Sometimes, a single slide can explain more than a long report. Points and Figures is our way of breaking down what India’s leading companies are telling their shareholders and analysts. We comb through the decks, pull out the charts and data points that actually matter, and highlight the signals behind the numbers—whether about growth plans, margins, new markets, or risks on the horizon.

This is an extension of The Chatter. While The Chatter focuses on management commentary and earnings call transcripts, Points and Figures dives into investor presentations—and soon, even annual reports—to decode what companies are showing, not just what they’re saying.

We go through every major investor presentation so you don’t have to—bringing you the sharpest takeaways that reveal not just what the company is saying, but what it really means for the business, its sector, and the broader economy.

In this edition, we have covered 15 companies across 5 industries.

Chemicals

Rain Industries

lndag Rubber

Engineering & Capital Goods

ABB India Limited

Power Mech Projects

Elgi Equipments

Fabtech Technologies

Praj Industries

DC Infotech and Communication

Schaeffler India Limited

FMCG

Marico Limited

Avanti Feeds Limited

Pharmaceuticals

Sanofi India Limited

Financial Services

HDFC Life Insurance Company Limited

Fino Payments Bank Limited

ICICI Prudential Asset Management

Chemicals

Rain Industries | Small Cap | Chemicals

Rain Industries Limited is a global manufacturer of critical raw materials for various industries. It has three main segments - Carbon, Advanced Materials, and Cement. The company is a major producer of CTP and CPC, supplying essential raw materials worldwide. It focuses on developing eco-friendly advanced materials and produces high-quality cement to meet the construction demand in South India.

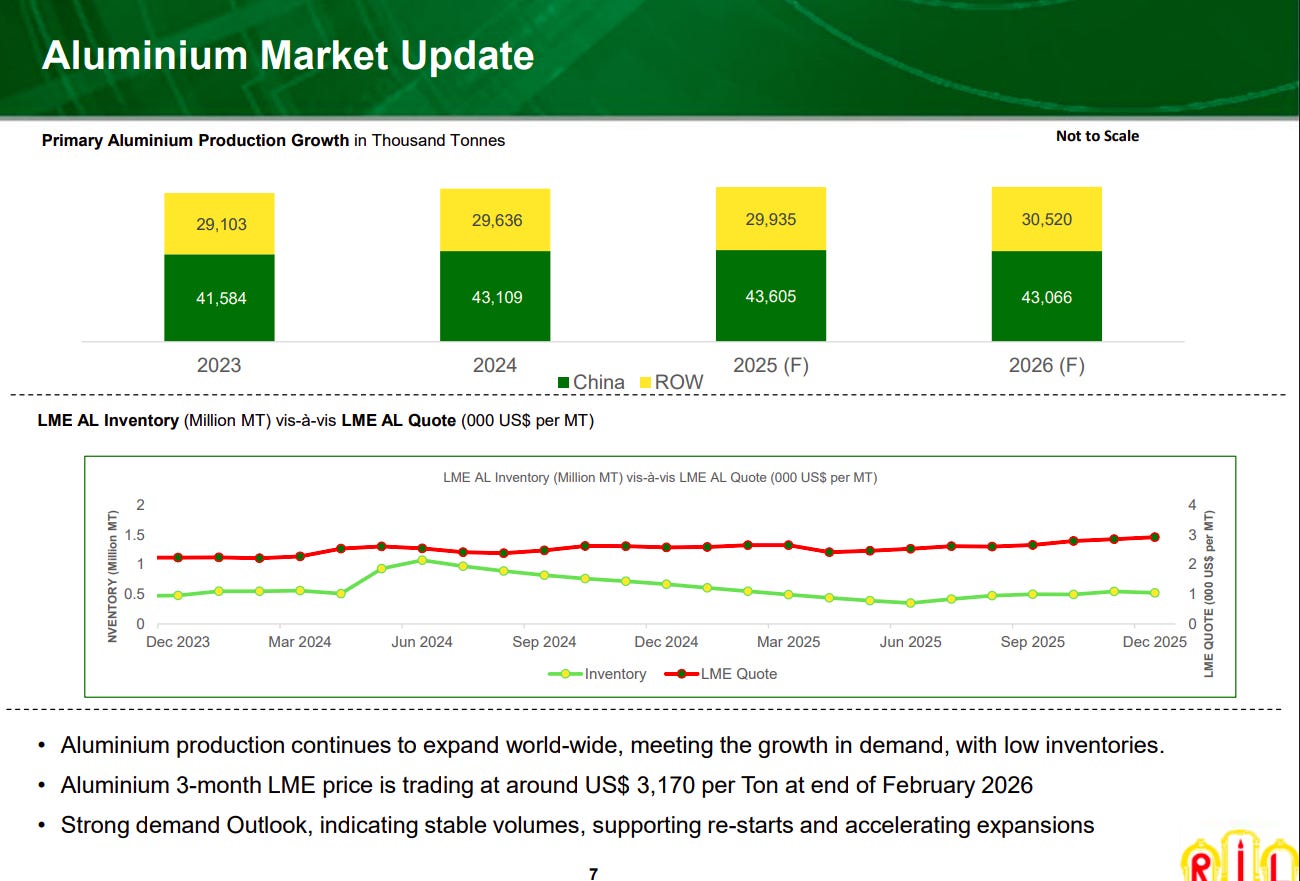

Global aluminium production continues to grow steadily, led by China, while inventories remain relatively low. LME aluminium prices are trading around $3,170 per ton (Feb 2026), supported by strong demand and ongoing capacity restarts and expansions.

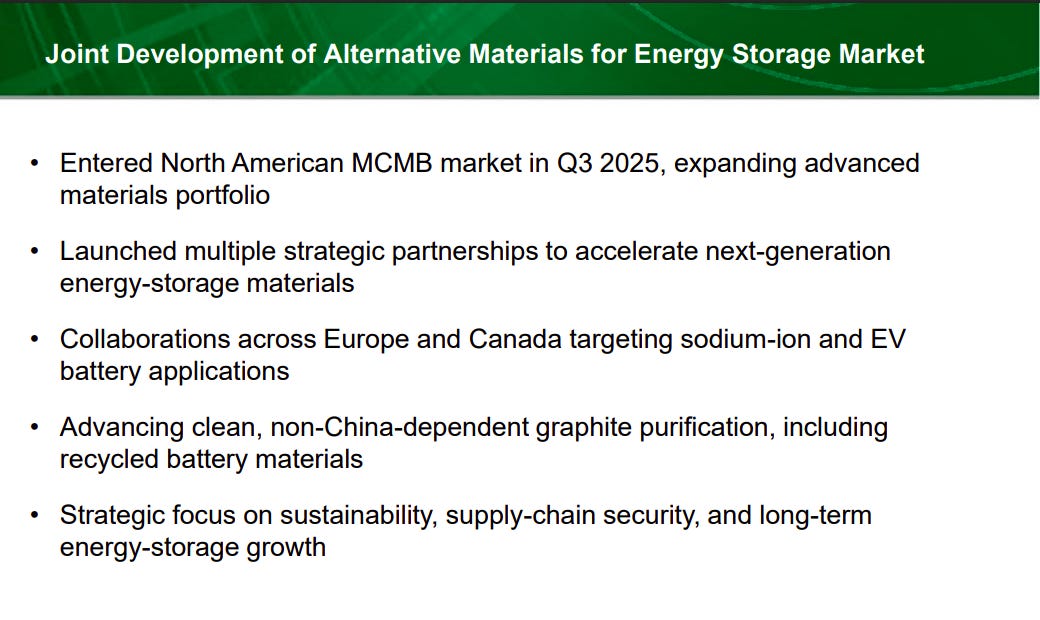

The company is expanding its advanced materials portfolio by entering the North American MCMB market and forming strategic partnerships in Europe and Canada. The focus is on next-generation battery materials, sodium-ion technologies, and reducing dependence on Chinese graphite supply chains.

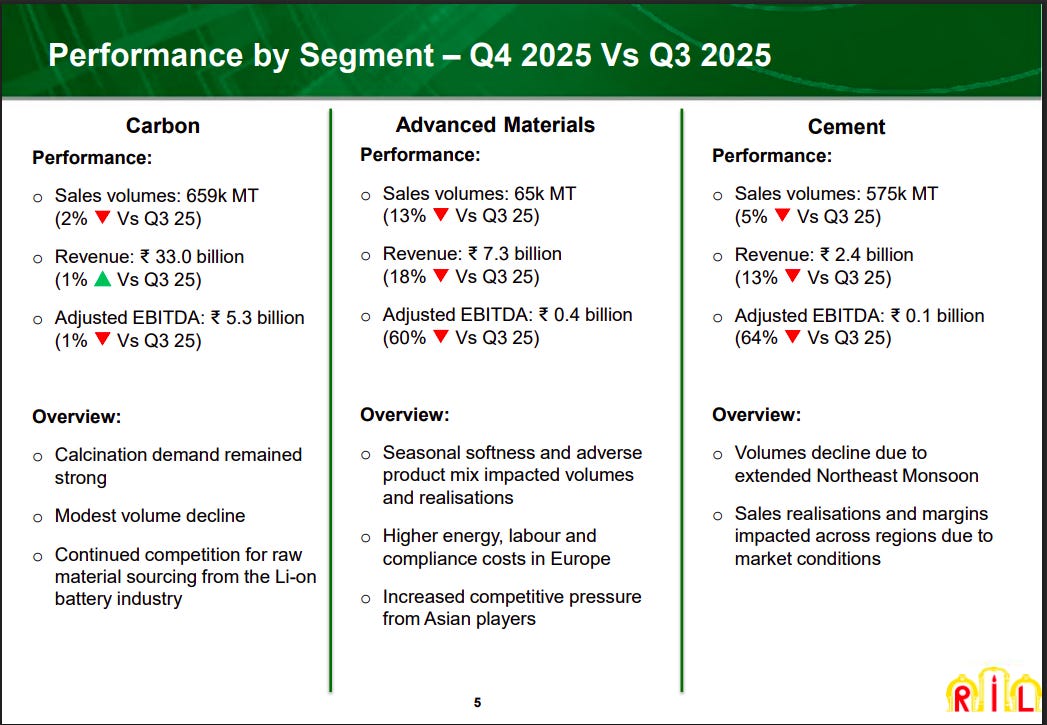

Carbon remained the strongest segment with stable revenues and EBITDA despite slight volume decline, supported by strong calcination demand. Advanced Materials and Cement saw weaker performance due to seasonal softness, higher costs in Europe, and lower volumes impacted by extended monsoon conditions.

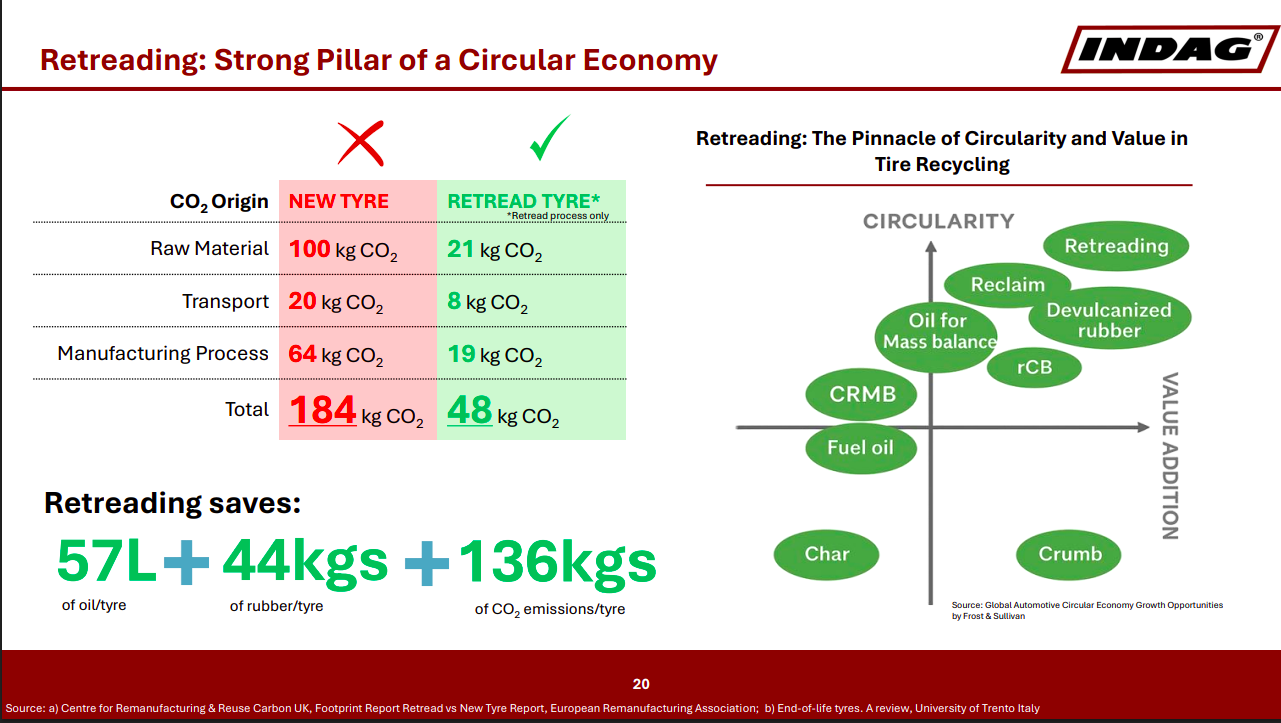

lndag Rubber | Nano Cap | Chemicals

Indag Rubber Ltd.pioneered the introduction of cold retreading technology in India.The company offers complete range of application specific tread patterns for transportation industry with cost effective tyre solutions.The products manufactured by the company includes Precured Tread Rubber,Un-vulcanized Rubber Strip Gum,Universal Spray Cement,Envelopes, etc.

