Sometimes, a single slide can explain more than a long report. Points and Figures is our way of breaking down what India’s leading companies are telling their shareholders and analysts. We comb through the decks, pull out the charts and data points that actually matter, and highlight the signals behind the numbers—whether about growth plans, margins, new markets, or risks on the horizon.

This is an extension of The Chatter. While The Chatter focuses on management commentary and earnings call transcripts, Points and Figures dives into investor presentations—and soon, even annual reports—to decode what companies are showing, not just what they’re saying.

We go through every major investor presentation so you don’t have to—bringing you the sharpest takeaways that reveal not just what the company is saying, but what it really means for the business, its sector, and the broader economy.

In this edition, we have covered 15 companies across 7 industries.

Financial Services

State Bank of India

BSE

Bank of Baroda

Punjab National Bank

Engineering & Capital Goods

KRN Heat Exchanger and Refrigeration

Suzlon Energy

Texmaco Rail & Engineering

Sanghvi Movers

Chemicals

Ester Industries

Retail

PN Gadgil Jewellers

Metals

Tata Steel

Auto Ancillary

Bosch

Samvardhana Motherson International Ltd.

Automobile

Tata Motors Passenger Vehicles Ltd.

Eicher Motors Ltd.

Financial Services

State Bank of India | Large Cap | Financial Services

State Bank of India (SBI) offers a diverse range of products and services to individuals, businesses, and institutions through its extensive network. Embracing change while upholding core values like Service, Transparency, Ethics, Politeness, and Sustainability, SBI remains a leading player in the banking sector.

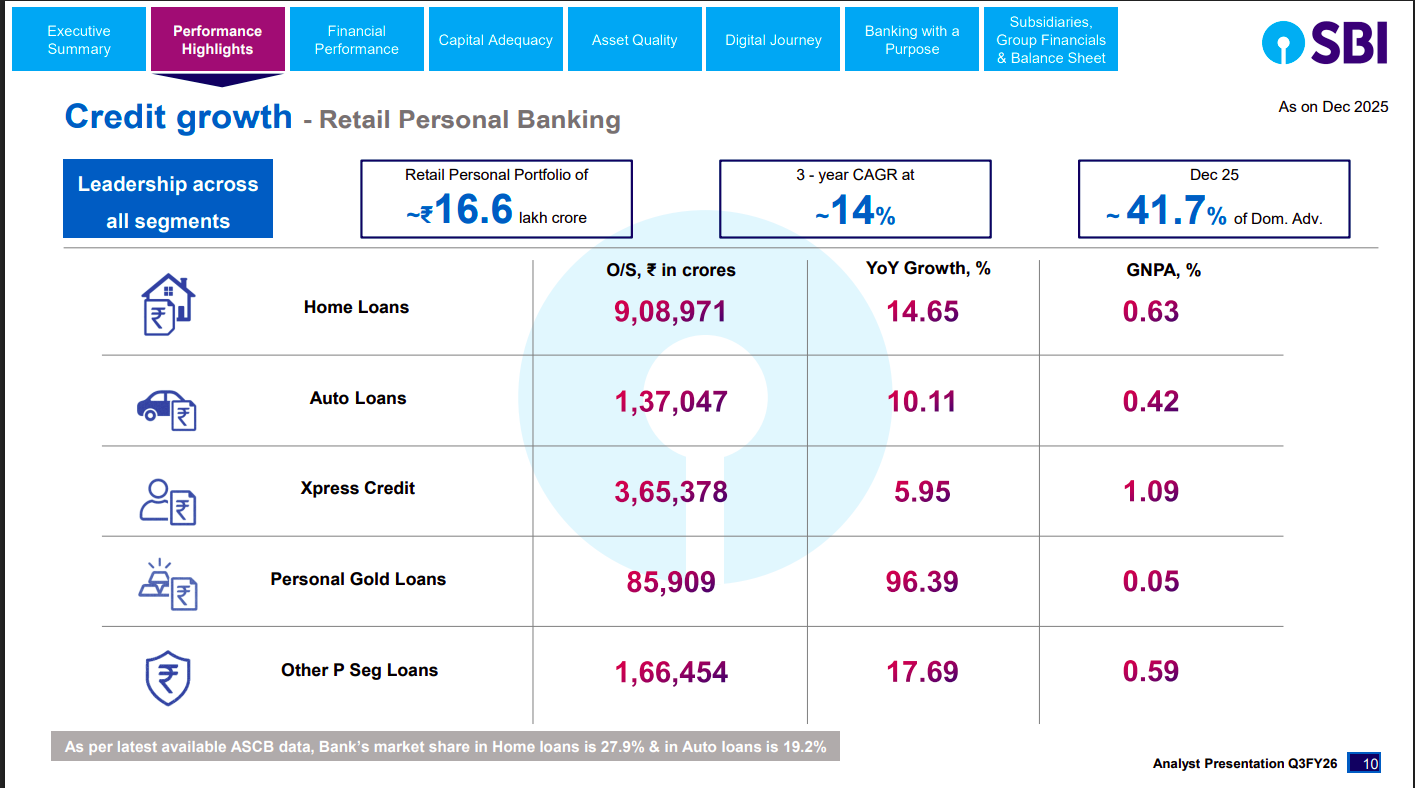

Retail personal loans continue to anchor SBI’s credit growth, with the portfolio reaching ~₹16.6 lakh crore and a 3-year CAGR of ~14%. Home loans dominate the book, while asset quality remains strong with GNPA below 1% across most segments.

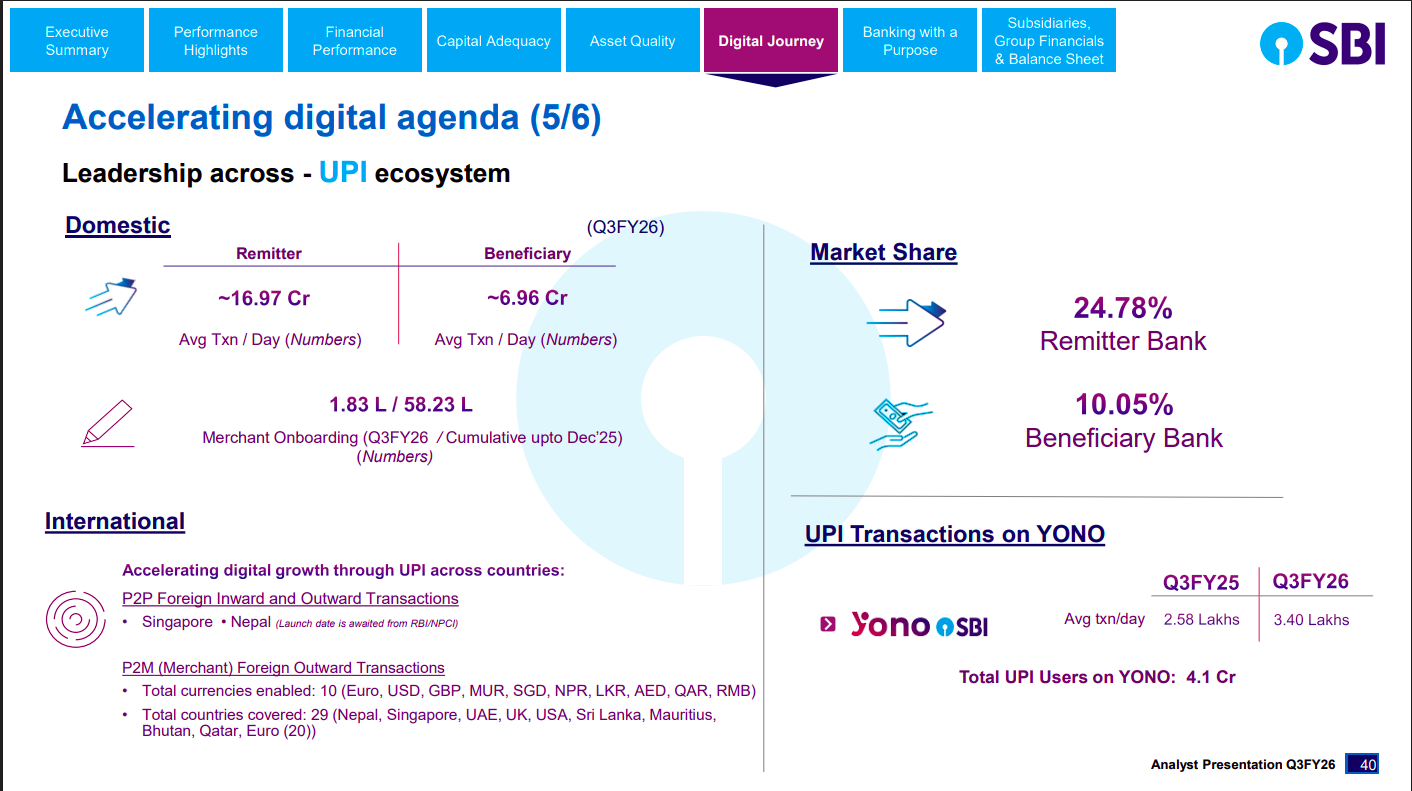

SBI retains leadership in the UPI ecosystem with ~25% remitter market share and strong growth in YONO UPI transactions. International UPI expansion and merchant onboarding continue to scale, reinforcing SBI’s digital moat.

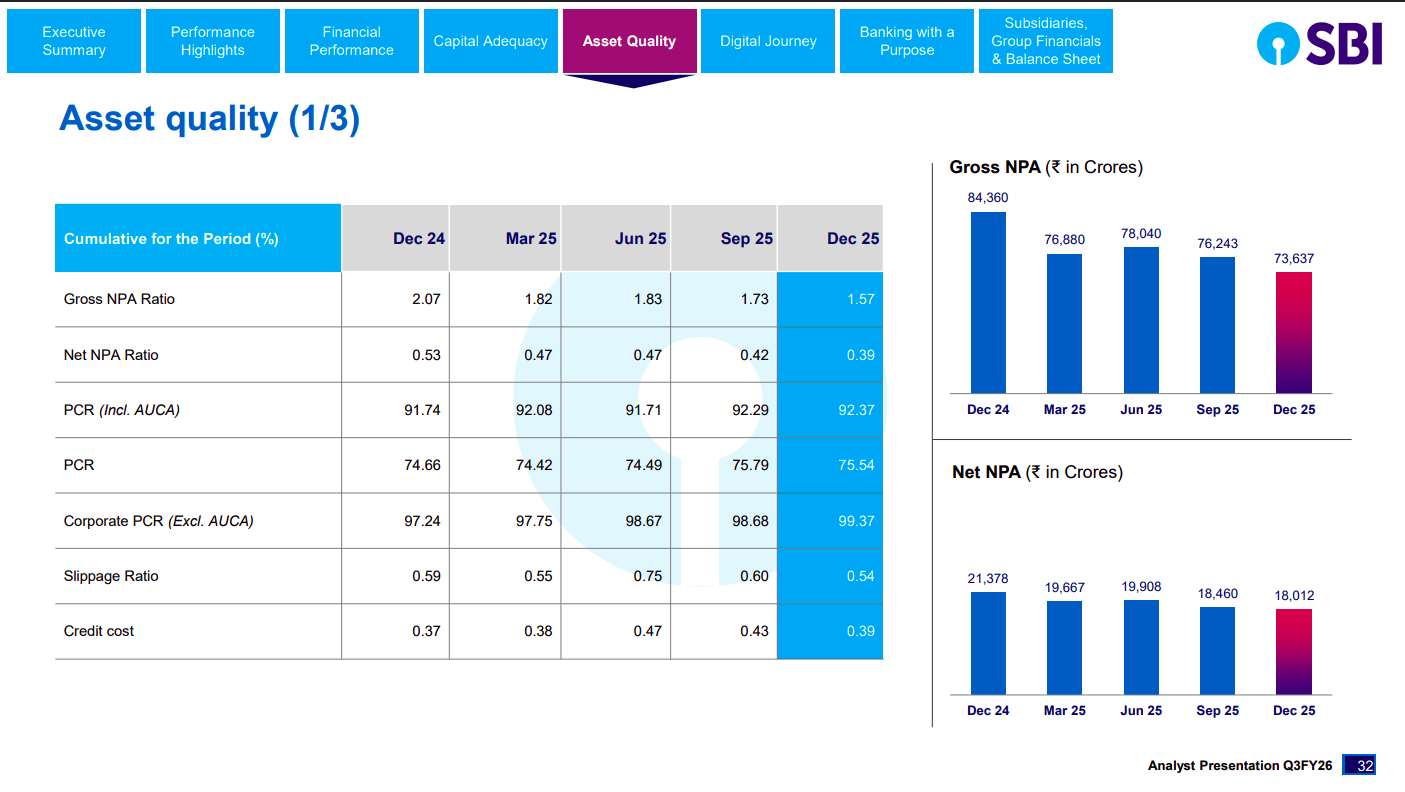

Asset quality continues to improve with GNPA declining to 1.57% and NNPA at 0.39% by Dec’25. High provision coverage ratios and lower slippages reflect sustained balance sheet strength.

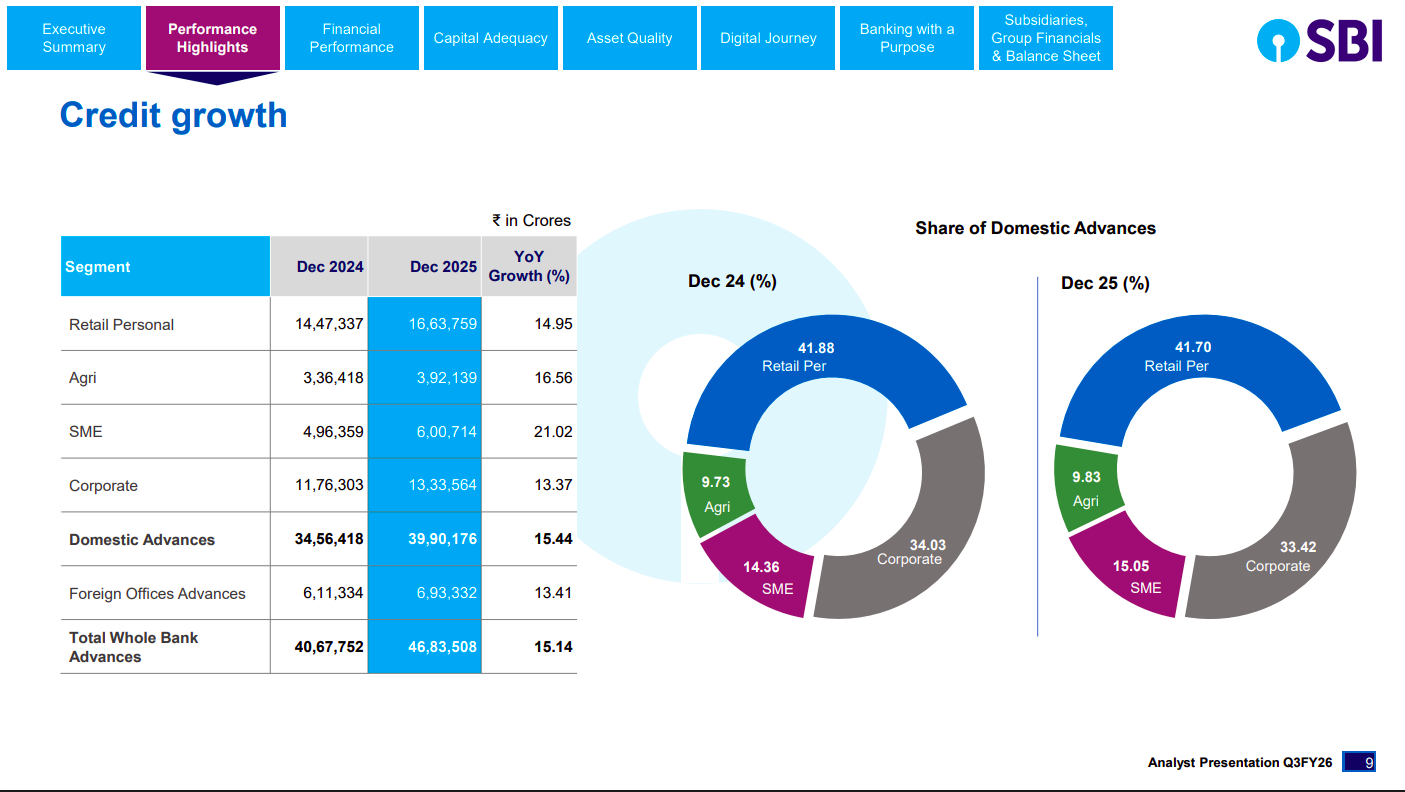

Overall advances grew ~15% YoY, driven by strong momentum in retail, SME, and agriculture segments. The mix remains stable, with retail contributing ~42% of domestic advances, underscoring a balanced growth profile.

