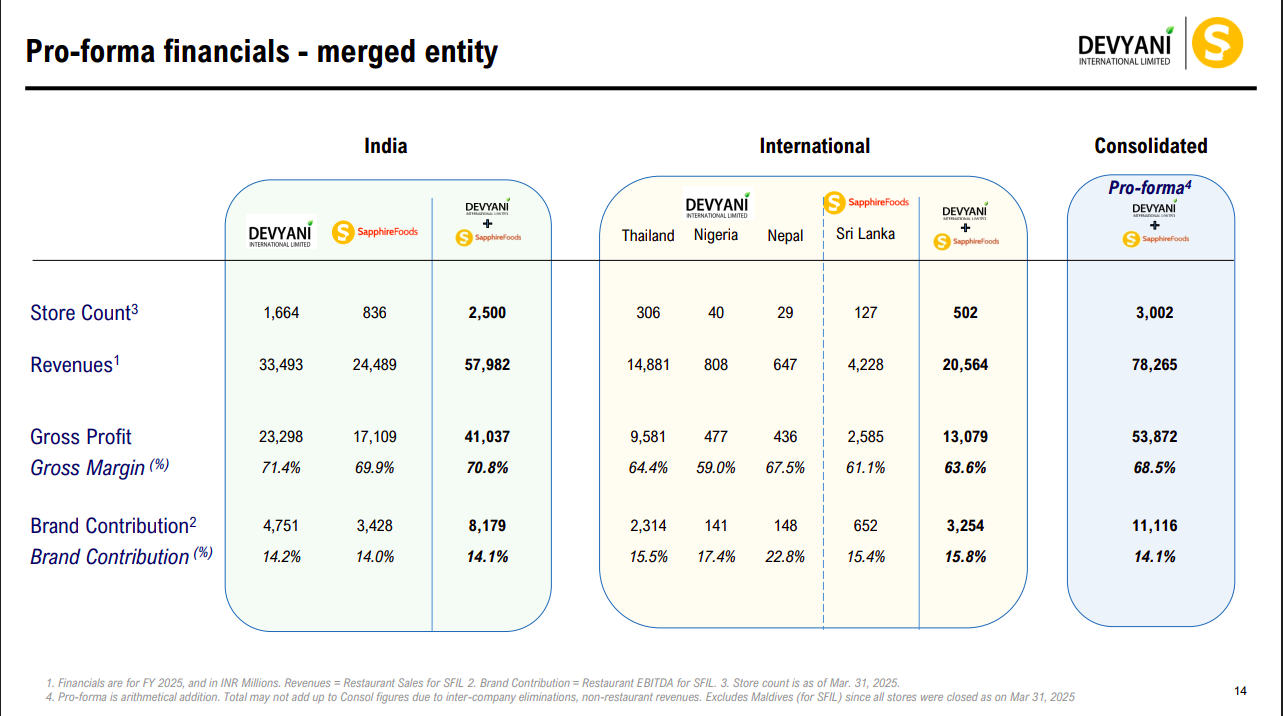

Post-merger, the combined entity operates ~3,002 stores with revenues of ₹78,265 Cr and EBITDA margins near 17%. India remains the profit engine, while international operations add scale and geographic diversification.

Chicken dominates the cuisine mix (~73%), followed by pizza, with cafés and local cuisine contributing smaller but growing shares. India contributes ~74% of revenues, with Thailand and Sri Lanka as key overseas markets.

The merged platform forms one of India’s largest QSR operators with strong gross margins (~69%) and EBITDA of ₹13,347 Cr.

Improved leverage (D/E ~0.34) and scale enhance profitability, expansion capacity, and long-term competitive positioning.

Sharat Industries | Micro cap | FMCG

Sharat Industries Ltd was incorporated on 7 May ‘90 and became public in 1992. They were engaged in acquaculture, the company’s products are processed prawn, quality hatched seed and feed. They were started with the objective of setting up an integrated aquaculture project consisting of a Hatchery, Feed mill, Grow-out Farm and Processing Plant which will produce Individually Quick Frozen (IQF) and other value added products.

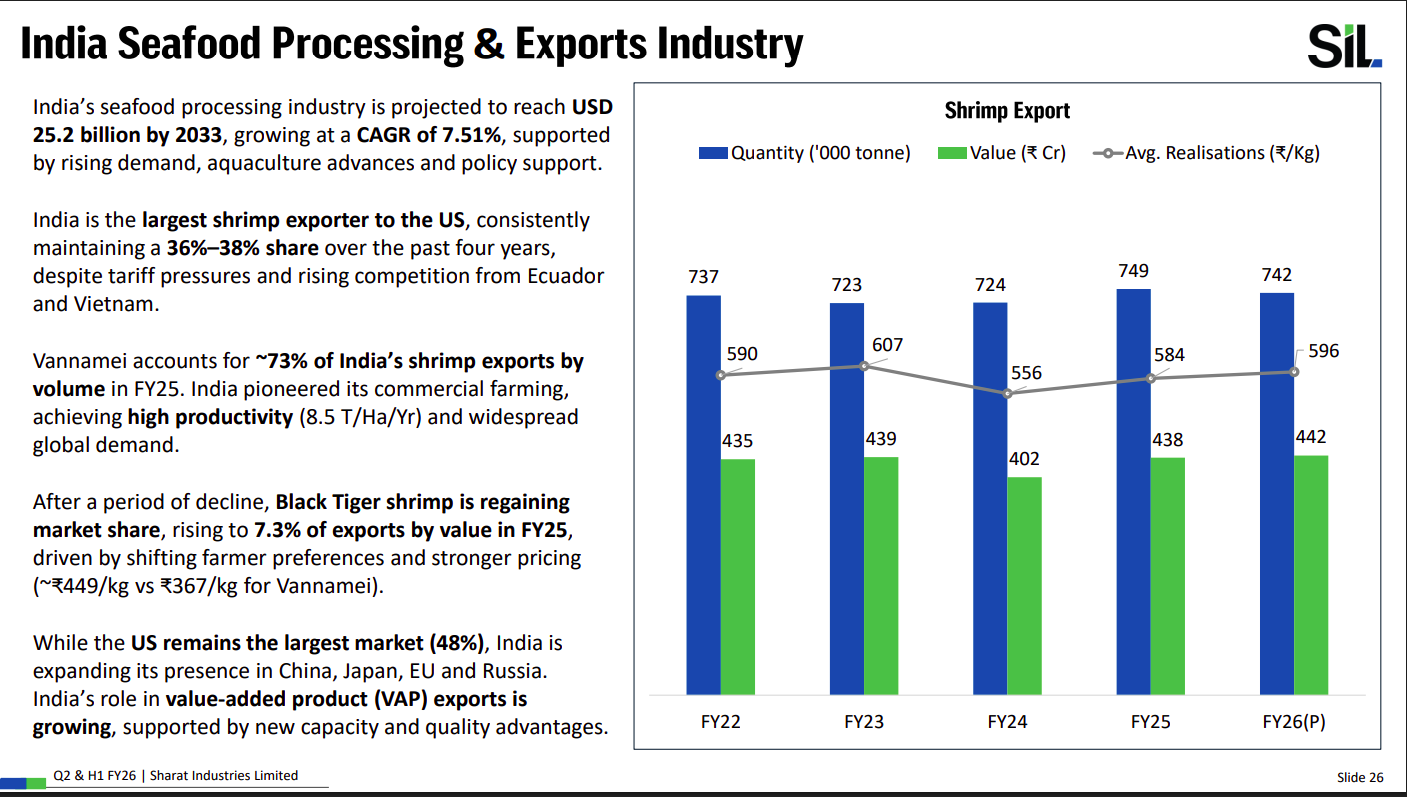

India’s seafood processing industry is set to reach USD 25.2 billion by 2033 at a 7.5% CAGR, driven by aquaculture growth and policy support. India remains the largest shrimp exporter to the US, with Vannamei dominating volumes and Black Tiger shrimp gaining value share. Export diversification and rising value-added products support long-term growth.

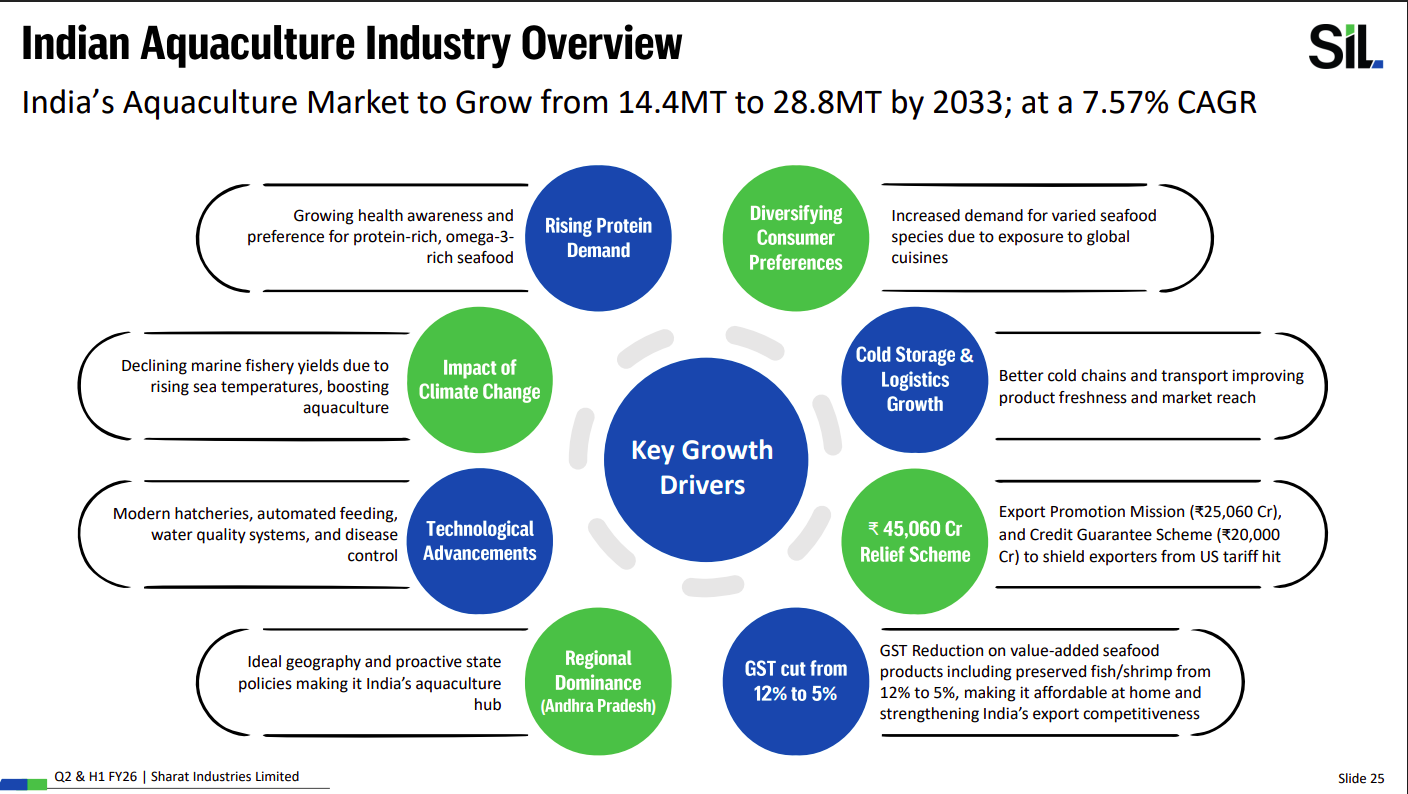

India’s aquaculture market is expected to double from 14.4 MT to 28.8 MT by 2033, growing at a 7.57% CAGR. Growth is driven by rising protein demand, technological advancements, cold-chain expansion, and supportive policies like GST cuts and export incentives. Andhra Pradesh remains a key regional hub.