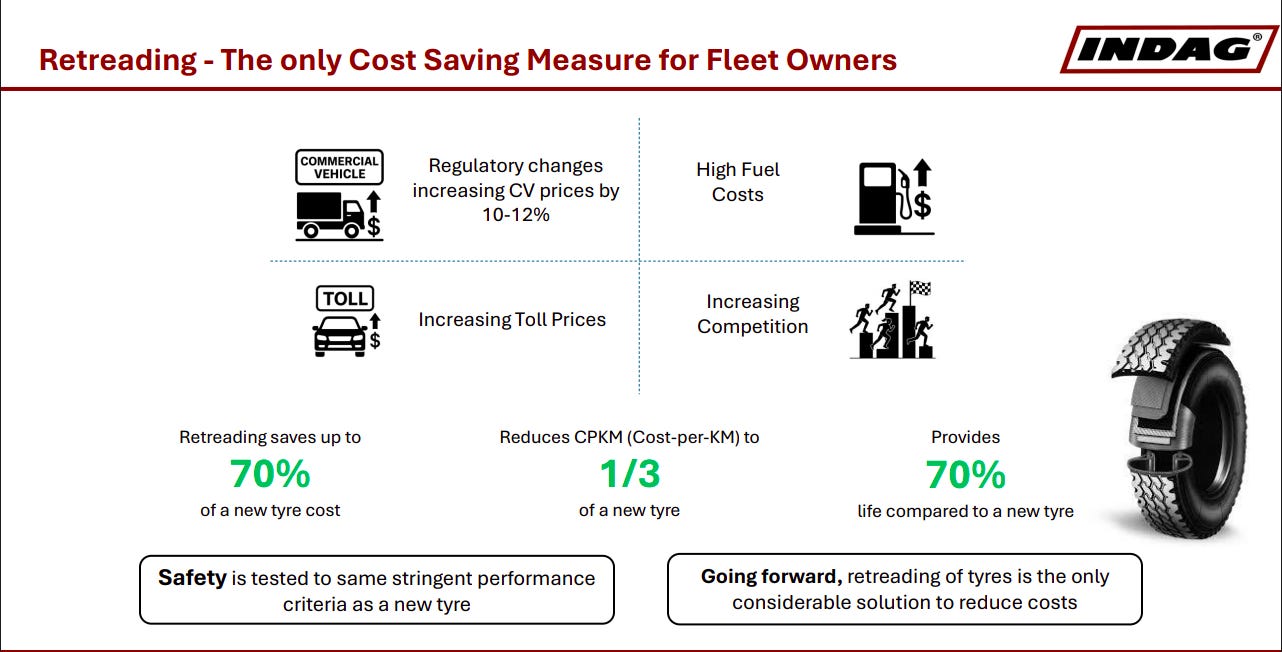

The tyre retreading industry remains significantly underpenetrated but is poised for strong growth due to improving road infrastructure, regulatory reforms, and rising environmental awareness. Increasing radialization in commercial vehicles and the gradual shift toward EV-compatible tyre designs further support long-term demand.

Tyre retreading offers a major cost advantage for fleet operators by saving up to 70% of the cost of a new tyre while delivering about 70% of the tyre life. With rising fuel prices, tolls, and vehicle costs, retreading significantly reduces cost-per-kilometre and remains one of the most effective fleet cost-management strategies.

Retreading plays a key role in the circular economy by drastically reducing environmental impact compared to manufacturing new tyres. Each retreaded tyre can save 57L of oil, 44kg of rubber, and 136kg of CO₂ emissions, while supporting recycling and value-added tyre recovery processes.

Engineering & Capital Goods

ABB India Limited | Large Cap | Heavy Electrical Equipment

ABB India is a technology leader in electrification and automation, serving industries like renewables, data centers, and railways through five domestic manufacturing locations. The company integrates engineering and digital solutions to improve industrial productivity and energy efficiency across the Indian market.

A widening gap between orders and revenue suggests that execution capacity is lagging behind demand. While this backlog secures future sales, it increases the risk of margin erosion from inflationary pressures during delivery.

Prioritizing high-growth digital and green infrastructure sectors over traditional manufacturing helps reduce cyclical risk. This strategic focus allows the company to capture premium pricing in specialized market segments.

The elimination of high customs duties via the India-Europe FTA provides a structural tailwind for lowering input costs. This change improves margin resilience and enhances India’s competitiveness as a global engineering hub.

New semiconductor and electronics manufacturing incentives create a structural demand floor for specialized power and automation solutions. Alignment with government capex ensures a long-term project pipeline less sensitive to traditional industrial cycles.

A 283% surge in robotics orders from the automotive sector signals a rapid shift toward industrial automation despite currently tepid revenue execution. Converting this massive backlog into profitable delivery remains the primary catalyst for unlocking the segment’s margin potential.

Reducing project revenue to 8% signals a shift away from low-margin EPC contracts to de-risk the business. Increasing product-led sales to 79% emphasizes a focus on standardized, higher-margin solutions with lower capital intensity.

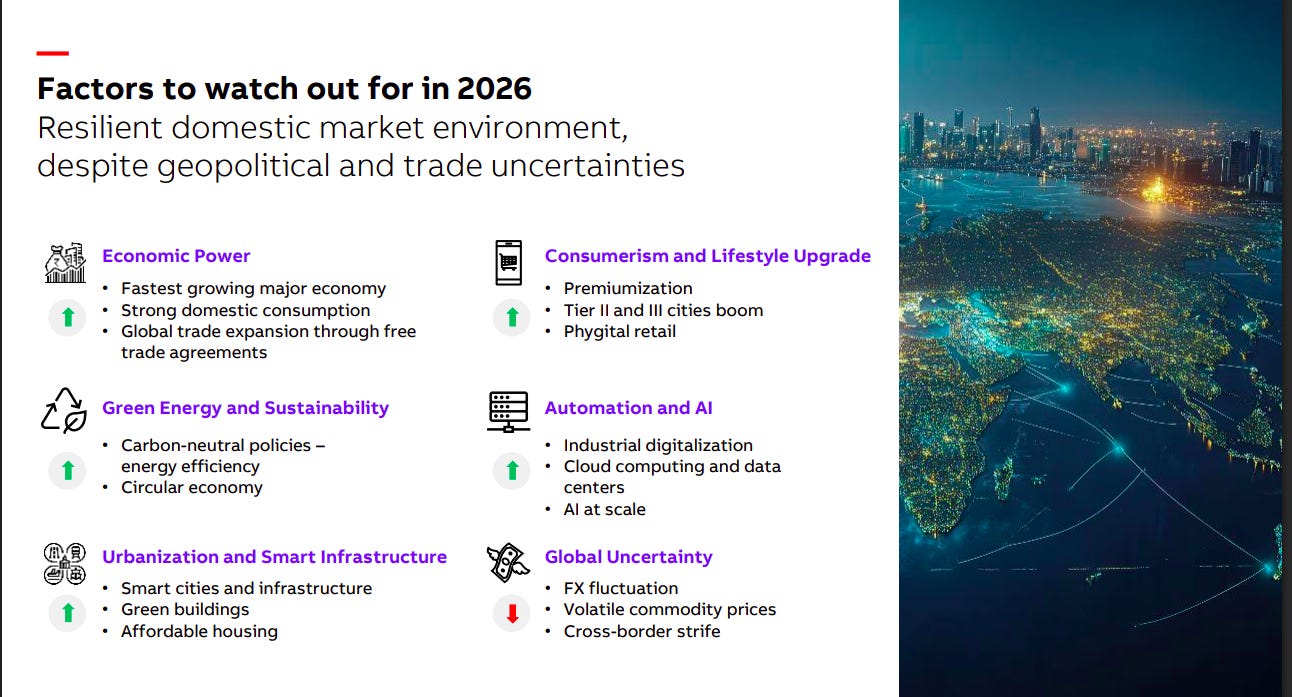

India’s domestic economy remains resilient, driven by strong consumption, premiumization, and urban infrastructure growth. At the same time, green energy adoption, AI-led industrial automation, and digitalization are key growth drivers, though global uncertainties such as FX volatility and geopolitical tensions remain risks.