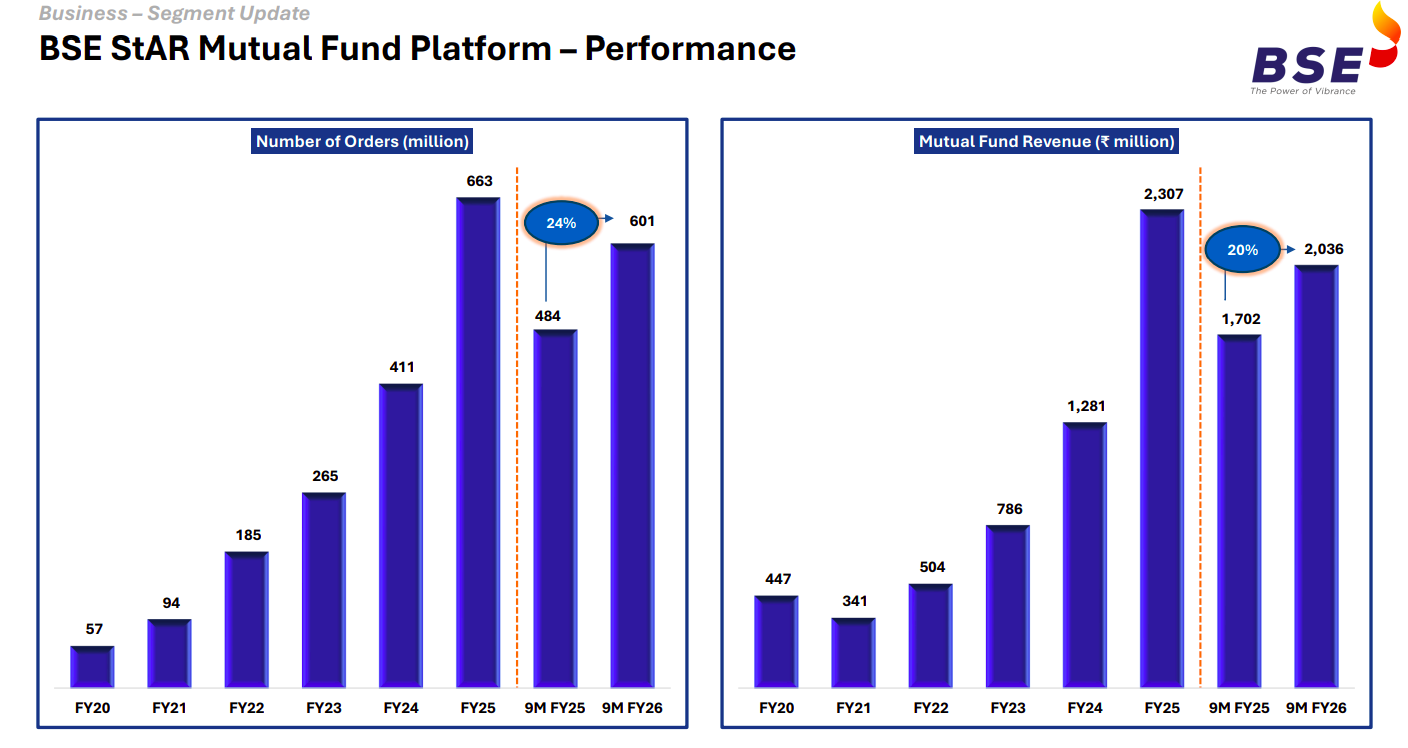

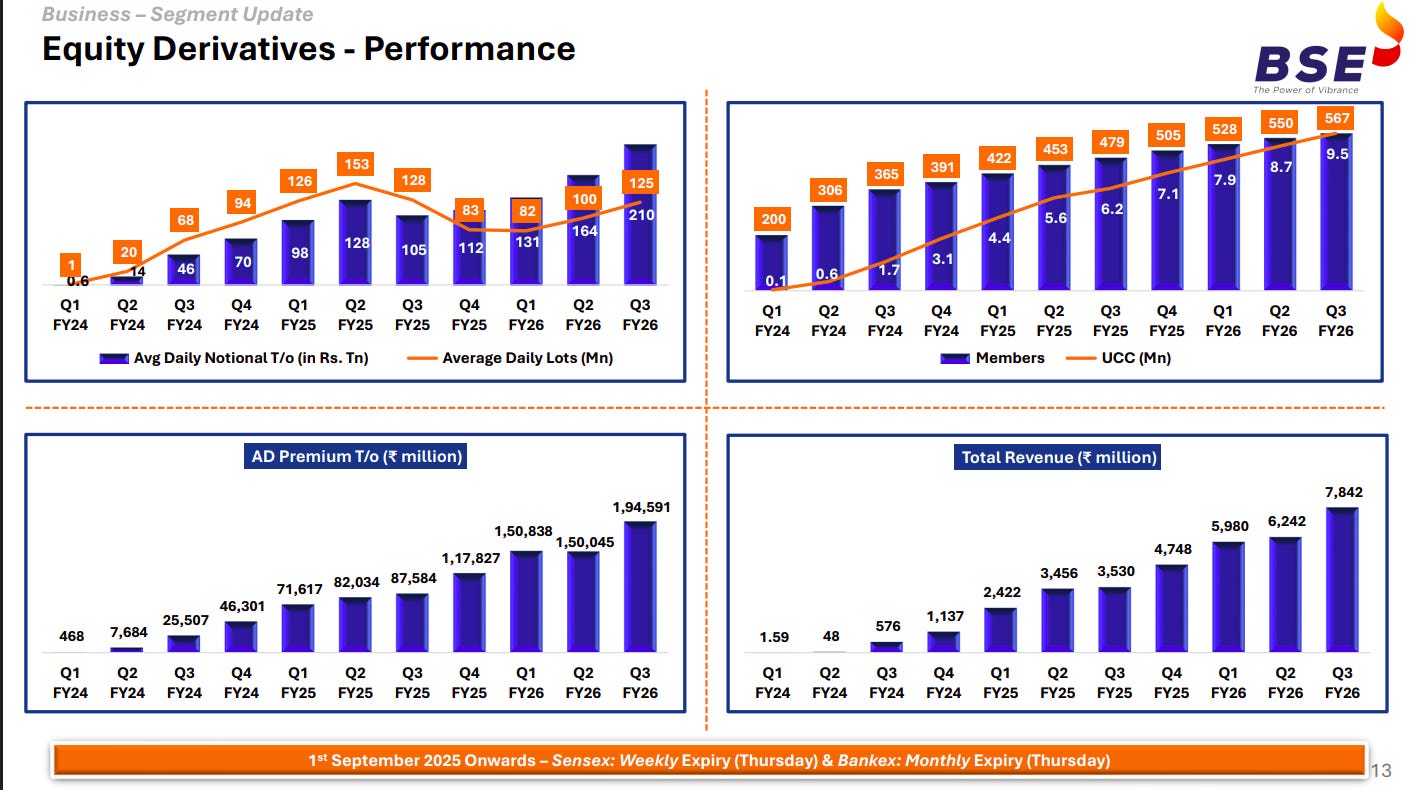

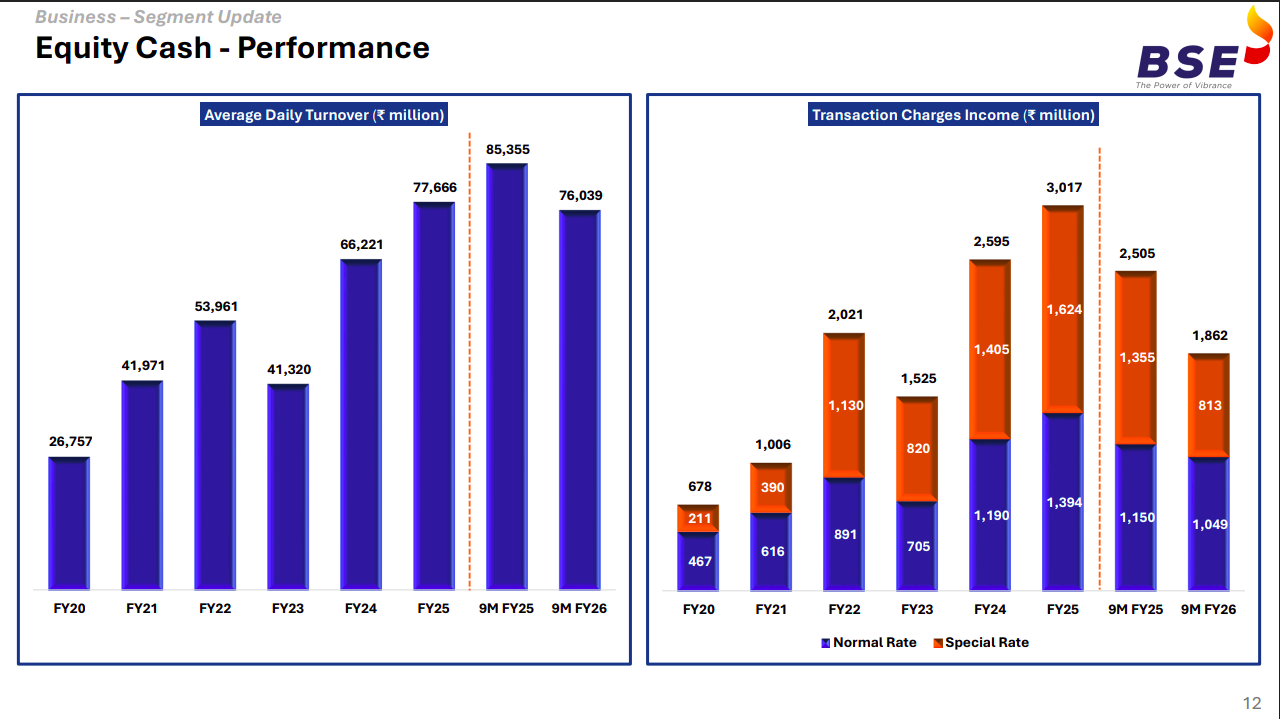

BSE | Large Cap | Financial Services

BSE Limited is the owner of the BSE exchange platform, the first stock exchange in Asia established in 1875. The company operates in listing, market, and data businesses, including primary and secondary market activities, data sales, and licensing. They also offer IT services, index product licensing, and financial training services.

BSE StAR MF continued strong scale-up, with order volumes rising ~24% YoY in 9MFY26, reflecting deeper distributor and investor adoption. Mutual fund revenues grew ~20% YoY, supported by higher transaction volumes and a steady expansion in industry participation.

Equity derivatives witnessed sharp growth, with average daily notional turnover and premium T/O scaling steadily through FY25–FY26. Rising members, UCC additions, and higher participation post new expiry structures drove total revenues to record highs.

Equity cash segment maintained healthy liquidity, with average daily turnover remaining elevated despite moderation from FY25 peaks. Transaction charge income stayed resilient, supported by a balanced mix of normal and special rate trades.

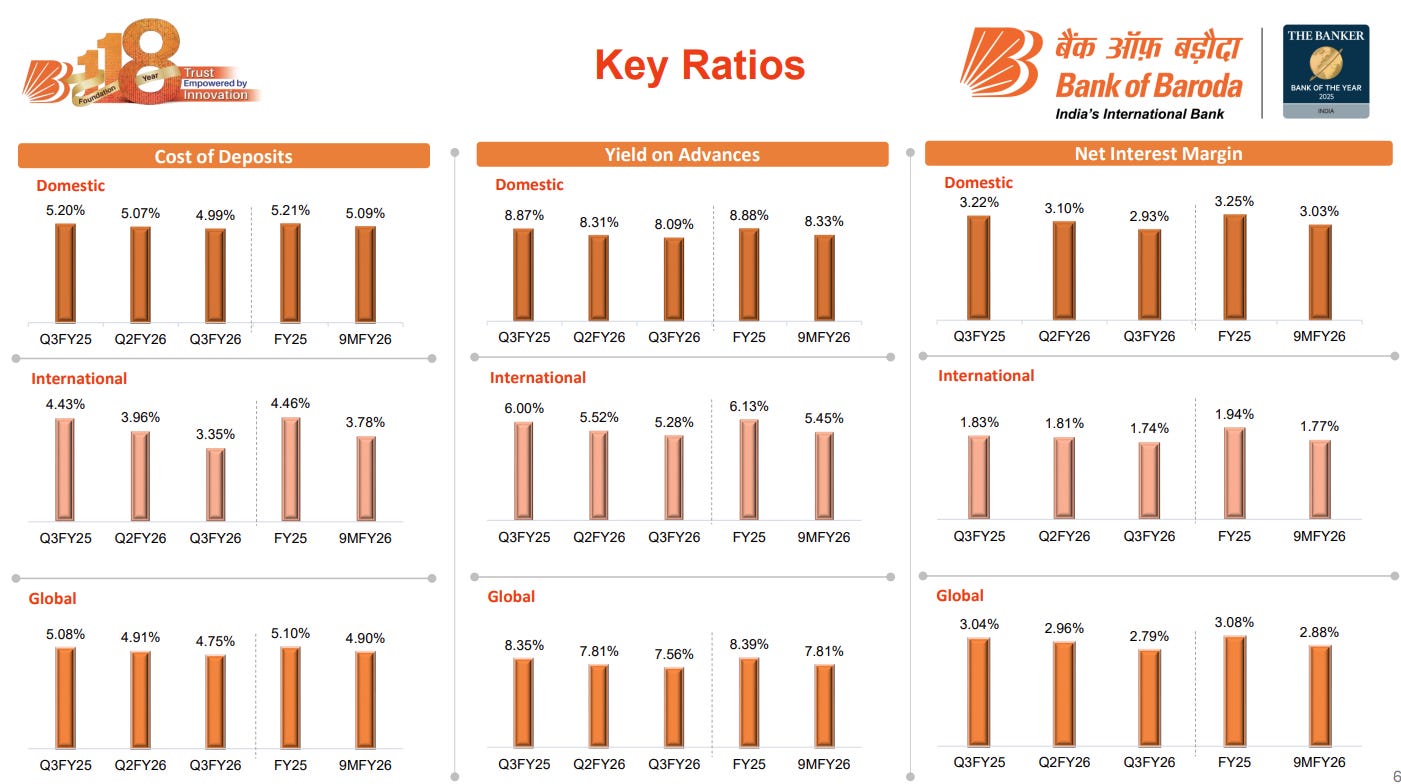

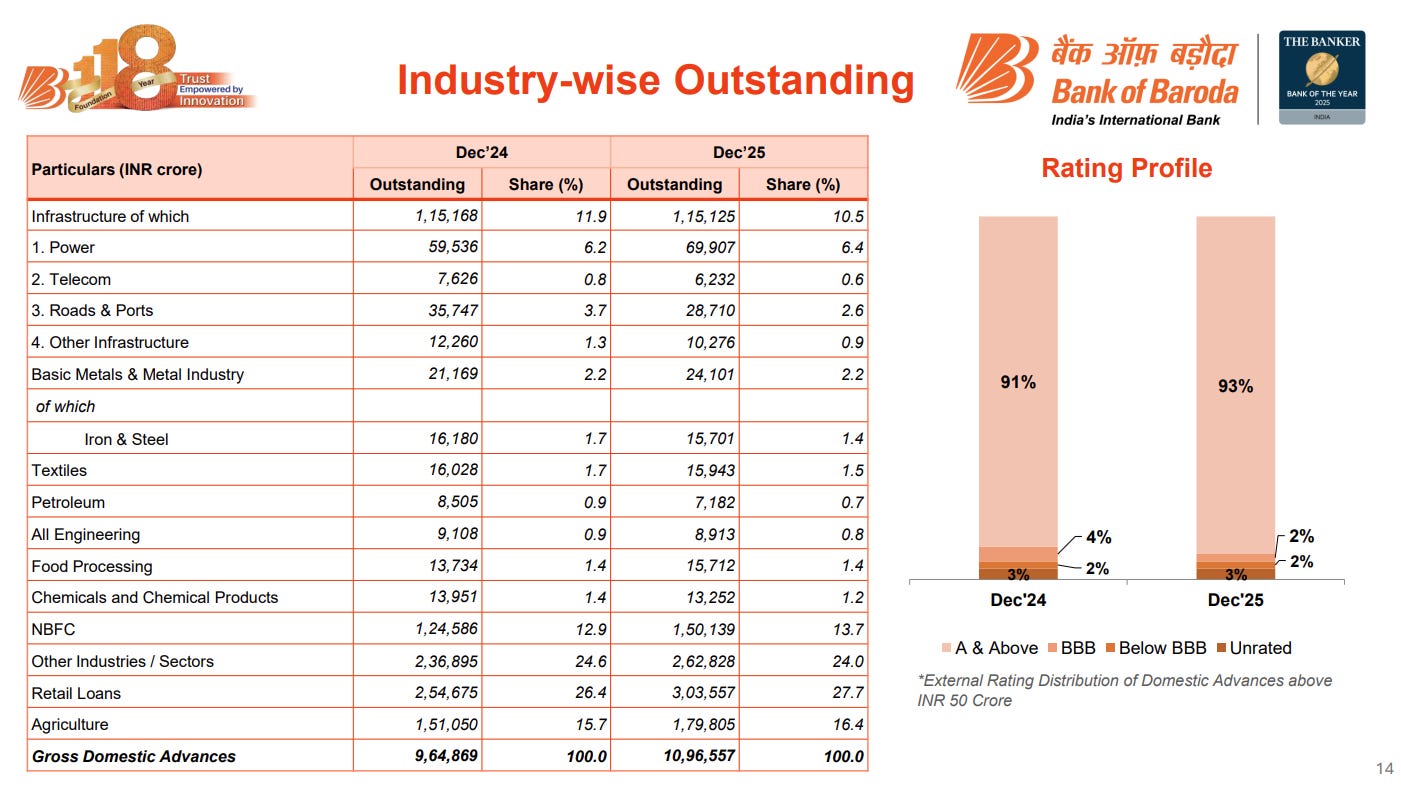

Bank of Baroda | Large Cap | Financial Services

Bank of Baroda offers a wide range of banking services including personal, corporate, international, SME, and rural banking, along with NRI services and treasury operations. It leverages advanced technology and alternate delivery channels like net banking, mobile banking, and e-lobbies to provide convenient and efficient customer service. The bank focuses on catering to diverse financial needs with innovative solutions.

BoB’s margins are normalising, not collapsing. Deposit costs have largely stabilised across domestic and international books, while yields on advances are gently easing—resulting in a controlled compression in NIMs. The key signal is discipline: margin pressure is coming from rate-cycle normalization, not competitive stress or funding panic, which keeps earnings quality intact even as peak-cycle spreads fade.

BoB’s loan growth is quietly shifting toward safer, higher-quality segments. Retail, agriculture, and NBFC exposures have expanded meaningfully, while infra and cyclical industrial segments like roads, telecom, metals, and petroleum have either shrunk or grown slower—reducing concentration risk. This shows up directly in asset quality: over 93% of the domestic book is now rated A and above, with sub-investment-grade exposure staying negligible despite balance sheet expansion.

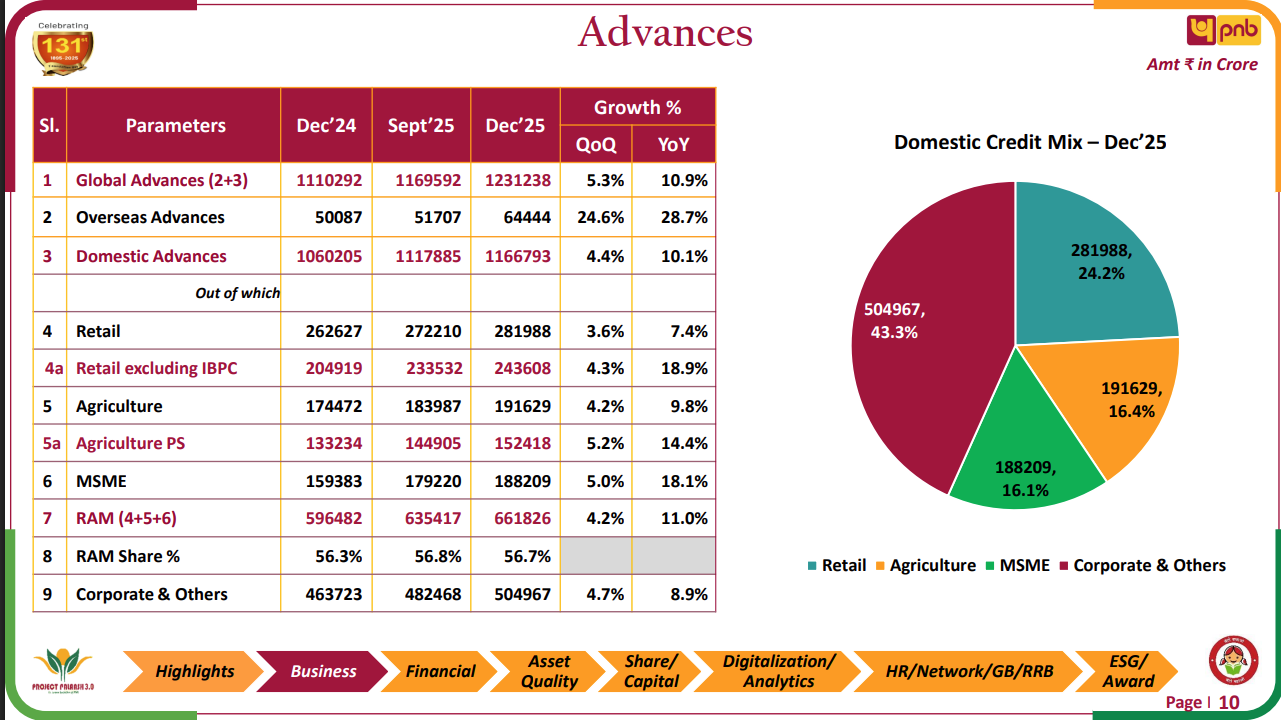

Punjab National Bank | Large Cap | Financial Services

Punjab National Bank, a premier banking institution in India, offers a wide range of financial products and services for both retail and corporate customers. Known for its strong franchise value, the bank continues to fulfill its social responsibilities while adopting technology to become a modern, techno-savvy institution.

PNB’s growth engine is now firmly retail- and MSME-led, not corporate-heavy. Domestic advances are growing at ~10% YoY, with RAM lending consistently at ~57% of the book, driven by strong momentum in MSME and retail (especially non-IBPC retail). Corporate credit is still the largest slice, but it’s growing slower than RAM—signalling a deliberate shift toward granular, higher-yield, and more diversified lending rather than balance-sheet-heavy wholesale growth.

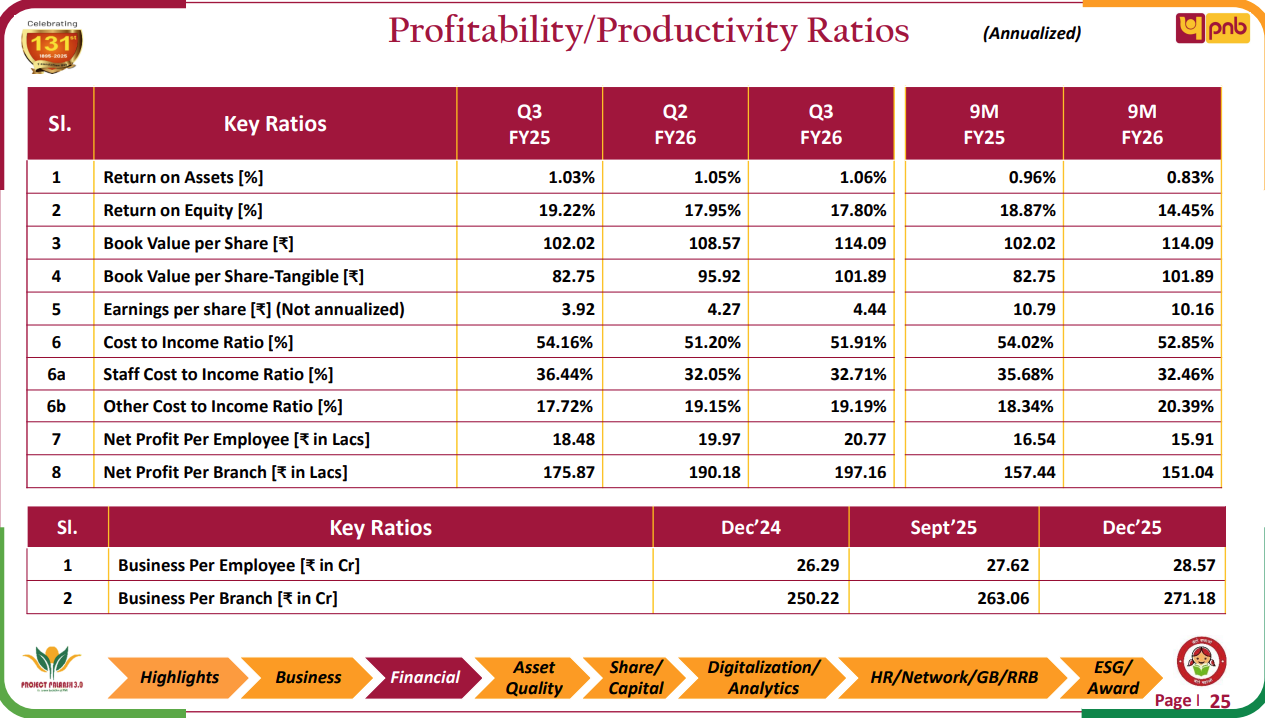

PNB’s profitability has structurally reset higher, but near-term ratios are normalising as the balance sheet scales up. ROA has crossed the 1% mark and stayed there, while ROE remains healthy in the high-teens despite some YoY moderation. The real story is operating leverage: cost-to-income is steadily improving, staff costs are coming down, and productivity per employee and per branch keeps rising, signalling a bank that is extracting more output from the same physical network rather than relying on balance-sheet risk to drive profits.