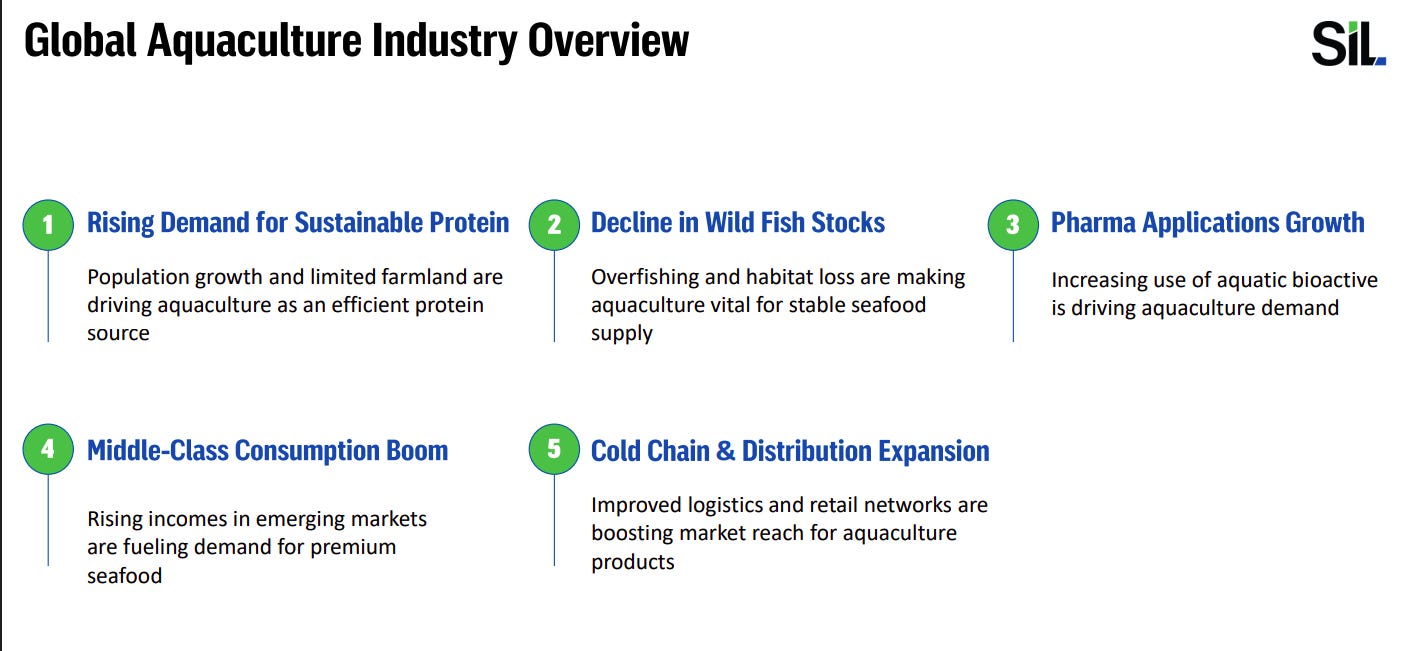

Global aquaculture demand is rising due to sustainable protein needs, declining wild fish stocks, and growing middle-class consumption. Expansion in cold-chain logistics and new pharma applications of aquatic bioactives are further boosting demand. Aquaculture is becoming critical for global seafood supply stability.

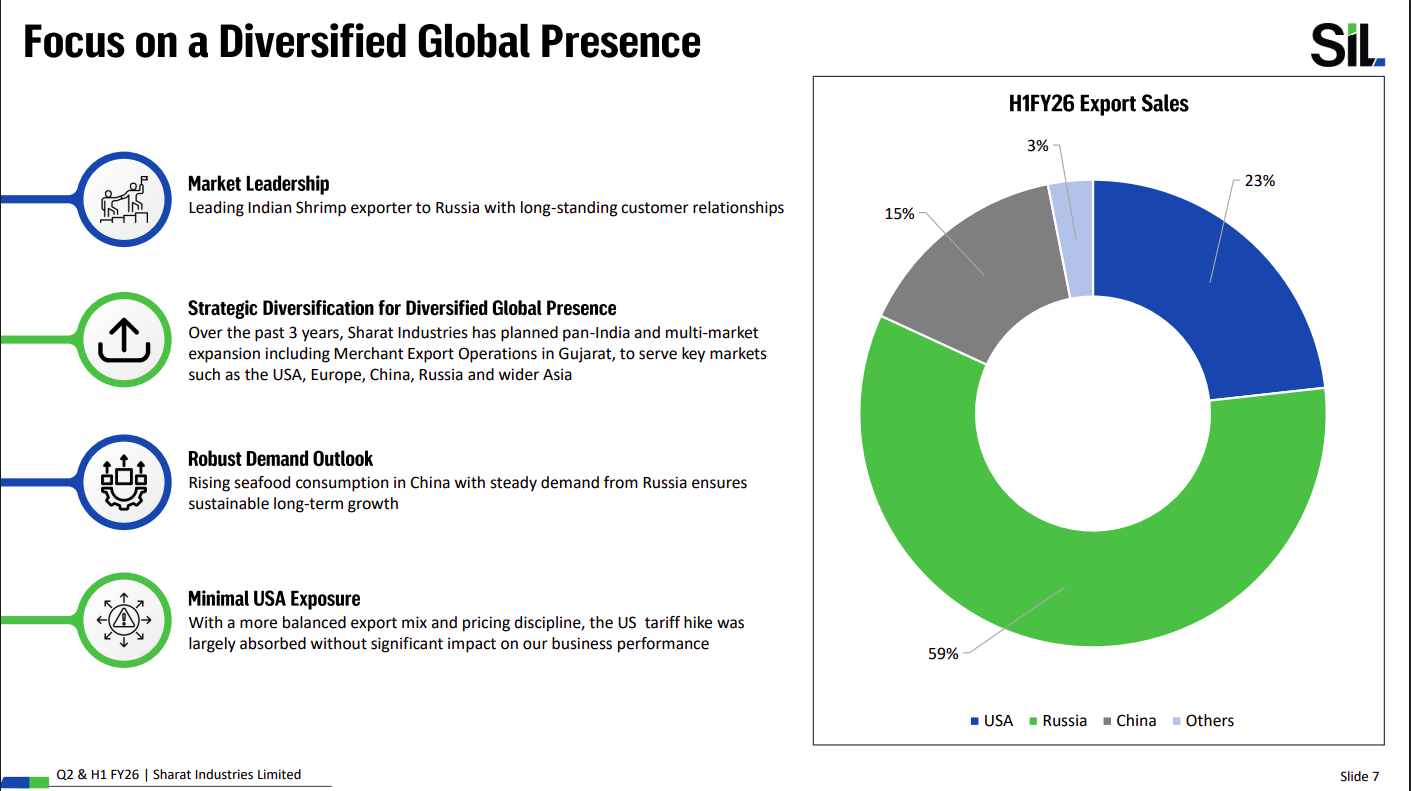

The company has built a diversified export footprint with strong positions in Russia, China, and Asia, reducing dependence on the US market. Russia leads the export mix, while pricing discipline has helped absorb US tariff pressures. This balanced geography supports stable, long-term growth.

Chemicals

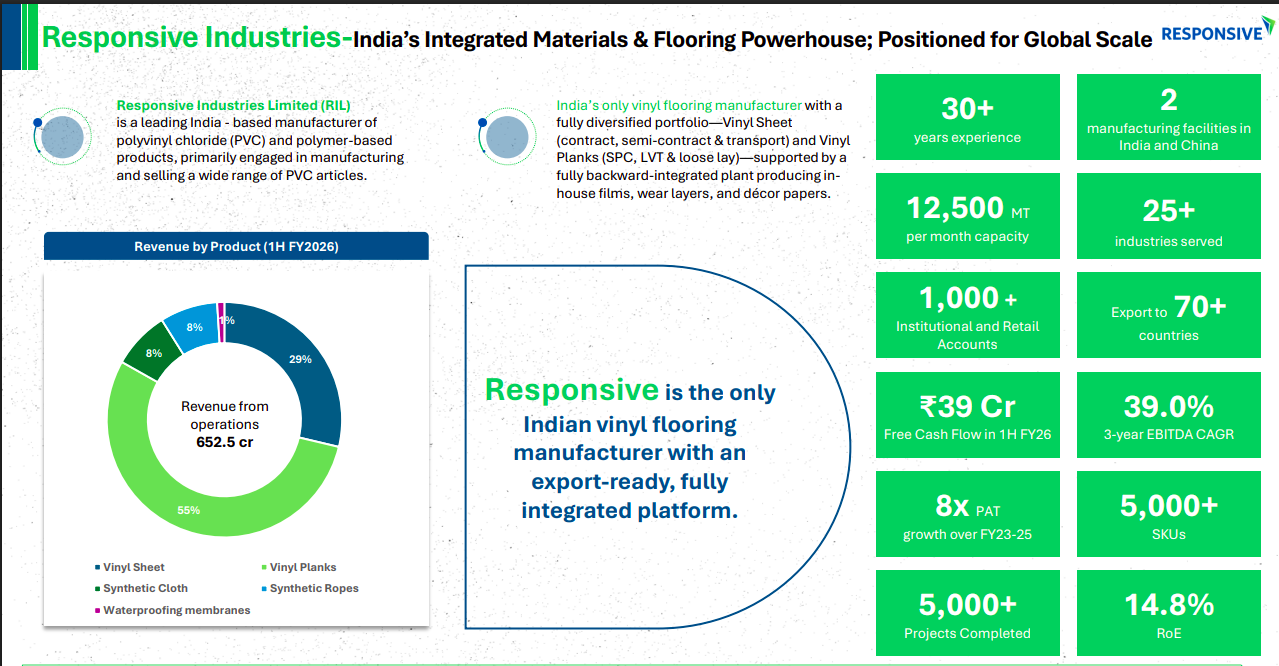

Responsive Industries |Small cap | Chemicals

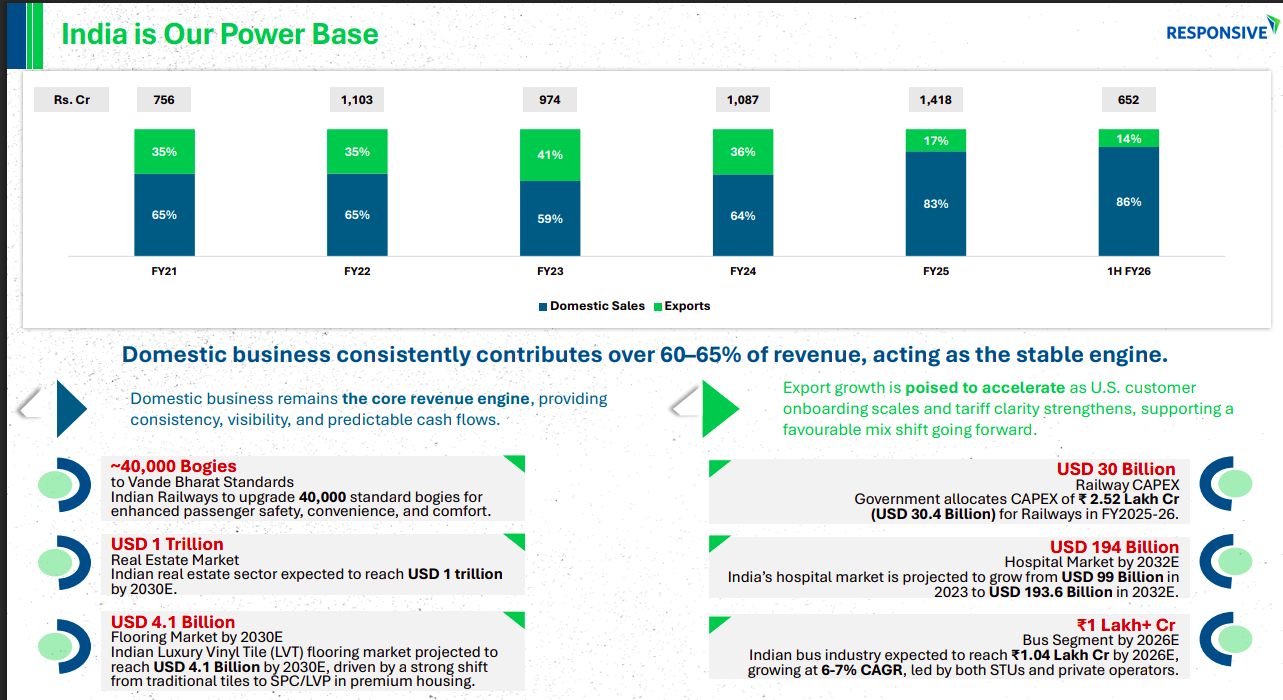

Responsive Industries Limited is a leading manufacturer of PVC Products. It serves as the undisputed standard for PVC products that are all in line with EU/US certifications.