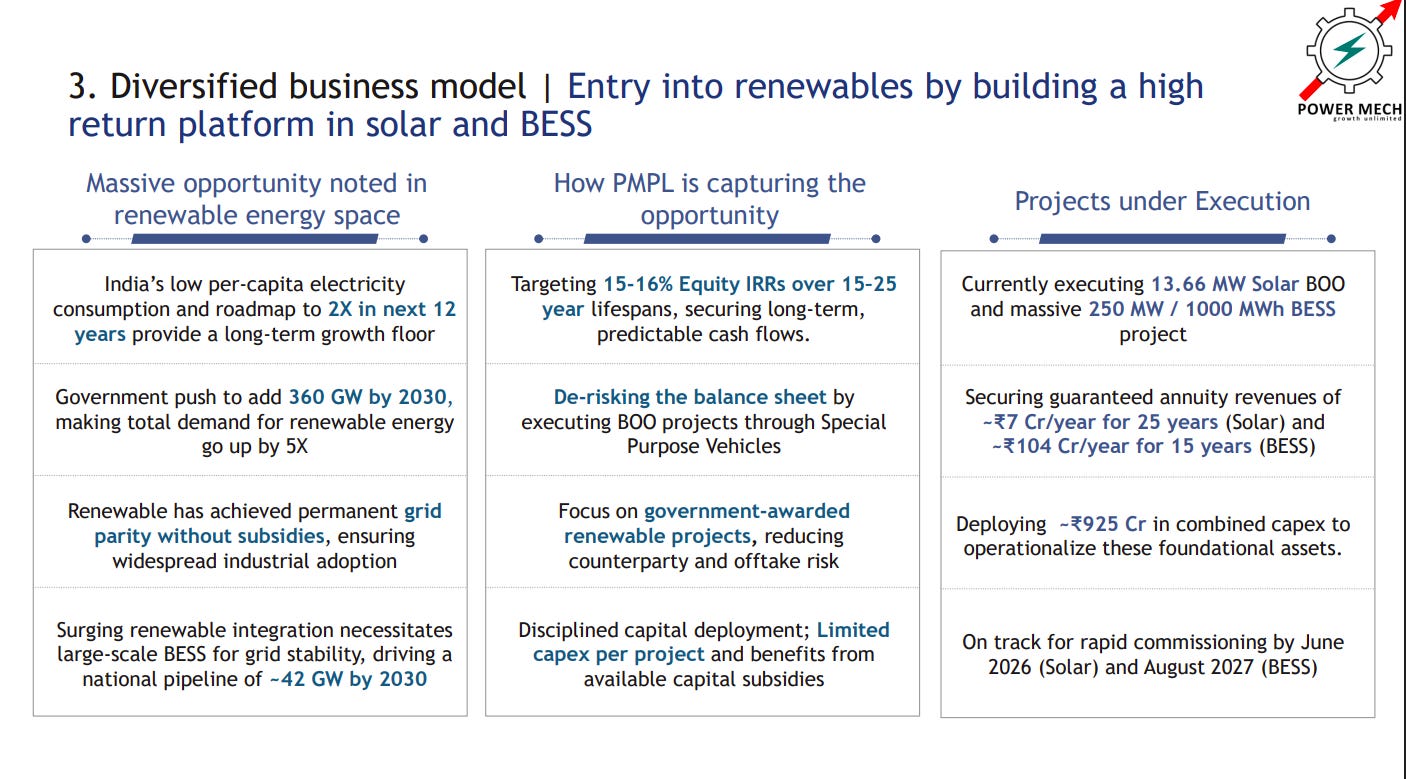

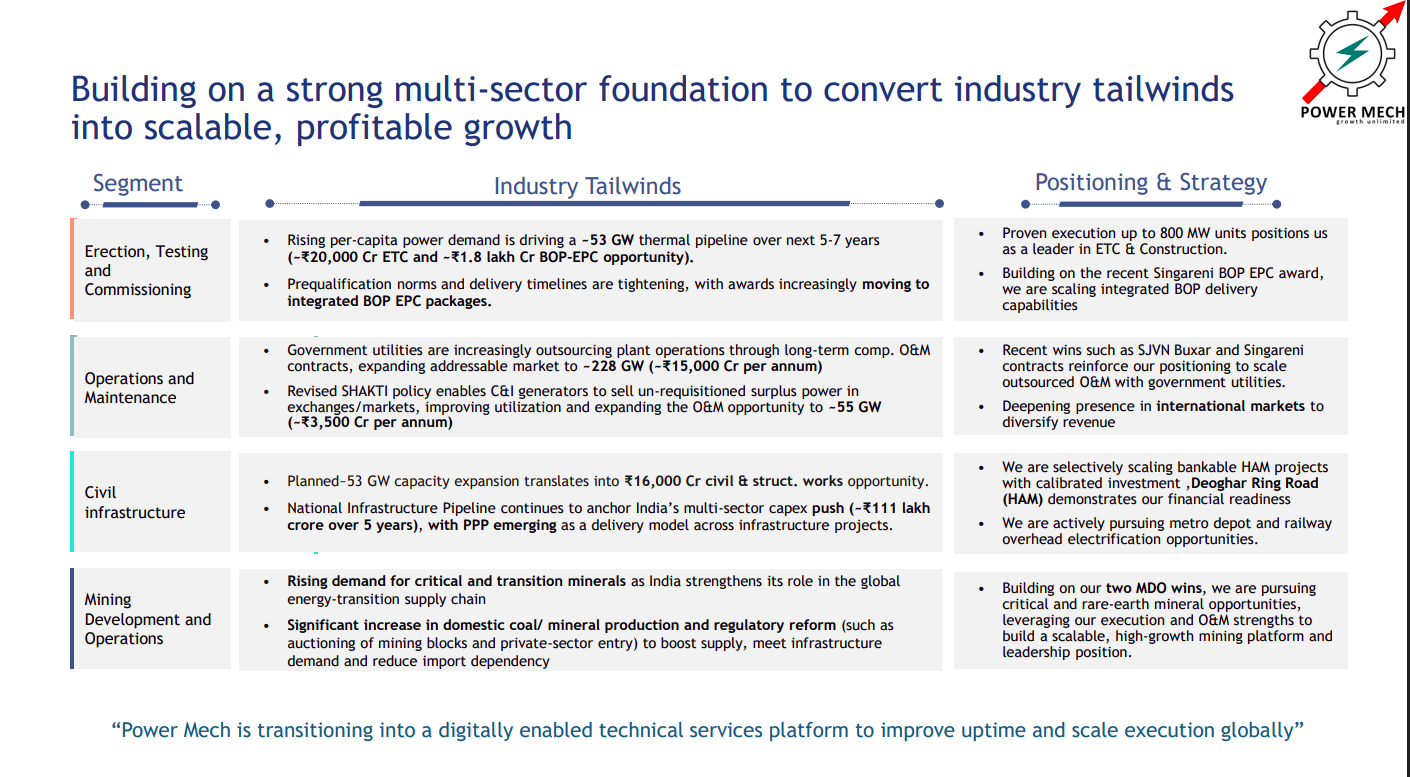

Power Mech Projects | Small Cap | Engineering & Capital Goods

Power Mech Projects Limited, based in Hyderabad, India, is a leading infrastructure construction company with a global presence. Established in 1999, the company specializes in providing a wide range of services in the power and infrastructure sectors. With expertise in power generation, operations, and maintenance, Power Mech operates in over ten countries worldwide.

Power Mech is expanding into renewable energy by building a platform in solar and battery energy storage systems (BESS). With government-backed projects and targeted 15–16% equity IRRs, the company is executing solar and BESS projects that will generate long-term annuity revenues.

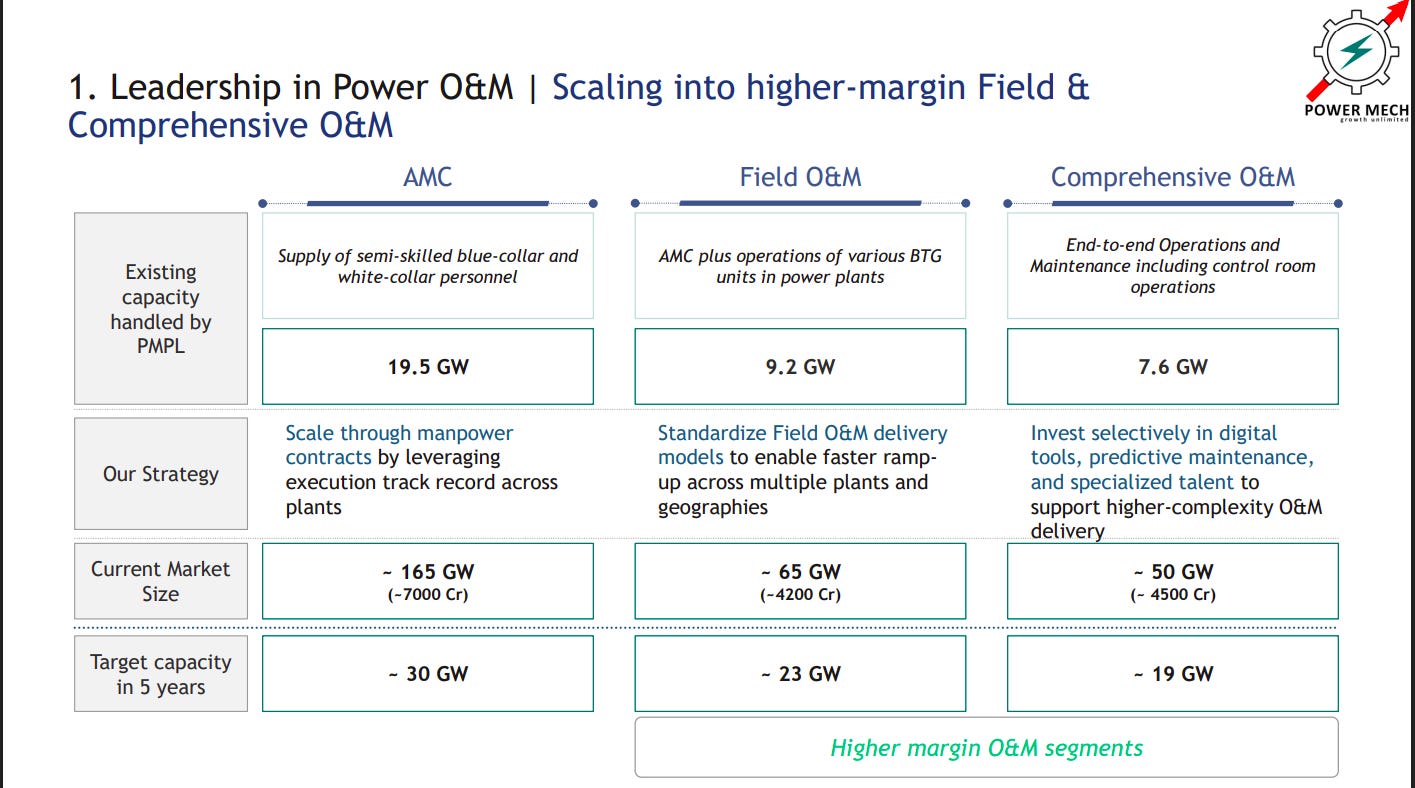

Power Mech has a strong presence in Operations & Maintenance (O&M) across power plants with capacities of 19.5 GW (AMC), 9.2 GW (Field O&M), and 7.6 GW (Comprehensive O&M). The strategy focuses on scaling higher-margin O&M services using standardized delivery models, digital tools, and predictive maintenance.

Power Mech is leveraging opportunities across power EPC, O&M, civil infrastructure, and mining operations to drive scalable growth. Strong industry tailwinds such as rising power demand, infrastructure capex, and energy-transition minerals are expected to support long-term revenue expansion.

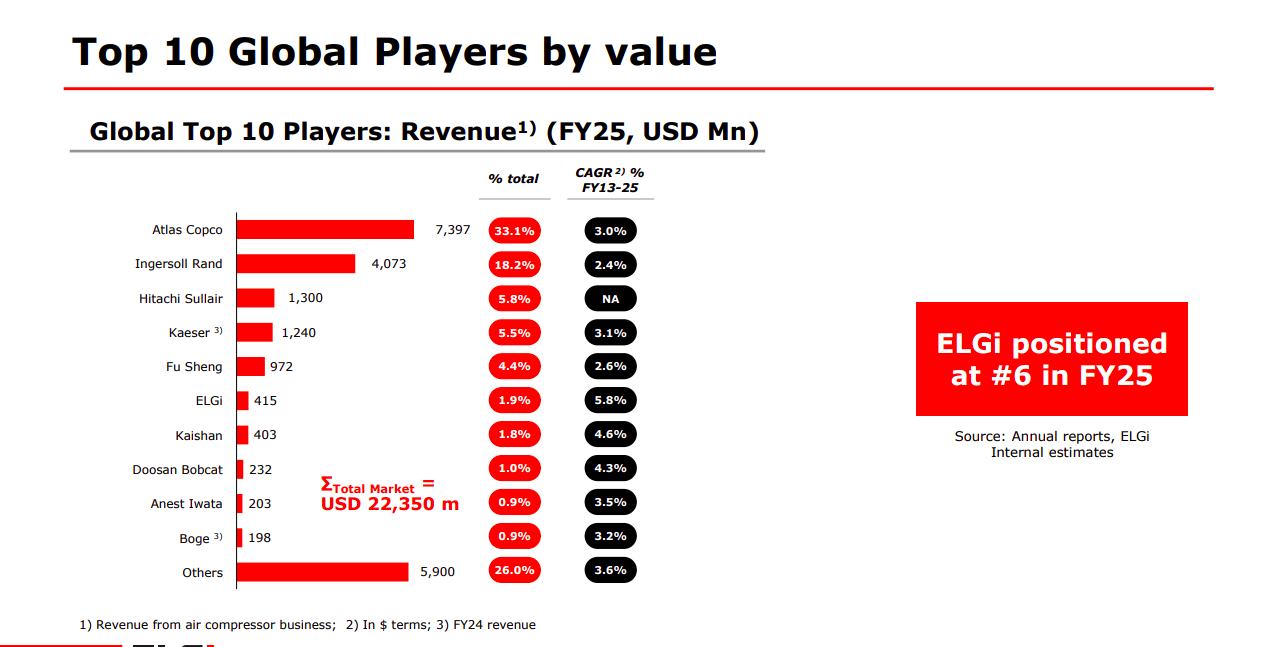

Elgi Equipments | Small Cap | Engineering & Capital Goods

Elgi Equipments Limited is a global leader in manufacturing innovative and technologically advanced compressed air systems. They offer a wide range of products including rotary screw compressors, reciprocating compressors, centrifugal compressors, dryers, filters, and accessories. With a focus on productivity and low cost of ownership, their solutions are widely used across various industries.

The global air compressor market is led by players such as Atlas Copco and Ingersoll Rand, with ELGi ranked #6 globally in FY25 with revenues of about $415 million. The total market size stands at roughly $22.35 billion, highlighting a highly competitive but large industry landscape.

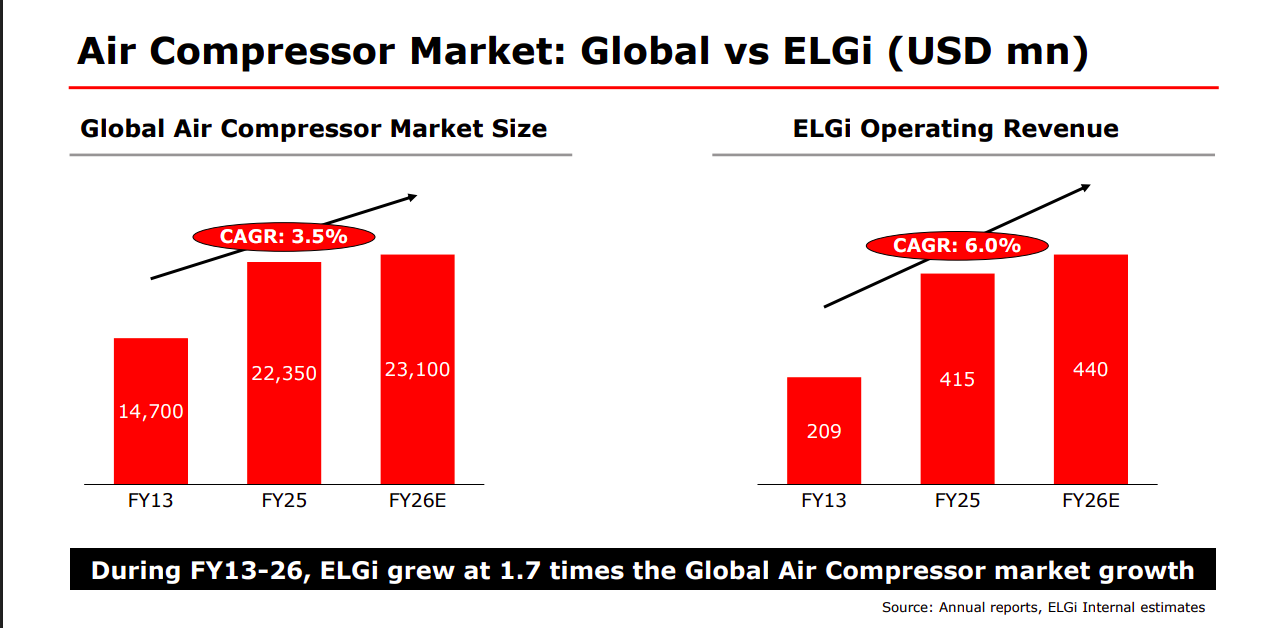

The global air compressor market has grown at a 3.5% CAGR from FY13–FY26, while ELGi’s revenues have expanded faster at around 6% CAGR. This implies ELGi has grown ~1.7x faster than the global market, indicating market share gains.