Engineering & Capital Goods

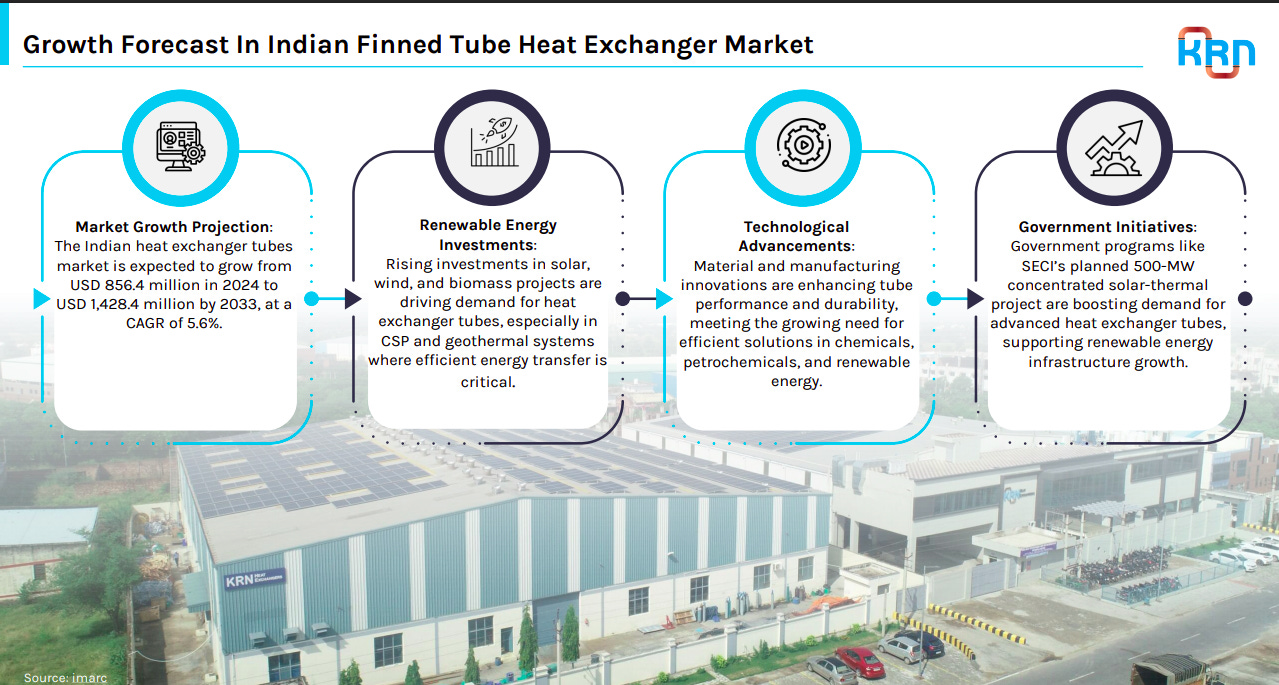

KRN Heat Exchanger and Refrigeration | Small Cap | Engineering & Capital Goods

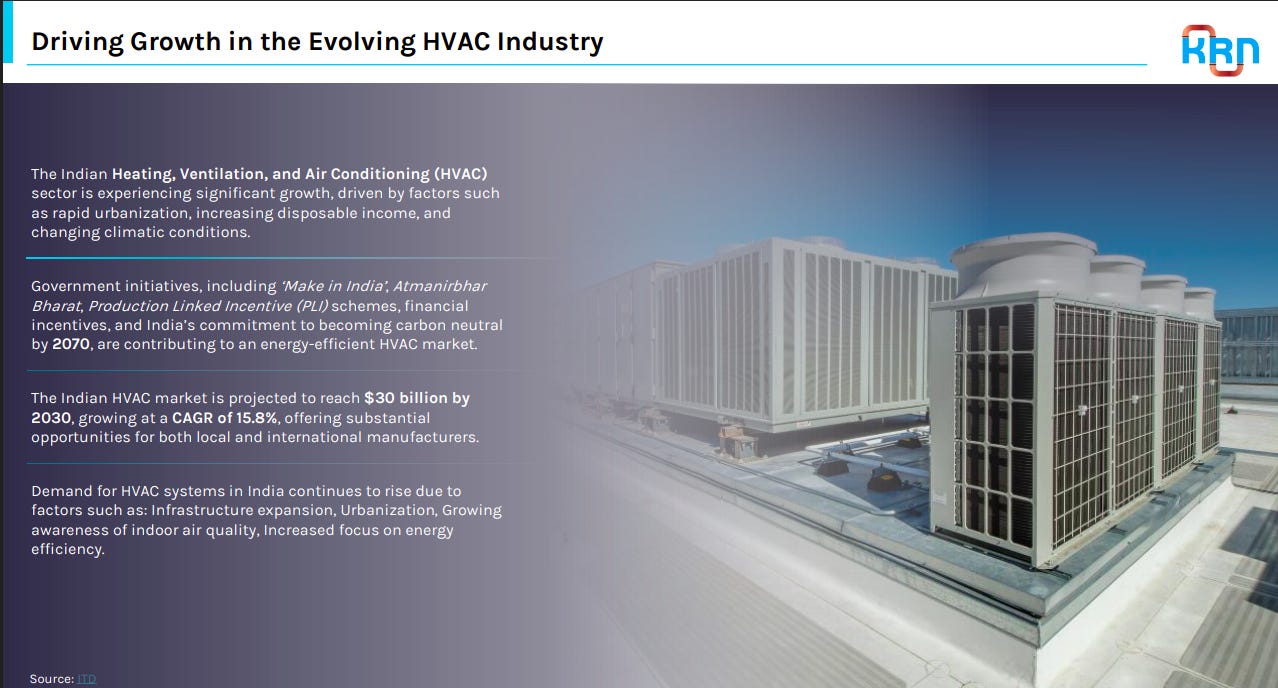

KRN Heat Exchanger and Refrigeration was incorporated on August 25, 2017 and the registered office of the company is located in Rajasthan, India. The company is engaged in the activity of manufacturing and sale of heating ventilation & Air conditioning part & accessories.

The Indian finned tube heat exchanger market is projected to grow from USD 856.4 million in 2024 to USD 1,428.4 million by 2033, at a CAGR of ~5.6%. Growth is driven by renewable energy investments, technology upgrades, and government-backed solar thermal initiatives.

India’s HVAC sector is witnessing strong growth due to urbanization, rising incomes, climate change, and energy-efficiency focus. Government programs like Make in India and PLI schemes are accelerating demand, with the market projected to reach ~$30 billion by 2030.

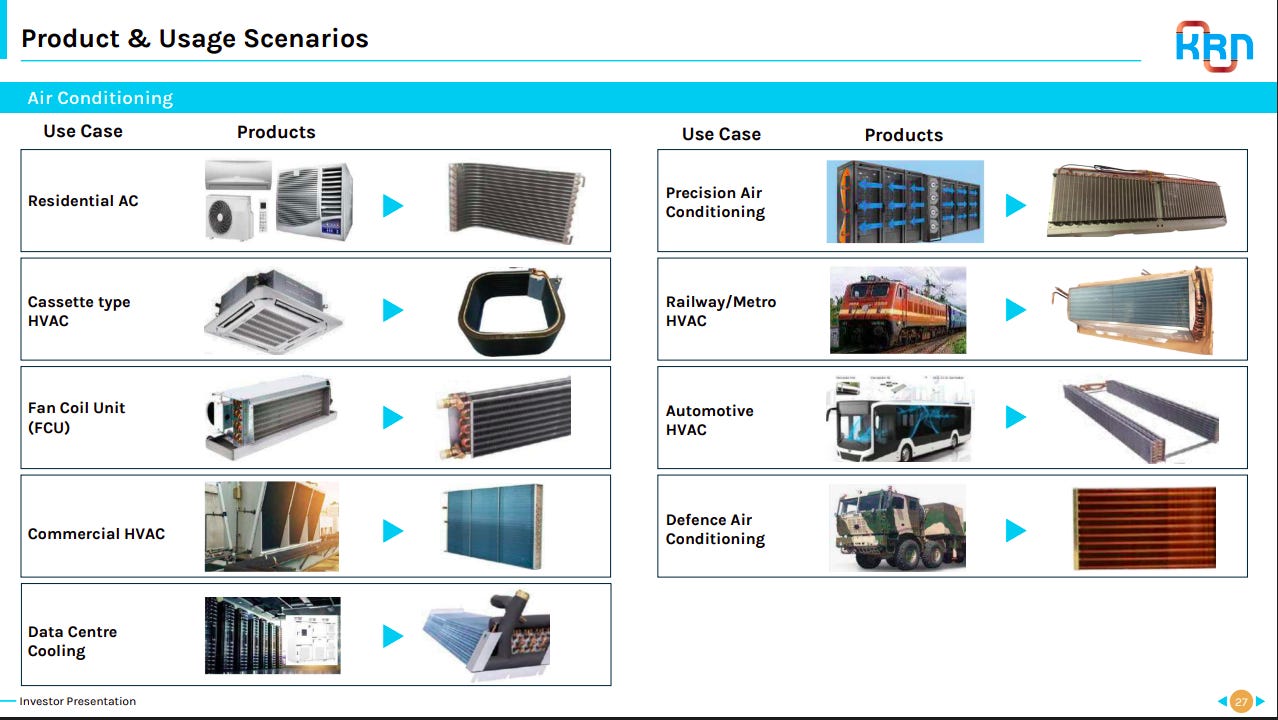

The company serves leading HVAC and industrial OEMs including Daikin, Schneider Electric, Kirloskar, Blue Star, Voltas, and Carrier. Long-standing relationships since 2018–21 highlight credibility, scale, and consistent product quality.

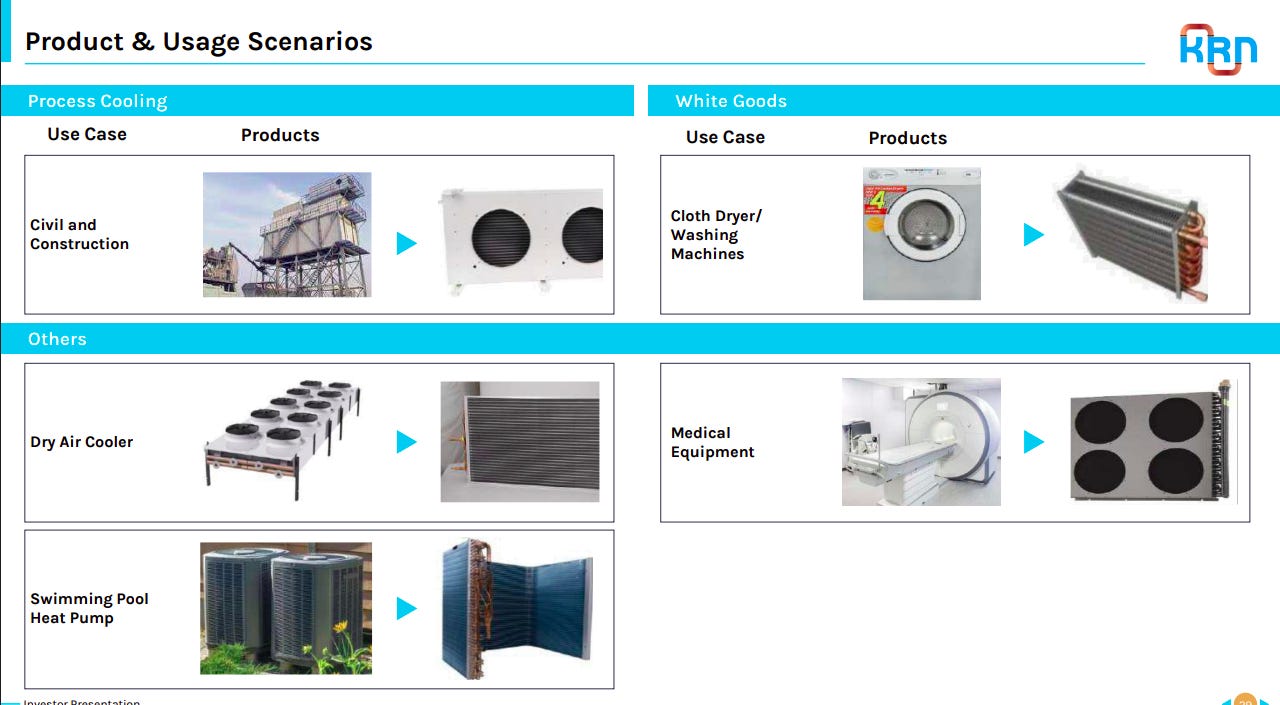

Finned tube heat exchangers are widely used across civil construction, industrial cooling, white goods, and medical equipment. Applications span dry air coolers, heat pumps, washing machines, and specialized process cooling systems.

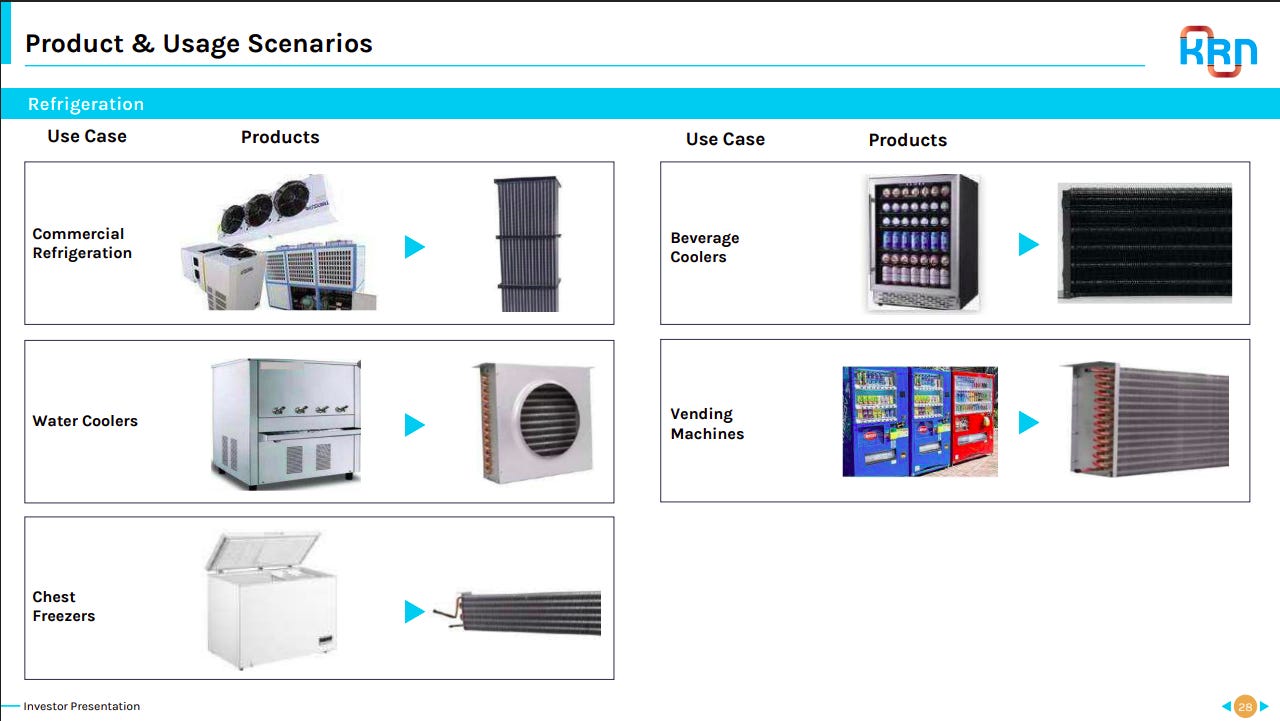

The products cater to commercial refrigeration, beverage coolers, vending machines, water coolers, and chest freezers. Rising cold-chain needs and retail refrigeration demand continue to support steady volume growth.

Heat exchangers are integral to residential, commercial, precision, railway, automotive, defense, and data-centre HVAC systems. Expansion in infrastructure, transport, and data centres is broadening application depth and demand visibility.

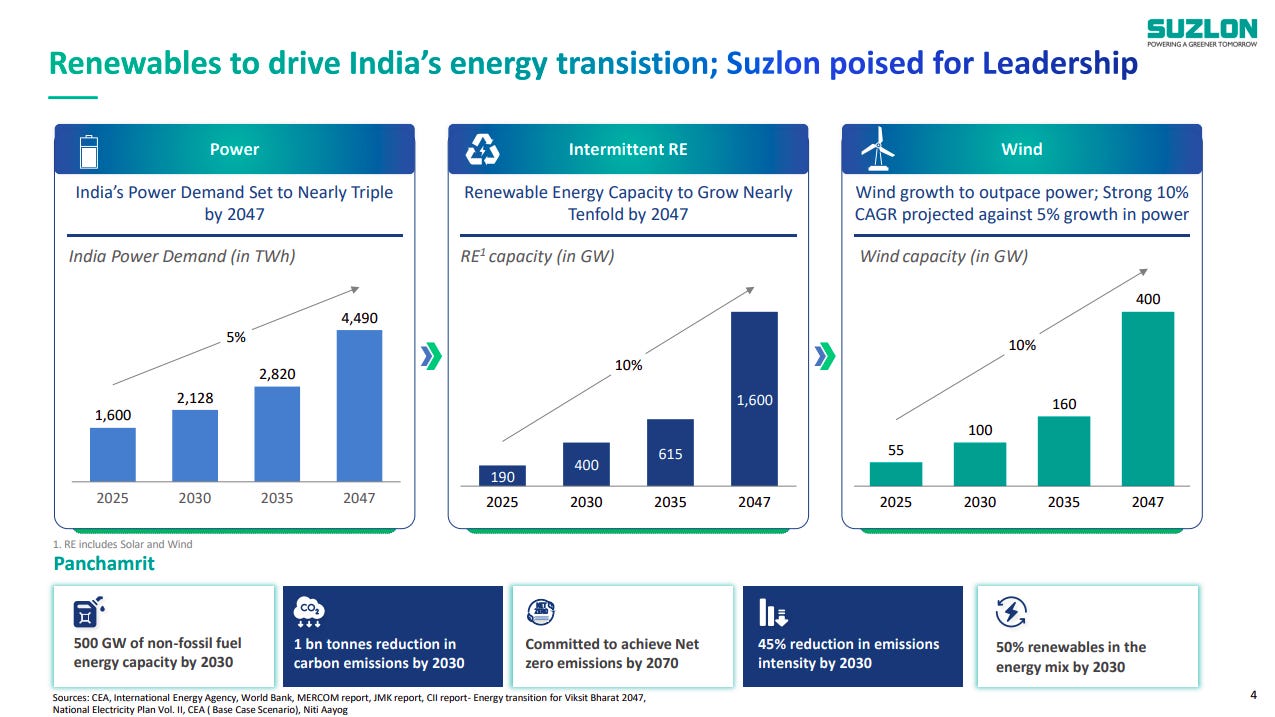

Suzlon Energy | Mid Cap | Engineering & Capital Goods

Suzlon is a company specializing in the design, development, manufacturing, and supply of Wind Turbine Generators for various capacities. They offer turnkey solutions for windfarm projects, focusing on reducing energy costs, ensuring high machine availability and reliability. With advanced R&D centers and training campuses in India, Suzlon’s turbines are designed to optimize performance and extend asset life, providing efficient solutions for renewable energy production.