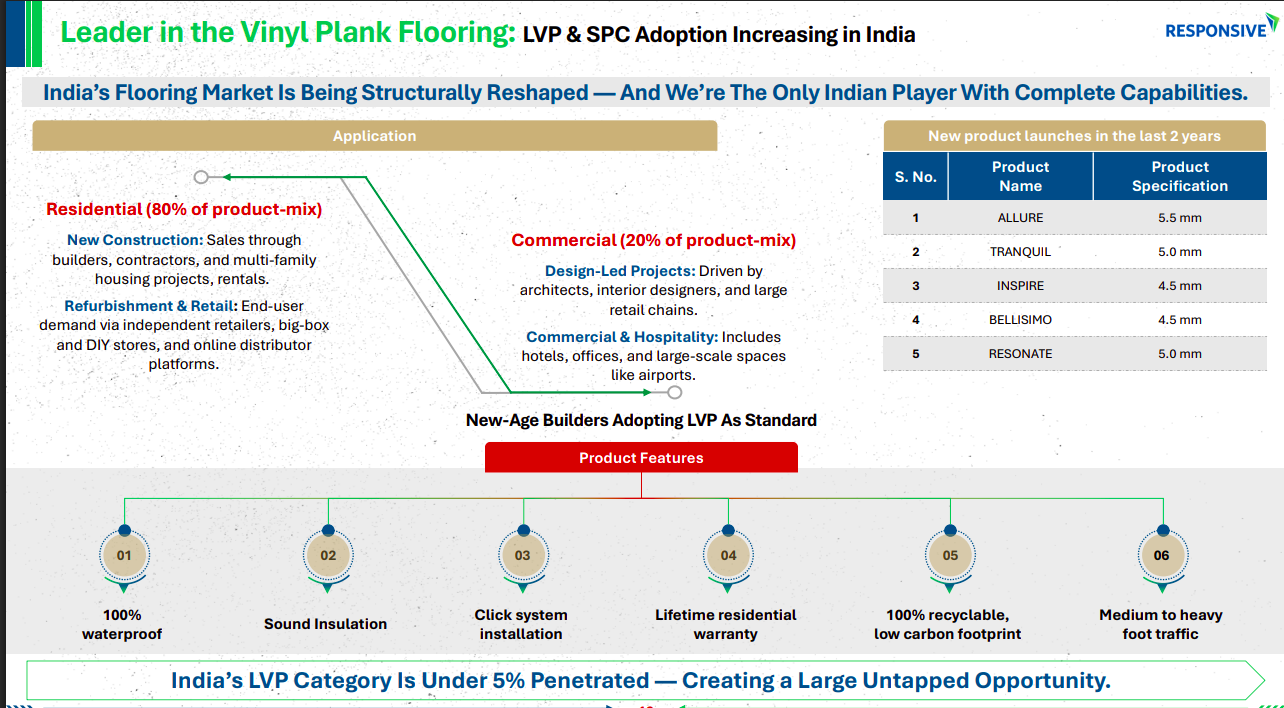

India’s flooring market is structurally shifting toward LVP/SPC, led by residential demand (~80%) with growing commercial adoption. Low penetration (<5%) creates a large runway, supported by waterproofing, easy installation, recyclability, and strong new product launches.

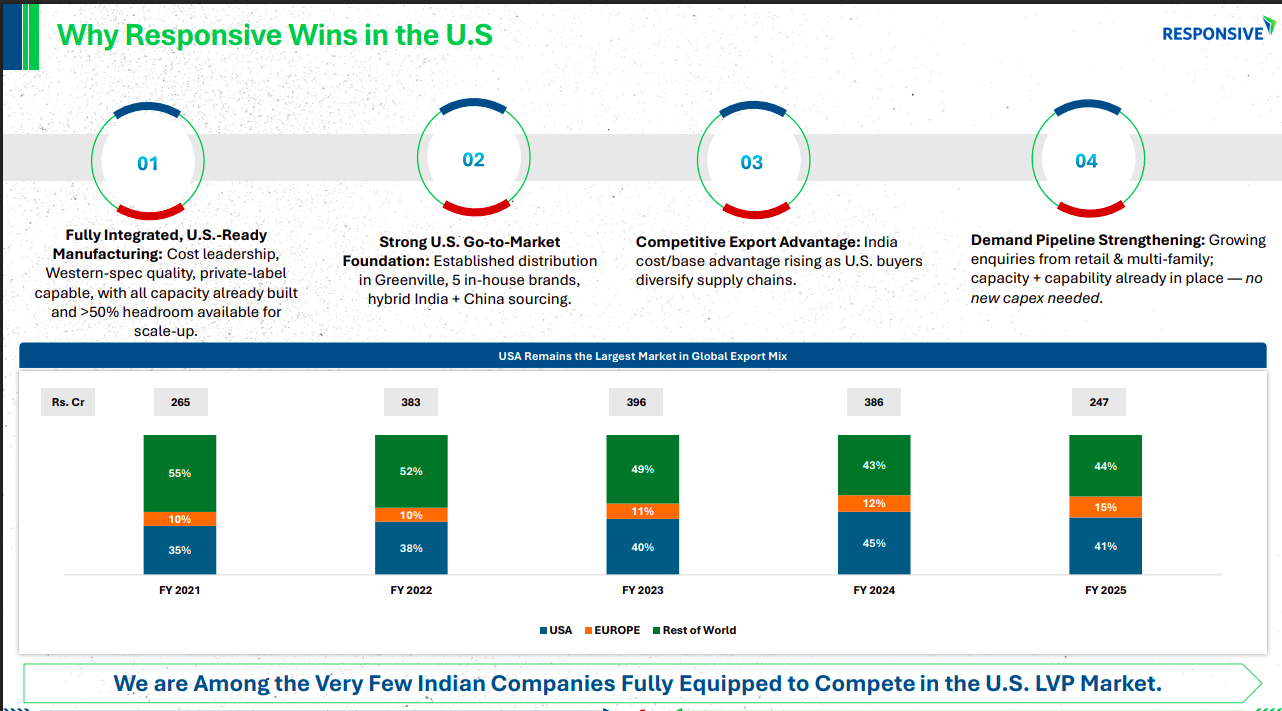

The $10B+ U.S. LVP market is dominated by Vietnam and China (~84% of imports), while India remains under 1%, creating a clear export opportunity. Responsive is India’s only scaled, export-ready manufacturer, with ₹247 crore exports in FY25 and active U.S. customer discussions.

Responsive combines fully integrated, U.S.-ready manufacturing with strong distribution, cost advantages, and an established export base. With capacity already in place, demand is scaling without incremental capex, and the U.S. remains the largest export market.

Domestic sales contribute over 60–65% of revenue, providing stability and predictable cash flows. Multiple domestic tailwinds—real estate, railways, hospitals, buses, and flooring—support sustained growth, while exports are set to accelerate.

Responsive is India’s only fully integrated vinyl flooring player with a diversified product mix and global scale. Strong operating metrics—global exports, high EBITDA CAGR, robust cash flows, and large installed capacity—position the company for sustained domestic and international growth.