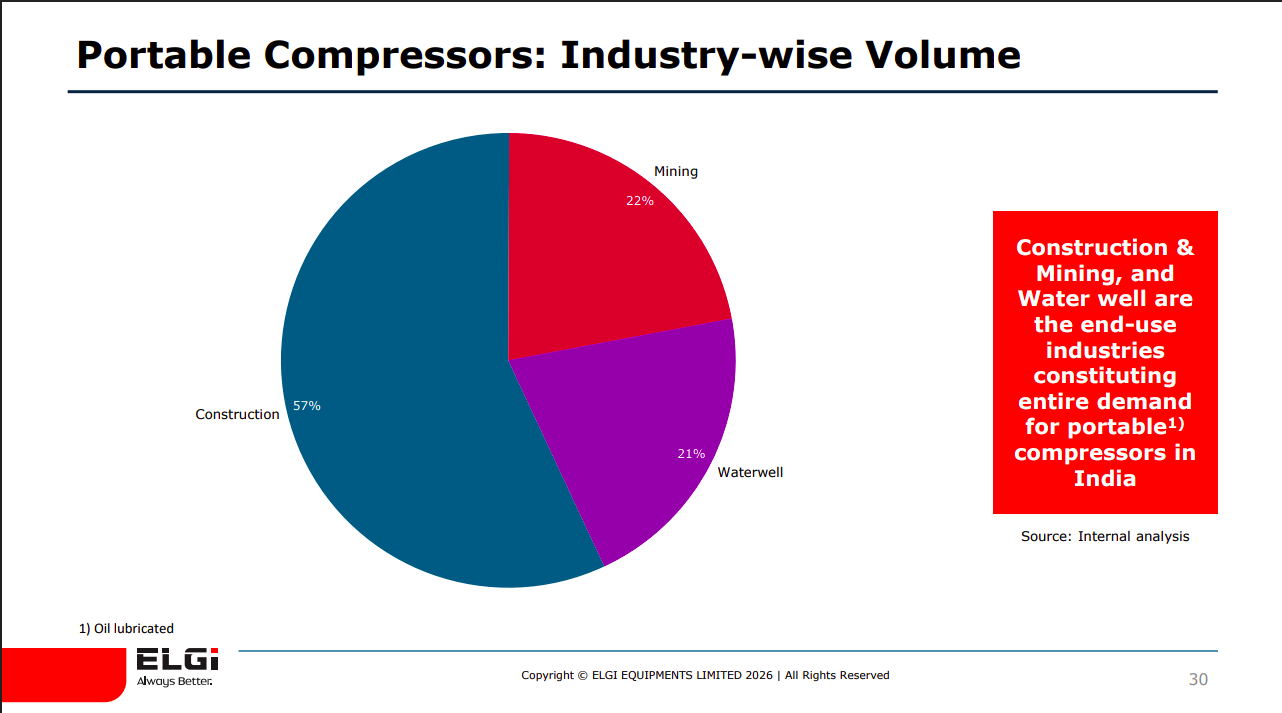

Portable compressors are primarily used in construction (57%), followed by mining (22%) and water well drilling (21%). These three sectors collectively account for the majority of demand, especially in infrastructure and resource extraction activities.

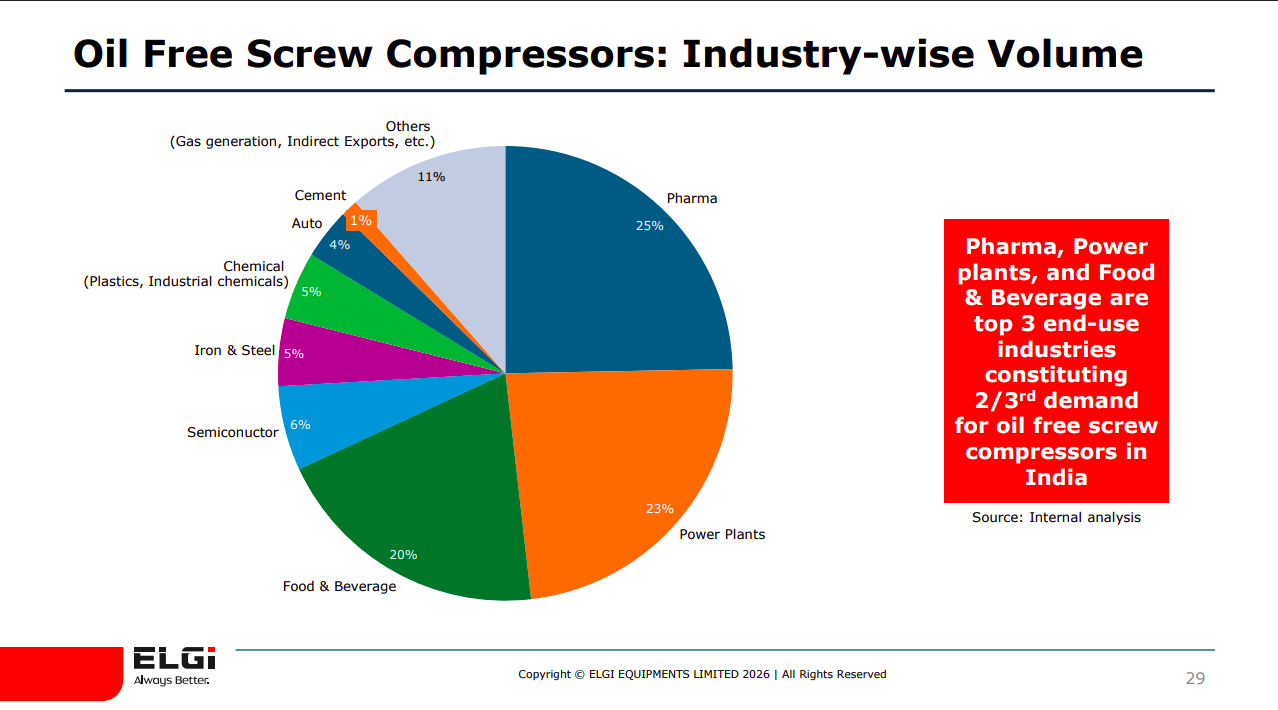

Demand for oil-free screw compressors is dominated by pharma (25%), power plants (23%), and food & beverage (20%). These industries require contamination-free compressed air, making oil-free technology critical.

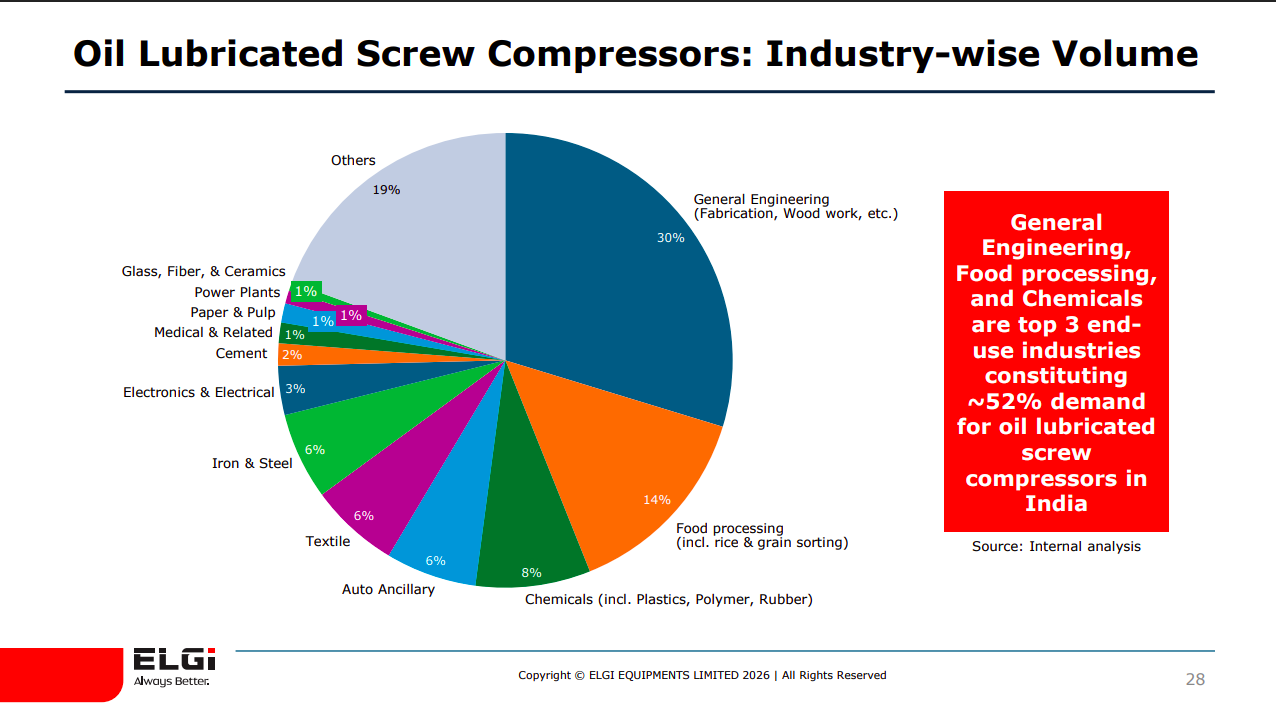

Oil-lubricated compressors see the highest demand from general engineering (30%), food processing (14%), and chemicals (8%). These sectors together contribute roughly half of total demand for this compressor category.

Compressed air systems are widely used across industries including automotive, textiles, pharma, electronics, food processing, oil & gas, mining, power, and construction. This broad applicability makes the air compressor market deeply linked to overall industrial activity and manufacturing growth.

Fabtech Technologies | Micro Cap | Engineering & Capital Goods

Fabtech Technologies provides end-to-end engineering solutions for pharmaceutical projects, including design, procurement, installation, and testing. Specializing in greenfield projects, it serves pharmaceutical, healthcare, and biotech clients globally, with a strong focus on emerging markets.