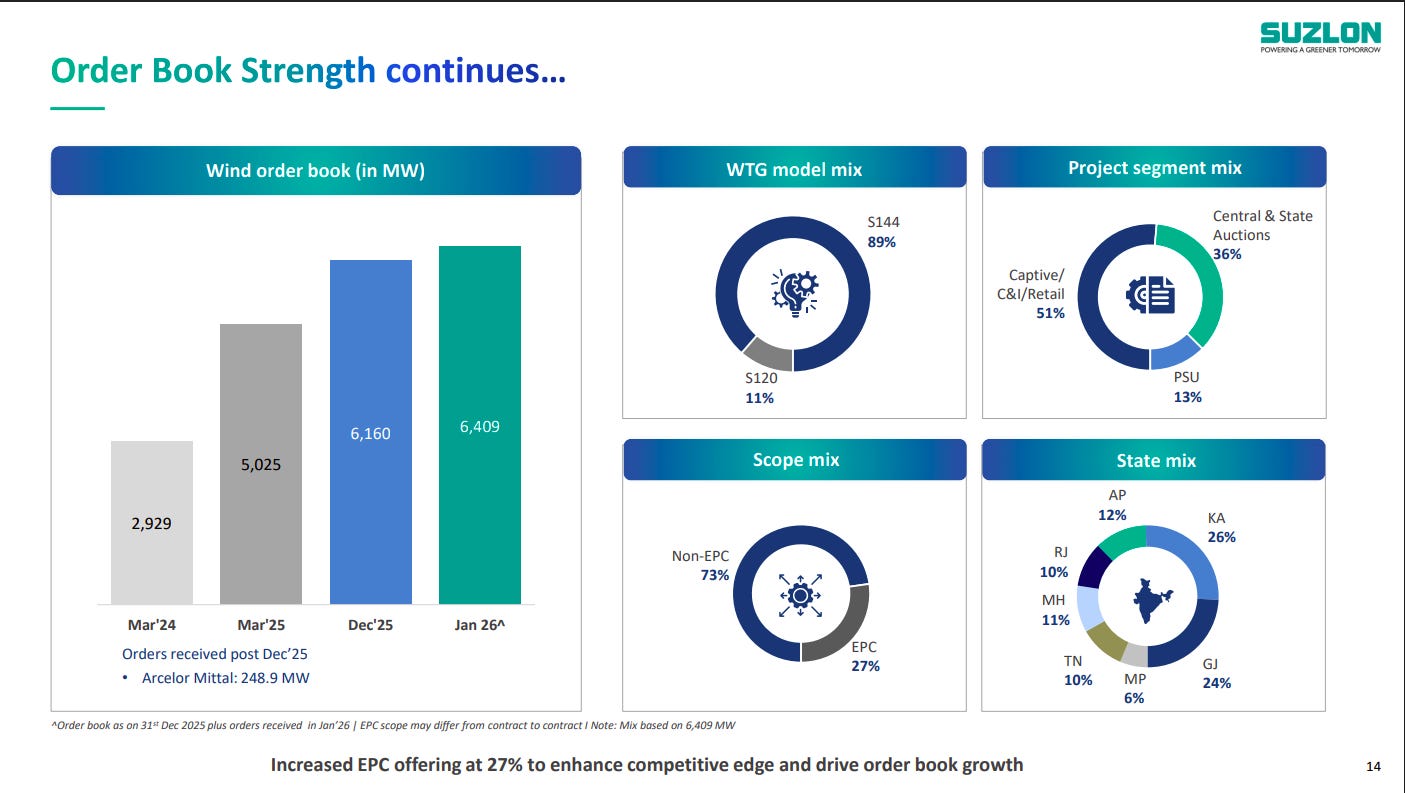

Suzlon’s wind order book has scaled up sharply to ~6.4 GW by Jan’26, reflecting strong execution momentum and sustained inflows. Orders are diversified across captive/C&I, auctions, and PSUs, with a healthy state and scope mix supporting visibility.

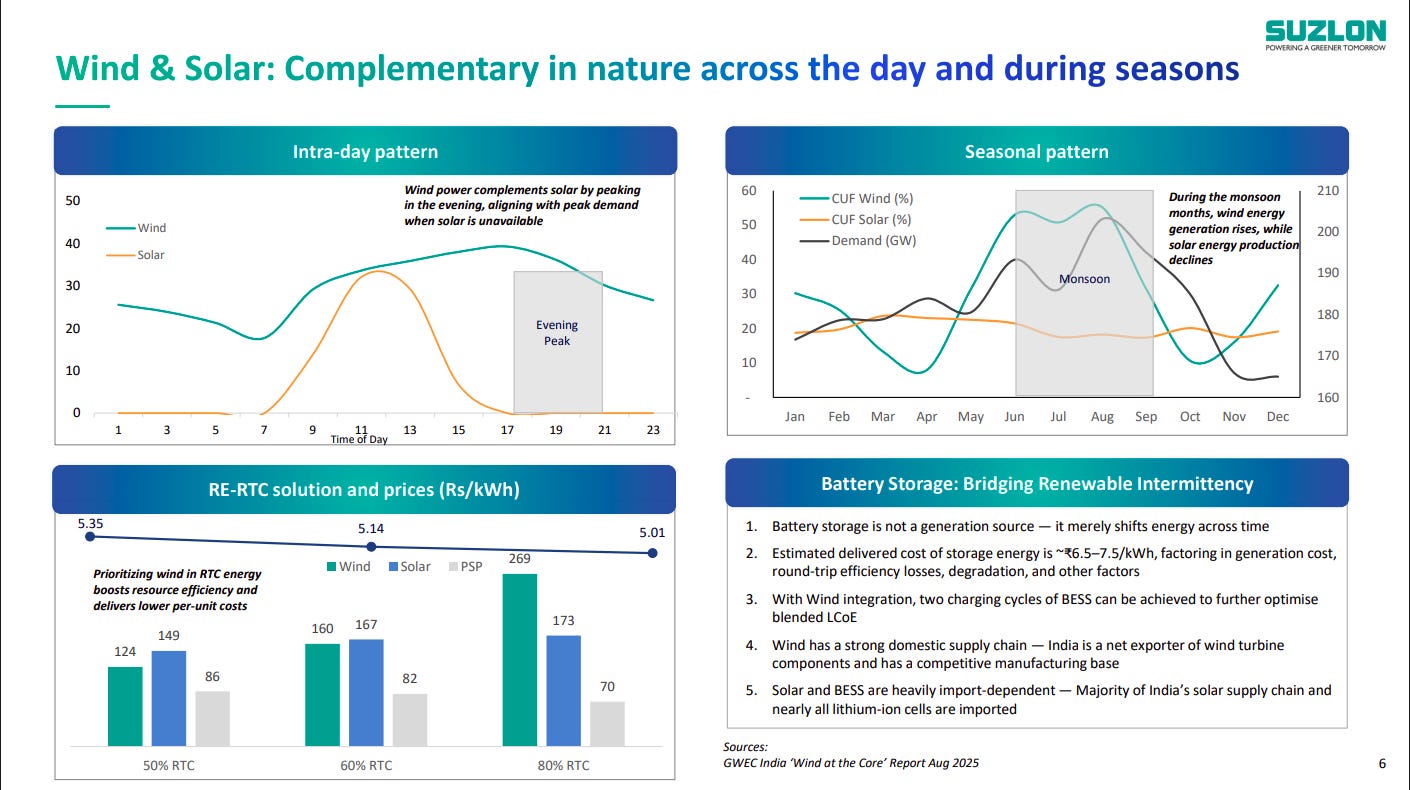

Wind and solar complement each other across intraday and seasonal cycles, improving grid stability and alignment with peak demand. Blended RE-RTC solutions, supported by wind and storage, help lower delivered power costs and manage intermittency.

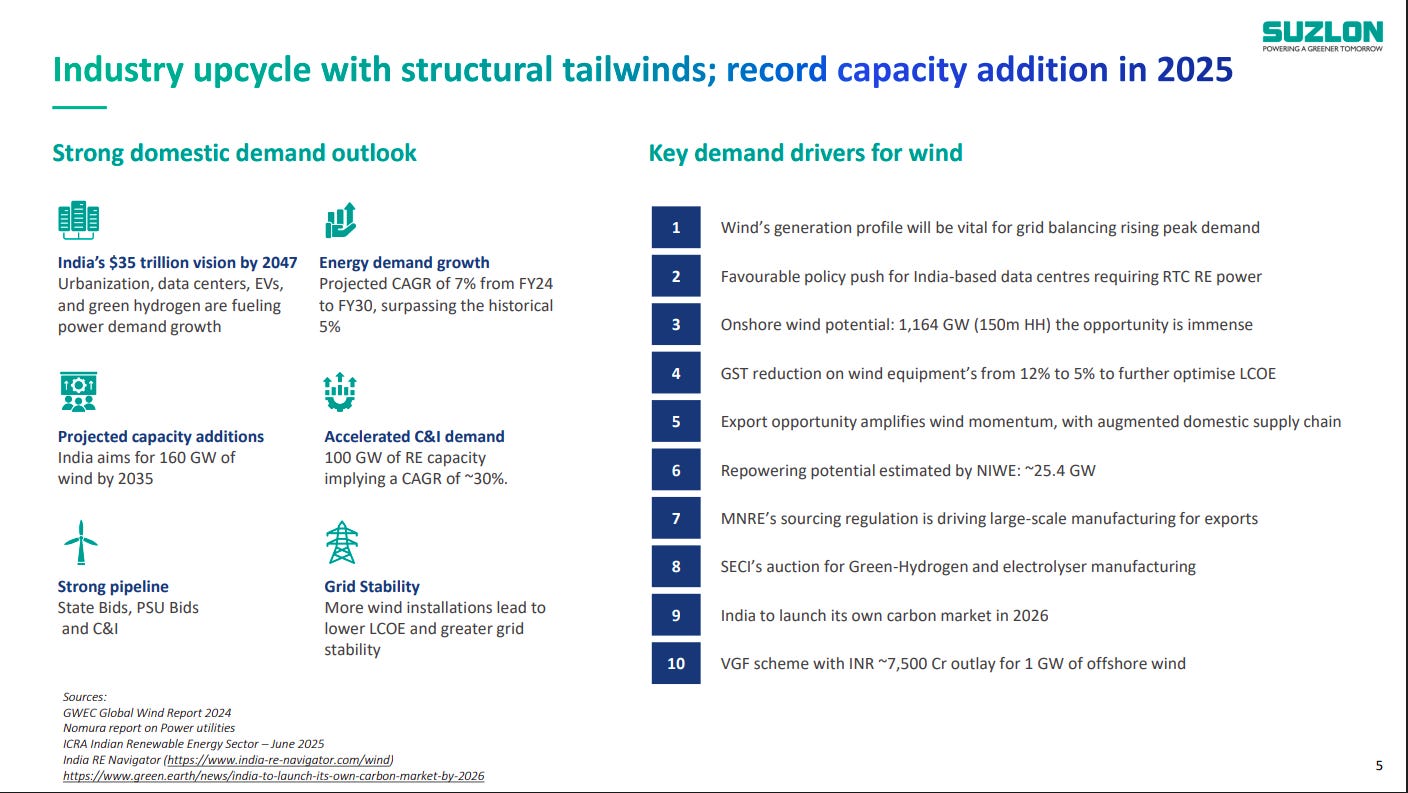

India’s wind sector is entering a structural upcycle, backed by rising power demand, policy support, C&I adoption, and grid-balancing needs. Large onshore potential, repowering opportunities, and export demand underpin long-term capacity additions.

India’s power demand is set to nearly triple by 2047, with renewable capacity expected to grow almost tenfold over the same period. Wind is projected to outpace overall power growth, positioning it as a core pillar of India’s energy transition.

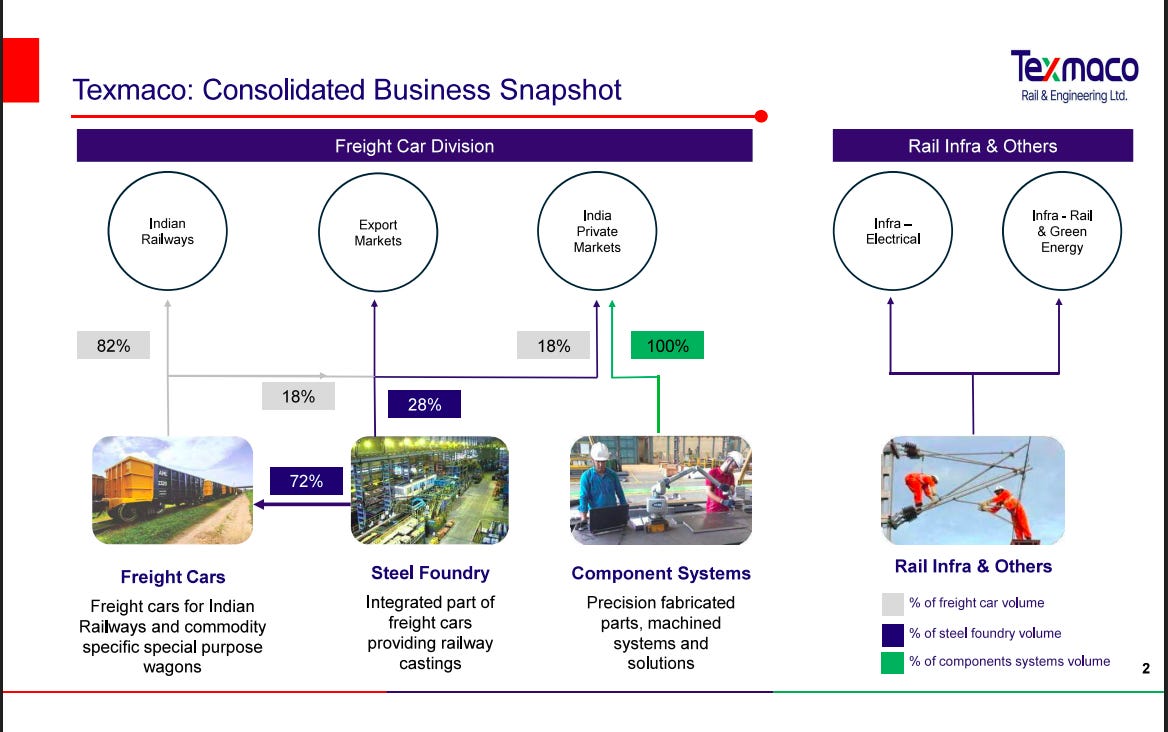

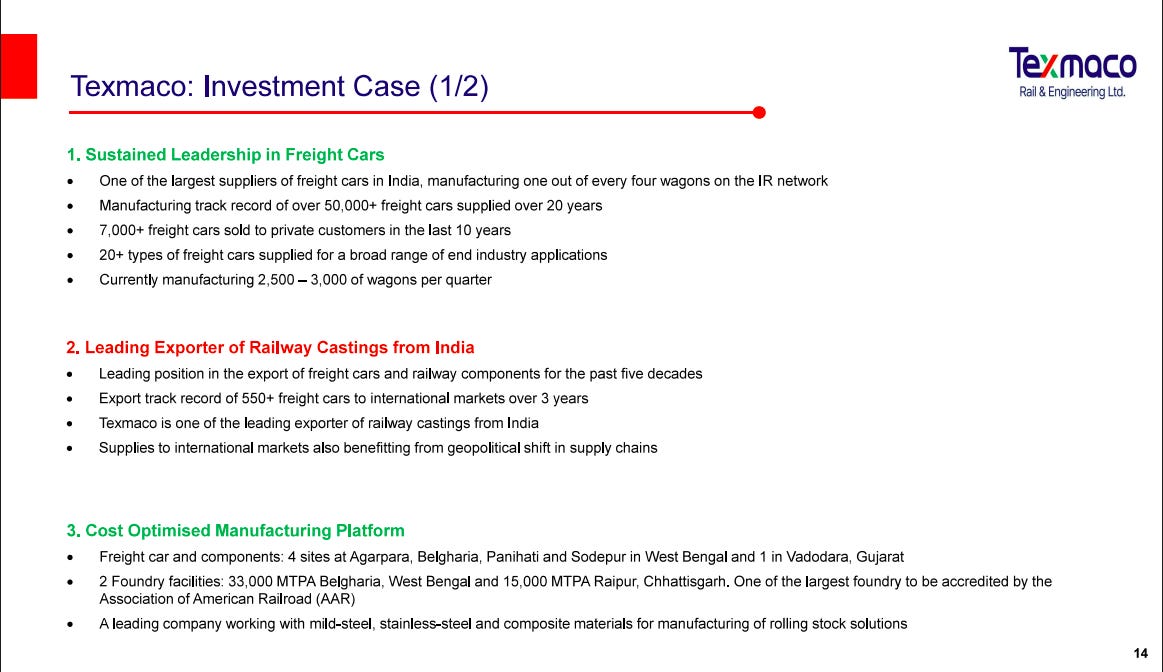

Texmaco Rail & Engineering | Small Cap | Engineering & Capital Goods

Texmaco Rail & Engineering Limited is a leading company in the engineering and infrastructure sector. It manufactures a wide range of products including railway freight cars, hydro-mechanical equipment, and steel castings. The company has established collaborations with reputed international firms to enhance its product offerings. Operating in heavy engineering and steel foundry divisions, Texmaco’s diversified product line includes pressure vessels, road repairing machinery, and agricultural equipment.

Texmaco operates across freight cars, steel foundry, component systems, and rail infra, with Indian Railways as the dominant end-market. The freight car division drives volumes, supported by integrated foundry and component capabilities, while rail infra and electricals add diversification.

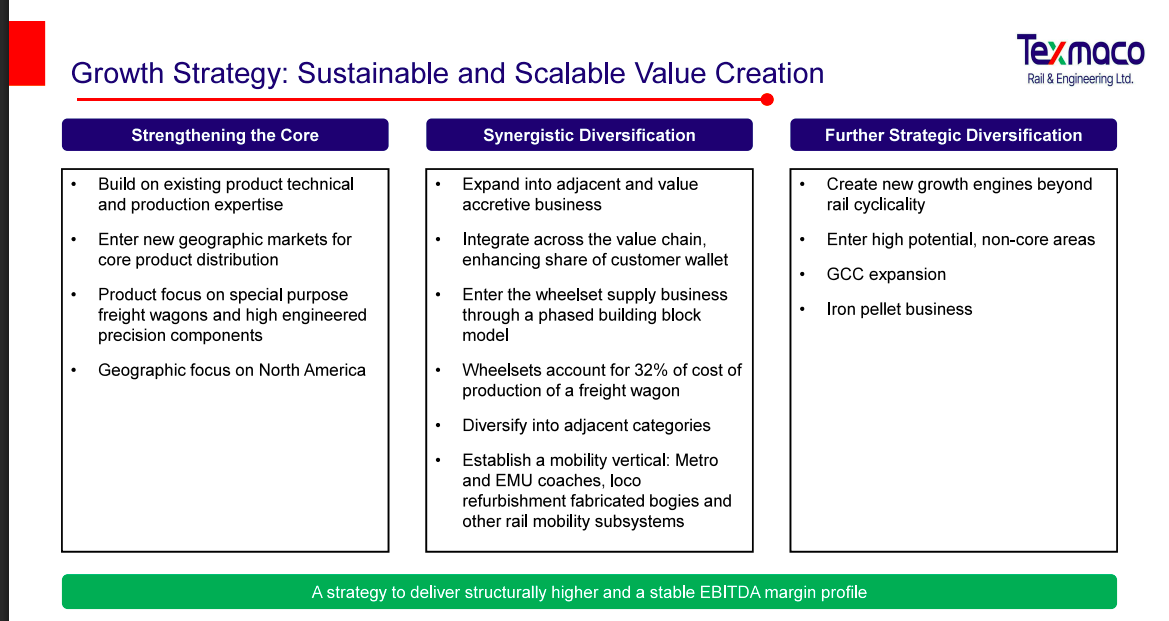

The strategy focuses on strengthening core freight wagon capabilities, expanding into value-accretive adjacencies like wheelsets and mobility solutions, and pursuing non-rail diversification. The objective is to reduce cyclicality and deliver structurally higher, stable EBITDA margins.

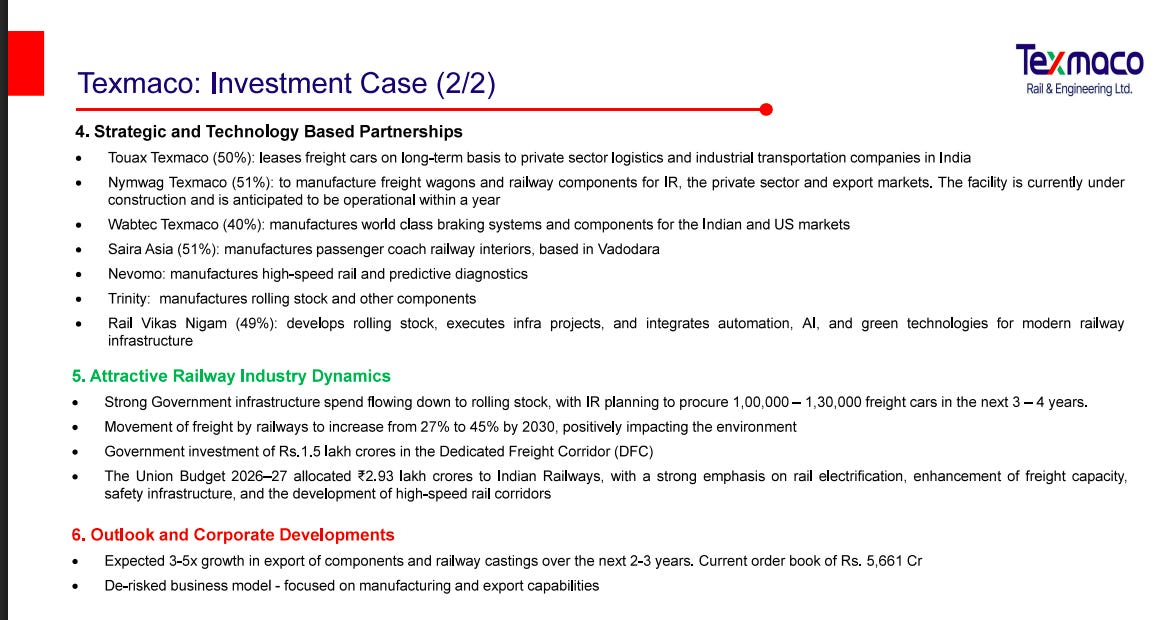

Strategic partnerships across leasing, braking systems, diagnostics, and rolling stock enhance technology depth and market access. Strong rail capex, freight corridor investments, and export growth underpin a positive medium-term outlook with a ₹5,661 crore order book.

