Sometimes, a single slide can explain more than a long report. Points and Figures is our way of breaking down what India’s leading companies are telling their shareholders and analysts. We comb through the decks, pull out the charts and data points that actually matter, and highlight the signals behind the numbers—whether about growth plans, margins, new markets, or risks on the horizon.

This is an extension of The Chatter. While The Chatter focuses on management commentary and earnings call transcripts, Points and Figures dives into investor presentations—and soon, even annual reports—to decode what companies are showing, not just what they’re saying.

We go through every major investor presentation so you don’t have to—bringing you the sharpest takeaways that reveal not just what the company is saying, but what it really means for the business, its sector, and the broader economy.

In this edition, we have covered 16 companies across 10 industries.

Energy

Power Grid Corporation

Adani Total Gas

Gujarat Gas Limited

Hindustan Petroleum Corporation Limited

JSW Energy Limited

Fertilizers

Chambal Fertilisers and Chemicals

Engineering & Capital Goods

Sanghvi Movers

Media & Entertainment

Basilic Fly Studio

Auto Ancillary

Escorts Kubota

UNO Minda Ltd.

Healthcare

Sun Pharmaceutical Industries

Cement

JK Cement Ltd.

Steel

JSW Steel

Retail

Kalyan Jewellers

Vishal Mega Mart Limited

Aviation

Interglobe Aviation Ltd. (Indigo)

Energy

Power Grid Corporation | Large Cap | Energy

Power Grid Corporation Of India operates a transmission network for power distribution and has diversified into telecom services by utilizing its transmission infrastructure. The company also offers consultancy services in areas such as power transmission, sub transmission, and distribution management.

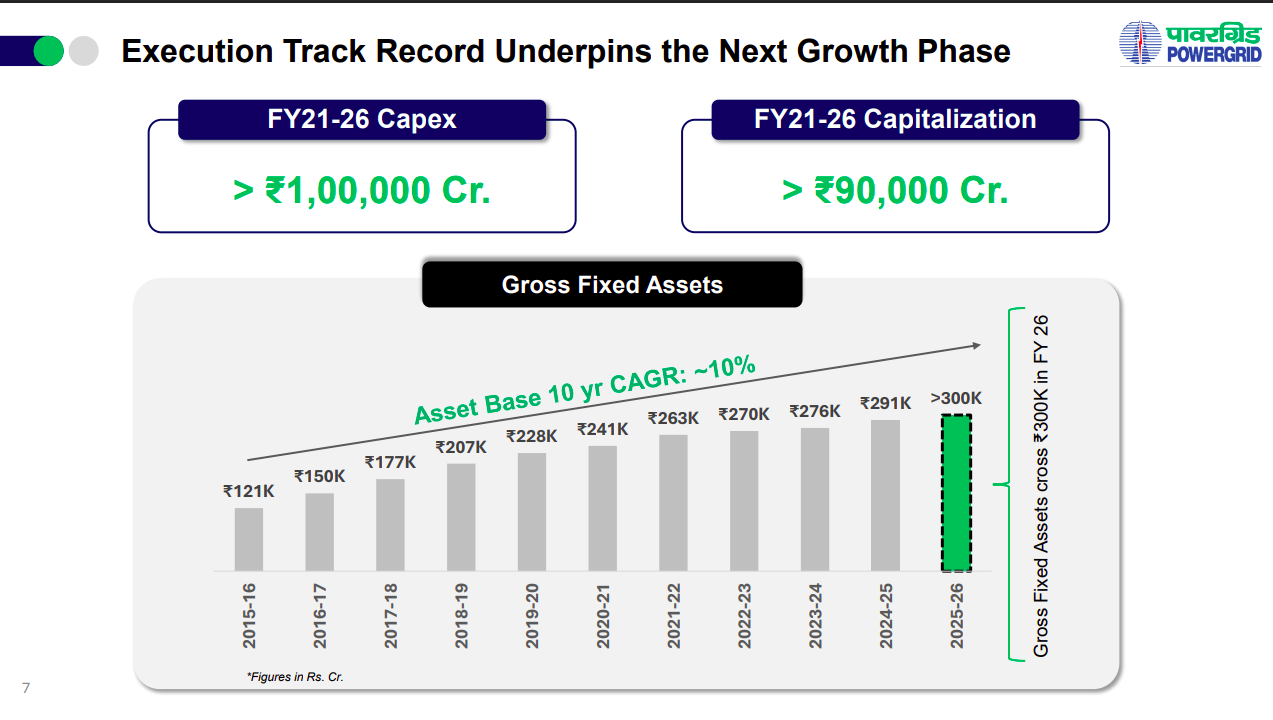

POWERGRID has compounded its asset base at ~10% CAGR over the last decade, with ₹1 lakh crore+ capex translating into ₹90,000+ crore capitalization. This reflects strong execution conversion and disciplined capital deployment.

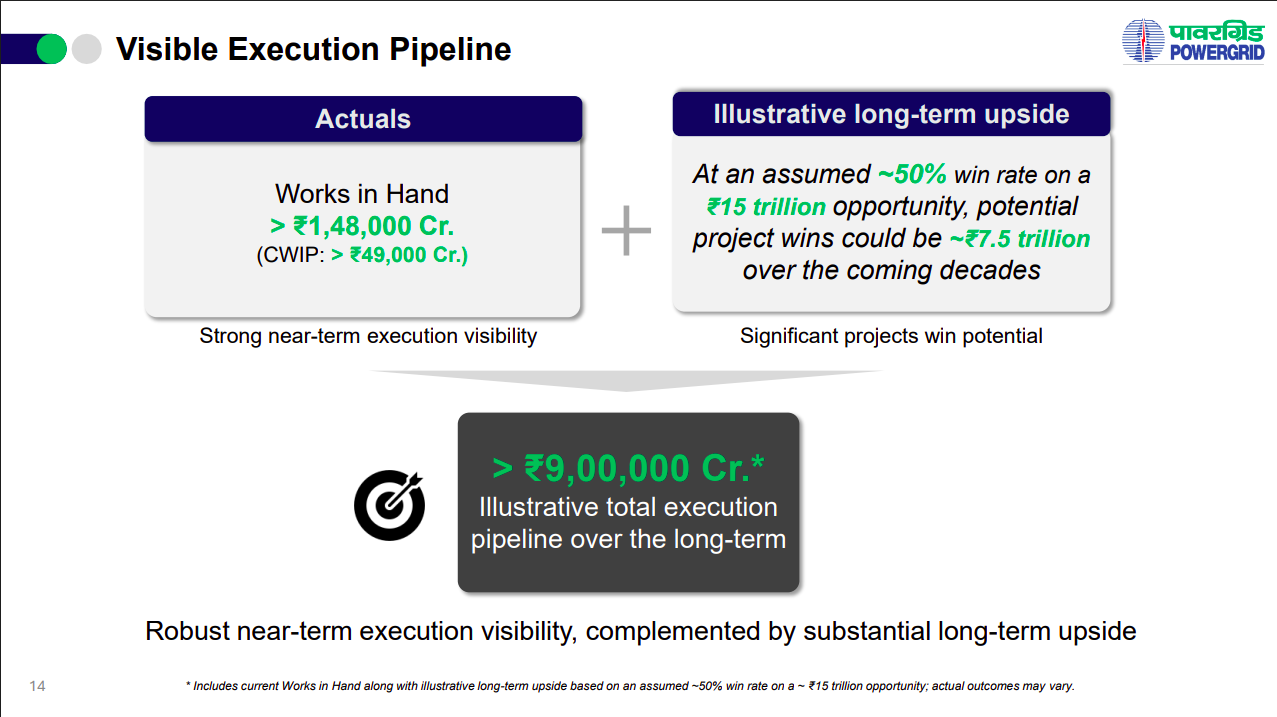

Near-term visibility remains robust with ₹1.48 lakh crore order book, while the long-term opportunity is massive. Even at a conservative win rate, this translates into a multi-lakh crore execution runway (~₹9 lakh crore).