Auto Ancillary

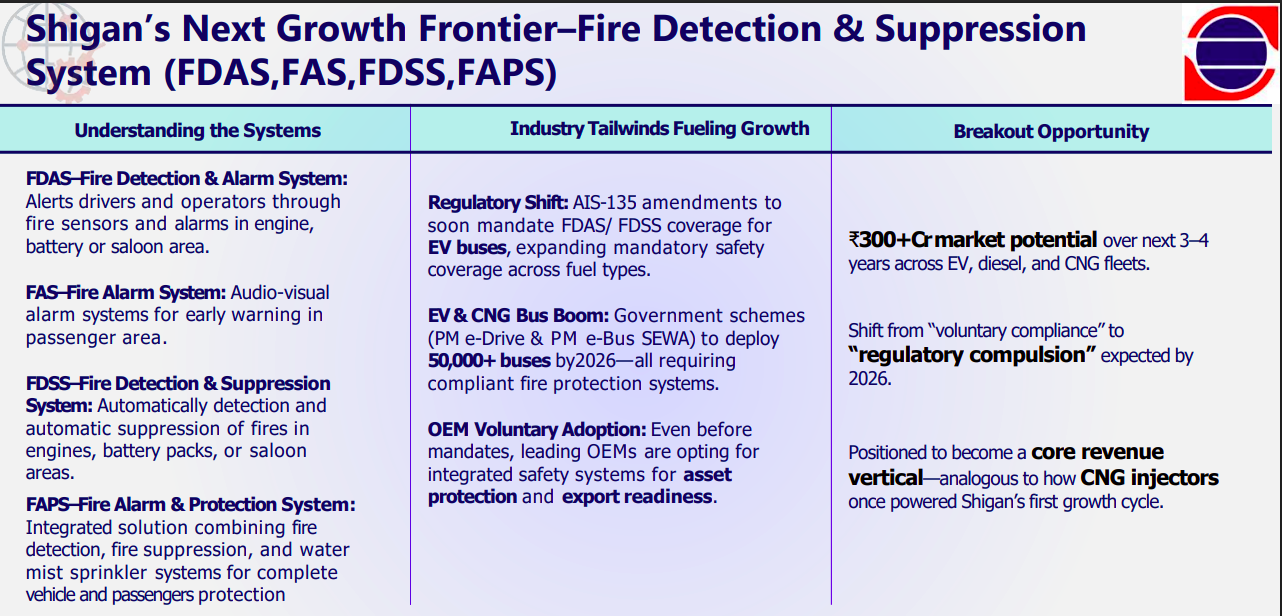

Shigan Quantum Technologies | Nano Cap | Auto Ancillary

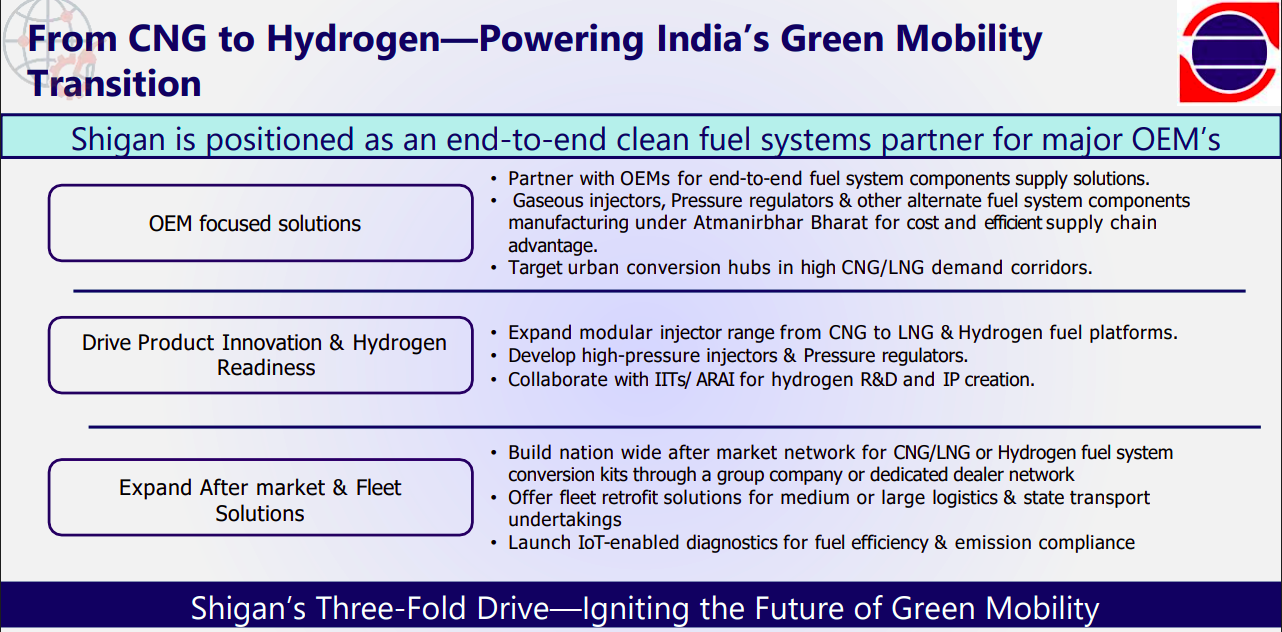

Shigan Quantum Technologies Limited specializes in designing, developing, and exporting LNG, CNG, and Hydrogen Fuel Kit Systems for various vehicles and industrial applications. Since April 2020, the company has also branched out into manufacturing Fire Detection & Alarm systems. It caters to both high duty and light-duty vehicles, power generation equipment, industrial machinery, and off-highway applications, exporting CNG fuel systems to several countries worldwide.

Shigan is positioning itself as an end-to-end clean fuel systems partner for OEMs, spanning CNG, LNG, and hydrogen platforms. Its strategy combines OEM-focused components, hydrogen-ready product innovation, and a nationwide aftermarket and fleet retrofit network to support India’s green mobility shift.

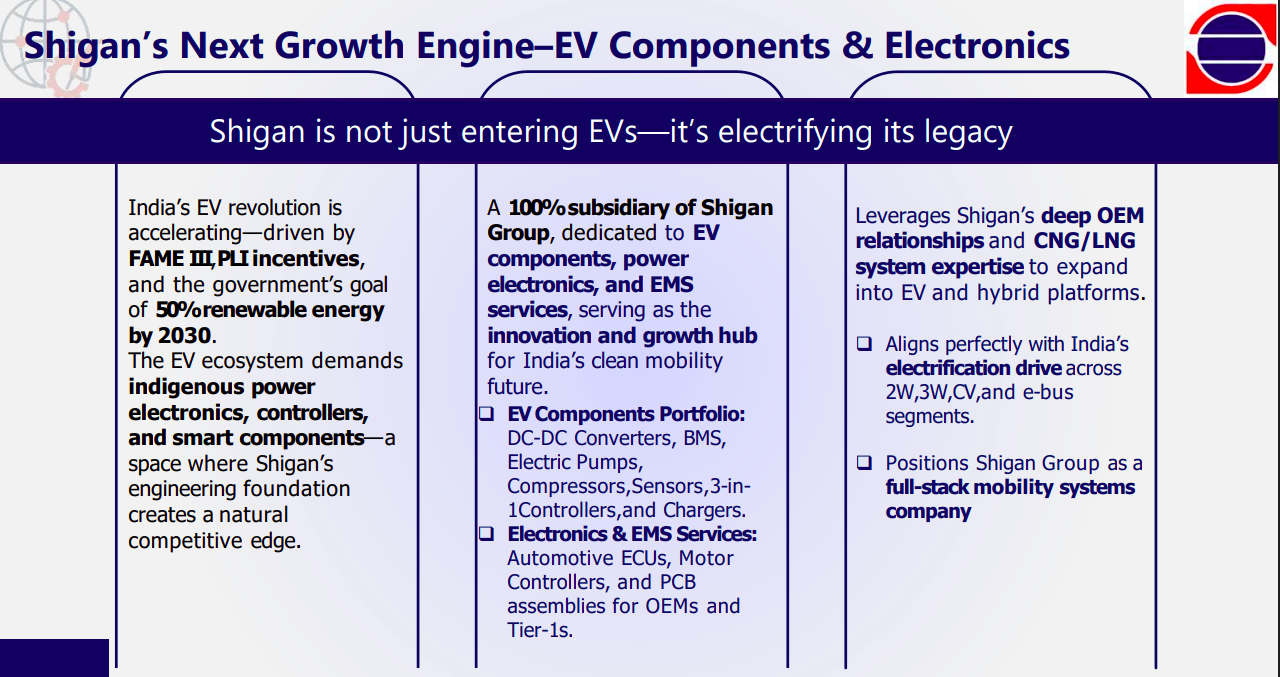

Shigan is leveraging its deep OEM relationships and fuel-system expertise to expand into EV components, power electronics, and EMS through a dedicated subsidiary. This move aligns with India’s EV push and positions the group as a full-stack mobility systems player across 2W, 3W, CVs, and e-buses.

Regulatory changes and rapid EV/CNG bus adoption are creating a large, mandatory market for onboard fire detection and suppression systems. With a ₹300+ crore opportunity emerging over the next 3–4 years, this vertical is poised to become a core revenue engine, similar to Shigan’s early CNG injector cycle.