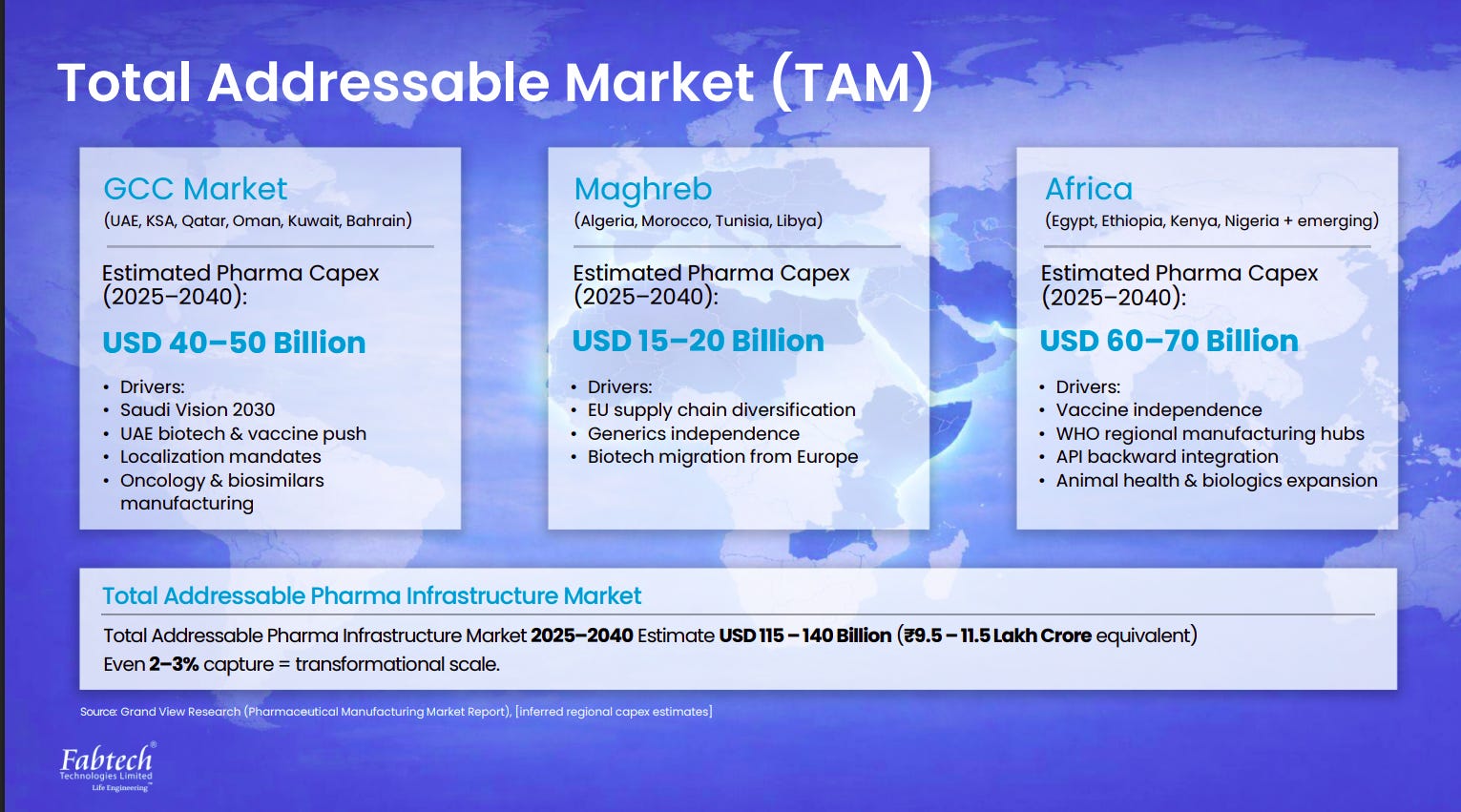

The global pharma infrastructure opportunity across GCC, Maghreb, and Africa is estimated at $115–140 billion between 2025–2040. Even capturing 2–3% of this market could be transformational, driven by regional pharma manufacturing expansion and supply chain localization.

The company currently has ~₹926 crore of confirmed orders ready for execution, providing near-term revenue visibility. Post its European acquisition, management expects pipeline conversion rates to improve to 10–20%, strengthening future order inflows.

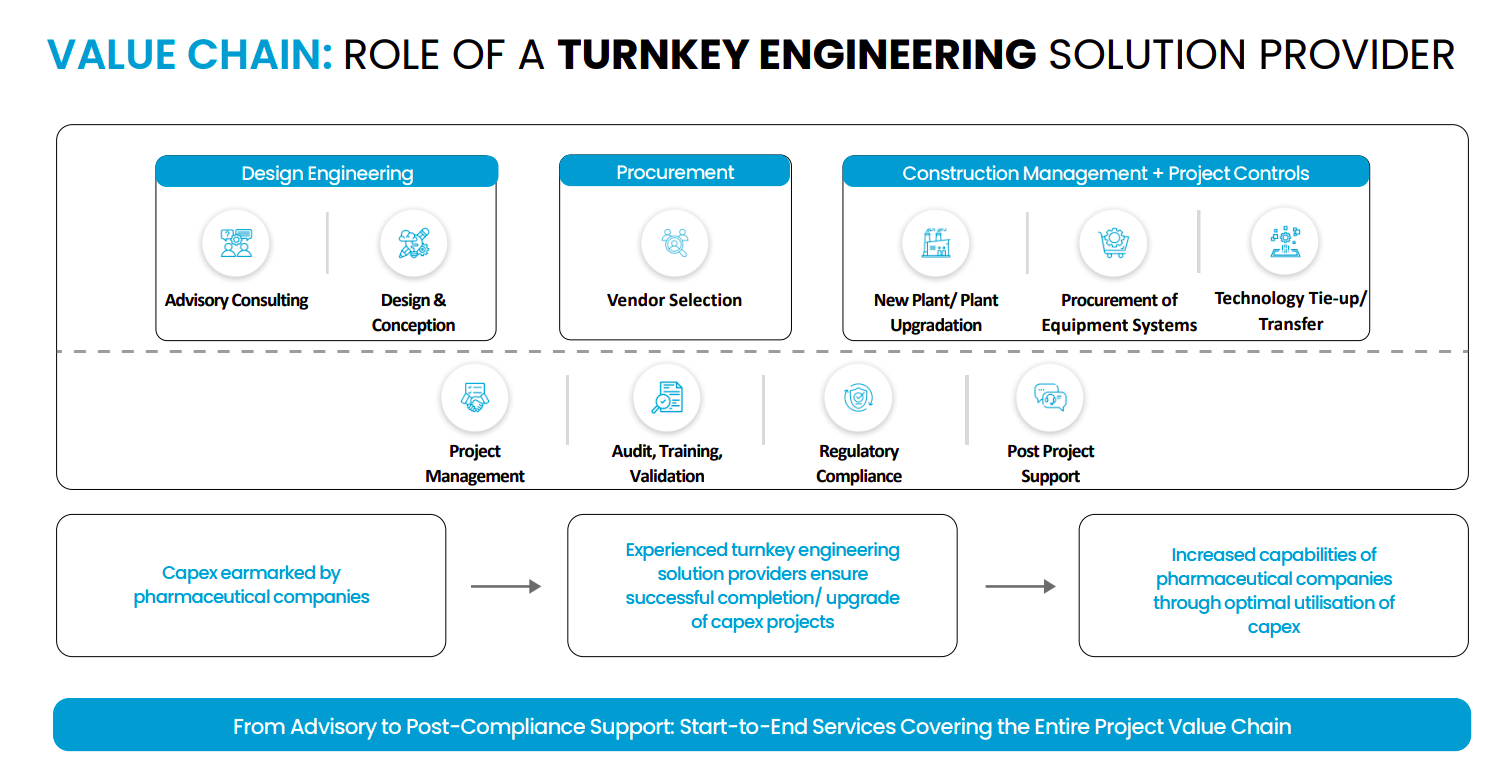

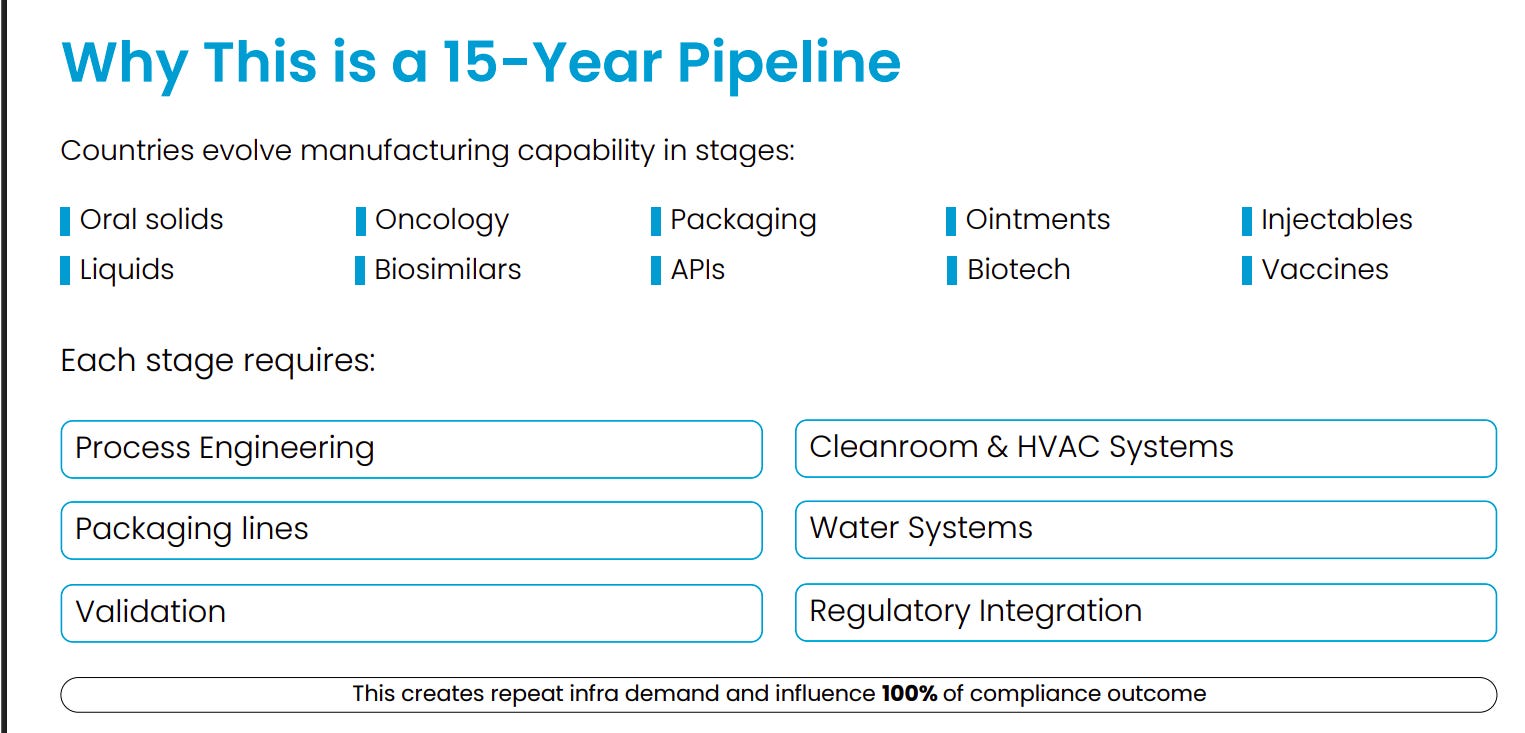

The company provides end-to-end turnkey engineering solutions across the pharmaceutical value chain, covering design, procurement, construction management, regulatory compliance, and post-project support. This integrated approach helps pharma companies efficiently execute and upgrade manufacturing facilities.

Pharmaceutical manufacturing evolves in stages—from oral solids and APIs to biologics and vaccines, creating long-term infrastructure demand. Each stage requires specialized engineering capabilities such as cleanrooms, HVAC systems, packaging lines, water systems, and regulatory validation.

Praj Industries | Small Cap | Engineering & Capital Goods

Praj Industries Limited is a global leader in providing solutions in biofuels, biomaterials, energy transition, critical process equipment, high purity water systems, brewery & beverages, and zero liquid discharge systems. They are at the forefront of the bioeconomy in India, with initiatives like Bio-Mobility and Bio-Prism focusing on biobased feedstock and sustainable product development.

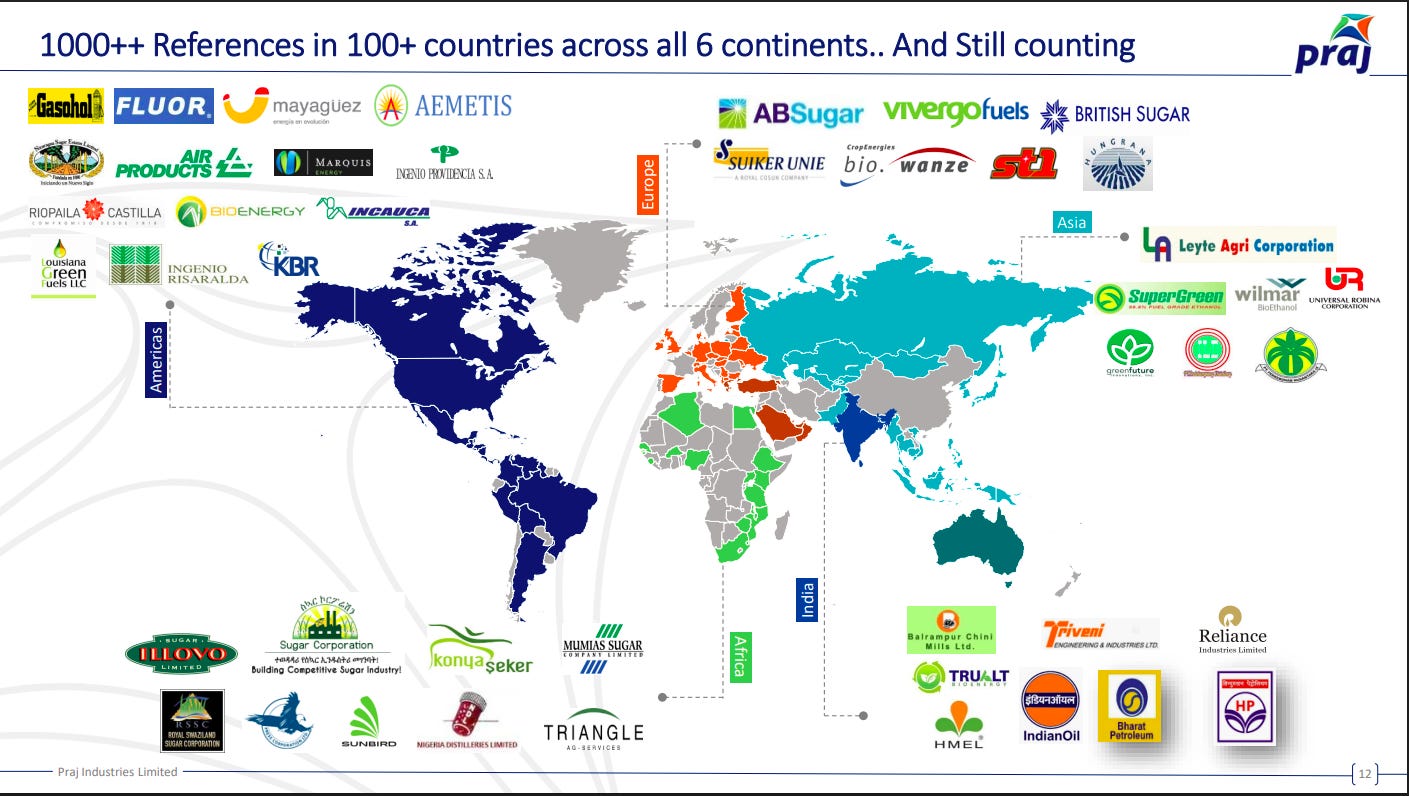

Praj has established a strong global footprint with 1000+ project references across 100+ countries spanning all six continents. The company works with leading global clients in biofuels, energy, and sugar industries, demonstrating its scale and international credibility.