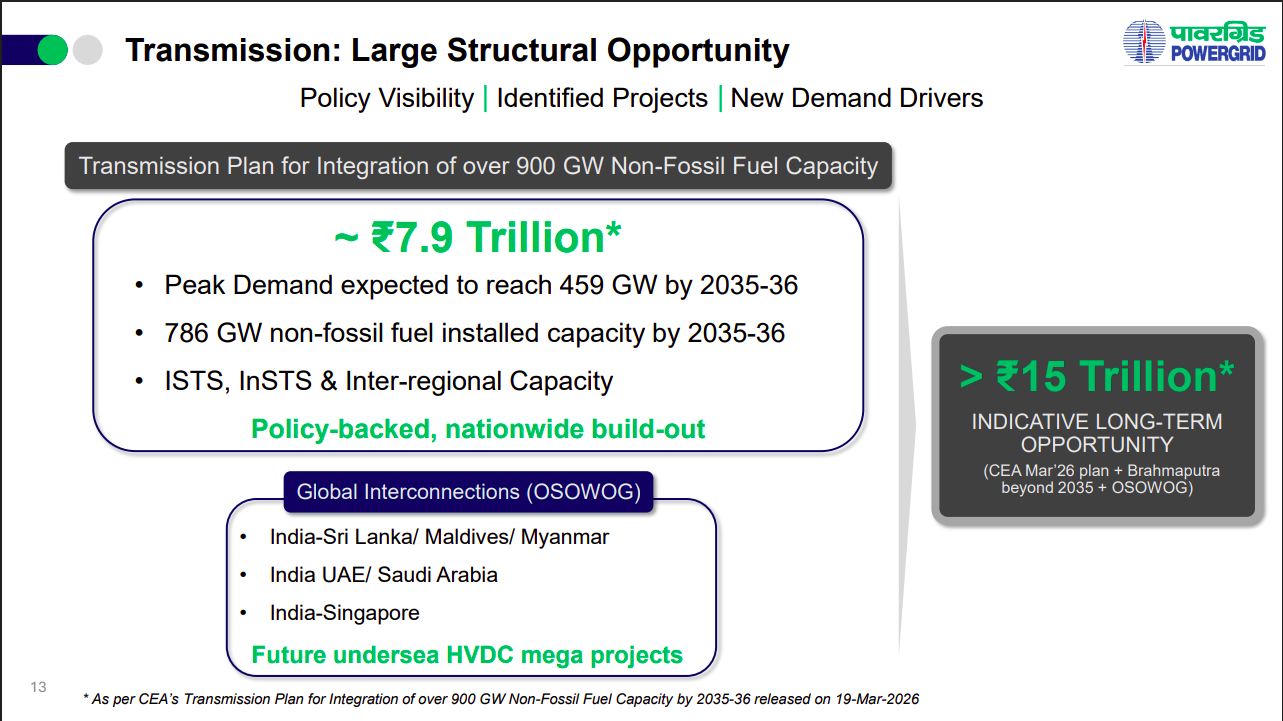

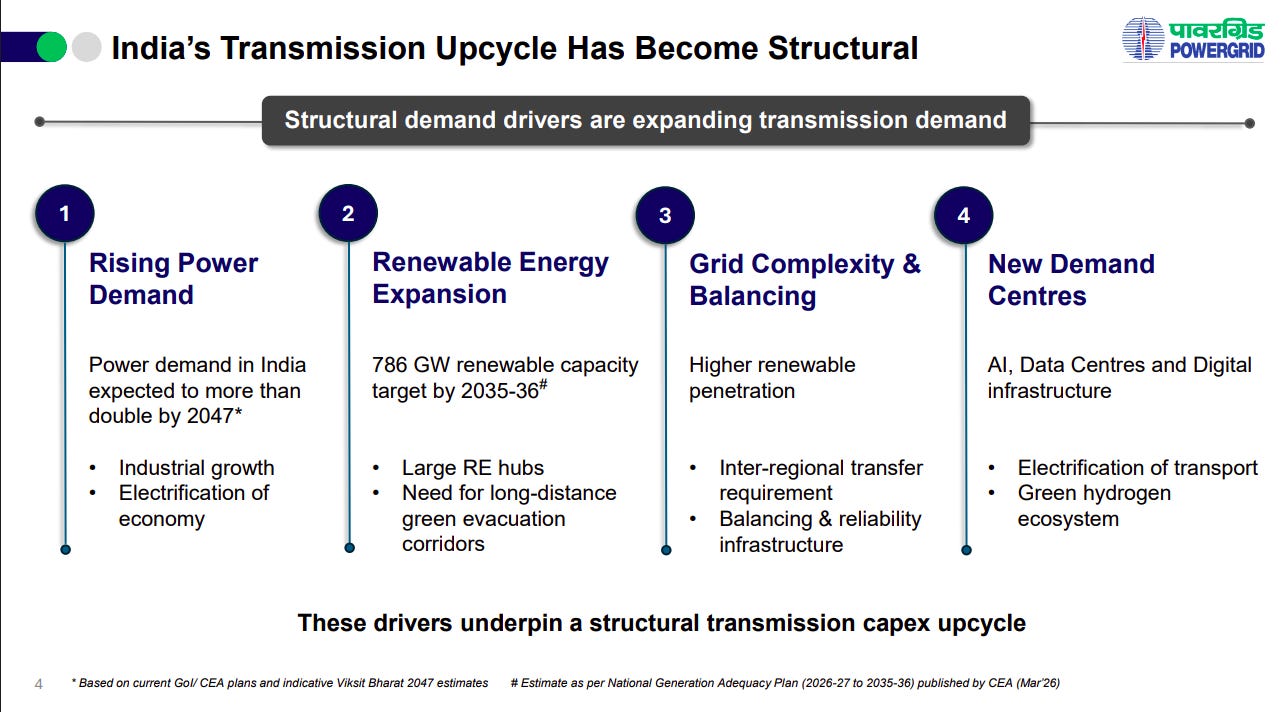

India’s transmission build-out is entering a policy-driven, multi-decade expansion phase, driven by renewables integration and rising demand. The opportunity size is ₹8–15 trillion, backed by nationwide grid expansion and cross-border connectivity.

A clear capex ramp-up is underway (₹82,000 crore planned over FY27–28), which should translate into steady capitalization growth (~₹65,000 crore). This underpins earnings visibility given the regulated return model.

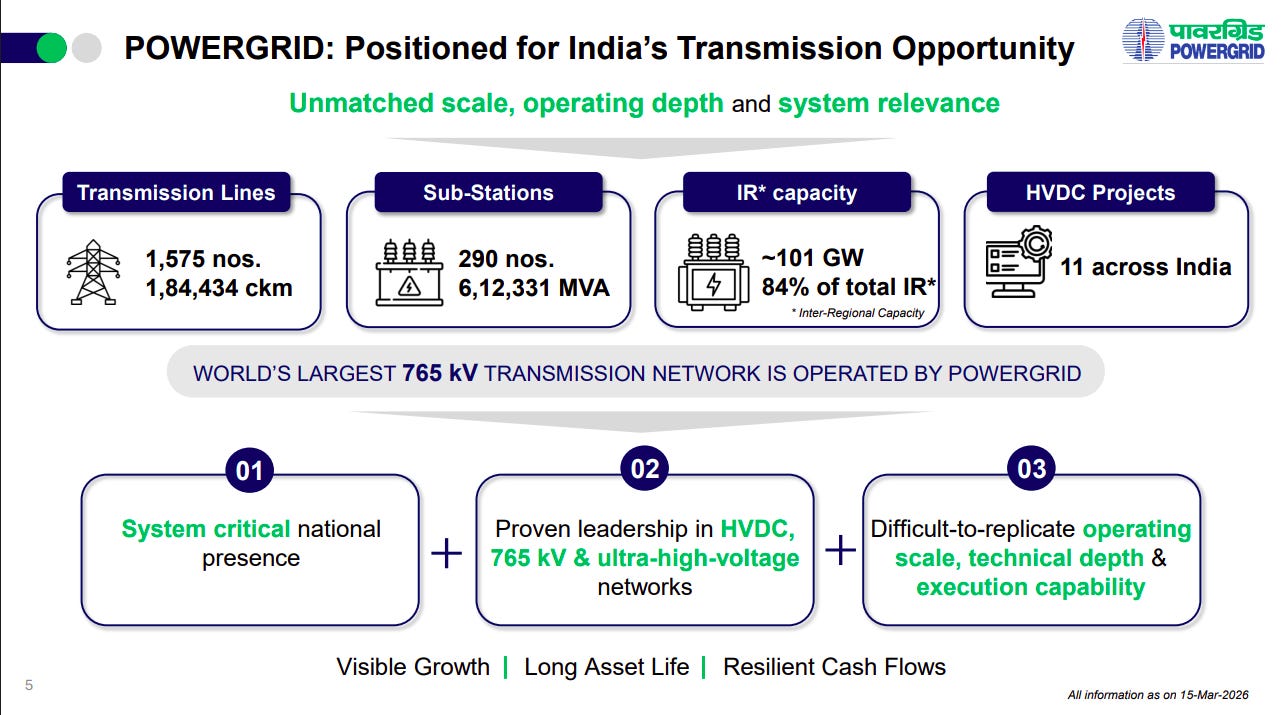

POWERGRID holds a system-critical position with unmatched scale in transmission, leadership in HVDC, and dominant inter-regional capacity. Its deep execution capability and high entry barriers create a durable moat that is difficult to replicate.

Transmission demand is being driven by long-term structural shifts—rising power demand, renewable expansion, and increasing grid complexity. This makes the capex cycle sustained and predictable rather than short-lived.