Texmaco is a leading freight car manufacturer in India with a long execution track record and strong export presence in castings and components. A cost-optimized manufacturing footprint and diversified product portfolio support scale, competitiveness, and margin resilience.

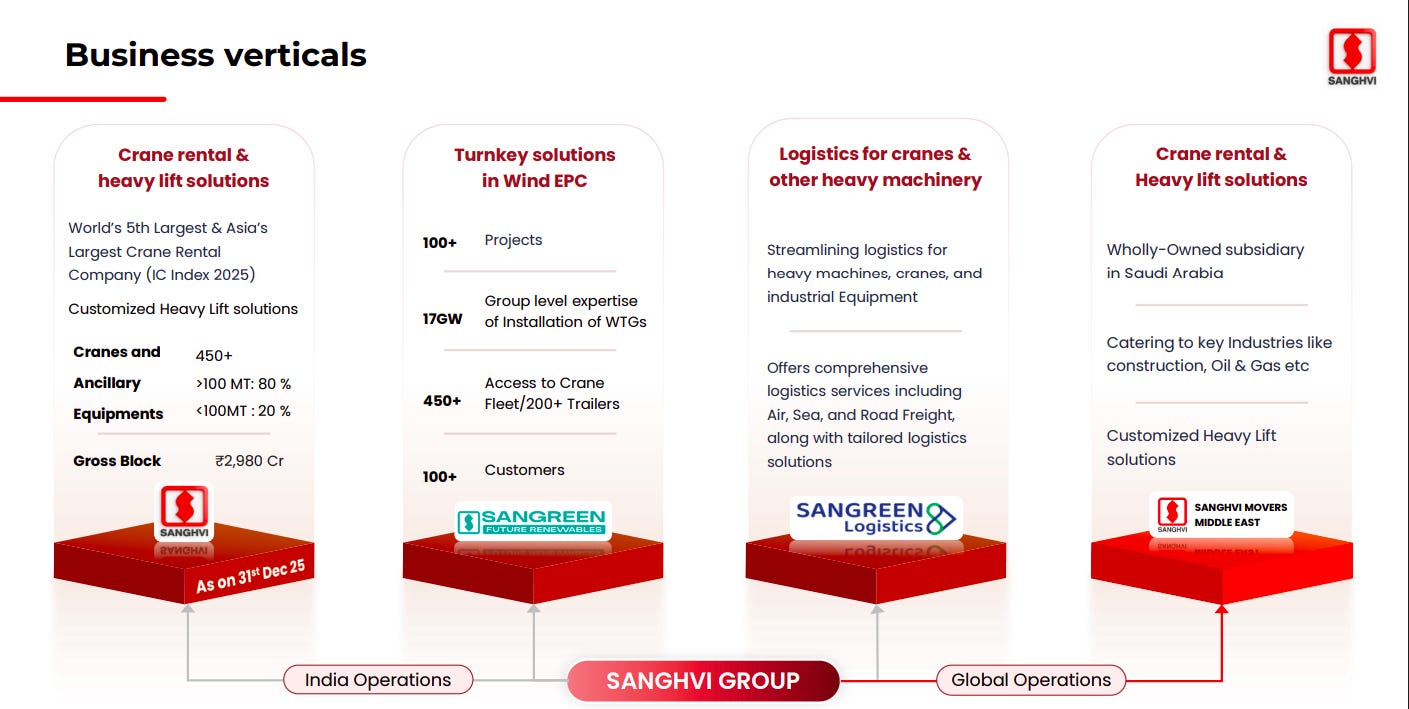

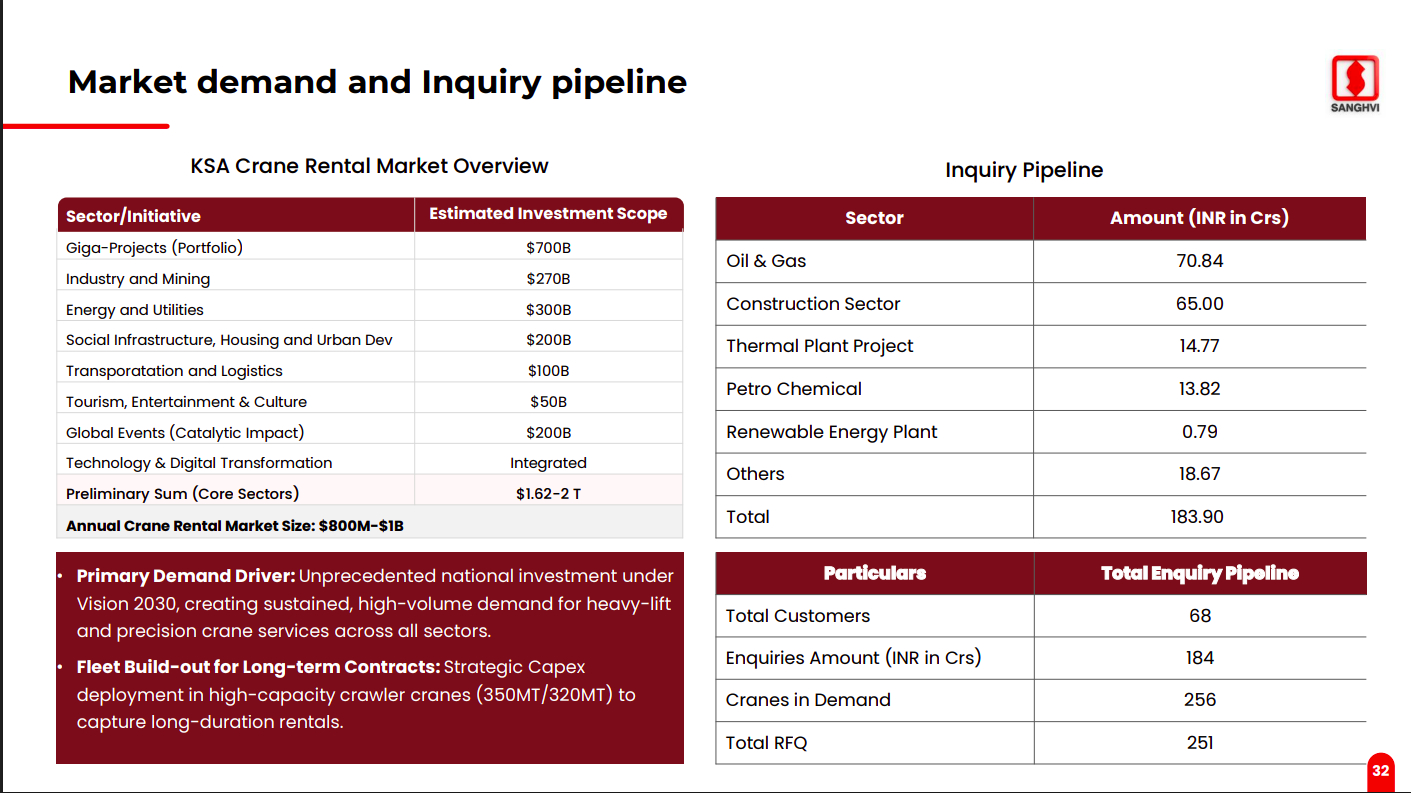

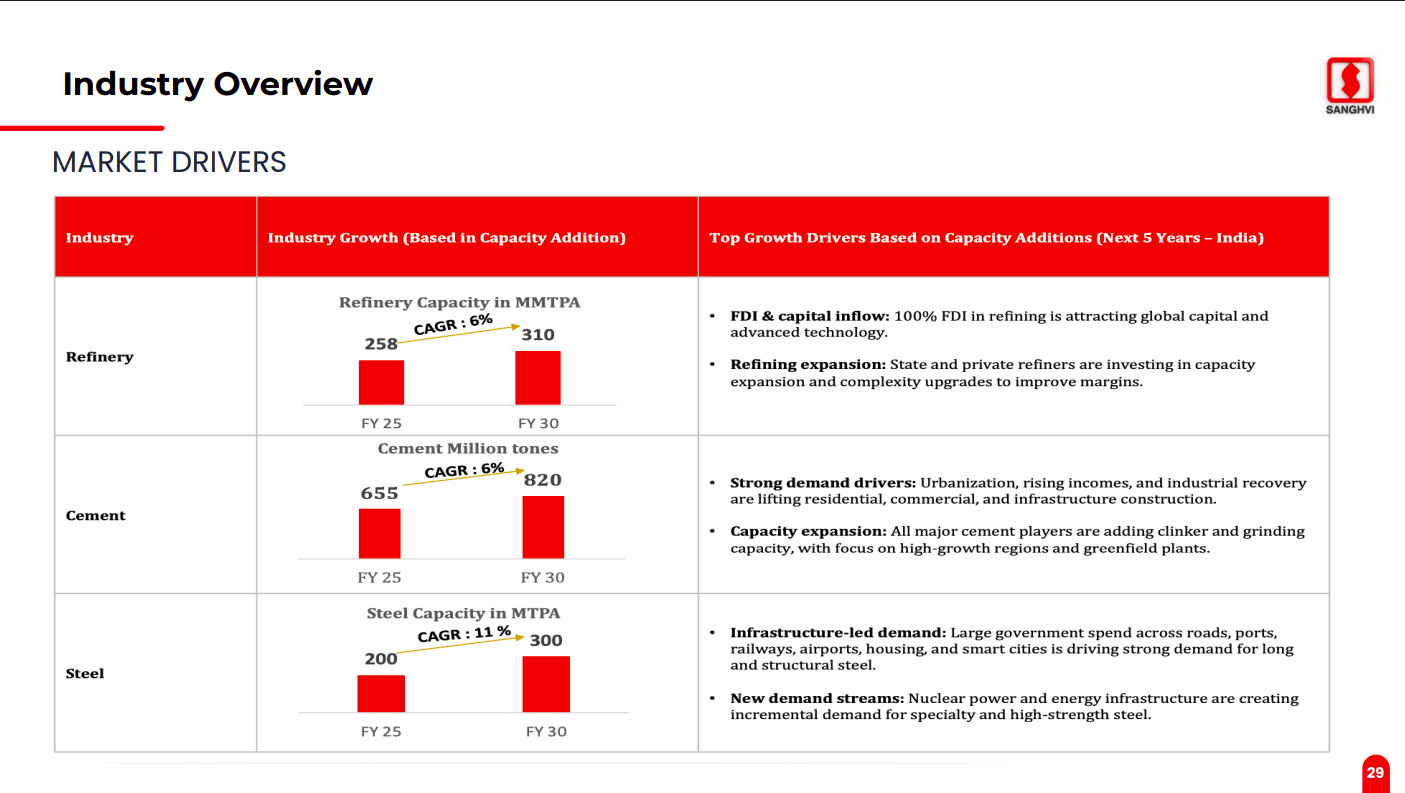

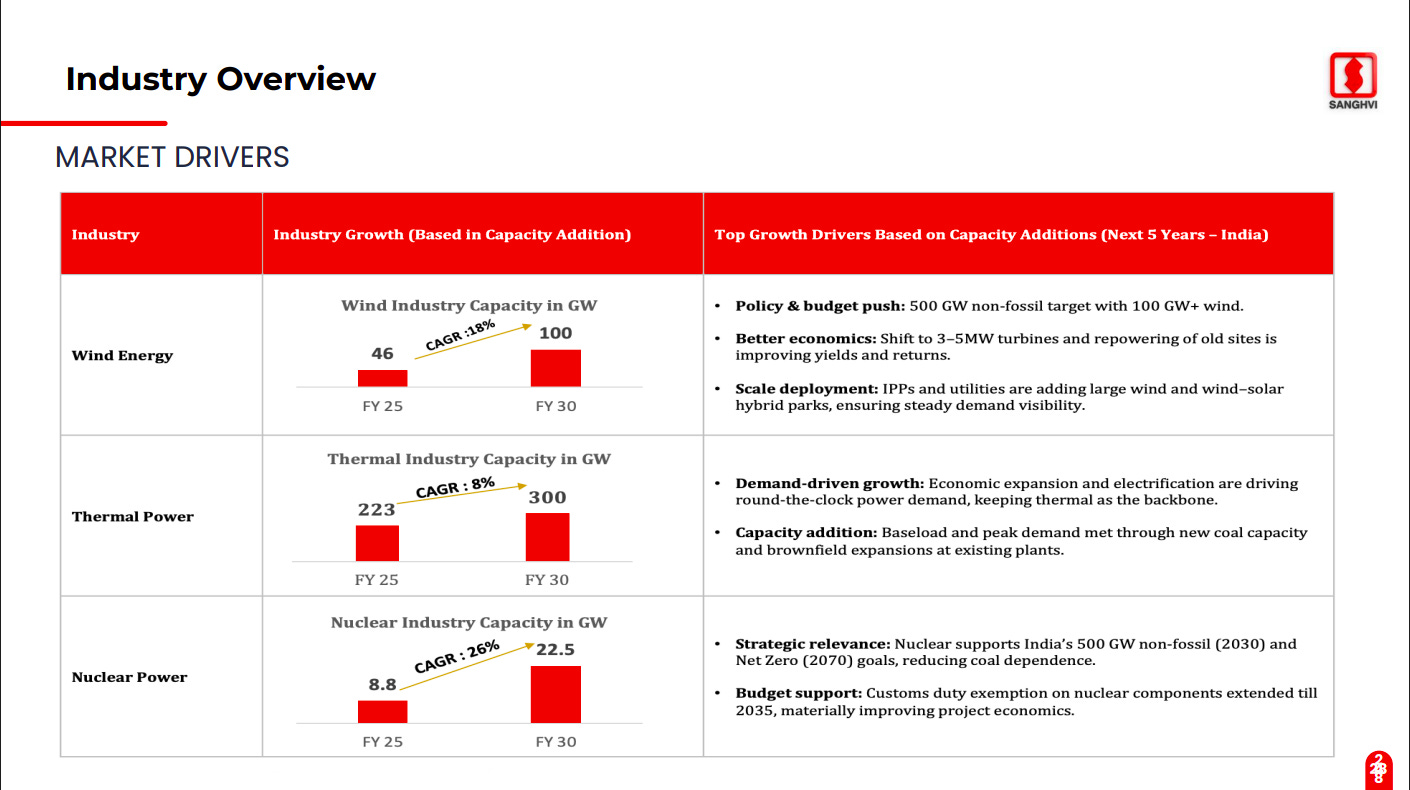

Sanghvi Movers | Small Cap | Engineering & Capital Goods

Sanghvi Movers Limited (SML) is the largest crane rental company in India. SML is a BS OHSAS 18001:2007 certified company. It is committed to being a top globally-ranked company in its core business with exceptional business ethics and morals.

Sanghvi Group operates across crane rental, heavy-lift solutions, wind EPC, and specialized logistics, with a strong presence in India and the Middle East. The group combines scale (450+ cranes), execution capability, and turnkey expertise to serve infrastructure, energy, and industrial projects.

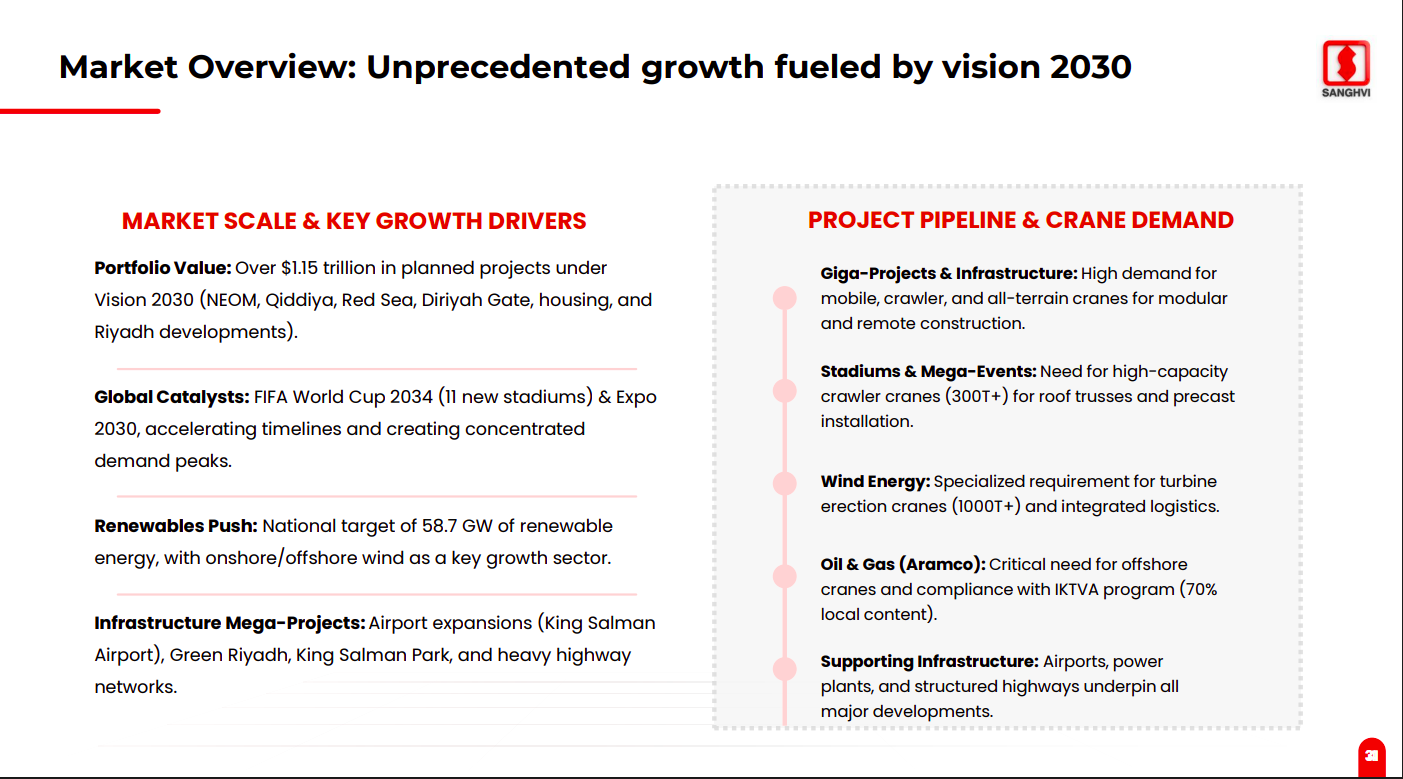

Saudi Arabia’s Vision 2030 is driving a $1.6–2 trillion investment pipeline across giga-projects, energy, infrastructure, and logistics. This is translating into a strong crane rental inquiry pipeline of ₹184 crore, led by Oil & Gas and construction sectors.

Over $1.15 trillion of planned projects, global events like Expo 2030 and FIFA World Cup 2034, and a strong renewables push are creating sustained demand for high-capacity cranes. Giga-projects, wind energy, and oil & gas are key demand anchors.

India’s refinery, cement, and steel capacities are set to expand at 6–11% CAGR over the next five years. Infrastructure spending, urbanization, and energy security are driving large, long-cycle demand for heavy lifting and project execution services.

Power sector capacity additions remain robust, led by wind (18% CAGR) and nuclear (26% CAGR), alongside steady thermal expansion. Policy support, scale deployment, and energy transition goals are creating long-term visibility for heavy equipment and crane demand.

Chemicals

Ester Industries | Micro Cap | Chemicals

Ester Industries Ltd specializes in the production and marketing of a wide range of polyester films and engineering plastics. Their product line includes various types of polyester films like Packaging Films, Metallized Films, and specialty products like Estoplast - EP Thermoplastic Polyester, XU Polyamide, and Polycarbonate. The company is known for its high-quality products used in industries including packaging and industrial applications.

ELITe targets multiple end-use industries—electronics, textiles, automotive, cosmetics, and packaging—using Loop’s patented recycled polyester technology. The JV addresses a ~$28 bn global specialty chemicals market, combining sustainability, product innovation, and supply-chain decarbonisation, anchored by a multi-year offtake agreement with Nike.