Engineering & Capital Goods

KSH International | Small Cap | Engineering & Capital Goods

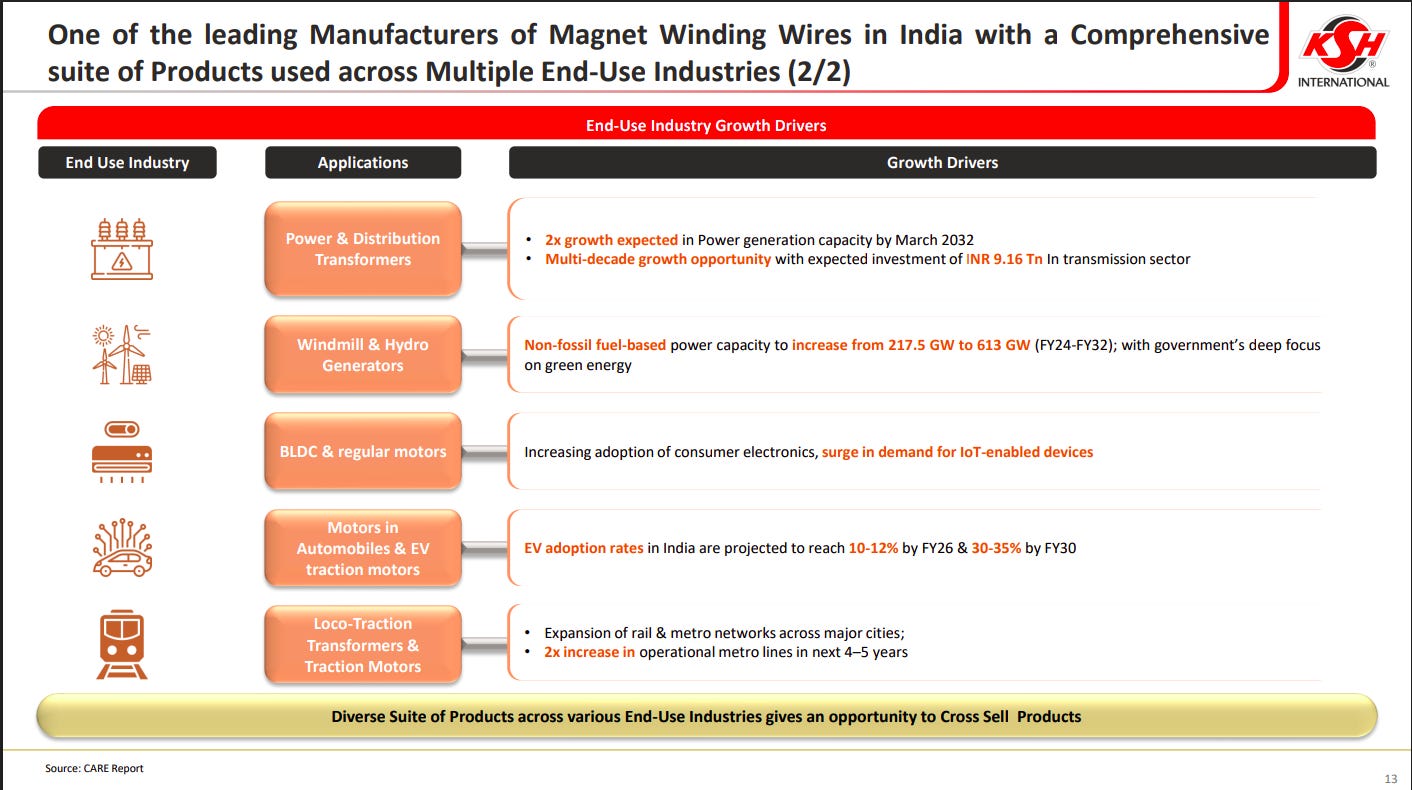

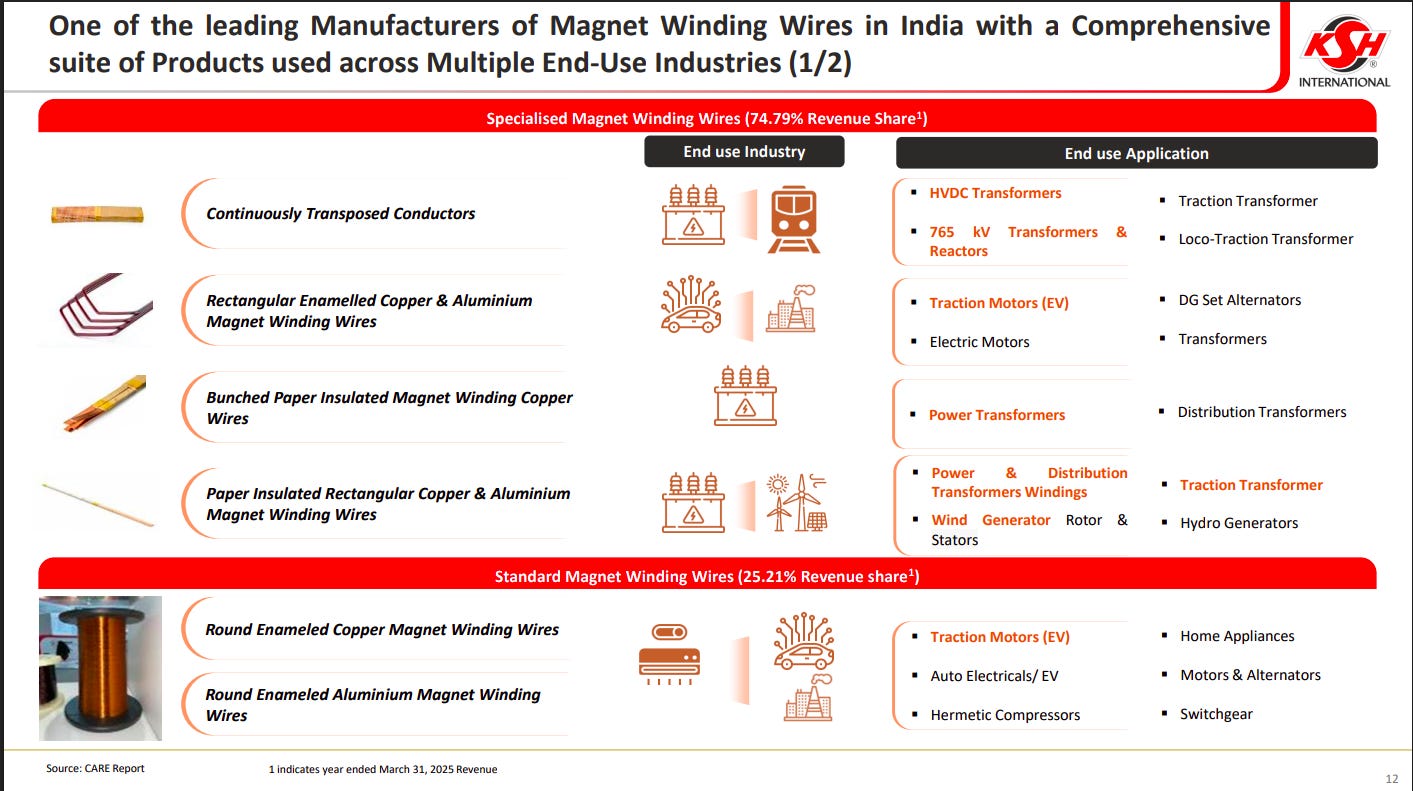

KSH International Ltd. manufactures and exports magnet winding wires and conductors used in transformers, motors, generators, and industrial equipment. It serves major OEMs across sectors and maintains a strong domestic and global supply presence.

Demand for magnet winding wires is being driven by power transmission, renewables, EV motors, and rail electrification. Strong capex in power grids, rapid EV adoption, and metro/rail expansion create multi-decade growth opportunities. The diversified end-use base also enables cross-selling across industries.

KSH has a comprehensive portfolio of specialised and standard magnet winding wires, with ~75% revenue from high-value specialised products. These are used across transformers, EV traction motors, generators, renewables, and industrial motors. The wide application footprint reduces dependency on any single sector.

KSH is India’s largest exporter of magnet winding wires, with a strong global customer base and long-standing relationships. It operates multiple manufacturing facilities with ongoing capacity expansion and delivers industry-leading margins and revenue growth. Exports span 20+ countries, supported by repeat business and diversified end markets.

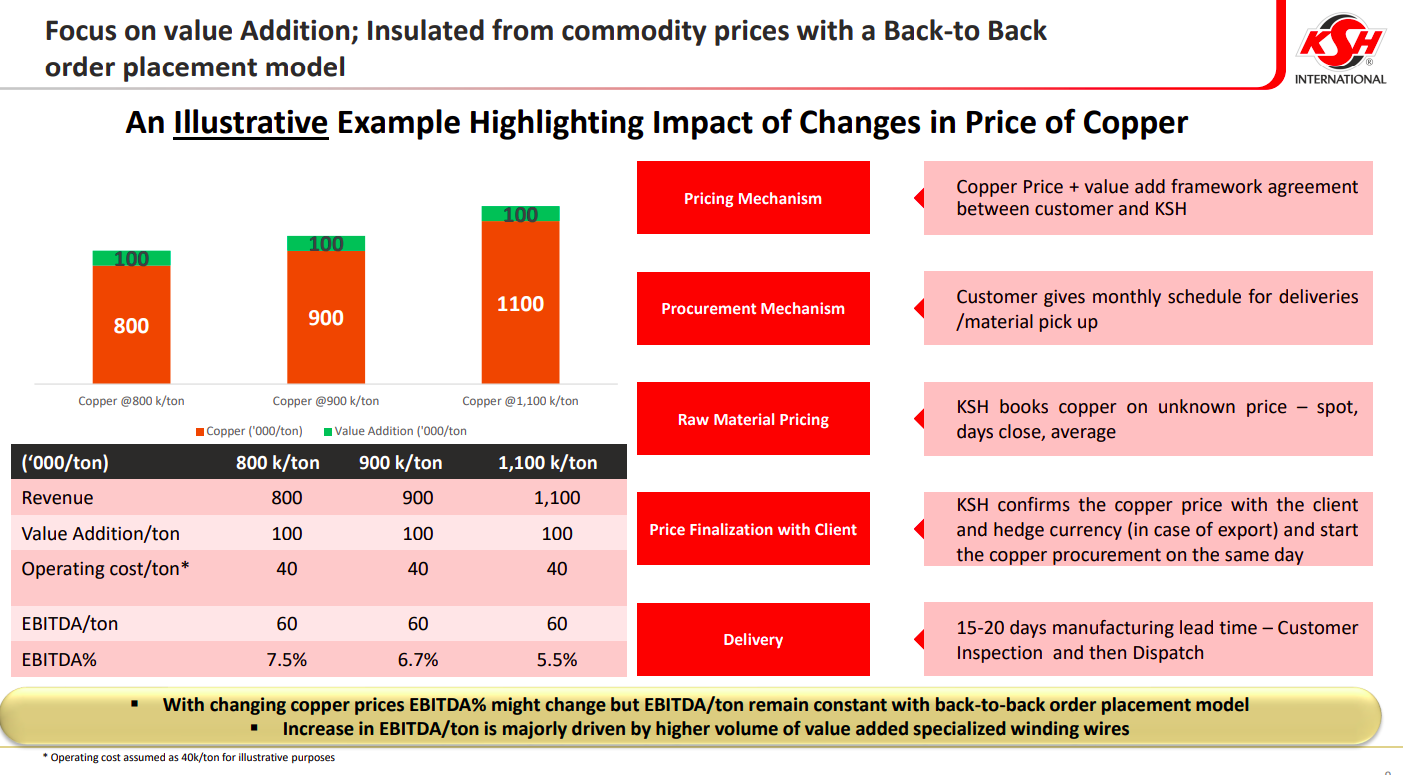

The back-to-back order model insulates profitability from copper price volatility by locking in value-addition per ton. While EBITDA margins may fluctuate with copper prices, absolute EBITDA per ton remains stable. Profit growth is driven by higher volumes of specialised, value-added winding wires rather than commodity price movements.

Metals

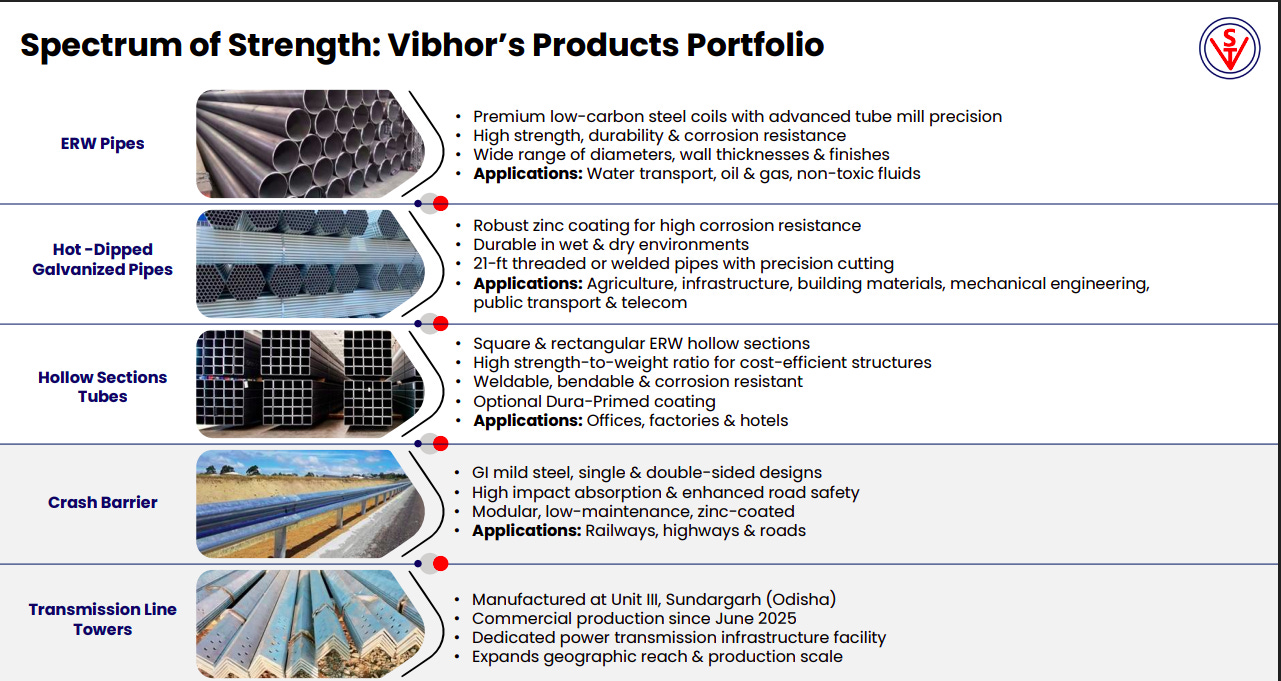

Vibhor Steel Tubes | Nano Cap | Metals

Vibhor Steel Tubes is a renowned manufacturer and exporter of Mild Steel/Carbon Steel ERW Black and Galvanized Pipes, Hallow Steel Pipe, and Cold rolled Steel Strips/Coils in India. With decades of experience, they supply steel pipes and tubes to heavy engineering industries for various applications like frames, shafts, bicycle frames, furniture, shockers, and structural engineering purposes.

Vibhor offers a diversified steel products portfolio spanning ERW pipes, galvanized pipes, hollow sections, crash barriers, and transmission line towers. These products serve critical infrastructure needs across water, oil & gas, construction, highways, railways, and power transmission, emphasizing durability, corrosion resistance, and scale.

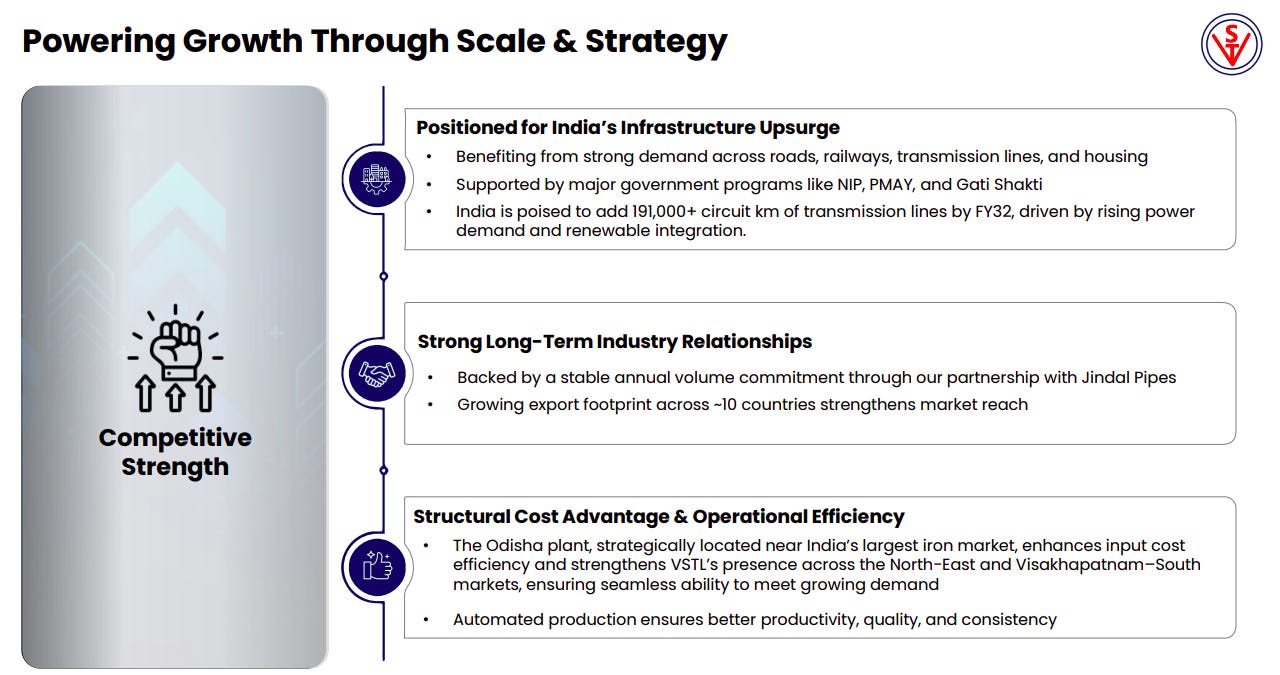

Vibhor is well positioned to benefit from India’s infrastructure upcycle, supported by government programs like NIP, PMAY, and Gati Shakti. Long-term industry partnerships, export expansion, and cost advantages from its Odisha plant underpin sustainable growth, operational efficiency, and competitive strength.