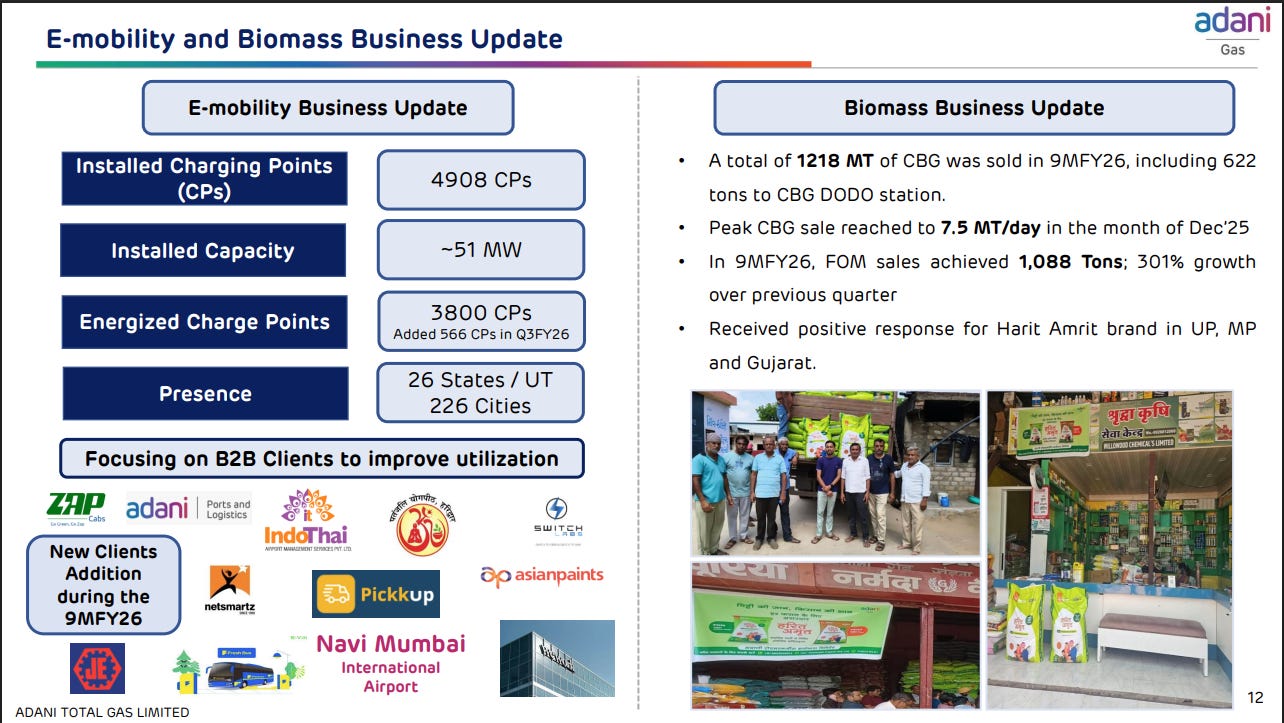

Adani Total Gas | Mid Cap | Energy

Adani Total Gas operates in the City Gas Distribution (CGD) sector, supplying natural gas to domestic, commercial, industrial, and vehicular users. The company is expanding its PNG network and promoting CNG as a cleaner fuel alternative. Additionally, it explores bio gas, bio fuel, EV, hydrogen, and other clean energy solutions to enhance sustainable energy access and reduce emissions across its operational areas.

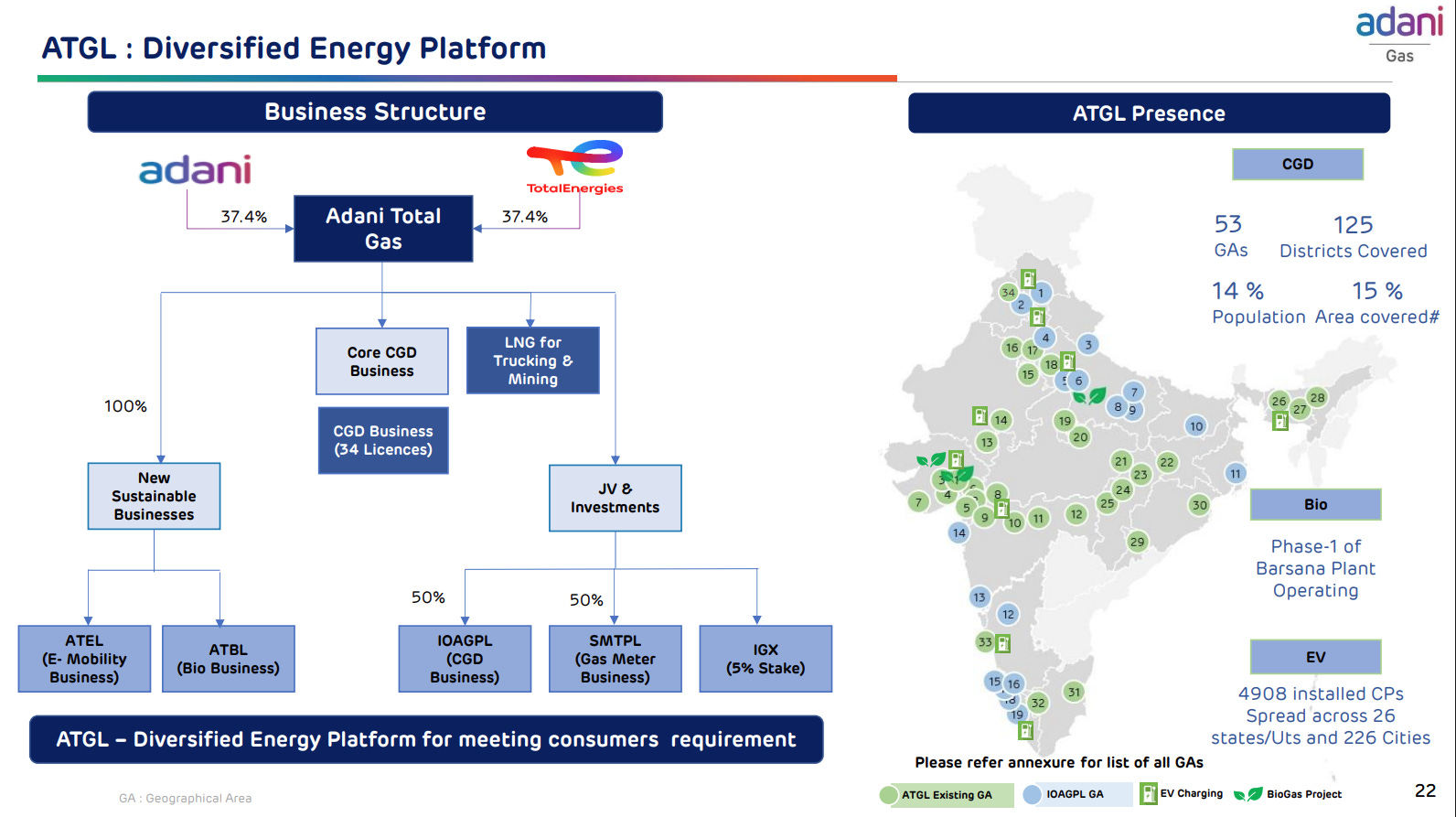

Adani Total Gas is positioning itself as more than just a city gas distributor—evolving into a diversified energy platform spanning core CGD, LNG, EV charging, and bio energy. While the core CGD business (34 licenses across 53 GAs) remains the backbone, the structure shows a clear push into adjacencies through JVs and new-age businesses, signalling a broader play on India’s energy transition rather than a pure gas utility story.

ATGL’s new energy bets are beginning to scale, with EV charging expanding to ~4,900 points across 226 cities and biomass seeing steady traction with rising CBG volumes and strong growth in FOM sales. The focus on B2B clients to improve utilization and early positive response to its bio-energy brand suggest these adjacencies are moving from pilot phase to meaningful contributors, supporting ATGL’s broader transition beyond traditional gas distribution.

Gujarat Gas Limited | Mid Cap | City Gas Distribution

Gujarat Gas is India’s largest city gas distribution player, operating a vast network across 44 districts in multiple states. The company provides natural gas to industrial, domestic, and commercial segments while maintaining a dominant and expanding CNG station footprint.

Industrial dominance makes volumes a proxy for manufacturing cycles and fuel-switching economics. This exposure links margins directly to the price gap between gas and alternative fuels.

Expanding to 27 bio-gas agreements helps decouple supply from volatile global gas pricing and currency risks. This localization strategy protects unit margins while ensuring compliance with green energy mandates.

The 12 MW captive solar project reduces fixed utility costs for CNG stations and corporate offices. Generating power internally protects margins from rising grid tariffs as the retail network expands geographically.

Hindustan Petroleum Corporation Limited | Large Cap | Oil & Gas - Refining & Marketing

HPCL is a leading Indian Maharatna central public sector enterprise operating large-scale refineries and a massive fuel marketing network. The company maintains a significant share in domestic petroleum product sales and is actively diversifying into natural gas and renewable energy.

HPCL’s 20.3% market share significantly outpaces its 13.87% refining capacity, creating a structural reliance on external product purchases. Expanding refining capacity is essential to internalizing margins and reducing exposure to volatile procurement costs.

Expansion into 25 city gas geographic areas and a 5 MMTPA LNG terminal signals a strategic shift toward a lower-carbon energy mix. This diversification builds stable utility-based revenue to buffer against cyclical refining and marketing volatility.

HPCL’s 302 granted patents and focus on indigenous catalysts signal a pivot toward technological self-reliance. Reducing dependence on foreign licenses helps lower operating costs and protect long-term refining margins.

Operating refineries at 105-115% utilization indicates that HPCL has reached its internal production ceiling. Future earnings growth is now highly sensitive to global price spreads rather than further volume gains.

Rapidly scaling CNG and EV charging stations ensures HPCL retains its retail dominance as consumer mobility patterns shift. This infrastructure pivot hedges against long-term demand risks for traditional petrol and diesel.

Increasing refining capacity to 45.3 MMTPA captures integrated margins by eliminating the need for expensive third-party fuel purchases. This self-sufficiency protects earnings from volatile global price spreads.

Scaling CNG and petrochemical capacity provides a strategic hedge against plateauing domestic demand for traditional fuels. This diversification secures growth in cleaner energy markets while reducing terminal value risk.

Expanding biofuel capacity to 300 TMT reflects a structural response to domestic blending mandates. Success in this segment is critical for protecting marketing margins as traditional fuel demand slows.

Commissioning refinery-based green hydrogen plants marks a shift from research to industrial-scale application. Developing this technology is vital for future-proofing refining assets against tightening environmental regulations.

Relying on biogas for nearly half of emission reductions indicates a strategy focused on scalable, proven technology. Investors must weigh this massive capital commitment against long-term regulatory survival.

JSW Energy Limited | Large Cap | Utilities - Power Generation

JSW Energy is a leading Indian power producer transitioning from a thermal-heavy base to a diversified green energy portfolio. The company operates across the power value chain, including generation, transmission, and now green hydrogen production.