Ester’s polyester film portfolio spans over 300+ BOPET SKUs, including metallized, holographic, coated, and high-barrier films, with up to 100% recycled content. Value-added products continue to gain share, driven by strong demand from food, beverage, personal care, industrial packaging, and security applications.

The industry is benefiting from sustainability mandates, export demand, and rapid growth in flexible packaging and e-commerce. India’s BOPET thin film market shows healthy ~80% capacity utilisation, supported by technological advancements and rising domestic as well as export demand.

Retail

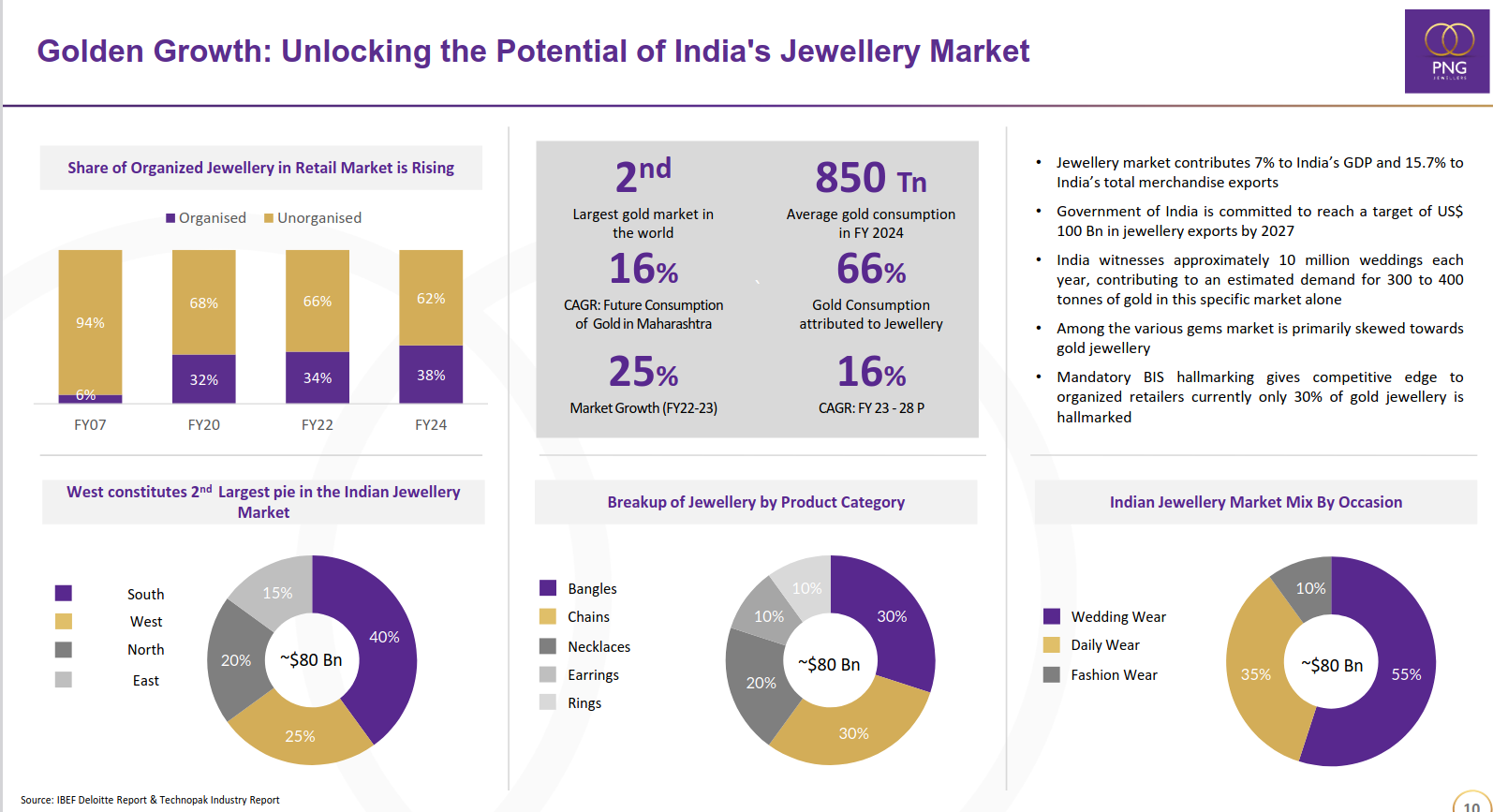

PN Gadgil Jewellers | Small Cap | Retail

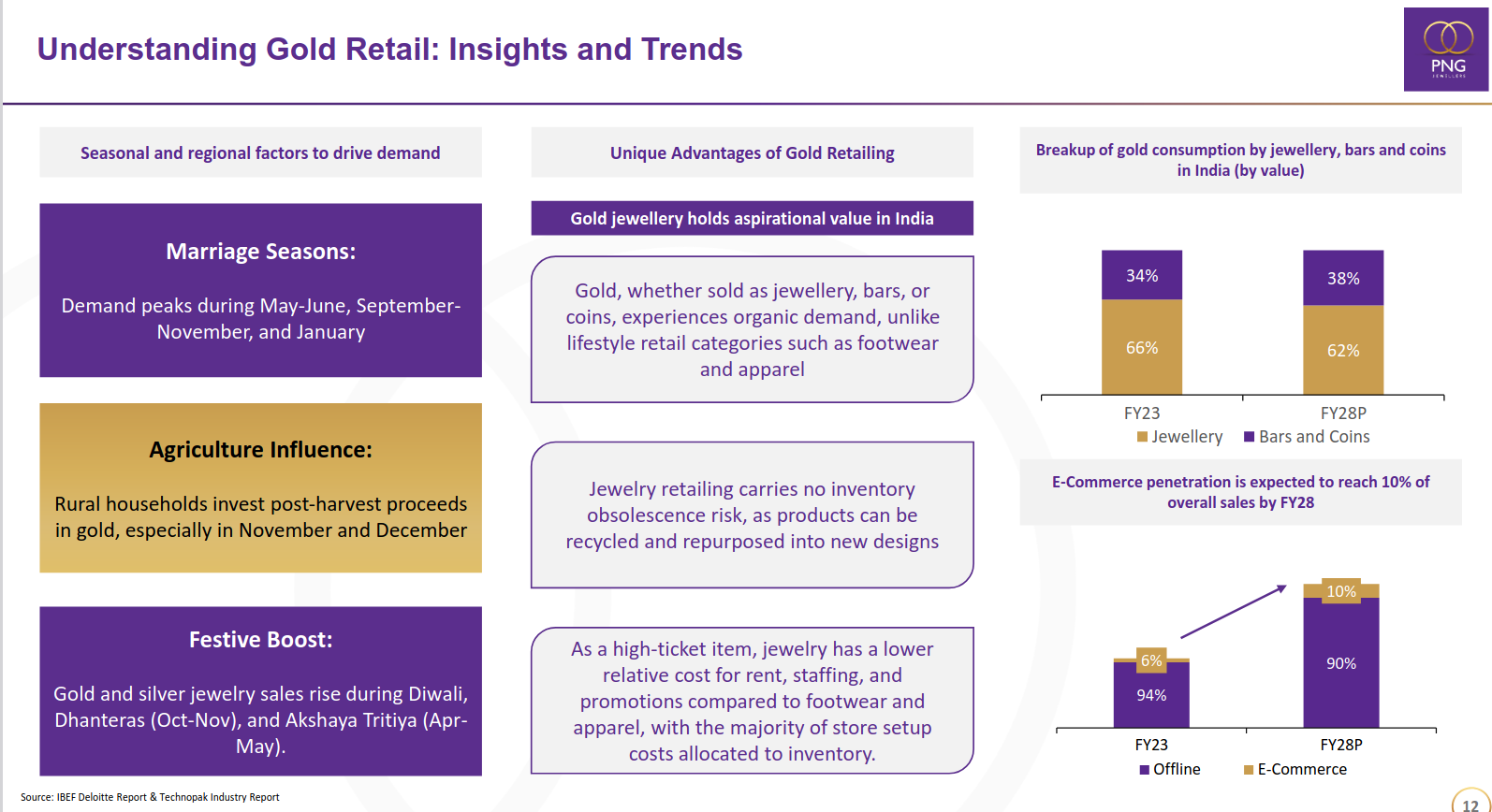

P.N. Gadgil Jewellers (PNG) specializes in designing, manufacturing, and retailing gold, silver, diamond, and platinum jewelry. With a strong legacy of over six generations, the company focuses on quality, traditional, and contemporary designs, offering customized options and maintaining high purity standards.

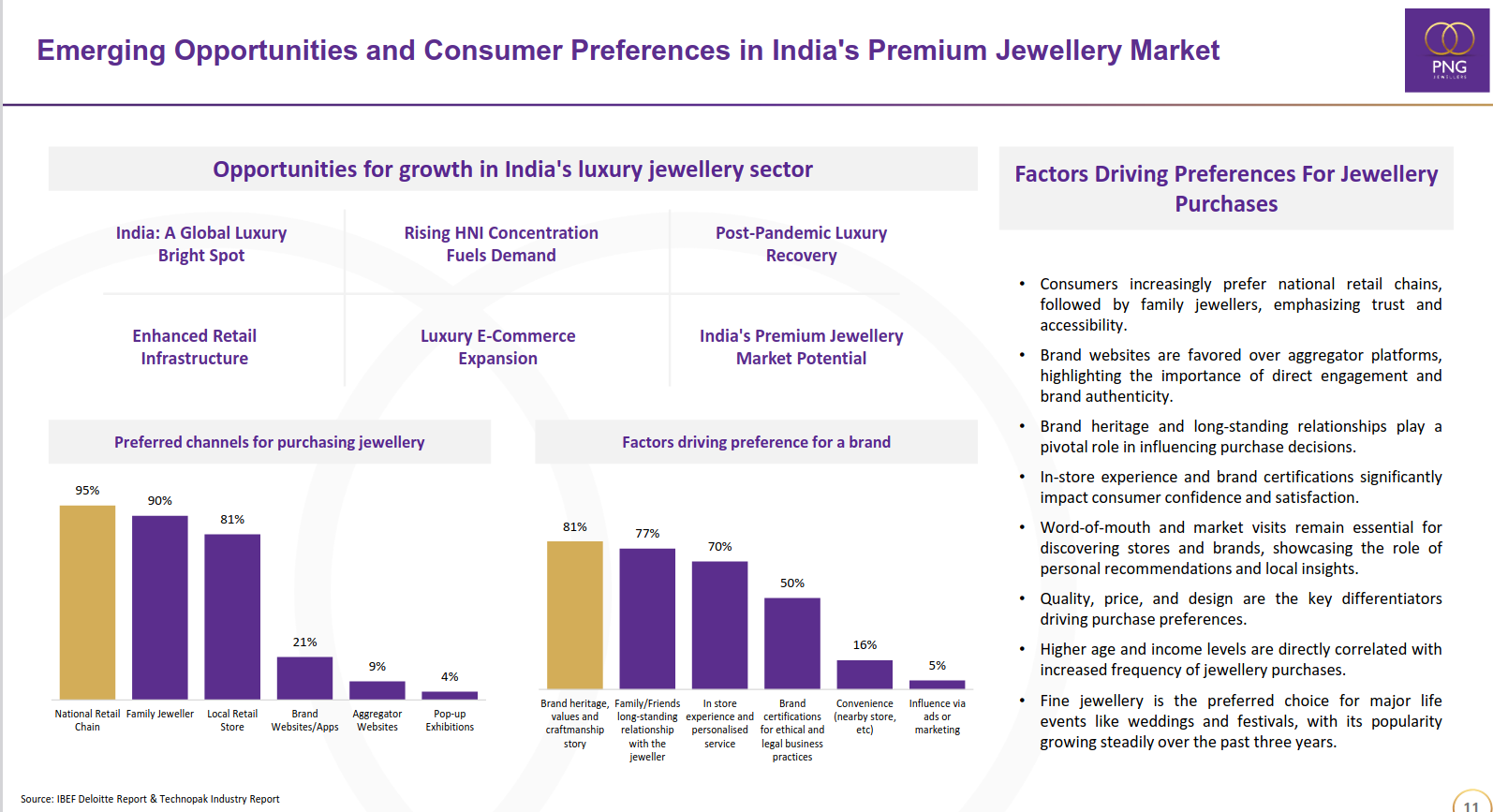

India’s jewellery market is scaling steadily, driven by rising formalisation, strong wedding-led demand, and increasing organised retail share. With ~$80 bn market size, gold jewellery dominates consumption, while policy support like BIS hallmarking favours organised players.

Premium and luxury jewellery demand is being fuelled by rising HNI concentration, post-pandemic recovery, and expanding luxury e-commerce. Consumers increasingly prefer national retail chains and trusted brands, with heritage, in-store experience, and certification driving purchase decisions.

Gold demand in India remains structurally resilient, supported by marriage seasons, festivals, and rural income cycles. Jewellery enjoys aspirational value, low obsolescence risk, and improving digital penetration, with e-commerce expected to reach ~10% of sales by FY28.

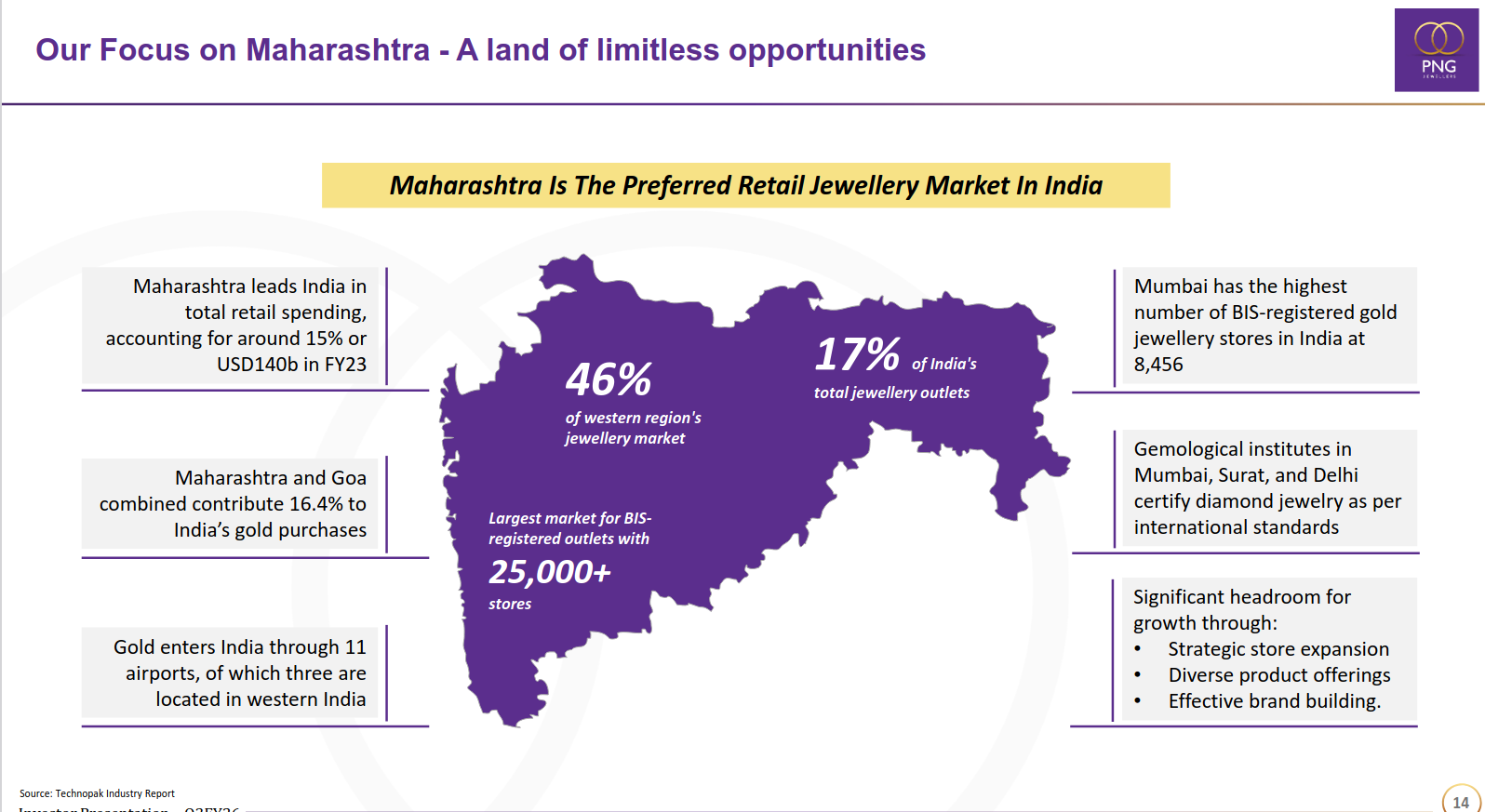

Maharashtra is India’s most attractive jewellery retail market, accounting for ~15% of total retail spending and 46% of the western region’s jewellery demand. High urbanisation, BIS-registered store density, and strong brand-led expansion provide significant headroom for growth.

Metals

Tata Steel | Large Cap | Metals

Tata Steel is a globally diversified steel producer with integrated operations from mining to marketing. Its raw material operations in India and Canada ensure self-sufficiency, while downstream business units in India include Ferro-Alloys, Tubes, Wires, Bearings, and more.

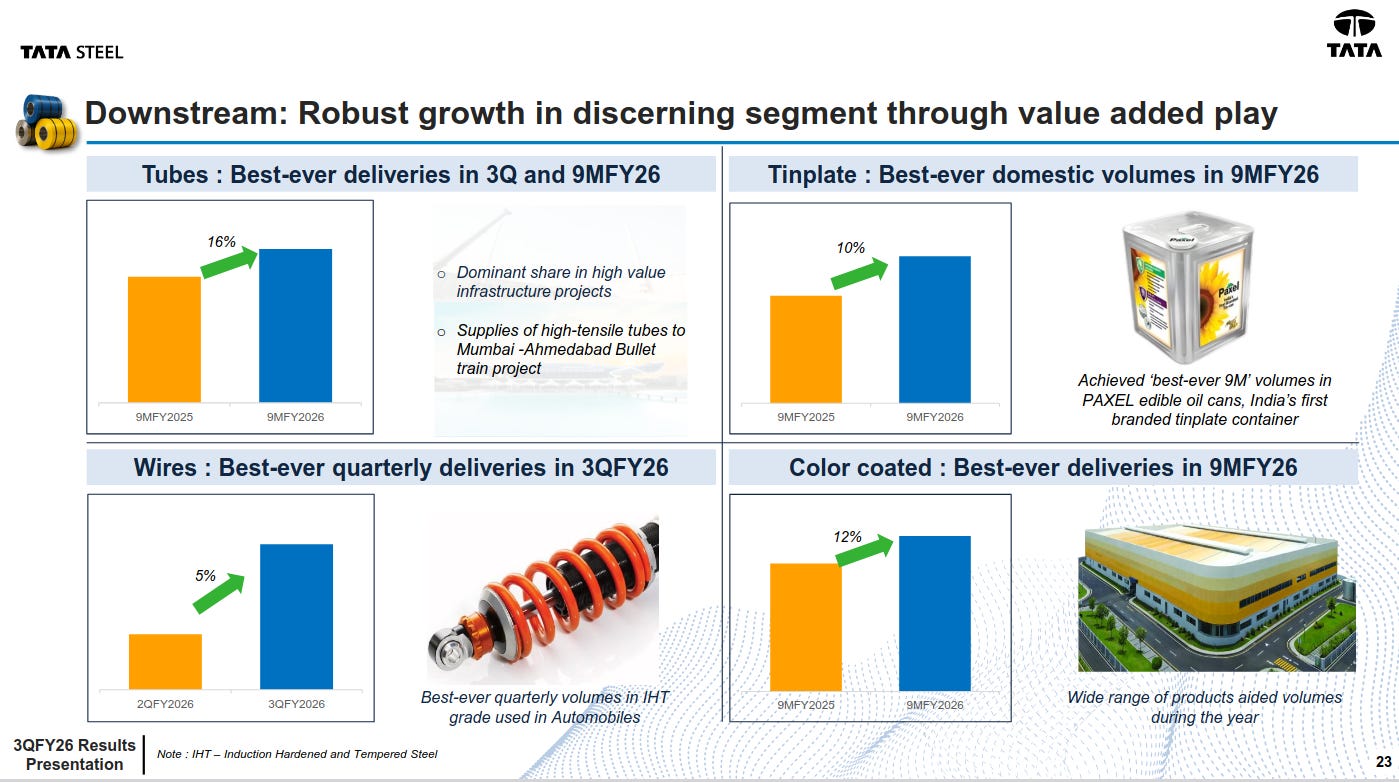

Downstream businesses delivered best-ever volumes across tubes, tinplate, wires, and color-coated products in 9MFY26/3QFY26. Growth was driven by high-value infrastructure, automotive applications, and a wider product mix.