Retail

Logica Infoway Ltd. | Retail | Retail

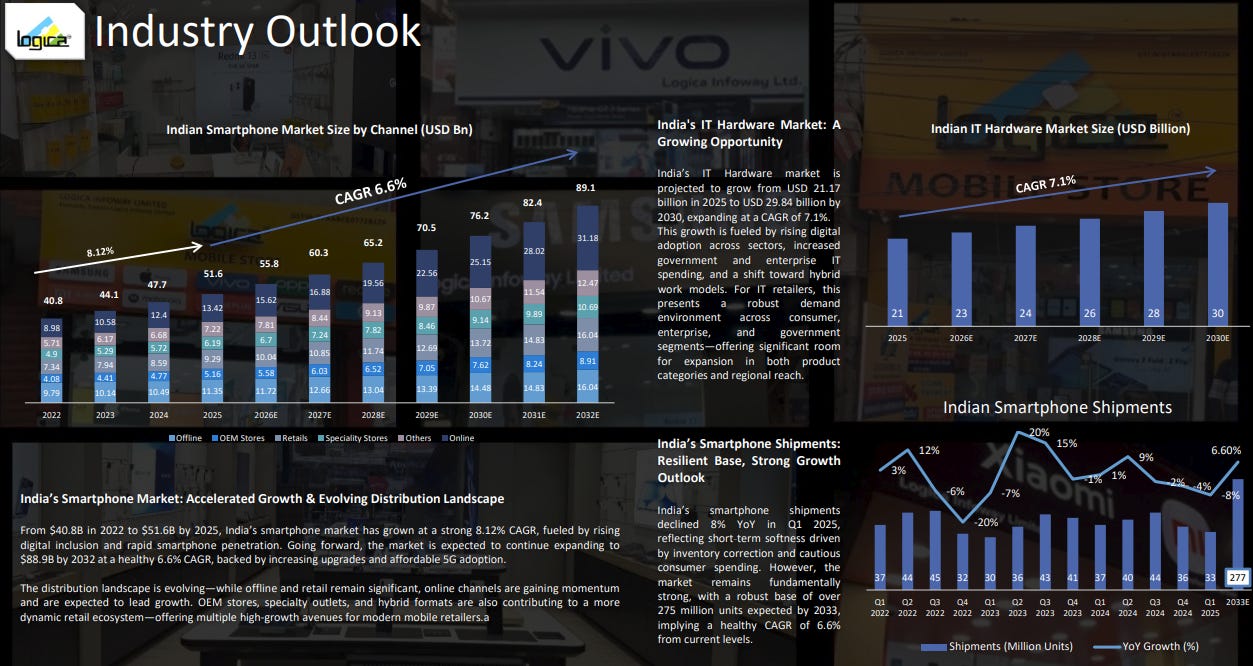

Eastern Logica Infoway Limited is a multi-brand retailer and distributor of smartphones, IT hardware, software, and accessories. They focus on providing networking and security solutions and operate multi-brand retail outlets offering customers a wide range of products under one roof. Established relationships with electronic brands ensure a diverse product showcase for a convenient shopping experience.

India’s smartphone market has grown from $40.8 billion in 2022 to an expected $51.6 billion by 2025, clocking an 8.12% CAGR, and is projected to reach $88.9 billion by 2032 at 6.6% CAGR. The growth is being driven by rising digital adoption, affordable smartphones, and 5G rollout. While offline and retail channels still dominate, online is gaining ground and expected to lead future growth. Meanwhile, India’s IT hardware market is set to jump from $5 billion in 2025 to nearly $30 billion by 2030—a 7.1% CAGR—fueled by digitization, government and enterprise IT spending, and hybrid work models. Smartphone shipments, after a brief dip, have rebounded strongly and are projected to grow steadily to 275 million units by 2033, backed by a robust base of 725 million users.

Agriculture

Narmada Agrobase | Nano cap | Agriculture

Narmada Agrobase is an ISO 9001:2015 certified company specializing in the manufacturing and processing of cotton seed meal cake, cattle feeds, and soya bean meal. Its high-protein products benefit cattle nutrition, while by-products serve industries like Textiles, Consumer Goods, and Paper. The company exports under the brand names ‘Churma’ and ‘Gaay Chhaap Narmada Pashu Aahar’.

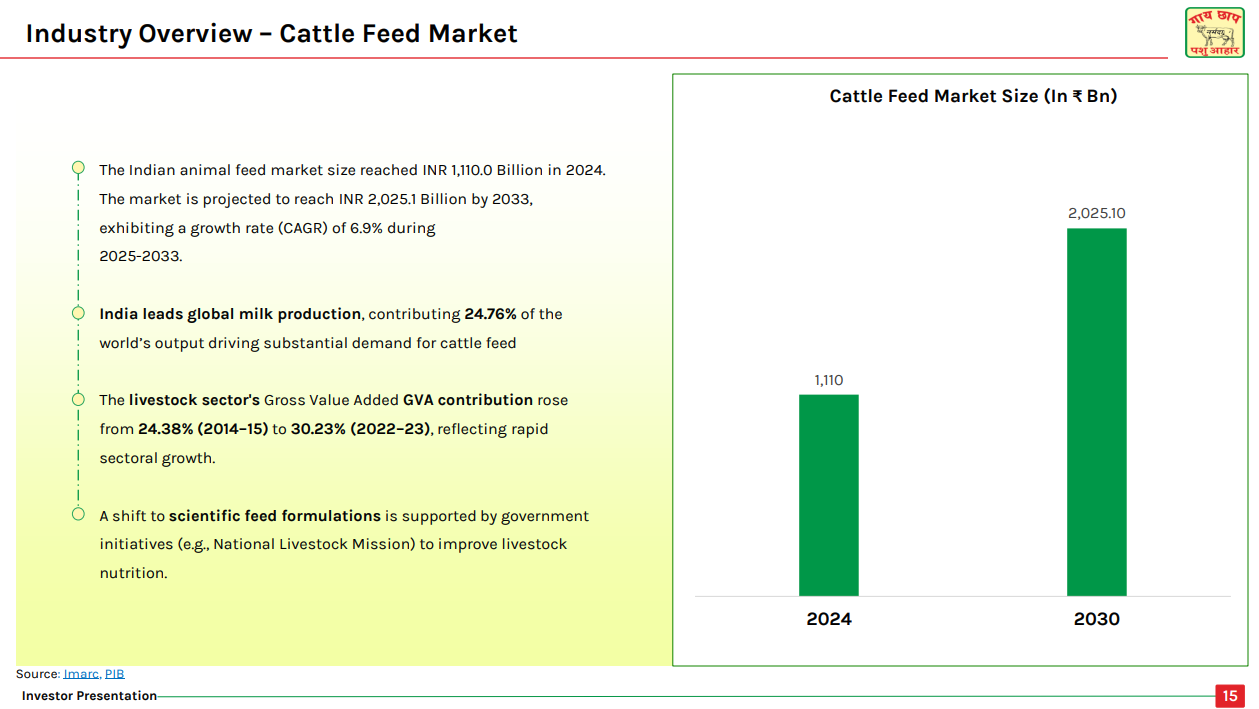

India’s animal feed market stood at ₹1,110 billion in 2024 and is expected to nearly double to ₹2,025.1 billion by 2033, growing at a healthy 6.9% CAGR. This growth is backed by India’s position as a global dairy leader—contributing 24.76% of the world’s milk production—which drives strong demand for quality cattle feed. The livestock sector’s contribution to the country’s Gross Value Added (GVA) has jumped from 24.38% in 2014-15 to 30.23% in 2022-23, reflecting rapid sectoral growth. There’s also a shift toward scientific feed formulations, supported by government initiatives like the National Livestock Mission, which aim to improve livestock nutrition and productivity.

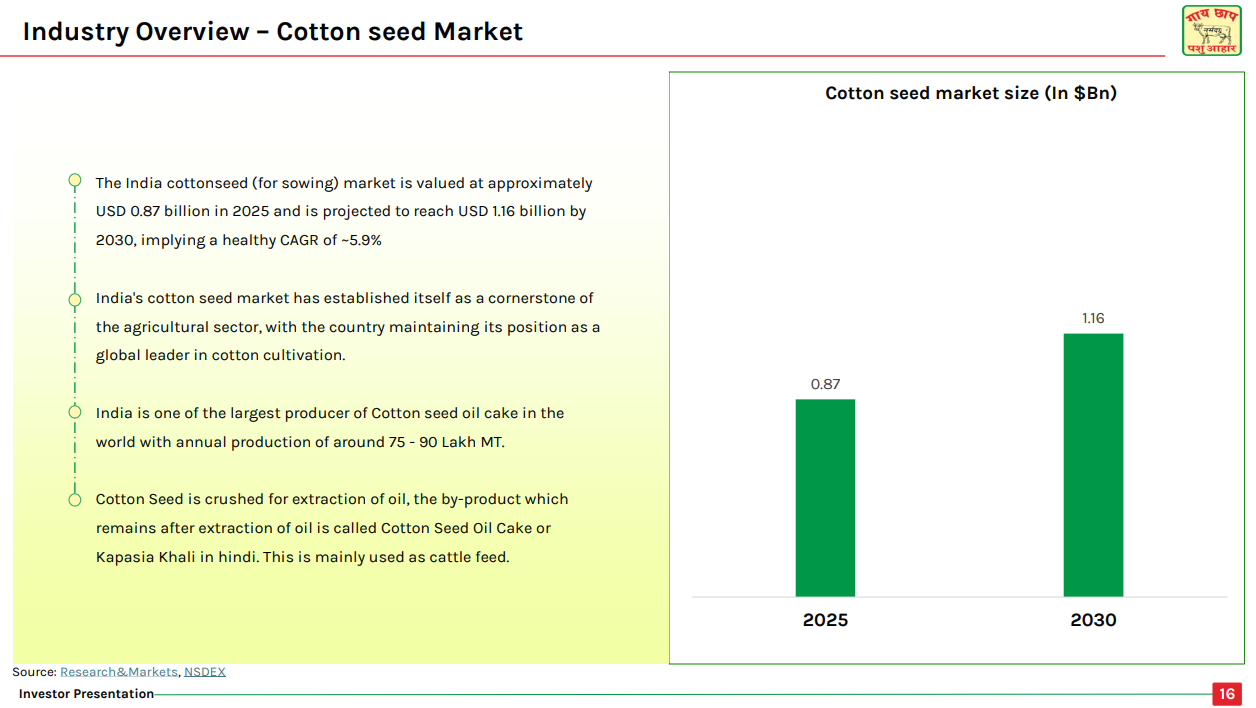

India’s cottonseed (for sowing) market is valued at around $0.87 billion in 2025 and is expected to grow to $1.16 billion by 2030, at a steady CAGR of roughly 5.9%. The country has established itself as a cornerstone of the agricultural sector and remains a global leader in cotton cultivation. India is also one of the largest producers of cotton seed oil cake in the world, with annual production ranging between 75-90 lakh metric tons. Cotton seeds are crushed to extract oil, and the by-product left behind—called cotton seed oil cake or Kapasia Khali in Hindi—is primarily used as cattle feed, adding another revenue stream to the cotton value chain.