Liquidity risk has decreased as debtor days fell from 96 to 73, providing the cash flow stability required for heavy capital investments. Shifting toward higher-quality offtakers like SECI and group captives secures more predictable collection cycles.

Transitioning to a 14 GW renewable pipeline secures long-term yields and protects margins from spot-market price volatility. This strategic shift moves the portfolio away from fuel-sensitive assets toward stable, green infrastructure.

Targeting 40 GWh of energy storage creates a structural moat by addressing renewable intermittency and capturing premium peak-demand pricing. Dominance in pumped hydro assets provides a significant competitive advantage over standard solar or wind generators.

Doubling capacity through renewables secures long-term cash flows and hedges against future carbon-related regulatory costs. This expansion strategy locks in grid access before infrastructure bottlenecks limit new additions.

Renewables are actively displacing thermal generation, which has contracted to 73% of the total generation mix. Incremental demand is increasingly captured by green assets that benefit from lower variable costs.

Fertilizers

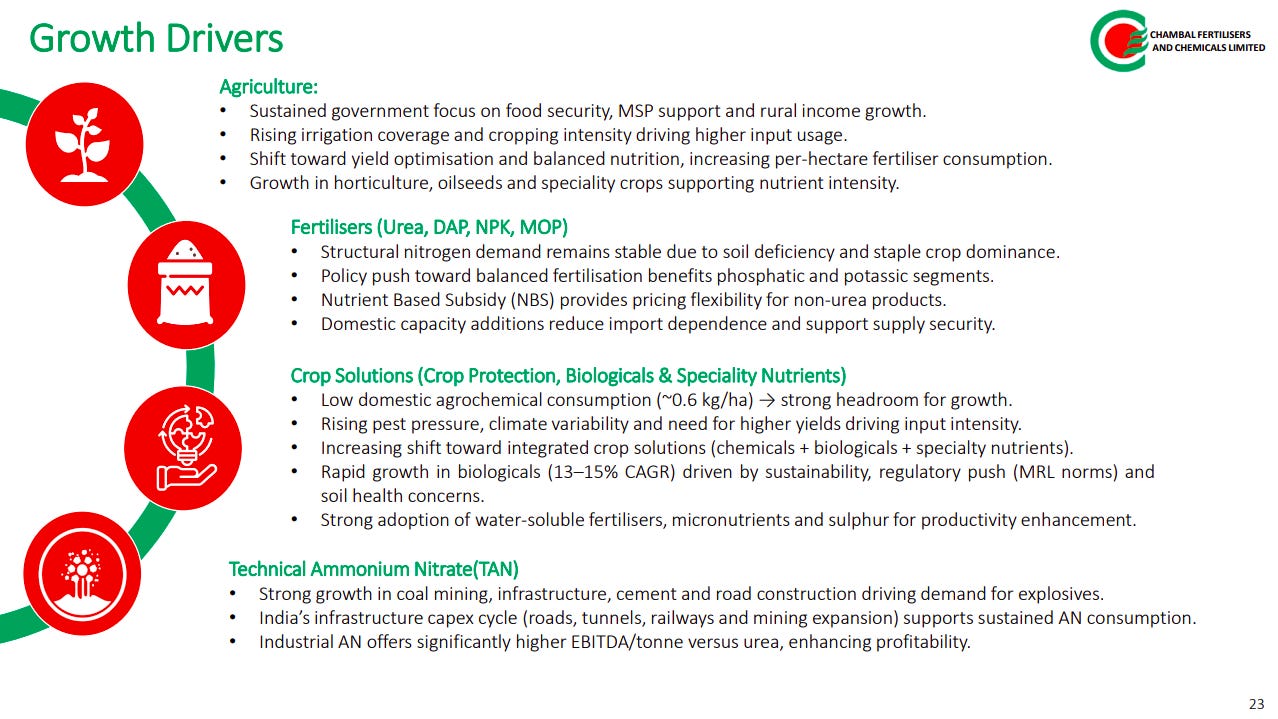

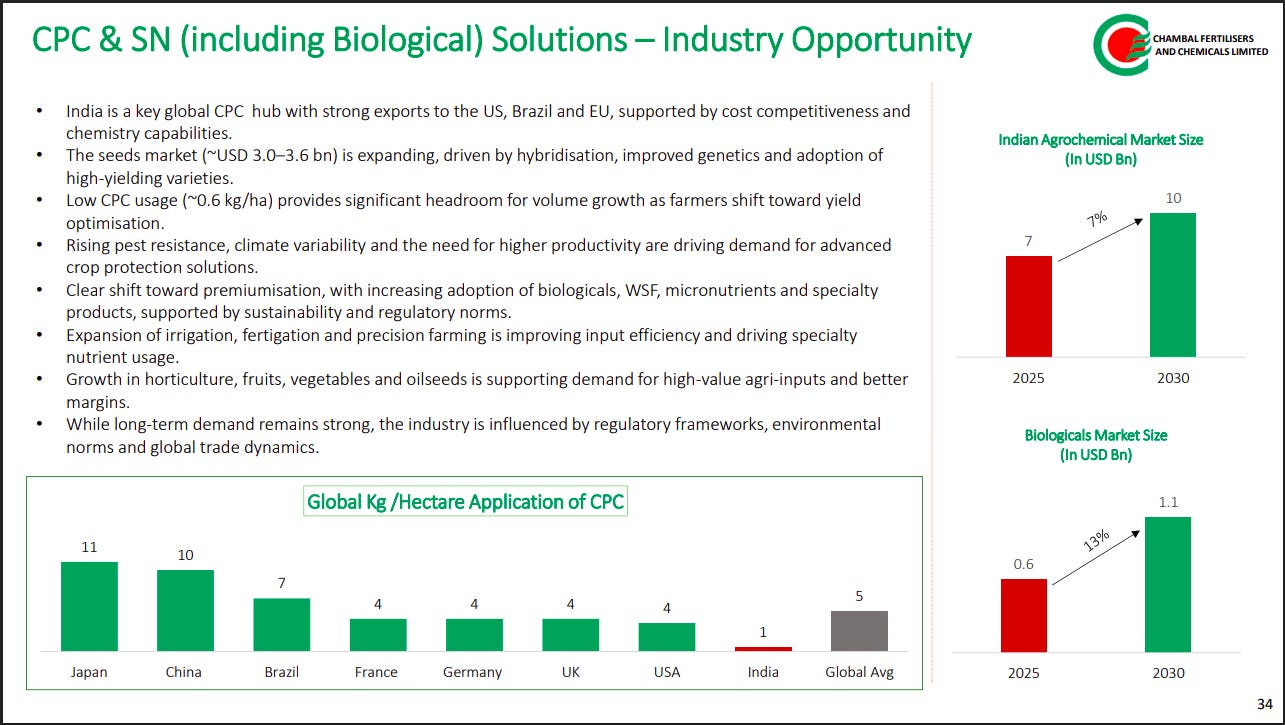

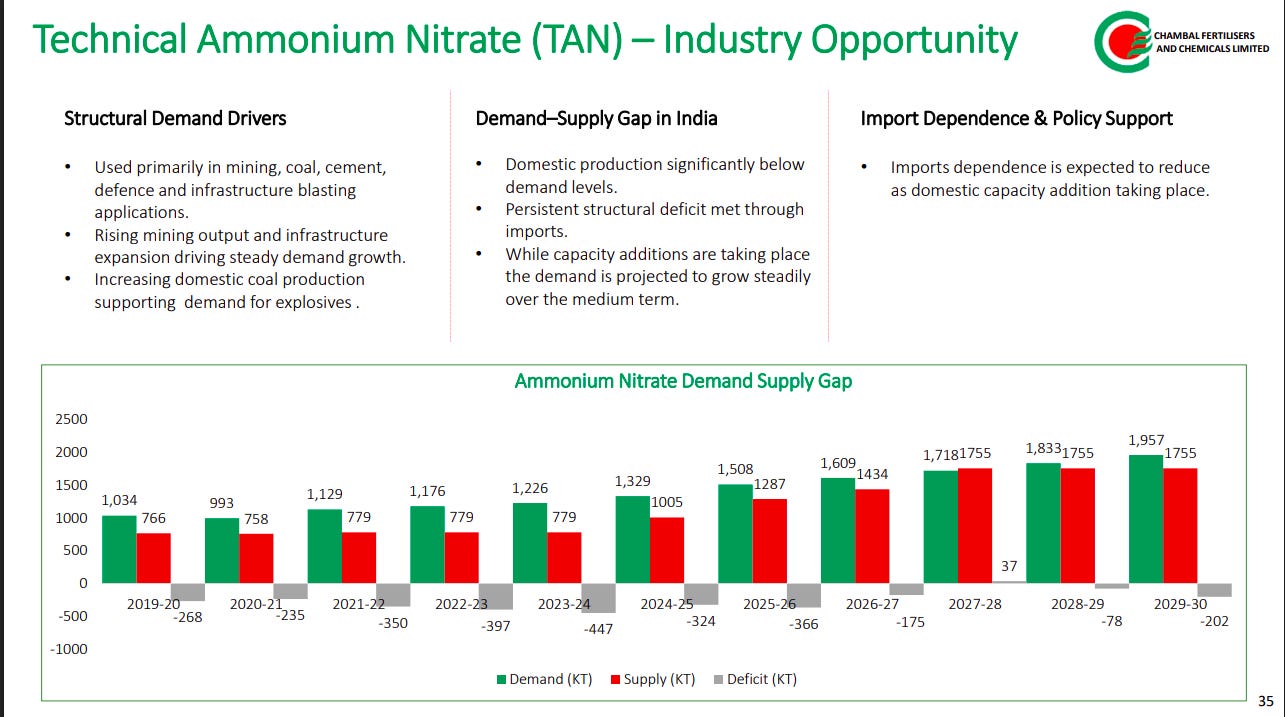

Chambal Fertilisers and Chemicals | Small Cap | Fertilizers

Chambal Fertilisers and Chemicals Limited is a major player in the production of Urea, fertilisers, and Agri-inputs. It serves farmers in multiple regions of India and holds a significant position as a fertilizer supplier in states like Rajasthan, Madhya Pradesh, Punjab, Uttar Pradesh, Bihar, Chhattisgarh, and Haryana.