Industrial Products saw strong momentum in engineering, appliances, and solar, supported by product innovation and customer-centric solutions. Expansion into oil & gas and shipbuilding, along with overseas orders, strengthened the order pipeline.

Auto downstream delivered record performance with strong YoY and QoQ growth, aided by new grade approvals and rapid ramp-up of CAL and CGL facilities. Advanced steels and coatings deepened OEM engagement and raised downstream contribution.

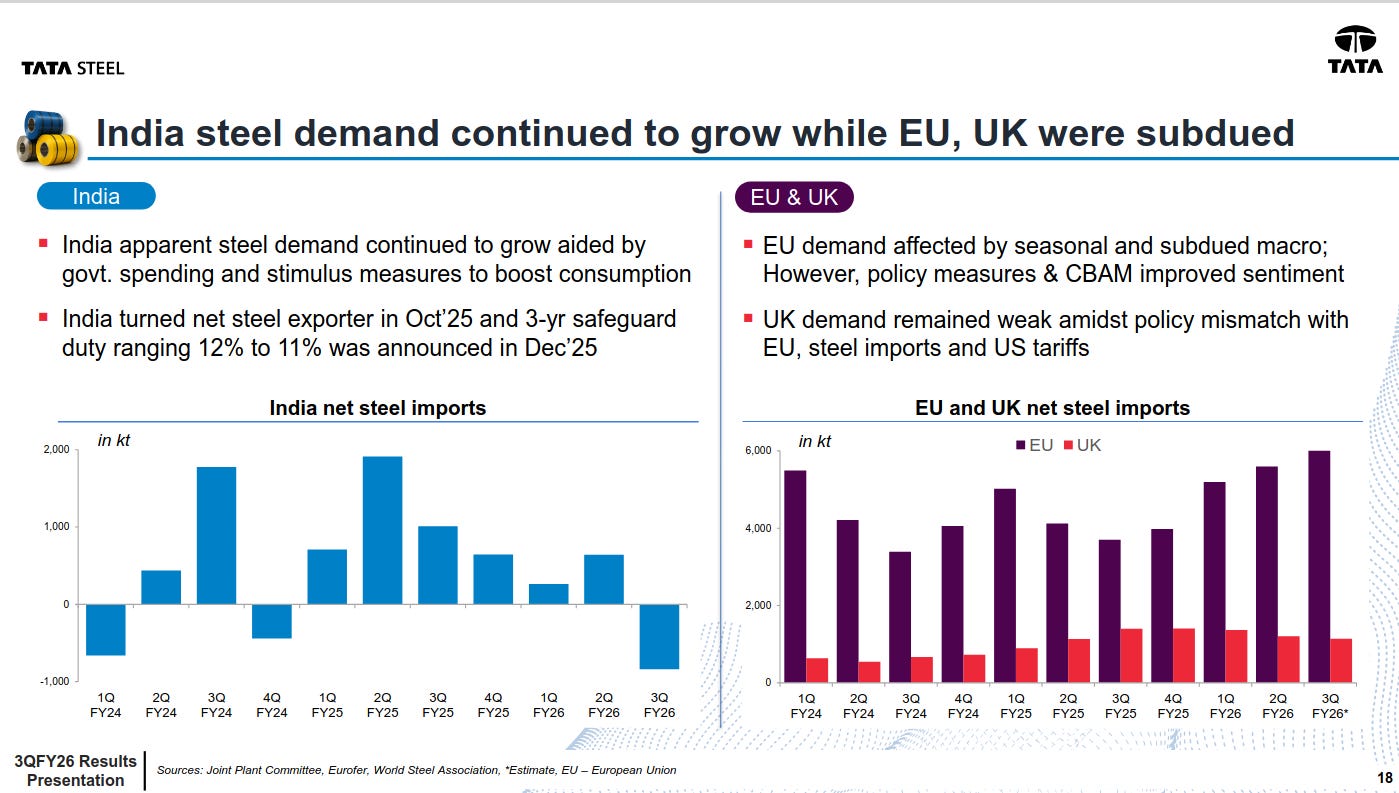

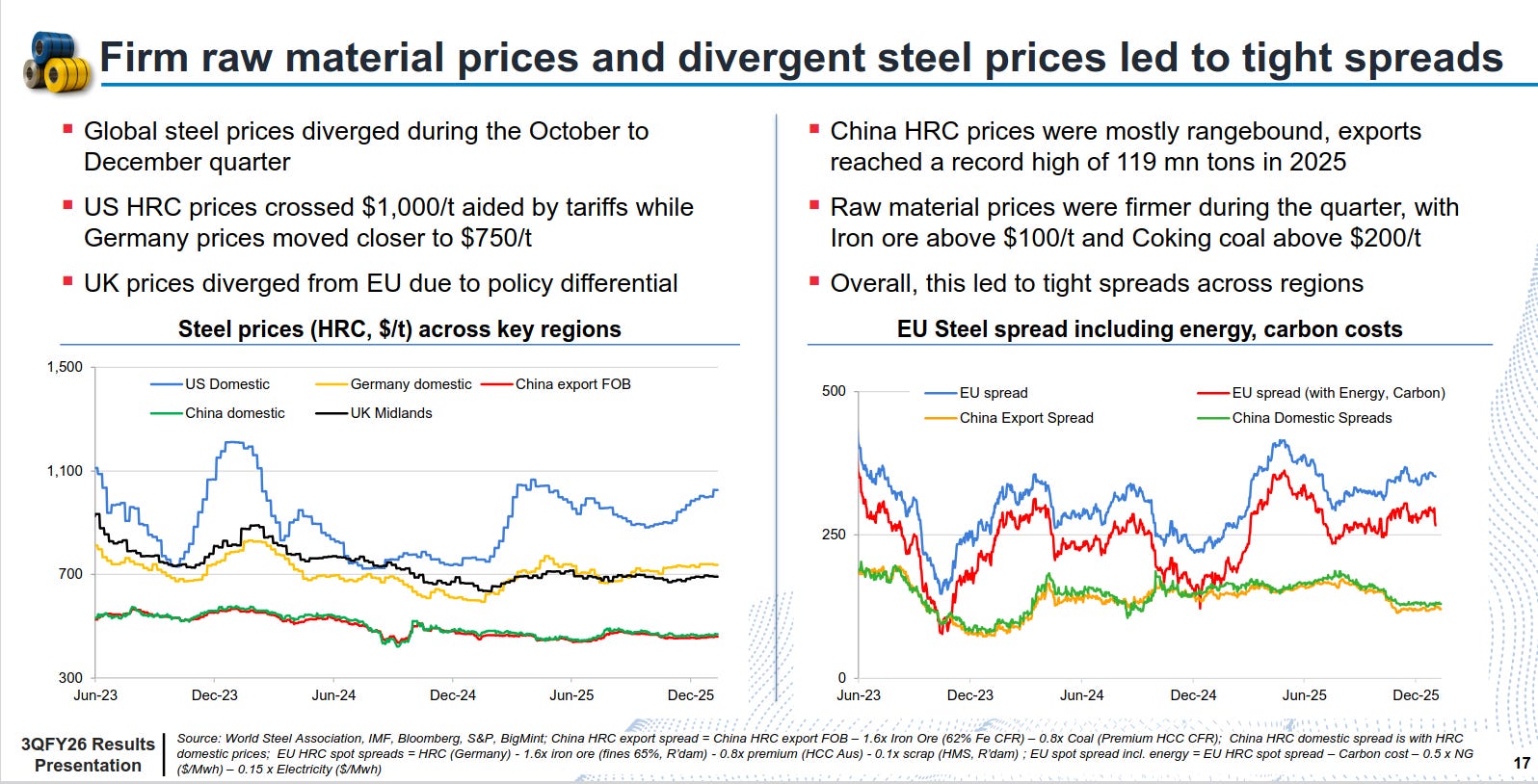

India’s steel demand remained resilient, supported by government spending and infrastructure push, while EU and UK demand stayed subdued due to macro and policy headwinds. India briefly turned a net exporter amid safeguard duty measures.

Firm iron ore and coking coal prices, along with divergent regional steel prices, compressed spreads during the quarter. Despite strong US pricing, elevated input costs kept overall margins tight across regions.

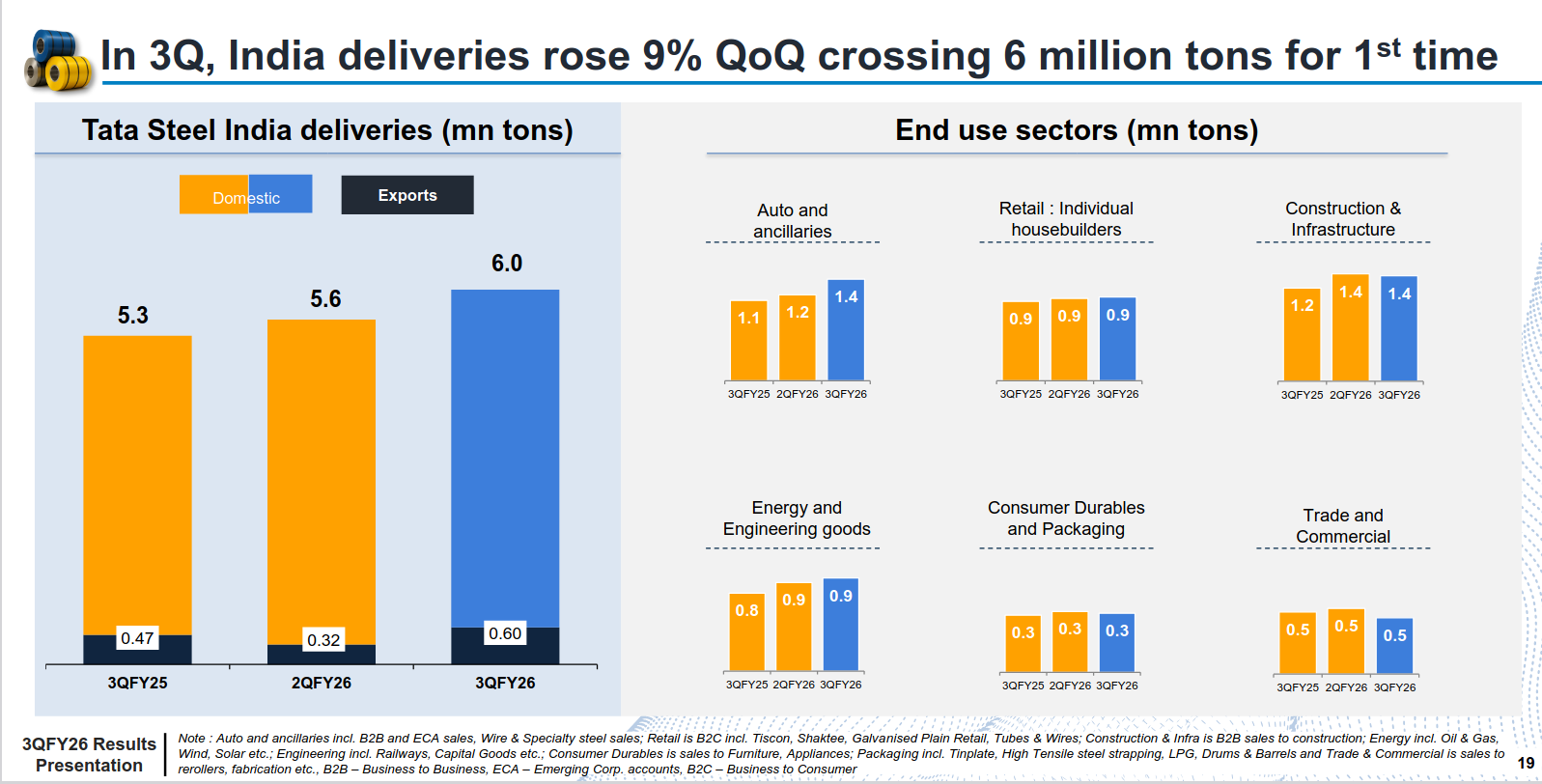

India deliveries rose 9% QoQ to a record 6 million tons, led by strong domestic demand. Auto, construction, infrastructure, and engineering segments contributed steadily to volume growth.

Auto Ancillary

Bosch | Large Cap | Auto Ancillary

Bosch is a top provider of technology and services in Mobility Solutions, Industrial Technology, Consumer Goods, and Energy and Building Technology. They also operate the largest development center outside Germany in India, focusing on engineering and technology solutions.

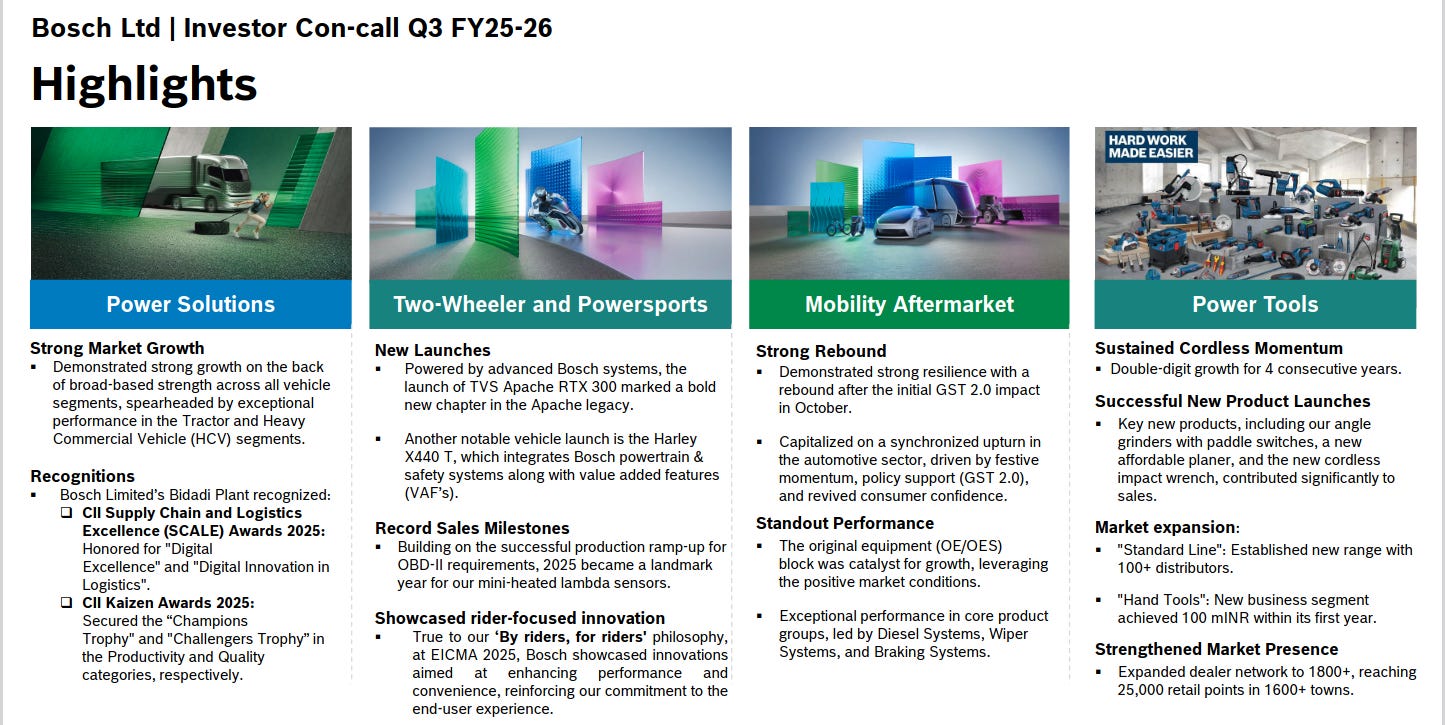

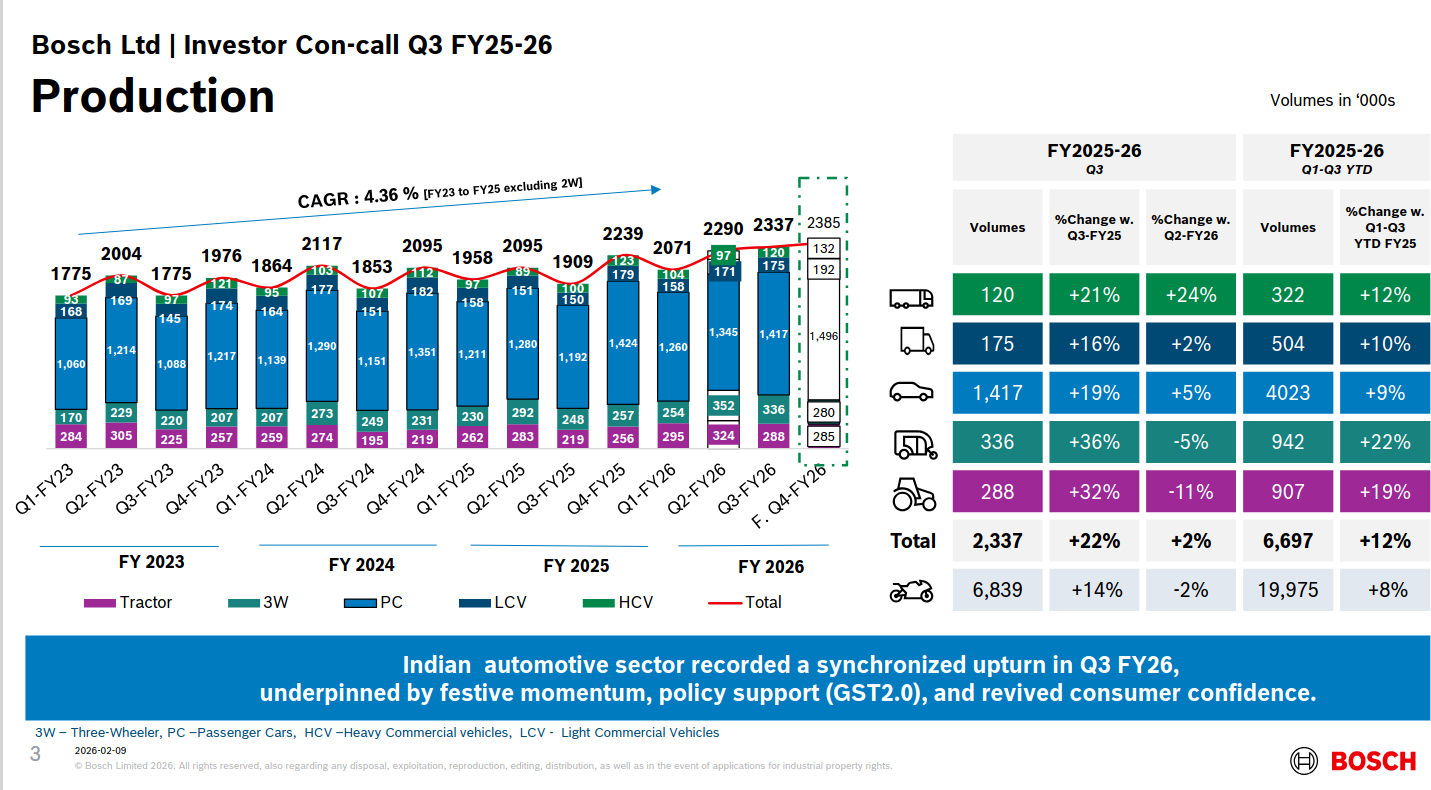

Bosch reported broad-based growth across Power Solutions, Two-Wheeler & Powersports, Mobility Aftermarket, and Power Tools, supported by strong demand, festive momentum, and new product launches. Aftermarket rebounded post GST 2.0, while Power Tools sustained double-digit growth and expanded distribution aggressively.