Textiles

Monte Carlo Fashions | Micro Cap | Textiles

Monte Carlo Fashions Ltd manufactures and distributes men’s and women’s apparel. The company manufactures shirts, t-shirts, and sportswear. Monte Carlo Fashions Ltd was incorporated in 2008 and is based in Ludhiana, India. Monte Carlo Fashions Ltd operates as a subsidiary of Oswal Woollen Mills Limited.

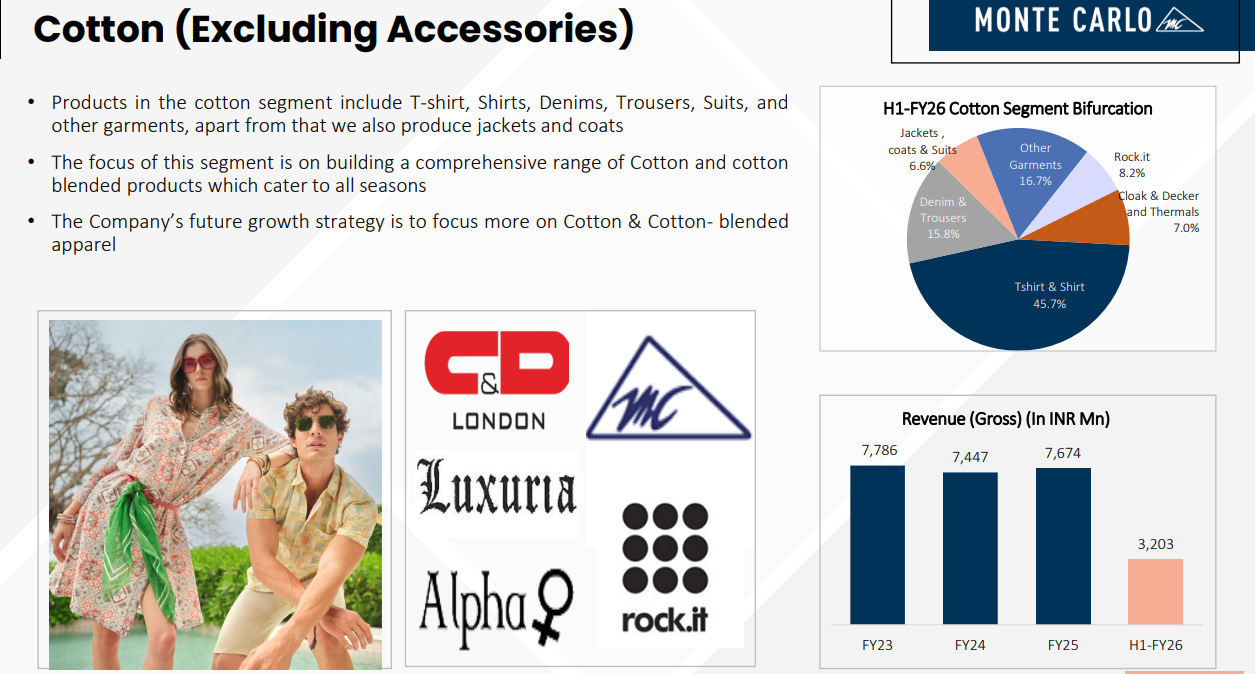

Monte Carlo’s cotton segment includes a wide range of products—T-shirts, shirts, denims, trousers, suits, and other garments, along with jackets and coats. The focus here is on building a comprehensive portfolio of cotton and cotton-blended products that cater to all seasons, with the company’s future growth strategy centered on expanding this segment further. In H1-FY26, T-shirts and shirts dominated the mix at 45.7%, followed by denims and trousers at 15.8%, while jackets, coats, and suits contributed 6.6%. Revenue from the cotton segment has remained relatively stable, hovering around ₹7,500-7,700 million in recent years, though H1-FY26 saw a dip to ₹3,203 million, reflecting the half-year period.

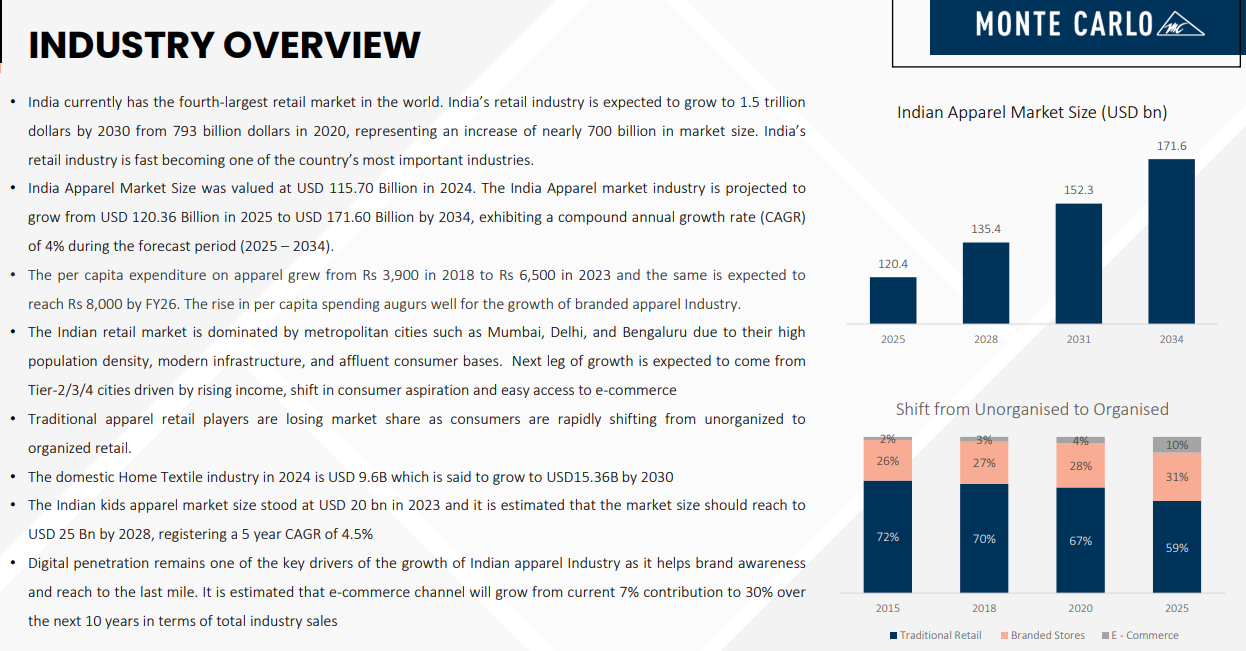

India has the fourth-largest retail market globally, expected to grow from $793 billion in 2020 to $1.5 trillion by 2030—an increase of nearly $700 billion. The apparel market alone was valued at $115.70 billion in 2024 and is projected to reach $171.60 billion by 2034, growing at a 4% CAGR. Per capita spending on apparel has also climbed from ₹3,900 in 2018 to ₹6,500 in 2023 and is expected to hit ₹8,000 by FY26, signaling strong demand for branded apparel. While metros like Mumbai, Delhi, and Bengaluru dominate the market, the next wave of growth is expected from Tier-2/3/4 cities, driven by rising incomes and better access to e-commerce. Traditional retail is losing ground as consumers shift to organized formats, with e-commerce expected to grow from 7% of total sales currently to 30% over the next decade. The domestic home textile industry is pegged at $9.6 billion in 2024 and could reach $15.36 billion by 2030, while the kids’ apparel market stood at $20 billion in 2023 and is estimated to grow to $25 billion by 2028 at a 4.5% CAGR.

Financial Services

Emkay Global Financial Services Ltd. | Micro cap | Financial Services

Emkay Global Financial Services offers the entire gamut of advisory services under one roof. Right from investing, trading, research and financial planning to portfolio management services, it provides its clients with integrated, robust and reliable solutions to satisfy all their financial needs.

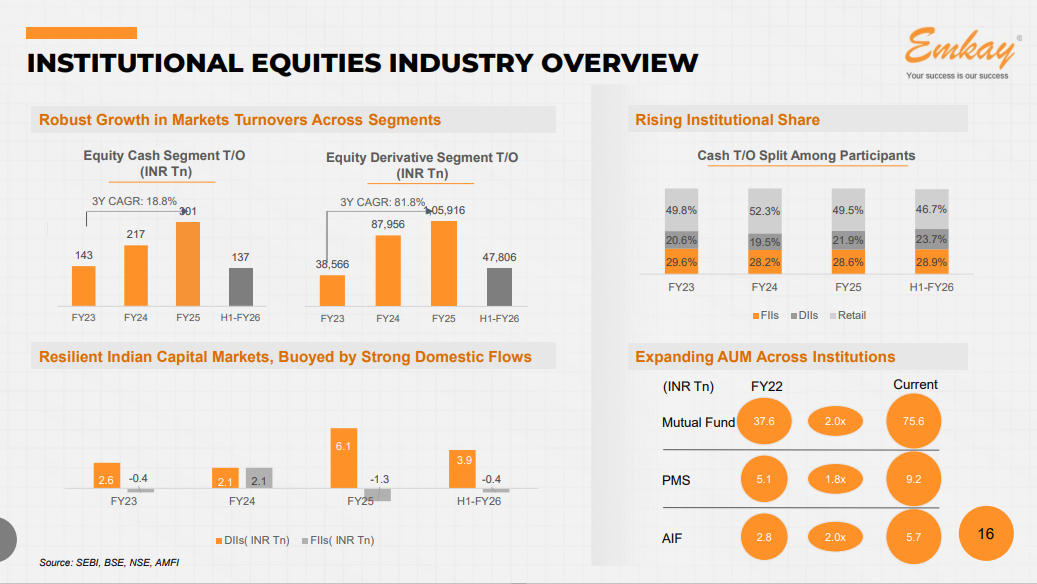

The institutional equities business has seen robust growth across both cash and derivatives segments. Equity cash turnover grew at an 18.8% CAGR over three years, reaching ₹301 trillion in FY25 before moderating to ₹137 trillion in H1-FY26. Equity derivatives turnover grew even faster at 81.8% CAGR, hitting ₹405.9 trillion in FY25, though it also saw a decline to ₹47.8 trillion in H1-FY26. The institutional share in cash trading has remained steady, with FIIs accounting for around 49-50%, DIIs for 19-20%, and retail for 28-29% over recent years. Indian capital markets have been resilient and buoyed by strong domestic flows, with domestic institutional inflows (DIIs) consistently offsetting foreign institutional outflows (FIIs) across FY23 to H1-FY26. Assets under management (AUM) have expanded significantly across institutions—mutual funds have grown from ₹37.8 trillion in FY22 to ₹75.6 trillion currently, PMS from ₹5.1 trillion to ₹9.2 trillion, and AIFs from ₹2.8 trillion to a notable ₹16 trillion.