Fertiliser demand is structurally supported by food security focus, irrigation expansion, and shift toward balanced nutrition. Beyond urea, growth is increasingly coming from specialty nutrients, crop protection, and biologics, while TAN offers a high-margin industrial growth lever linked to infra and mining.

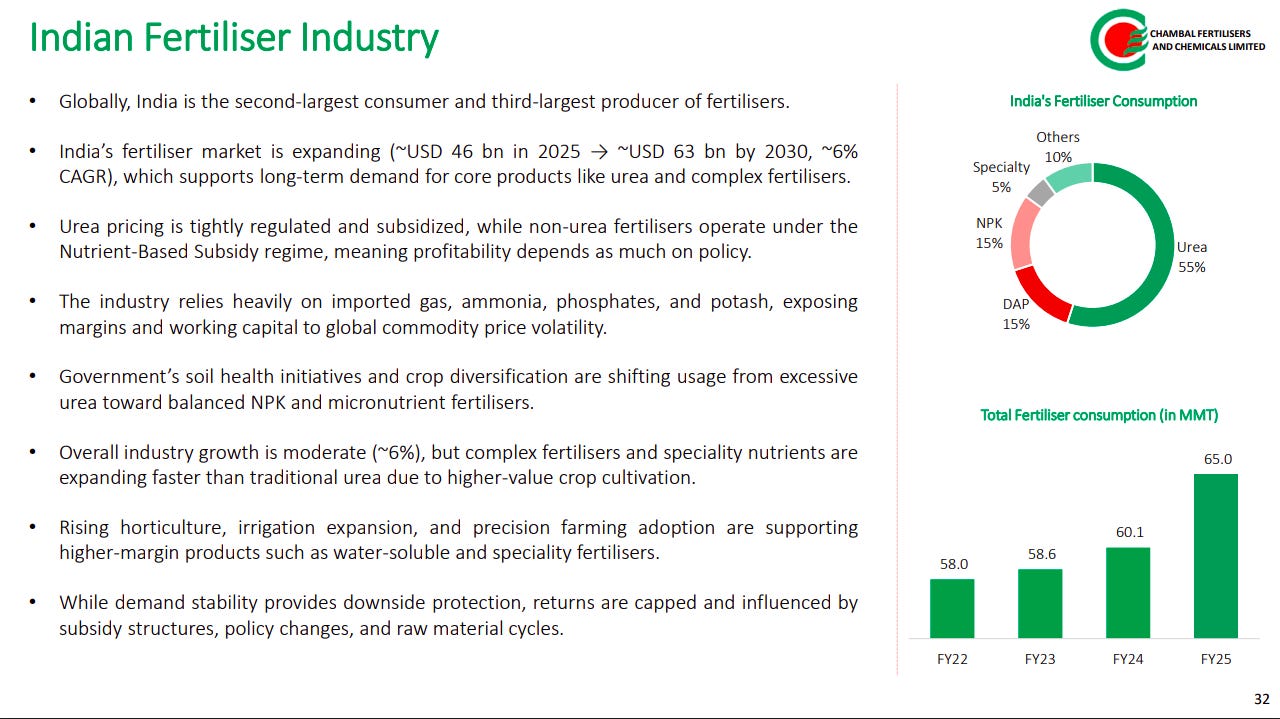

India is a large, policy-driven market (~$46bn → $63bn by 2030, ~6% CAGR) with stable demand but capped returns due to subsidy control. The real growth lies in non-urea, complex fertilisers and specialty inputs, supported by crop diversification and precision farming.

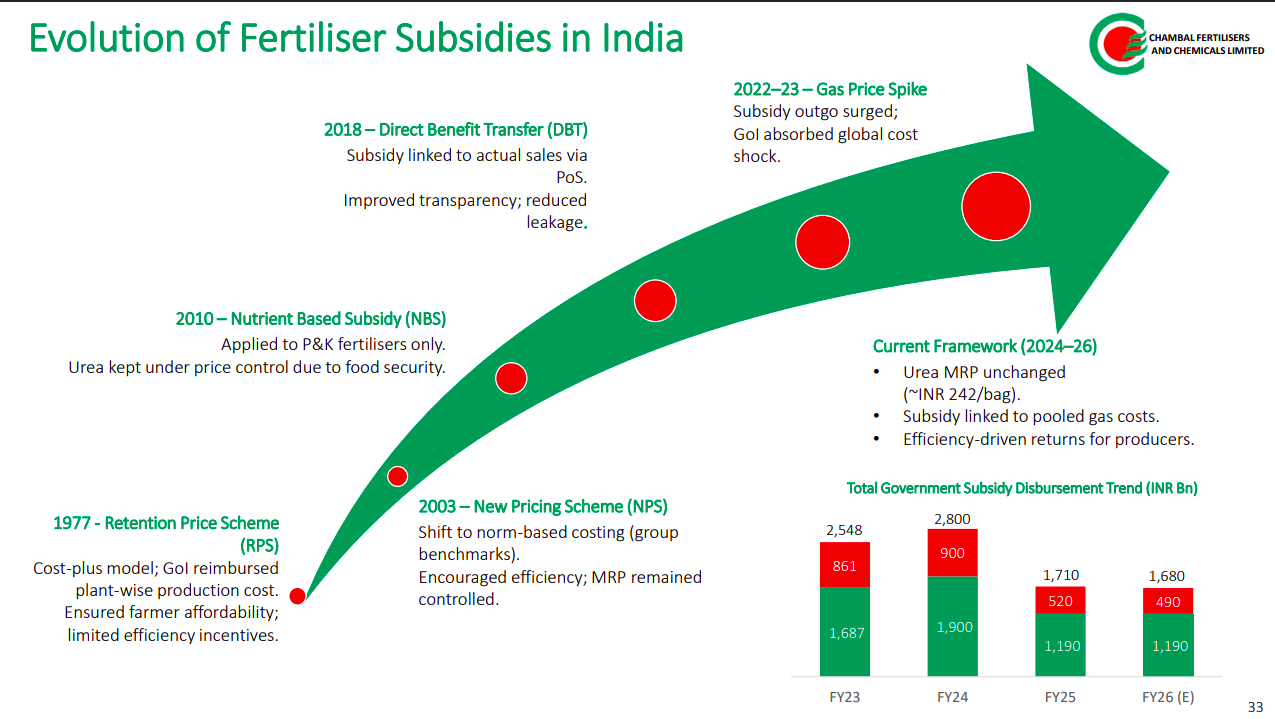

The sector has transitioned from cost-plus (RPS) to efficiency-linked regimes (NBS, DBT), improving transparency and discipline. However, earnings remain tightly linked to gas prices and subsidy payouts, with FY23–24 highlighting how global shocks can distort profitability.

India has very low agrochemical intensity (~0.6 kg/ha vs global 4–10 kg), creating significant headroom for growth. Premiumisation (biologicals, WSF, micronutrients) and export competitiveness position this segment as the key margin expansion lever.

TAN demand is driven by mining, infrastructure and explosives, with a persistent domestic supply deficit. Capacity additions may reduce imports, but structurally this remains a tight, high-margin segment with strong volume visibility.

Subsidy receivables remain a core working capital swing factor, with improving trends but still elevated levels. While payouts are stabilising, cash flow visibility in fertilisers continues to be policy-dependent rather than purely operational.