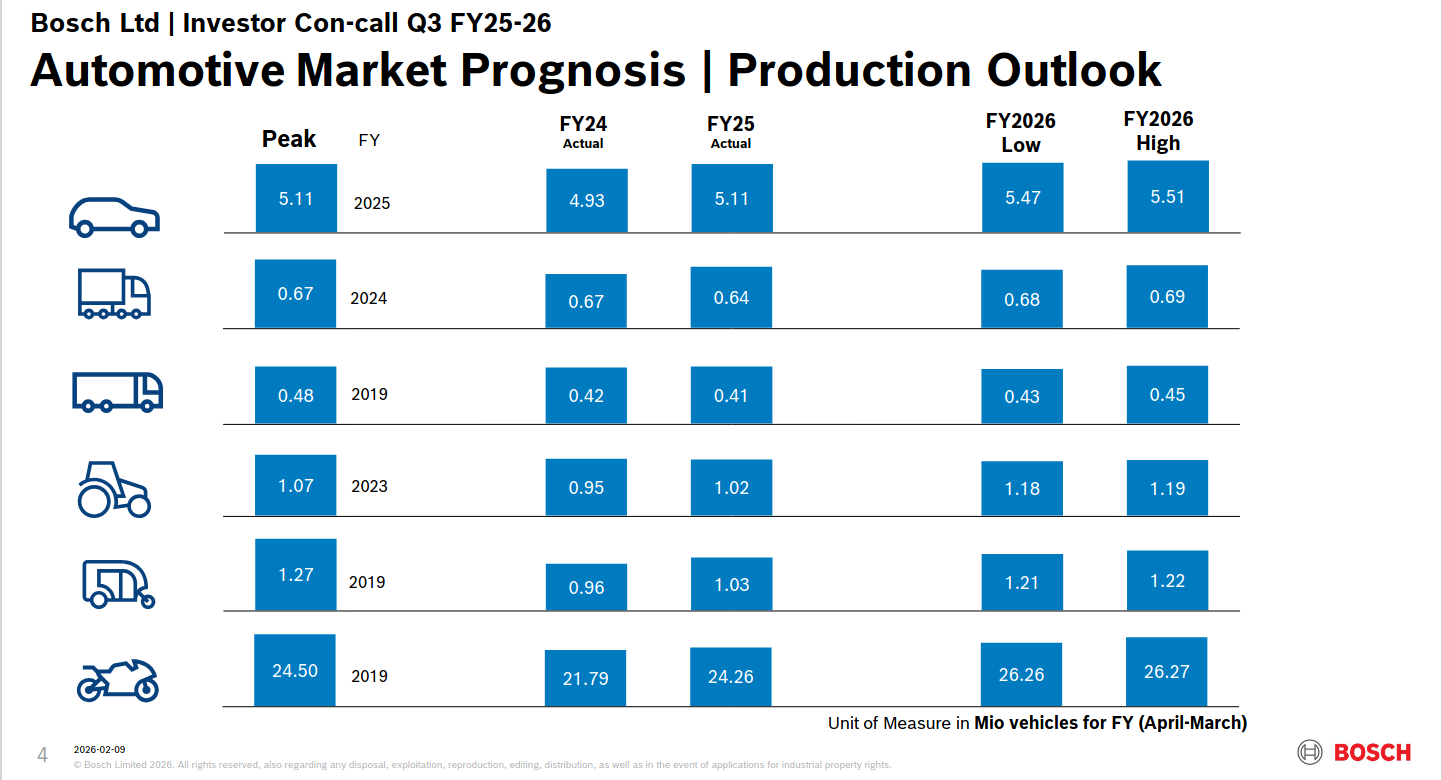

FY26 production outlook remains constructive across passenger vehicles, CVs, tractors, and two-wheelers, with volumes expected to exceed FY25 levels. The range-based forecast signals steady demand recovery, supported by policy support and improving macro conditions.

Production volumes rose strongly in Q3 FY26, reflecting a synchronized upturn in the Indian auto sector driven by festive demand and improved consumer confidence. Growth was led by passenger cars, LCVs, and tractors, with overall volumes showing healthy YoY and sequential expansion.

Samvardhana Motherson International Ltd. | Large Cap | Auto Ancillary

Samvardhana Motherson International manufactures and supplies components to automotive OEMs through its divisions: Wiring Harness, Vision Systems, and Polymer Products. The company aims to be a globally preferred sustainable solutions provider, offering diverse products and services to strengthen its market presence.

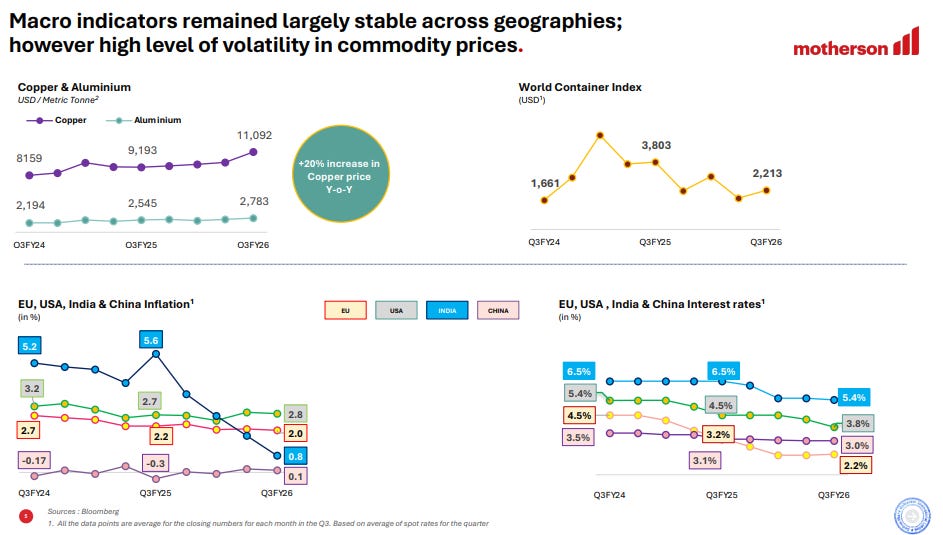

Macro indicators have stayed stable but commodity prices have swung wildly. Copper jumped 20% year on year while aluminum also rose steadily. The World Container Index spiked to $3,803 before falling back to $2,213. Inflation has cooled across the board with the EU down to 2.8%, the USA at 2.2%, and India and China both below 1%. Interest rates have eased slightly everywhere with the EU at 6.5%, the USA at 4.5%, and India and China around 3%.

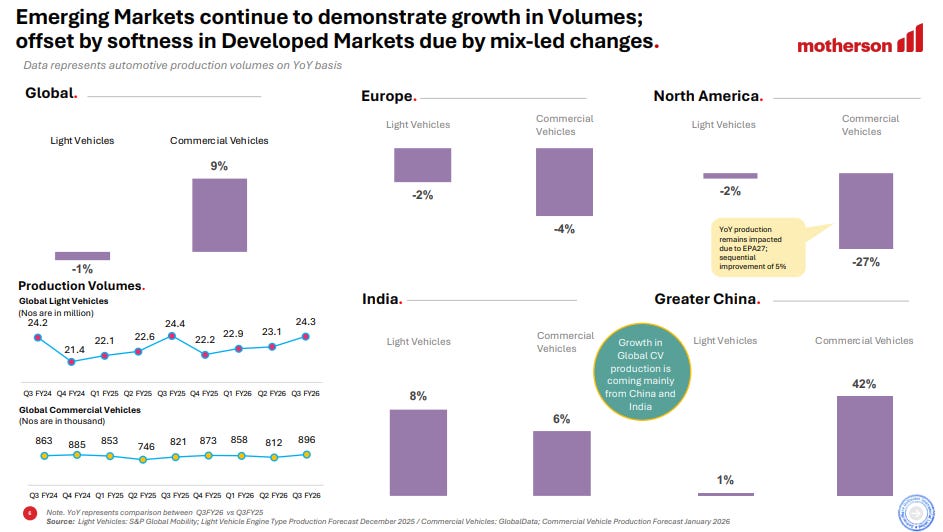

Global auto production is mixed. Light vehicles fell 1% but commercial vehicles rose 9%. Europe and North America both declined while India grew 6-8% across segments. Greater China led with a massive 42% jump in commercial vehicles. Most global growth is now coming from China and India.

Automobile

Tata Motors Passenger Vehicles Ltd. | Large Cap | Automobile

Tata Motors passenger Vehicles Ltd is a global automobile manufacturer known for cars and utility vehicles. With a focus on e-mobility solutions and innovation, it leads India’s commercial vehicles market and ranks highly in passenger vehicles. Tata Motors emphasizes engineering excellence and tech-enabled automotive solutions to meet evolving market and customer needs.

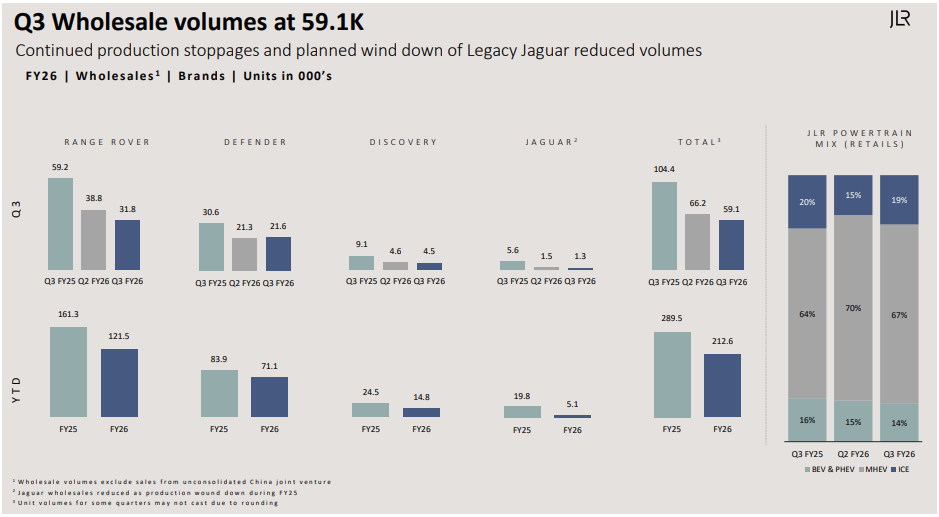

JLR’s Q3 wholesale volumes stood at 59.1K units, impacted by continued production stoppages and the planned wind down of Legacy Jaguar. Range Rover fell from 59.2K in Q3 FY25 to 31.8K in Q3 FY26, while Defender dropped from 30.6K to 21.6K. Discovery and Jaguar also saw declines, with Jaguar down to just 1.3K units. Total volumes decreased from 104.4K to 59.1K quarter on quarter and from 289.5K to 212.6K year on year. The JLR Powertrain mix for retails shows BEV rising from 16% in Q3 FY25 to 20% in Q3 FY26, while MHEV and ICE shares have adjusted accordingly.

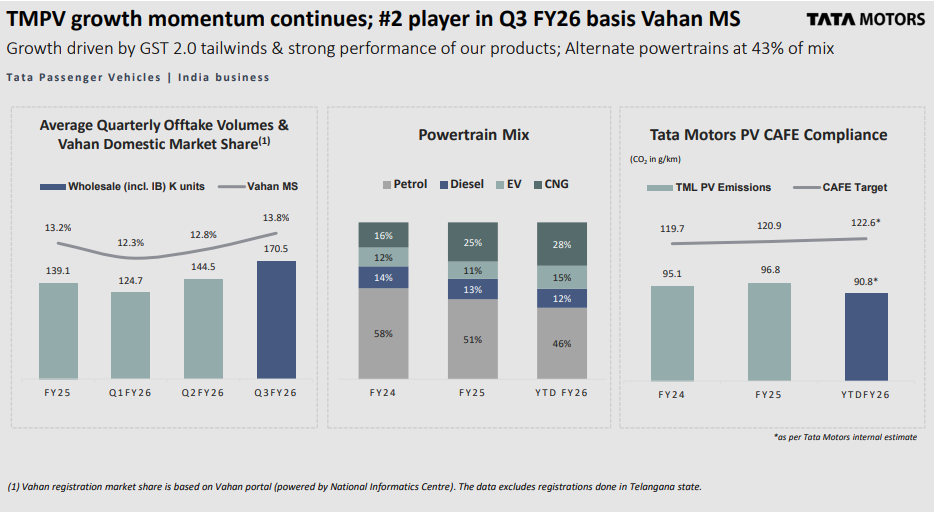

Tata Motors maintained strong growth momentum in Q3 FY26, becoming the #2 player on a Vahan MS basis. Average quarterly offtake volumes reached 170.5K units with Vahan domestic market share climbing to 13.8%. Growth has been driven by GST 2.0 tailwinds and strong product performance. The powertrain mix shows alternate powertrains now at 43% of the mix, with petrol dropping from 58% in FY24 to 46% YTD FY26, while EV and CNG have grown to 15% and 12% respectively. Tata Motors PV CAFE compliance has improved significantly with TML PV emissions falling from 119.7 g/km in FY24 to an estimated 90.8 g/km YTD FY26, comfortably below the CAFE target of 122.6 g/km.

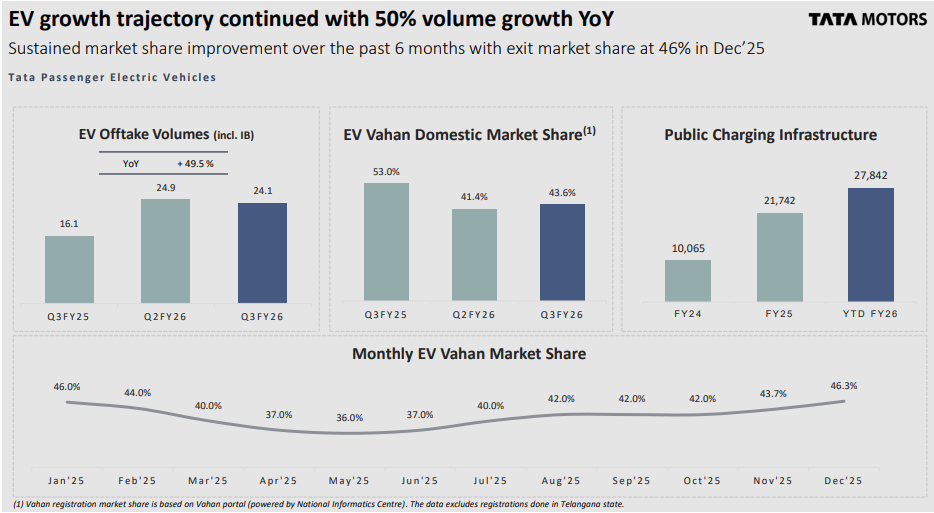

Tata Motors EV business continued its strong growth trajectory with 50% volume growth year on year. EV offtake volumes rose from 16.1K units in Q3 FY25 to 24.1K units in Q3 FY26, up 49.5% YoY. EV Vahan domestic market share has steadily improved from 53.0% in Q3 FY25 to 43.6% in Q3 FY26, with exit market share at 46% in December 2025. Monthly EV Vahan market share has recovered from a low of 36.0% in May 2025 to 46.3% by December 2025, showing sustained improvement over the past six months. Public charging infrastructure has expanded rapidly from 10,065 chargers in FY24 to 27,842 YTD FY26, supporting the growth of EV adoption.

Eicher Motors Ltd. | Large Cap | Automobile

Eicher Motors is a global automobile company based in Chennai, India, known for owning Royal Enfield, the oldest motorcycle brand in continuous production. It also co-owns VE Commercial Vehicles (VECV), a leader in commercial vehicle innovation. The company is publicly listed on the Bombay Stock Exchange and National Stock Exchange.

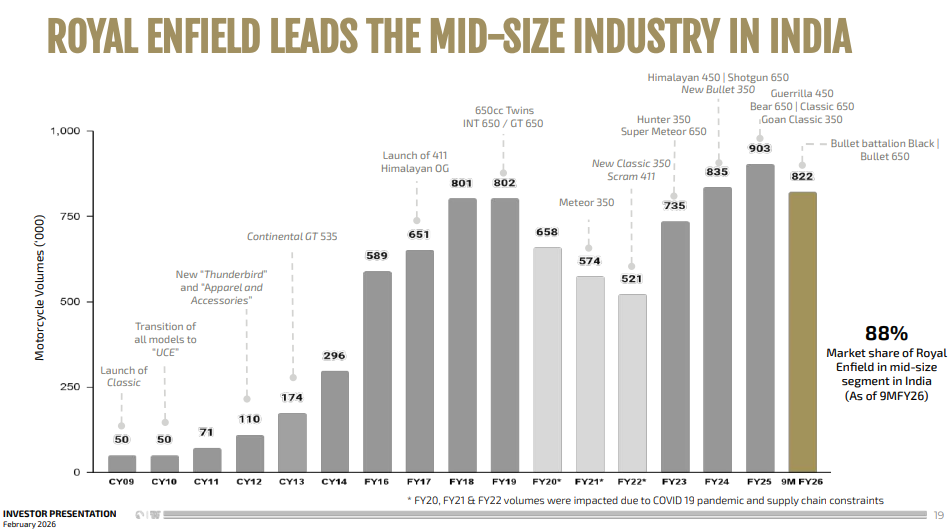

Royal Enfield dominates the mid-size motorcycle segment in India with an 88% market share as of 9MFY26. The company has grown steadily from 50K units in CY09 and CY10 to 903K units in FY25. Key milestones include the launch of the Classic in CY09, the transition to UCE engines, and the introduction of models like the Continental GT 535, Himalayan 450, Shotgun 650, and various 350cc and 650cc twins. Royal Enfield’s volume peaked at 903K in FY25 before dipping slightly to 822K in 9MFY26. The chart shows consistent growth driven by product expansion and new launches across multiple segments.

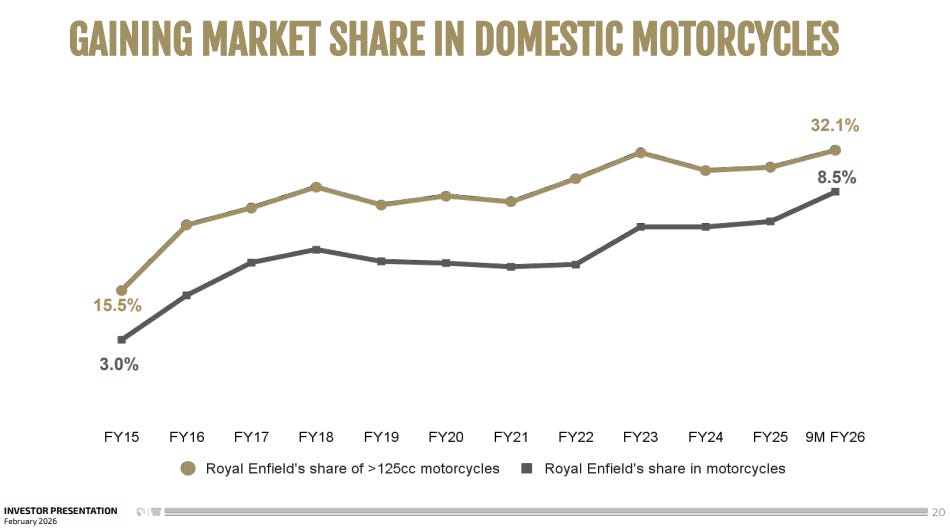

Royal Enfield has steadily gained market share in domestic motorcycles. In the overall motorcycle market, Royal Enfield’s share grew from 3.0% in FY15 to 8.5% in 9M FY26. In the over 125cc segment, its share jumped from 15.5% in FY15 to 32.1% in 9M FY26, peaking at around 32% in FY23. The consistent upward trend reflects Royal Enfield’s strong positioning and growing dominance in the mid-size and premium motorcycle categories.

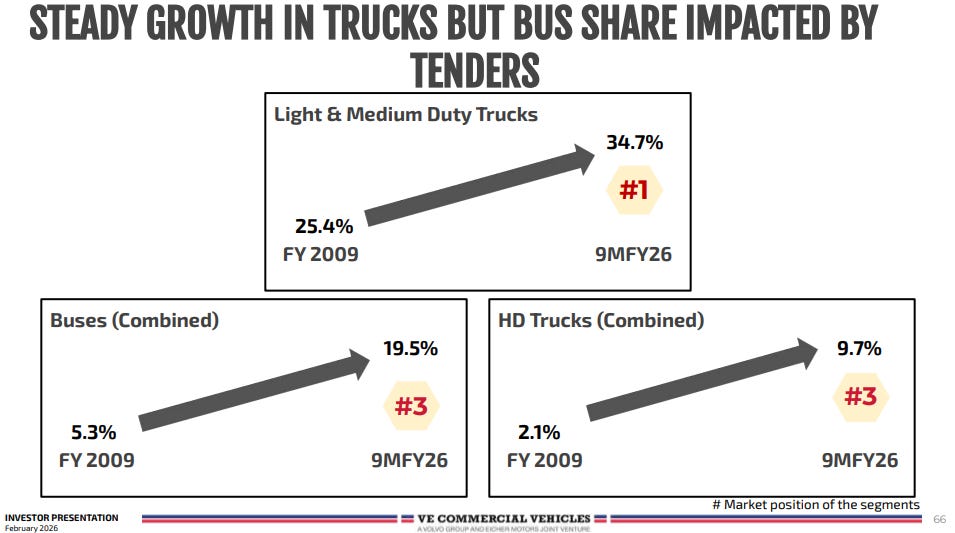

VE Commercial Vehicles (part of Eicher Motors) has shown steady growth in trucks while bus market share has been impacted by tenders. In light and medium duty trucks, VE’s market share rose from 25.4% in FY2009 to 34.7% in 9MFY26, securing the #1 position. In buses, the share climbed from 5.3% to 19.5%, ranking #3. Heavy duty trucks also grew from 2.1% to 9.7%, holding the #3 spot. VE Commercial Vehicles has strengthened its leadership in the light and medium duty truck segment while steadily gaining ground in buses and heavy duty trucks.

That’s it for now! Your feedback will really help shape how Points and Figures evolves. Drop it down in the comments below!

Quotes in this newsletter were curated by Meher, Kashish & Vignesh.

Disclaimer: We’ve used AI tools in filtering and cleaning up the quotes from the images so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Points and Figures is run by the same team that creates The Daily Brief and Aftermarket Report.