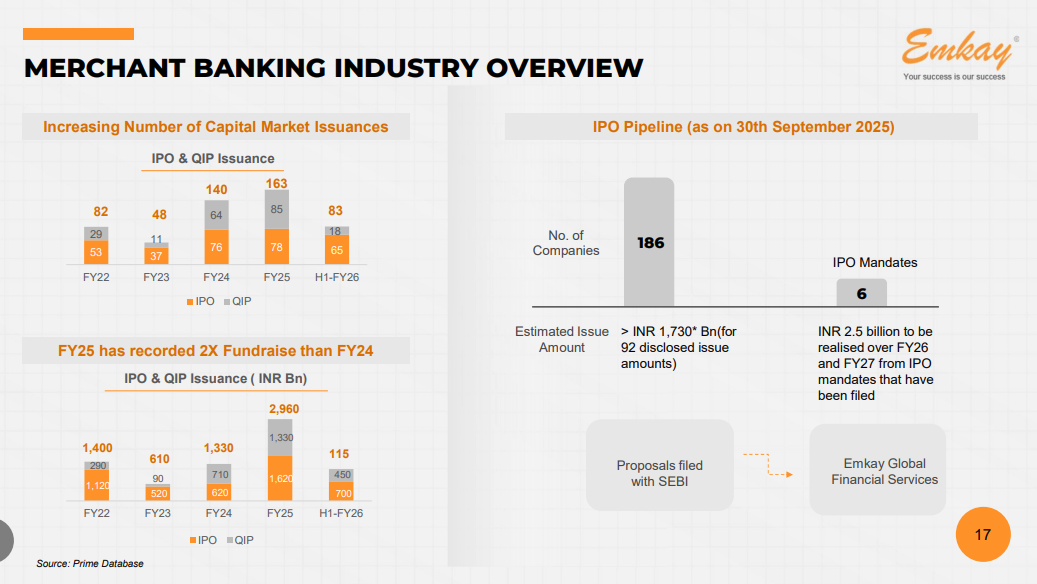

The number of capital market issuances has been climbing steadily—from 82 IPOs and QIPs in FY22 to 163 in FY25, with H1-FY26 already recording 83 issuances. FY25 was a standout year, recording twice the fundraise amount of FY24, with total IPO and QIP issuances reaching ₹2,960 billion compared to ₹1,330 billion the previous year. As of September 30, 2025, the IPO pipeline is strong with 186 companies in the queue, representing an estimated issue size of over ₹1.73 trillion (based on 92 disclosed amounts). There are also six IPO mandates filed that are expected to realize around ₹2.5 billion over FY26 and FY27. Emkay Global Financial Services has proposals filed with SEBI, positioning itself to participate in this growing merchant banking opportunity.

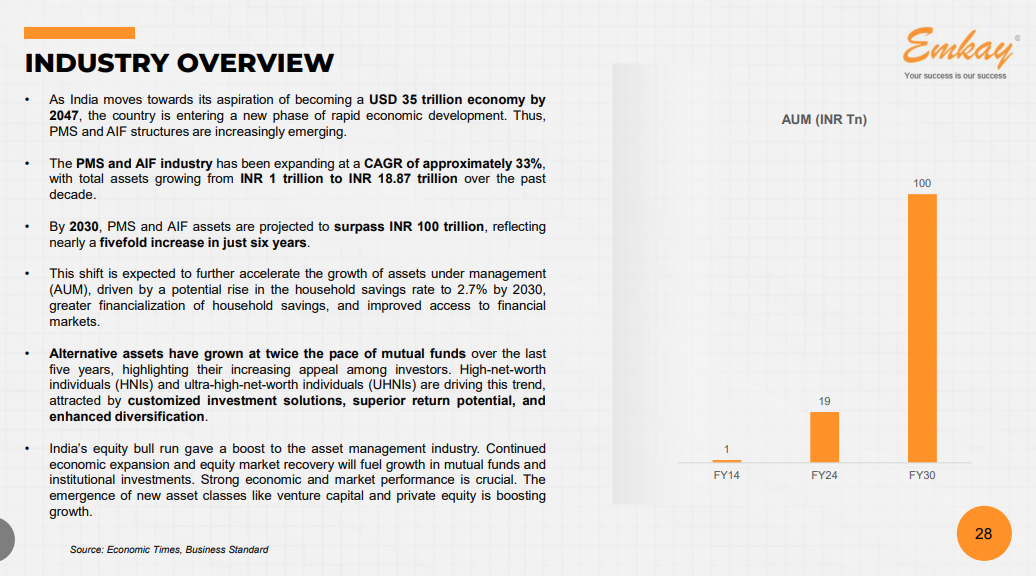

As India targets becoming a $35 trillion economy by 2047, PMS and AIF structures are rapidly emerging to meet growing investor demand. The PMS and AIF industry has expanded at a CAGR of around 33%, with total assets growing from ₹1 trillion to ₹18.87 trillion over the past decade, and is projected to surpass ₹100 trillion by 2030—a nearly fivefold increase in just six years. This growth is being driven by rising household savings rates (expected to hit 2.7% by 2030), greater financialization of savings, and improved access to financial markets. Alternative assets have grown at twice the pace of mutual funds over the last five years, fueled by high-net-worth and ultra-high-net-worth individuals seeking customized investment solutions, superior returns, and enhanced diversification. India’s equity bull run has further boosted the asset management industry, with continued economic expansion and equity market recovery expected to drive growth in both mutual funds and institutional investments, alongside emerging asset classes like venture capital and private equity.

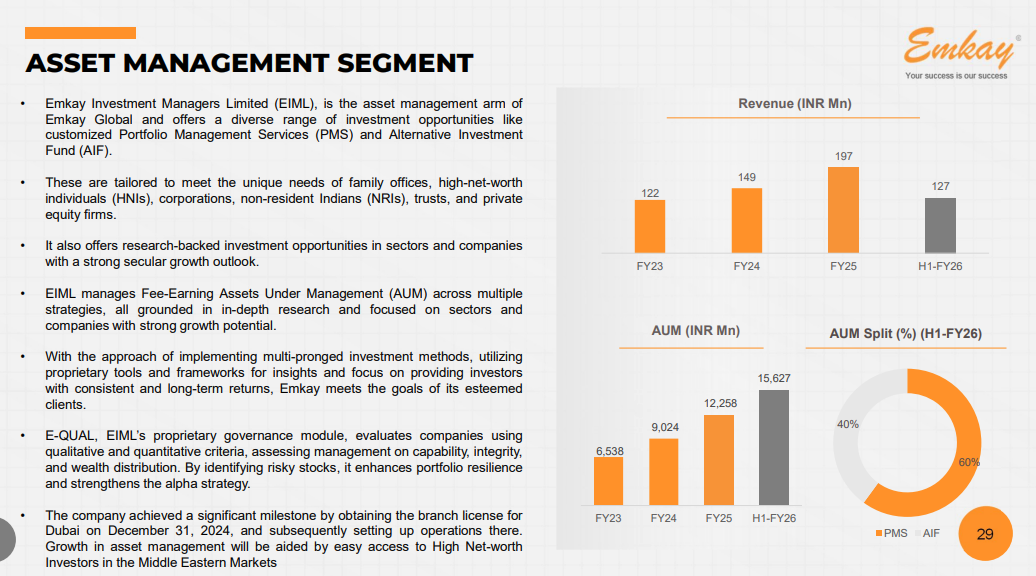

Emkay Investment Managers Limited (EIML) is the asset management arm of Emkay Global, offering customized Portfolio Management Services (PMS) and Alternative Investment Funds (AIF) tailored for family offices, high-net-worth individuals, corporations, NRIs, trusts, and private equity firms. The segment focuses on research-backed investment opportunities in sectors and companies with strong secular growth outlooks. EIML manages fee-earning AUM across multiple strategies, all grounded in in-depth research, and uses proprietary tools like E-QUAL—a governance module that evaluates companies on capability, integrity, and wealth distribution to identify risky stocks and enhance portfolio resilience. Revenue has grown steadily from ₹122 million in FY23 to ₹197 million in FY25, though H1-FY26 came in at ₹127 million. AUM has also expanded impressively, from ₹6,538 million in FY23 to ₹15,627 million in H1-FY26, with AIF now accounting for 60% of the mix and PMS 40%. A major milestone was obtaining the branch license for Dubai in December 2024, opening up growth opportunities in the Middle Eastern markets by providing easier access to high-net-worth investors in the region.

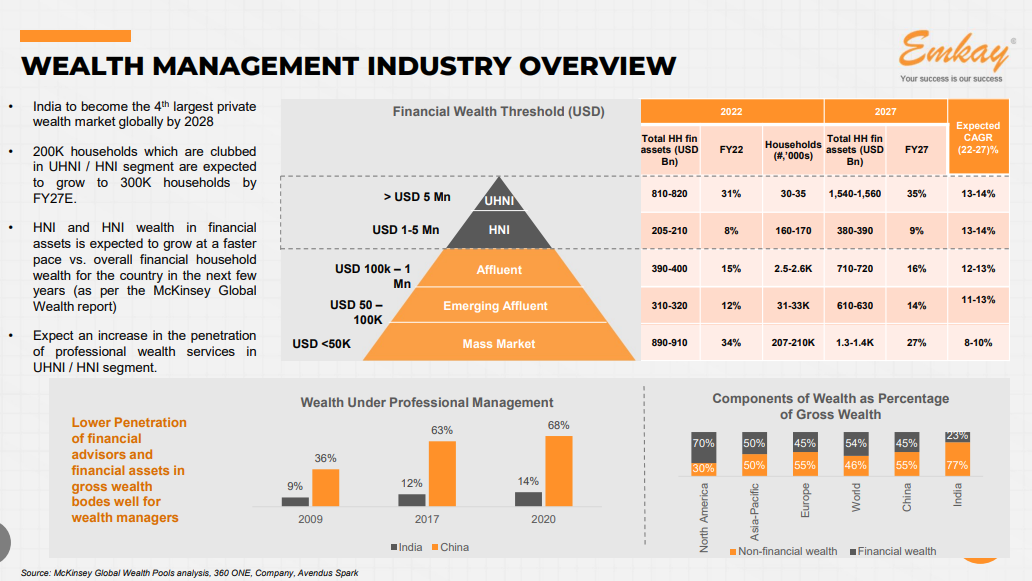

India is set to become the world’s fourth-largest private wealth market by 2028, with around 200,000 households expected to enter the UHNI/HNI segment by FY27E. HNI and HNWI wealth in financial assets is projected to grow at a faster pace than overall financial household wealth in the country over the next few years, according to McKinsey’s Global Wealth report. The wealth pyramid shows different segments—from the mass market (under $50K) to UHNI (over $5 million)—with the affluent and emerging affluent categories holding significant household counts and financial assets expected to grow at 12-16% CAGR through FY27. However, wealth under professional management remains low in India—just 9% in 2009, rising to 36% by 2017 and 63% by 2020—compared to China’s 68%, highlighting a significant opportunity for wealth managers. Additionally, components of wealth as a percentage of gross wealth vary across regions, with India having the highest share of non-financial wealth (77%) compared to more developed markets, suggesting room for increased financialization and professional wealth management penetration.Bayer

That’s it for now! Your feedback will really help shape how Points and Figures evolves. Drop it down in the comments below!

Quotes in this newsletter were curated by Meher, Kashish, & Vignesh.

Disclaimer: We’ve used AI tools in filtering and cleaning up the quotes from the images so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Points and Figures is run by the same team that creates The Daily Brief and Aftermarket Report.

Really liked this breakdown. Investor presentations have so much information, but most of us do not have the time to go through every slide. The way you pull out only the meaningful points makes it so much easier to understand what’s really happening in these companies. Looking forward to more editions like this.