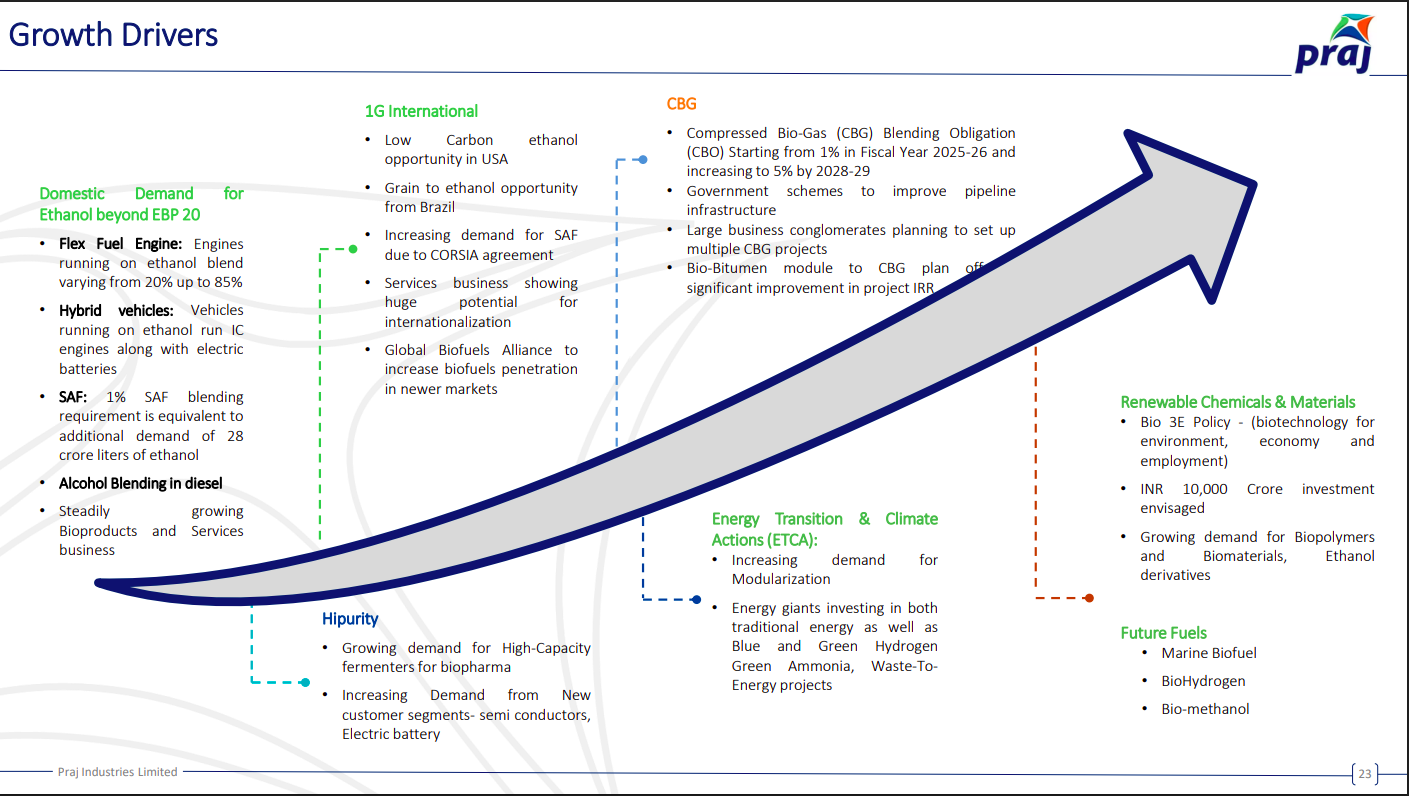

Praj’s growth is driven by increasing global demand for ethanol blending, sustainable aviation fuel (SAF), compressed biogas (CBG), and energy transition technologies. Additional opportunities are emerging in renewable chemicals, bio-based materials, and future fuels such as biohydrogen and biomethanol.

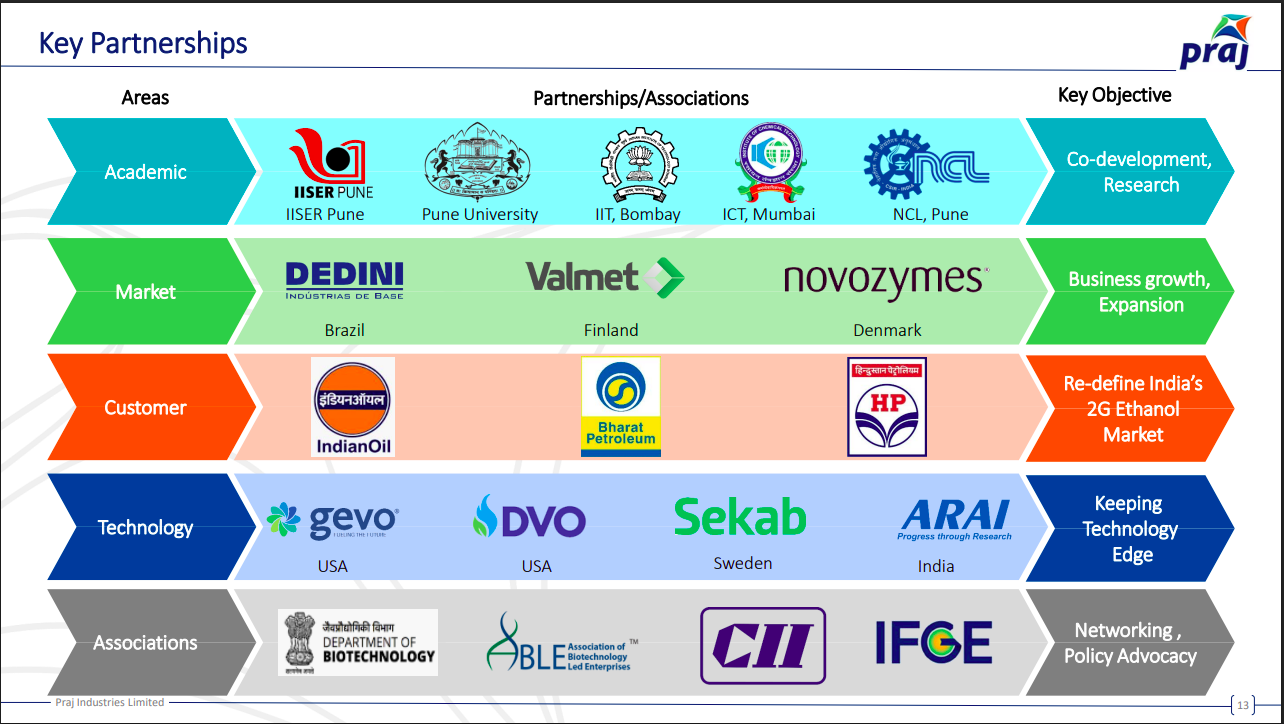

Praj has built strong collaborations across academia, technology partners, global markets, and major customers to strengthen innovation and market expansion. Partnerships with institutions, energy companies, and technology firms help accelerate R&D, biofuel adoption, and advanced biotech solutions.

DC Infotech and Communication | Micro Cap | Engineering & Capital Goods

DC Infotech and Communication Limited is a company involved in the reselling and distribution of computers and peripherals. They follow a broad-based distribution model, dealing with multiple brands and products such as networking, security, desktop virtualization, digital signage, and various IT solutions.

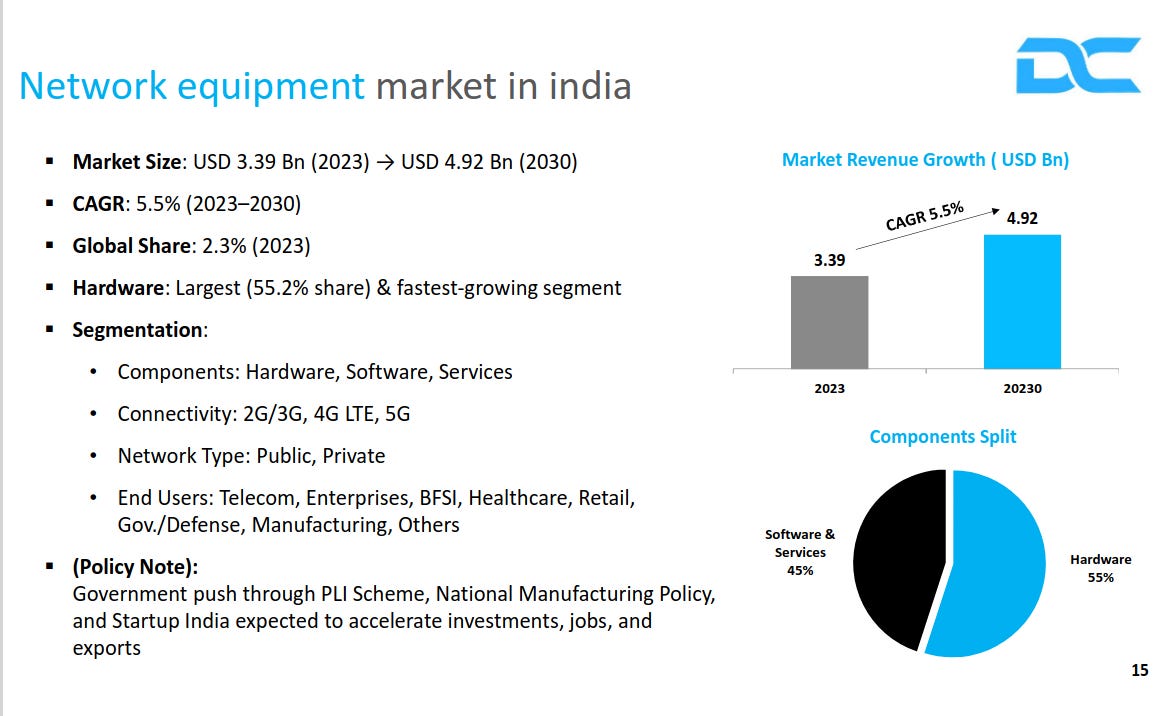

India’s network equipment market is projected to grow from $3.39B in 2023 to $4.92B by 2030 (5.5% CAGR). Hardware remains the largest segment, while government initiatives such as PLI and national manufacturing policies are expected to boost domestic production and technology investments.