Engineering & Capital Goods

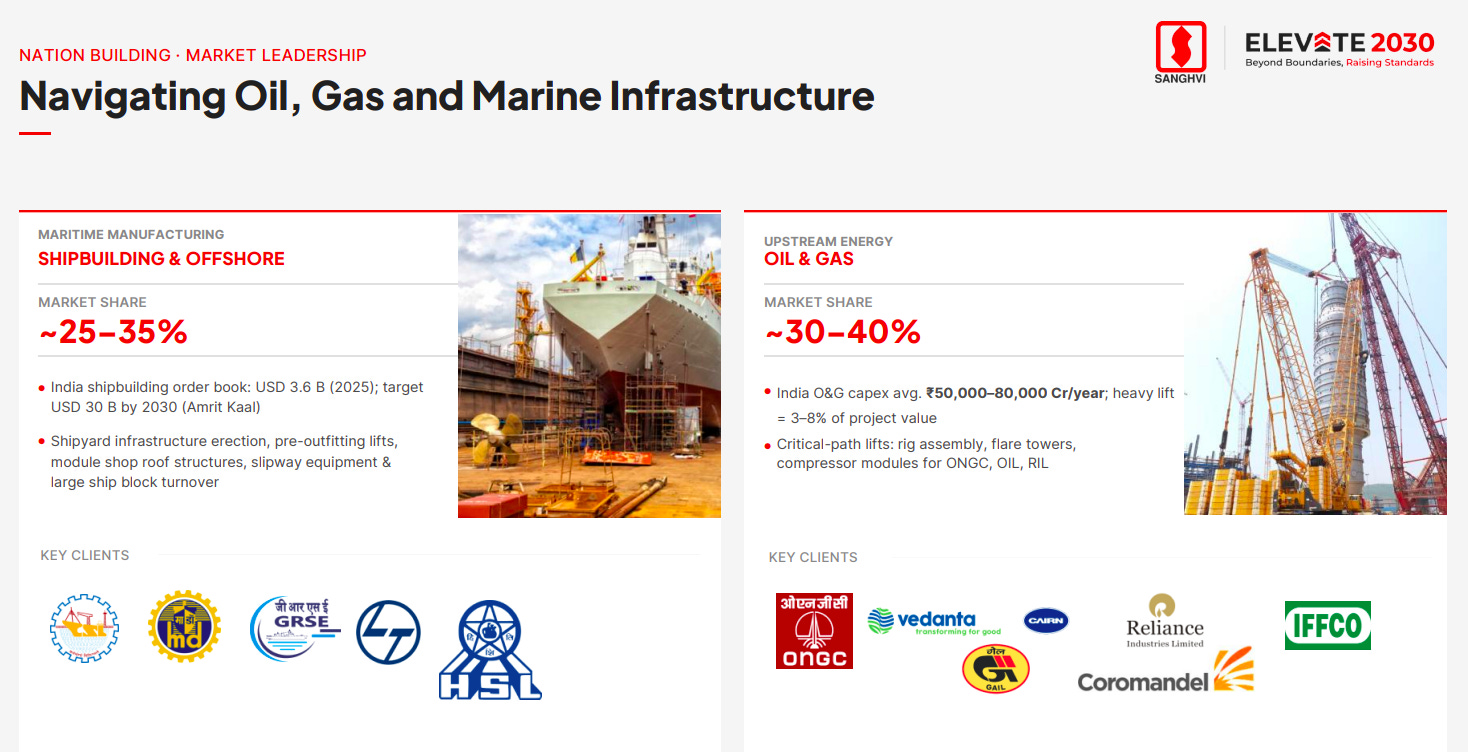

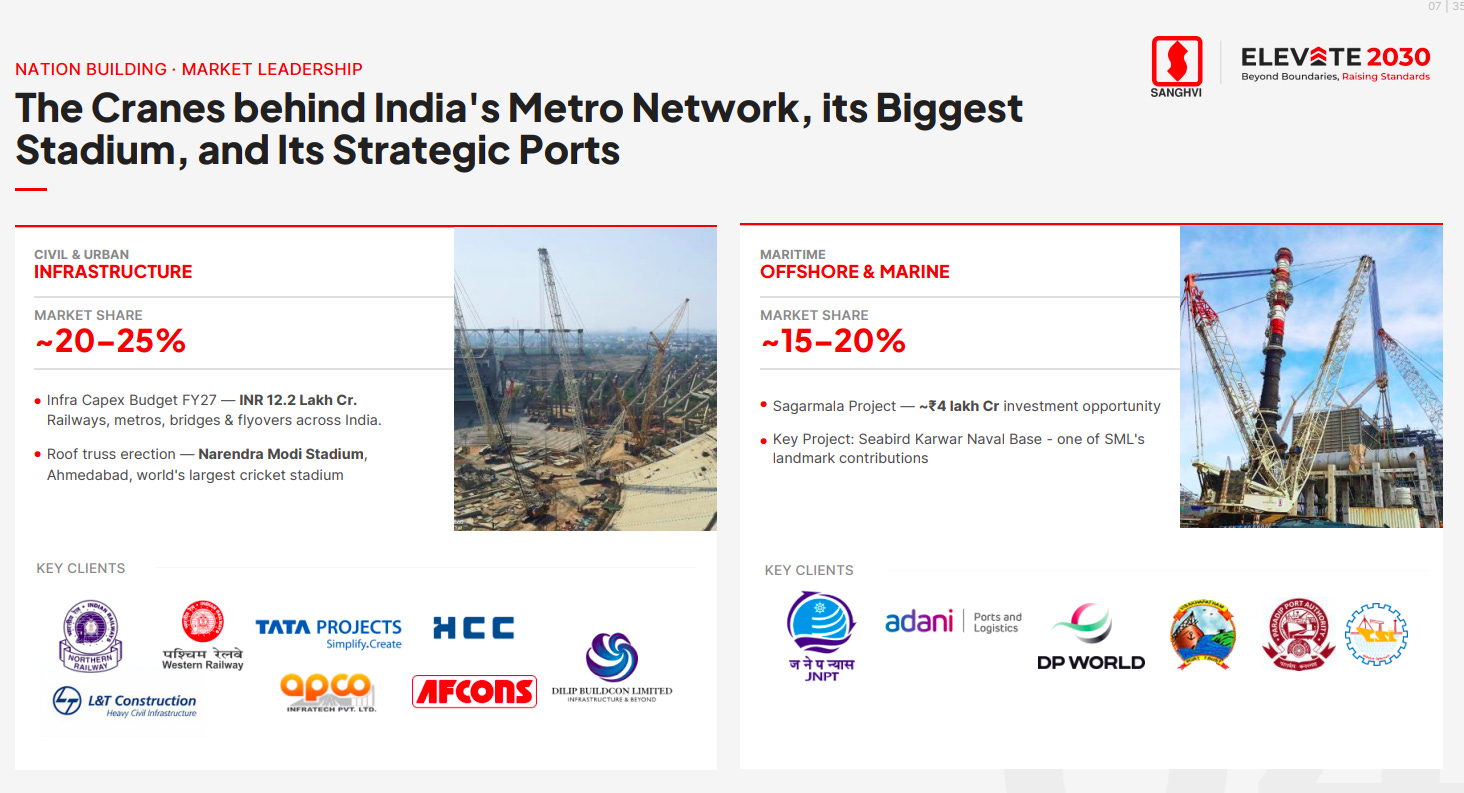

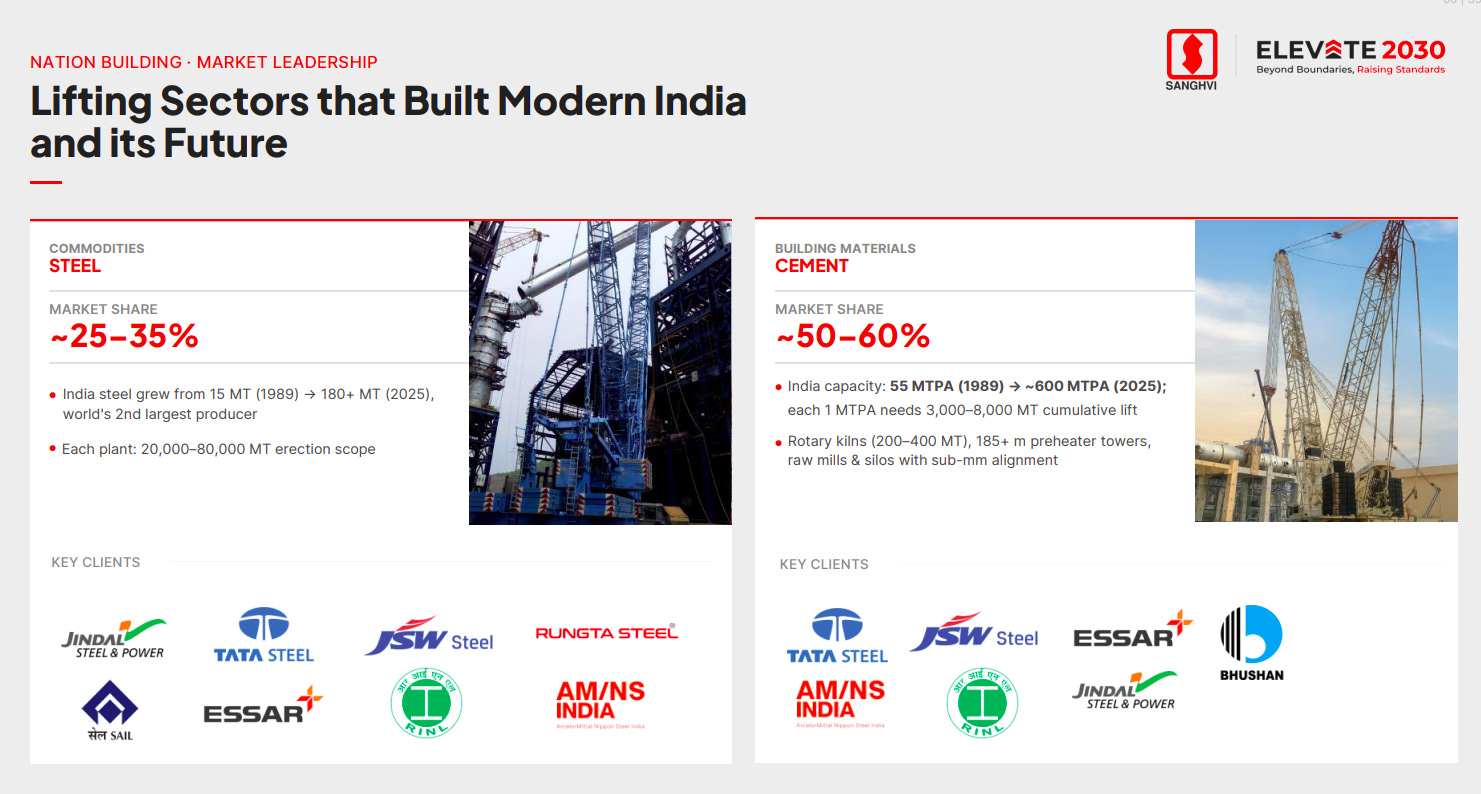

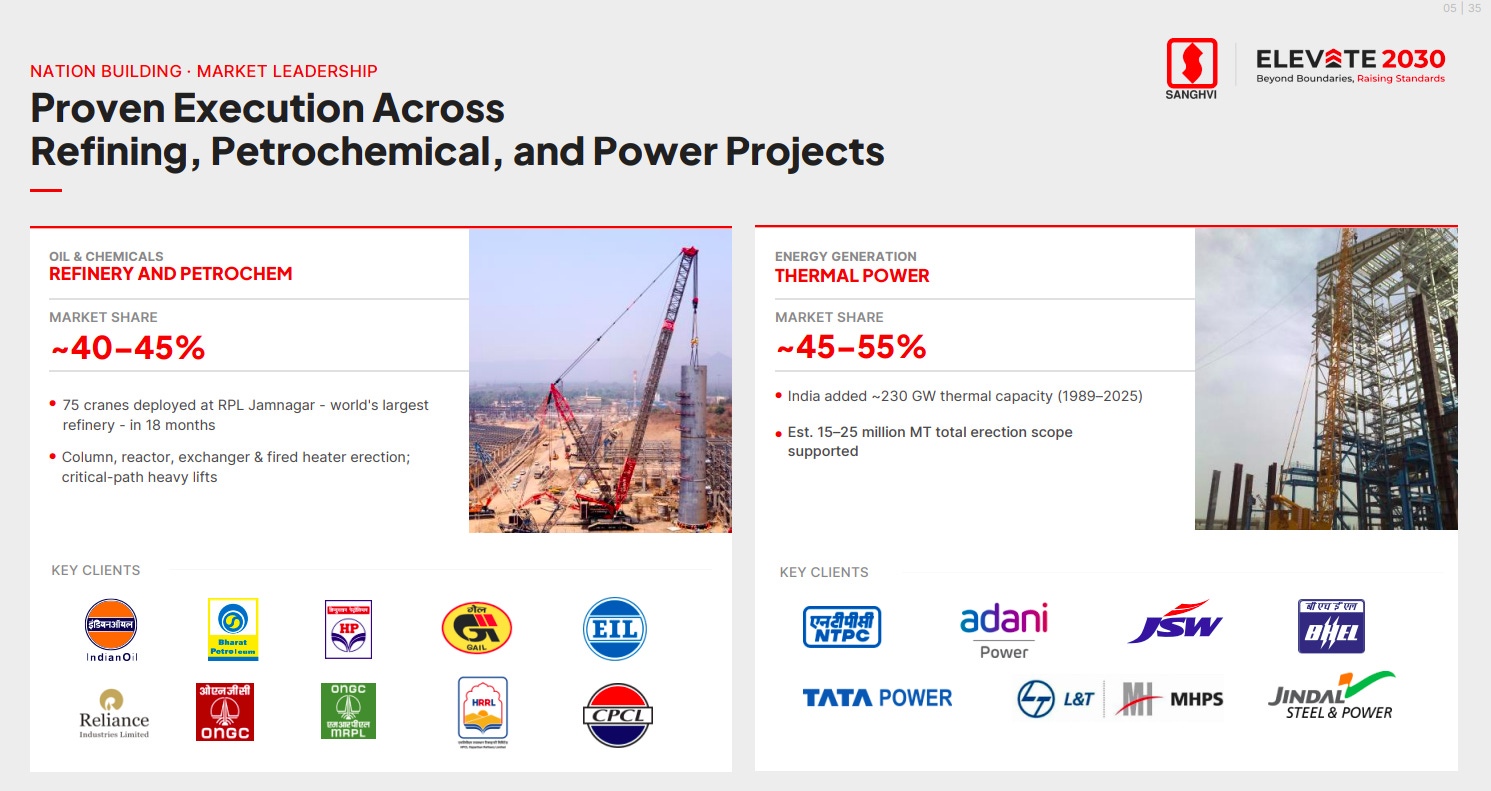

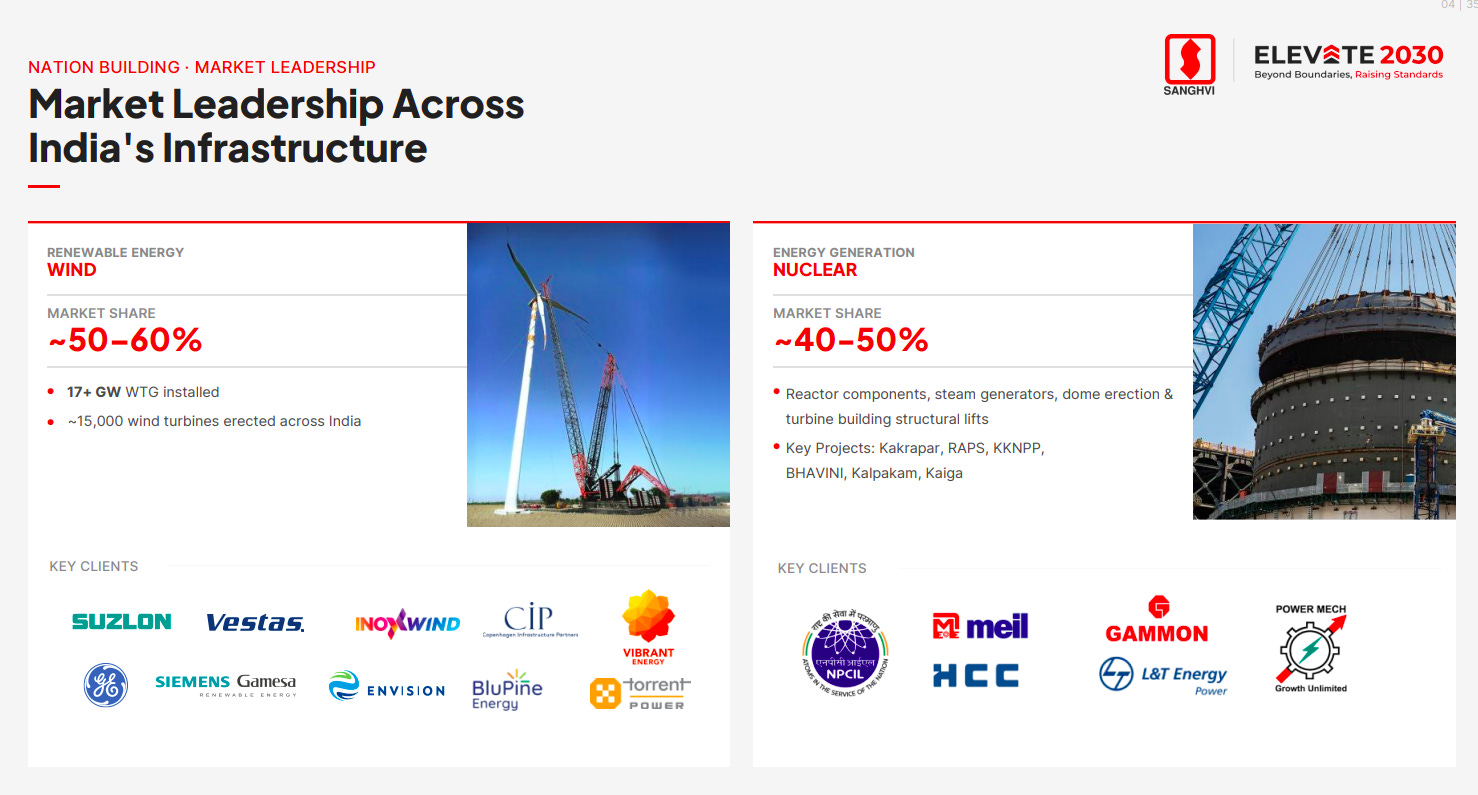

Sanghvi Movers | Small Cap | Engineering & Capital Goods

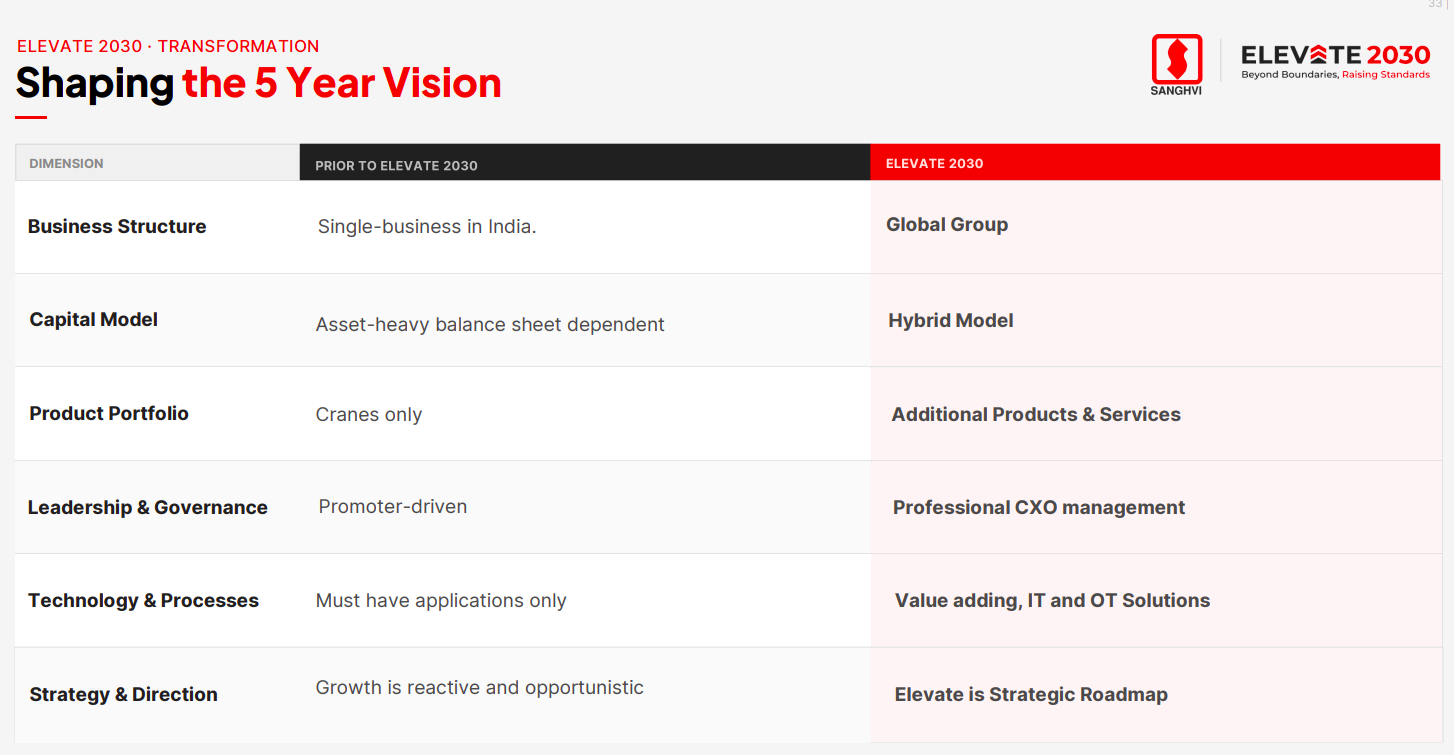

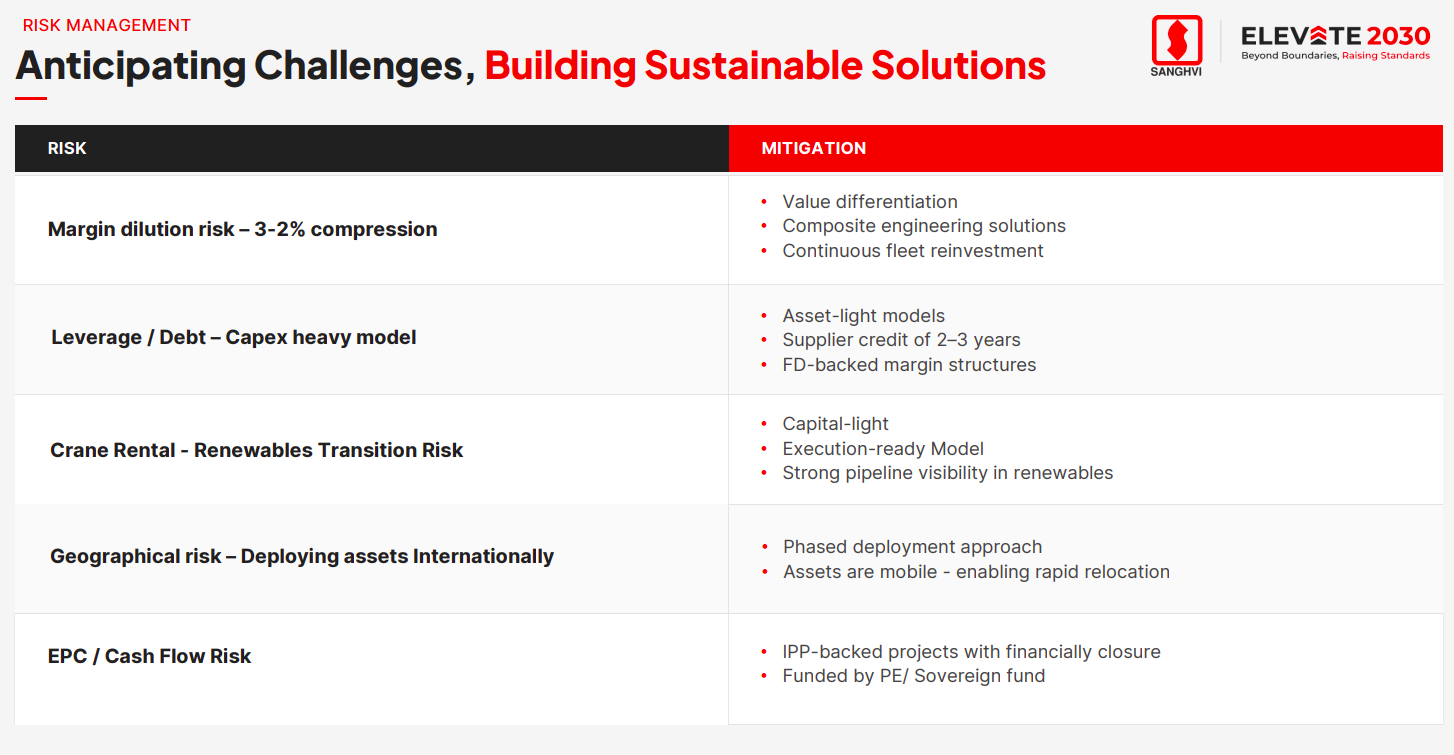

Sanghvi Movers Limited (SML) is the largest crane rental company in India. SML is a BS OHSAS 18001:2007 certified company. It is committed to being a top globally-ranked company in its core business with exceptional business ethics and morals.

The company is transitioning from a domestic, asset-heavy crane business to a global, hybrid platform. The shift toward value-added services, diversified offerings, and professional management signals a move from cyclical execution to scalable, structured growth.