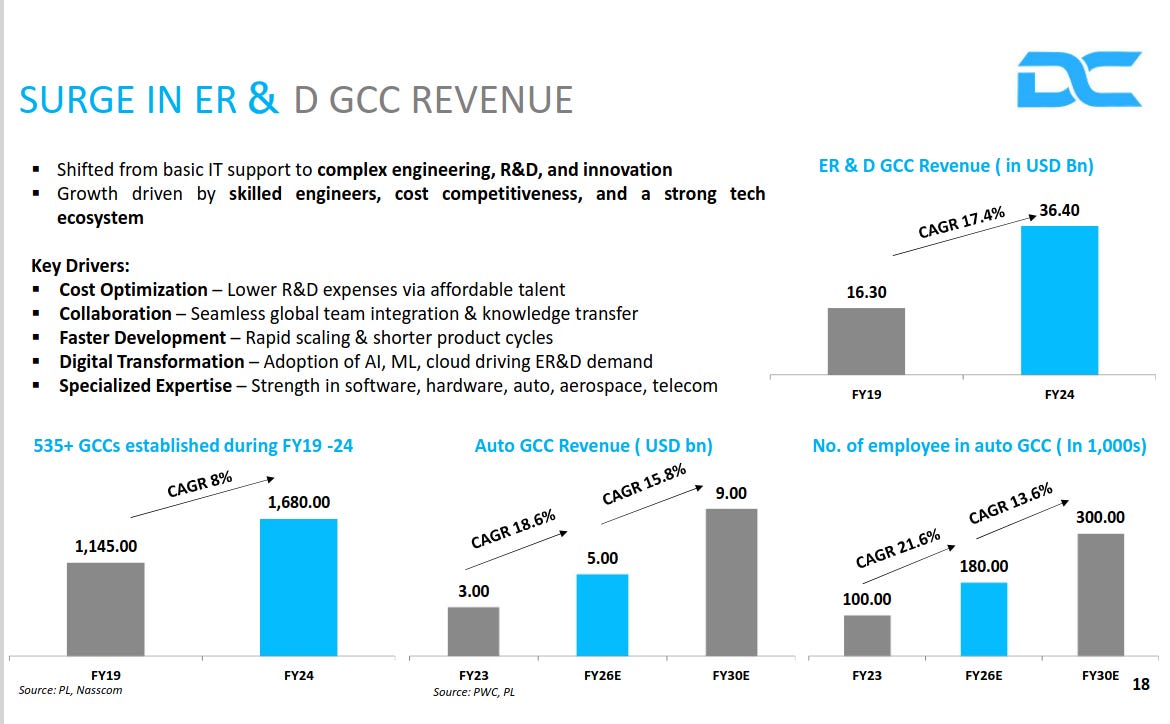

Engineering, R&D, and design GCCs in India are expanding rapidly as companies move from basic IT support to advanced engineering and innovation work. ER&D GCC revenues grew from $16.3B in FY19 to $36.4B in FY24 (17.4% CAGR), driven by skilled talent, cost advantages, and digital transformation.

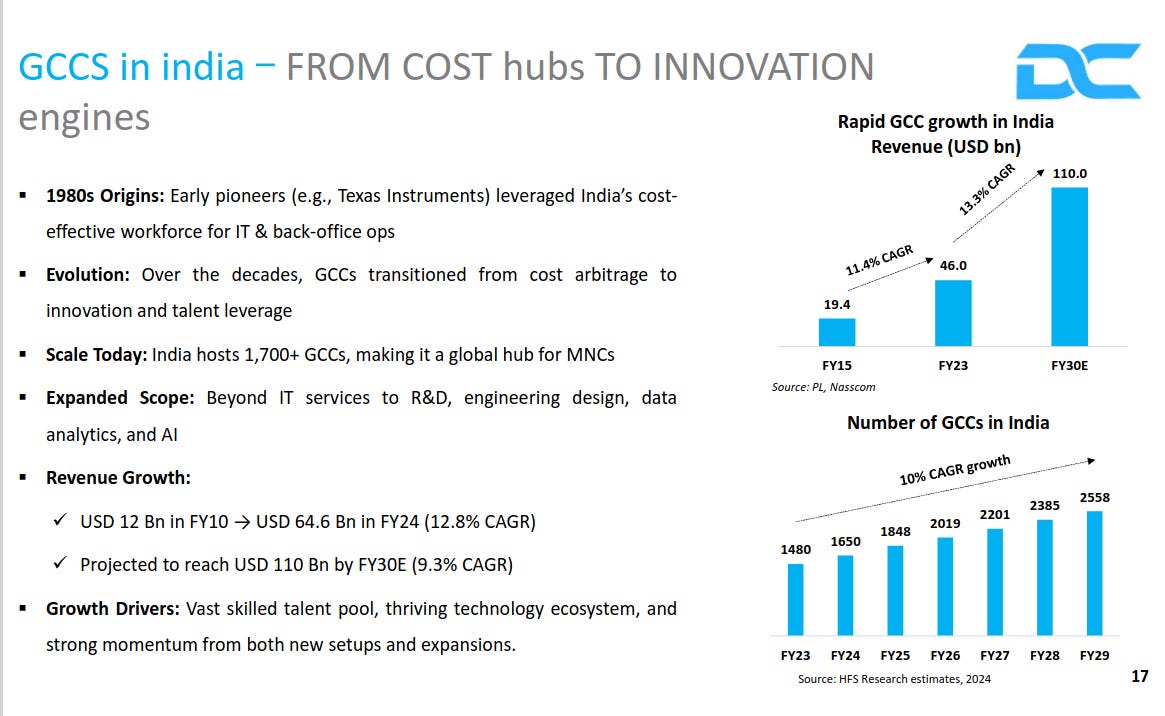

India’s GCC ecosystem has evolved from back-office cost centers to global innovation and R&D hubs, hosting over 1,700 GCCs. Revenue is expected to grow from $46B in FY23 to $110B by FY30, supported by a strong talent pool and expanding engineering, AI, and analytics capabilities.

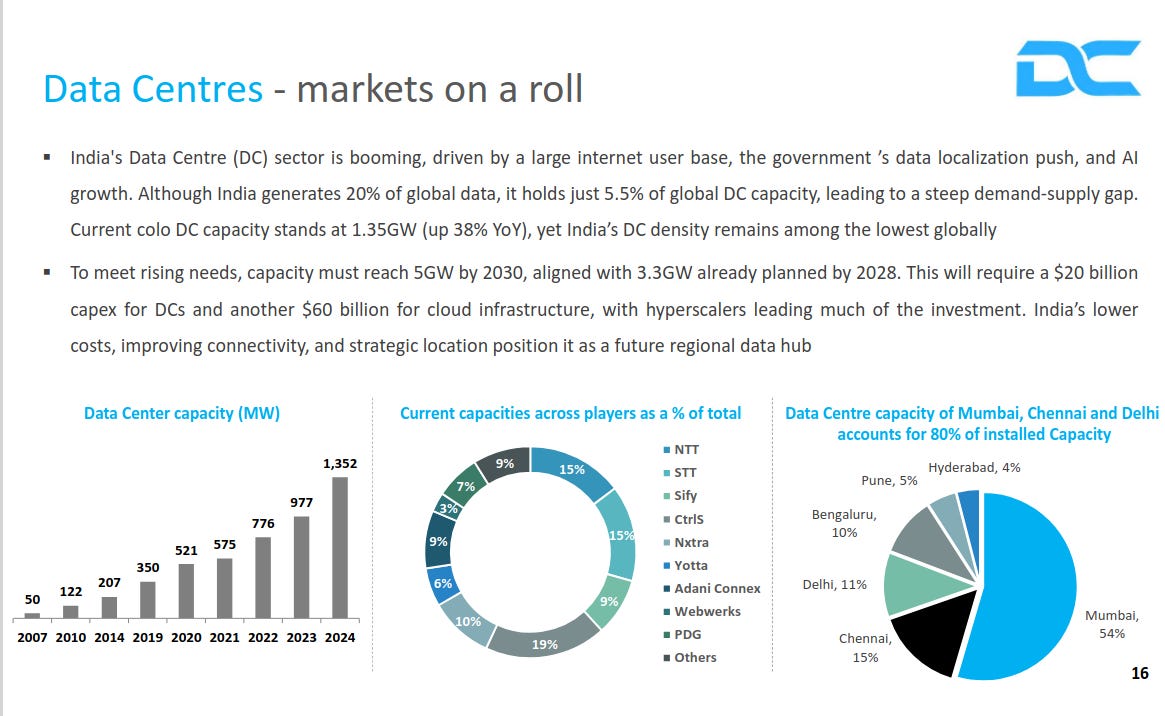

India’s data centre sector is growing quickly due to data localization policies, AI adoption, and rising internet usage. Capacity has surged to ~1.35 GW, and is expected to reach ~5 GW by 2030, requiring significant investments in data and cloud infrastructure.

Schaeffler India Limited | Mid Cap | Engineering & Capital Goods

Schaeffler India is a leading manufacturer of high-precision components and systems for the automotive and industrial sectors. It maintains a strong market position through its specialized bearings and motion technology solutions for both domestic and export markets.

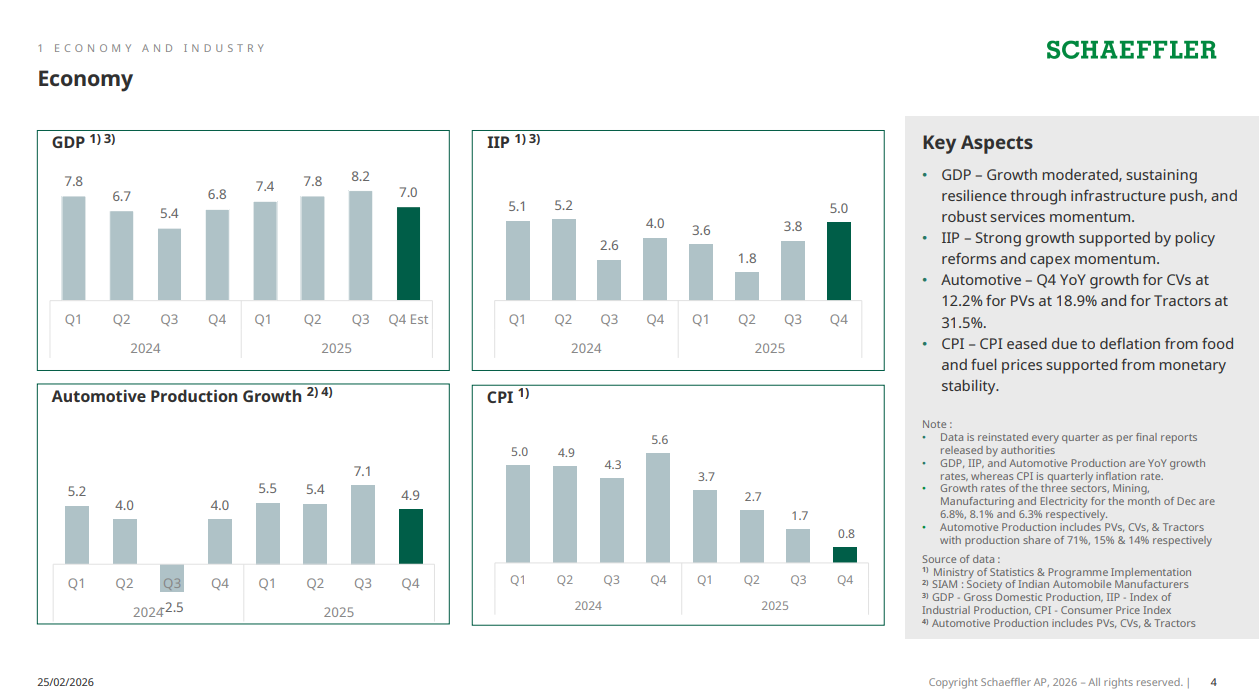

India’s GDP growth picked up to 8.2% in Q3 2025 before easing slightly to an estimated 7.0% in Q4, while industrial production (IIP) rebounded sharply to 5.0% in Q4 2025 after a soft patch mid-year. Automotive production growth came in at 4.9% in Q4 2025, cooling from 7.1% the previous quarter, with tractors leading the segment at 31.5% YoY growth. On the inflation front, CPI dropped to just 0.8% in Q4 2025, helped by falling food and fuel prices — a sign that price pressures are well under control for now.

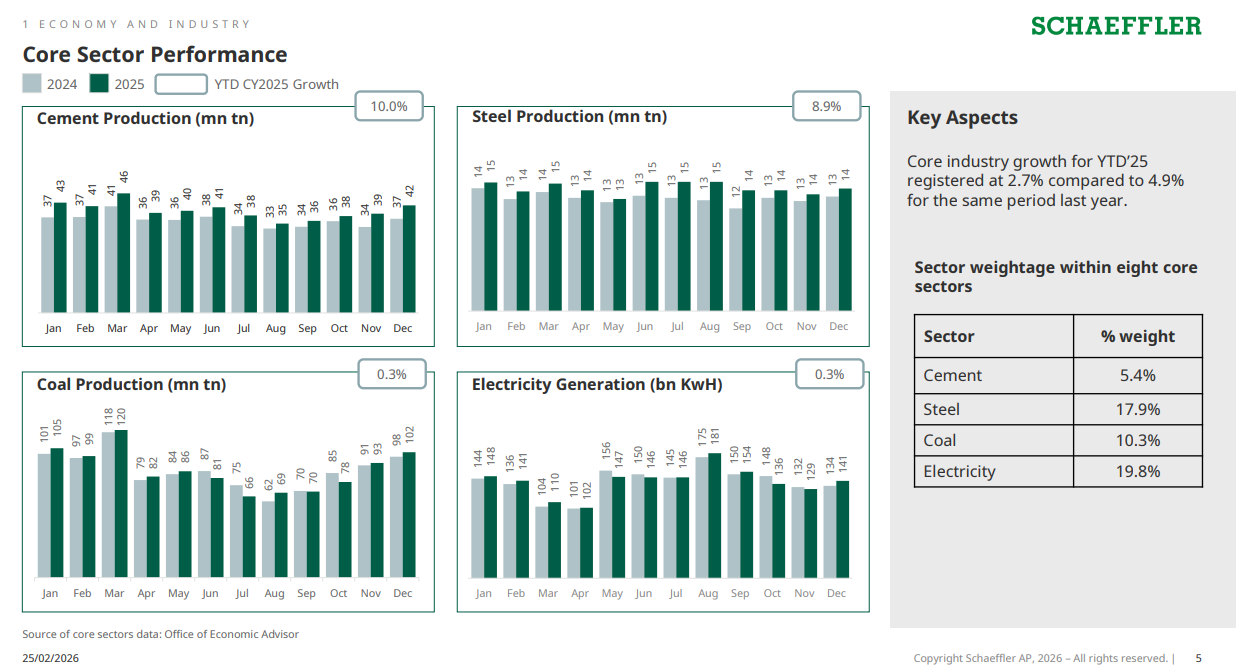

Core industry growth slowed to 2.7% in YTD 2025, down from 4.9% in the same period last year — a noticeable cooldown. Cement and steel production were the brighter spots, posting YTD CY2025 growth of 10.0% and 8.9% respectively, while coal and electricity generation barely moved at 0.3% each. Together, these four sectors carry over 53% weightage in the eight core industries, so their performance is a useful pulse check on India’s broader industrial momentum.

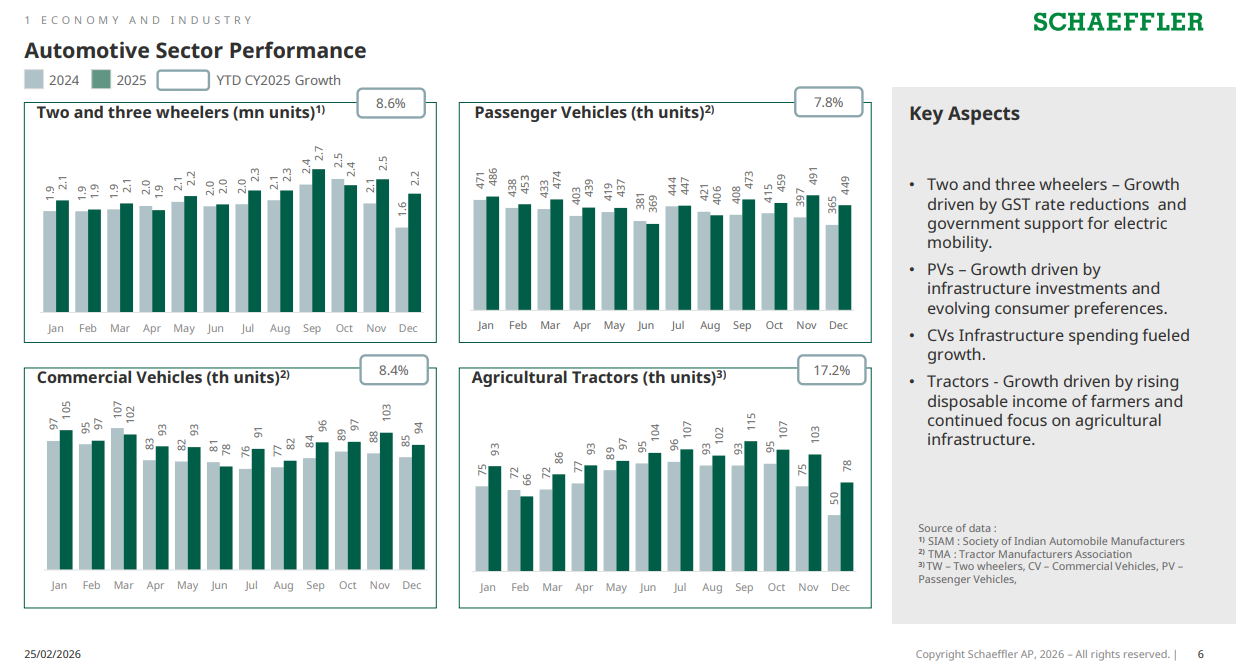

India’s automotive sector posted broad-based growth in CY2025, with two and three wheelers up 8.6% YTD — helped by GST rate cuts and the push toward electric mobility. Passenger vehicles grew 7.8% and commercial vehicles 8.4%, both riding on infrastructure spending and evolving consumer demand. The standout was agricultural tractors at 17.2% YTD growth, driven by rising farmer incomes and continued government focus on agricultural infrastructure.

FMCG

Marico Limited | Mid Cap | FMCG

Marico is a leading Indian consumer goods company specializing in health, beauty, and wellness products with a strong international presence. It is currently executing a strategic pivot from commodity-linked staples toward a high-margin, digital-first portfolio of premium brands.

Rapid expansion in digital payments and the D2C market provides a structural tailwind for the pivot toward premium categories. This strategic shift aims to reduce the company’s long-term sensitivity to mass-market commodity price fluctuations.

Acquiring brands like Plix and Cosmix shifts the portfolio toward functional wellness categories with higher price points and inelastic demand. These integrations are central to improving overall unit economics and building stronger brand loyalty.

The 4700BC acquisition demonstrates a scalable model for premium niche brands, supported by a 45% digital sales mix. High digital penetration allows these acquired brands to bypass traditional retail hurdles and reach profitable scale more efficiently.

The Beardo acquisition has achieved 1900 bps in EBITDA margin expansion, validating Marico’s ability to scale digital-first brands profitably. Success in this segment demonstrates a viable path for growth beyond the company’s core legacy portfolio through supply chain and marketing synergies.

Marico’s 6x scale-up of the Plix brand showcases a repeatable playbook for capturing high-growth nutraceutical niches via content-led marketing. This vertical provides a strategic growth cushion that helps offset the inherent cyclicality of mass-market commodity categories.

Avanti Feeds Limited | Small Cap | FMCG

Avanti Feeds is a leading Indian manufacturer of shrimp feed and a major exporter of processed shrimp to global markets. The company operates through a vertically integrated model serving the aquaculture industry from feed production to value-added exports.

Shrimp processing revenue grew 36.8%, offsetting a 9.6% decline in the core shrimp feed segment. This mix shift indicates a successful transition toward value-added exports despite softer demand for agricultural inputs.

Processing EBITDA margins expanded to 13% from 8% YoY, driven by improved pricing and lower freight costs. Maintaining these gains is essential for the segment to transition from a volume-led model to a sustainable margin driver.

North America accounts for 64.5% of processed shrimp sales, highlighting significant geographical concentration risk. This high exposure makes the business highly sensitive to U.S.

Processed shrimp EBITDA margins have stabilized at 13.5%, nearly double the levels seen in late FY25. This sustained inflection confirms that operational efficiencies and currency benefits are materially boosting export division earnings.

Shrimp processing volumes are nearing total FY25 levels, signaling a strategic pivot toward higher-value export markets. This shift improves earnings quality by providing a buffer against domestic shrimp farming volatility.

Shrimp feed margins have structurally rebounded to nearly 18%, signaling the end of severe raw material cost pressures. The core business has successfully restored its pricing power and operational efficiency.

Pharmaceuticals

Sanofi India Limited | Mid Cap | Pharmaceuticals

Sanofi India is a major pharmaceutical player specializing in insulin and chronic care therapies like cardiology and neurology. The company is currently transitioning to a leaner, partnership-focused model to drive efficiency and focus on its market-leading diabetes franchise.

Prioritizing the Insulin franchise while partnering legacy brands reduces sales overhead without sacrificing market reach. This shift focuses resources on high-moat segments to drive long-term profitability.

A resilient market share in Lantus (man-made insulin) despite new competition demonstrates a strong brand moat. Expanding digital outreach to Tier II and III cities targets significant volume growth in under-penetrated regions.

Transitioning into specialized molecules like Teplizumab (diabetes) moves the portfolio toward high-value niche therapies. Local RWE studies for Soliqua create a data-driven competitive advantage for premium offerings.

Exiting volatile exports stabilizes earnings by prioritizing the higher-margin and more predictable domestic chronic care market. This strategy reduces reliance on global tender cycles and enhances valuation stability.

Substantial structural cost reductions are successfully offsetting flat domestic sales growth. This efficiency-led approach sustains profitability during the company’s fundamental business transformation.

Increasing the dividend payout to 87% highlights strong cash flow and the limited capital intensity of the new partnership model. This level of return signals high confidence in sustained shareholder value.

Financial Services

HDFC Life Insurance Company Limited | Large Cap | Financial Services

HDFC Life is a leading private sector life insurer in India, offering a comprehensive suite of individual and group insurance solutions. The company leverages a strong multi-channel distribution network, including major bank partnerships and an extensive agency force, to drive long-term value.

New surrender value regulations and GST impacts are meaningful drags, reducing new business margins by a combined 1.3 percentage points. Scaling the revised product profile is critical to recapturing these margin points through higher-value sales.

Multi-year market share gains and consistent compounding of embedded value validate the strength of a diversified distribution model. This sustained performance across different market cycles demonstrates strong long-term terminal value potential.

Expanding into complex savings and annuity products signals a strategic shift to capture more household wealth. This diversification helps stabilize earnings by reducing reliance on mortality-related risks.

Scaling AI in onboarding and claims processing helps decouple business growth from headcount and operational costs. These efficiencies are critical for defending margins as the company expands into lower-ticket markets.

While persistency is stable across most channels, the sharp drop in 61st-month retention for unit-linked products signals high sensitivity to market cycles. Managing long-term retention in this segment remains a key challenge.

The significant drop in brand recall from Tier 1 to Tier 3 markets highlights a major hurdle for rural expansion. Closing this awareness gap is vital as metropolitan markets approach saturation.

Rapid growth in retail credit creates a structural opportunity for credit-linked protection products as insurance attachment rates rise. Deepening retail indebtedness makes the protection segment a more durable growth engine that is less sensitive to discretionary savings trends.

The massive projected gap in retirement savings indicates a multi-decade runway for annuity and pension products as India’s population ages. Success in this segment will depend on product innovation that addresses longevity risk while maintaining capital efficiency.

Fino Payments Bank Limited | Small Cap | Financial Services

Fino Payments Bank operates a high-volume, digital-first financial services platform focused on transaction banking and remittances for the unbanked population. It utilizes a vast merchant-led distribution network to maintain an asset-light model and is currently transitioning into a Small Finance Bank.

Reaching majority digital throughput allows the bank to scale volumes without proportional increases in physical overhead. This transition creates significant operating leverage and improves long-term cost efficiency.

Renewal revenue reaching 14% of the mix confirms deepening customer stickiness and a shift toward a primary banking relationship. Growing average balances indicate the bank is capturing a larger share of customer wealth.

Achieving a 1.7% cost of funds at record deposit levels provides a formidable competitive edge in liability gathering. This low-cost funding base is a critical strategic pillar for the bank’s intended Small Finance Bank transition.

UPI-active customers maintain triple the average balances of non-digital users and show significantly higher engagement. Digital adoption is the most effective lever for building a stable, high-value deposit base with superior economics.

ICICI Prudential Asset Management | Large Cap | Financial Services

ICICI Prudential Asset Management is a leading Indian investment manager offering a broad suite of mutual fund and alternative investment products. It maintains a dominant market position by leveraging a vast distribution network and strong brand presence across retail and institutional segments.

Passive AUM growth of nearly 40% year-on-year highlights a structural shift toward low-cost index and ETF products in the Indian market. Achieving scale in this segment is critical for defending market share against new digital competitors.

Systematic transaction volumes more than doubling over two years signify a successful shift toward stable, annuity-like revenue streams. This growth provides a predictable floor for management fee income by securing long-term investor commitments.

Acquiring fund management rights from ICICI Venture signals a strategic expansion into high-margin private equity and venture capital. This move allows the firm to capture a larger share of institutional and high-net-worth investor portfolios.

Direct distribution reaching 28% of equity AUM reflects rising digital adoption among self-directed investors. However, the 72% reliance on intermediaries underscores the continued importance of traditional channels for driving growth in semi-urban markets.

That’s it for now! Your feedback will really help shape how Points and Figures evolves. Drop it down in the comments below!

Quotes in this newsletter were curated by Meher, Vignesh & Kashish.

Disclaimer: We’ve used AI tools in filtering and cleaning up the quotes from the images so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Points and Figures is run by the same team that creates The Daily Brief and Aftermarket Report.

The Chatter by Zerodha feels like student entering library ! thanks