Key risks remain around margin compression, leverage, and execution volatility, but the model is evolving toward asset-light structures, differentiated offerings, and better project visibility. Importantly, cash flow risk is mitigated through financially closed projects and institutional counterparties.

Strong positioning in high-value, critical lifts (~30–40% share) where execution complexity creates entry barriers. With India’s O&G capex cycle picking up, this segment offers high-ticket, margin-accretive opportunities.

Core infra (metros, bridges, ports) and marine projects provide steady, visibility-led demand (~20–25% share). Government capex and mega projects (Sagarmala, defence infra) create a long runway for crane deployment.

Well entrenched in large industrial capex cycles, with meaningful share across steel and cement projects. These sectors provide bulk, repeatable execution opportunities, though relatively more cyclical than infra.

Strong execution track record in complex, critical-path projects (40–55% share) including refineries and thermal power. These projects drive high utilisation and premium pricing due to technical complexity.

Leadership in wind (~50–60% share) and strong presence in nuclear reflects positioning in next-gen energy infrastructure. This is a key strategic pivot toward long-term, structurally growing segments.

Media & Entertainment

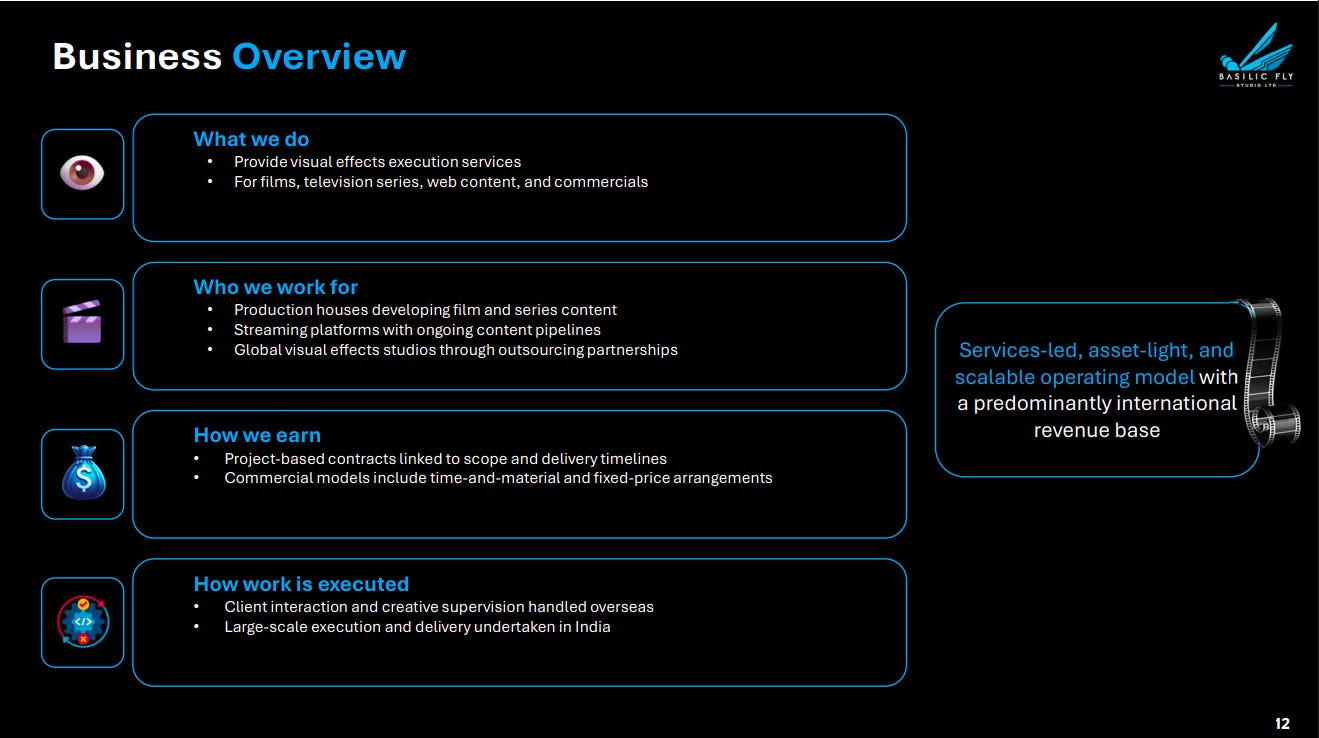

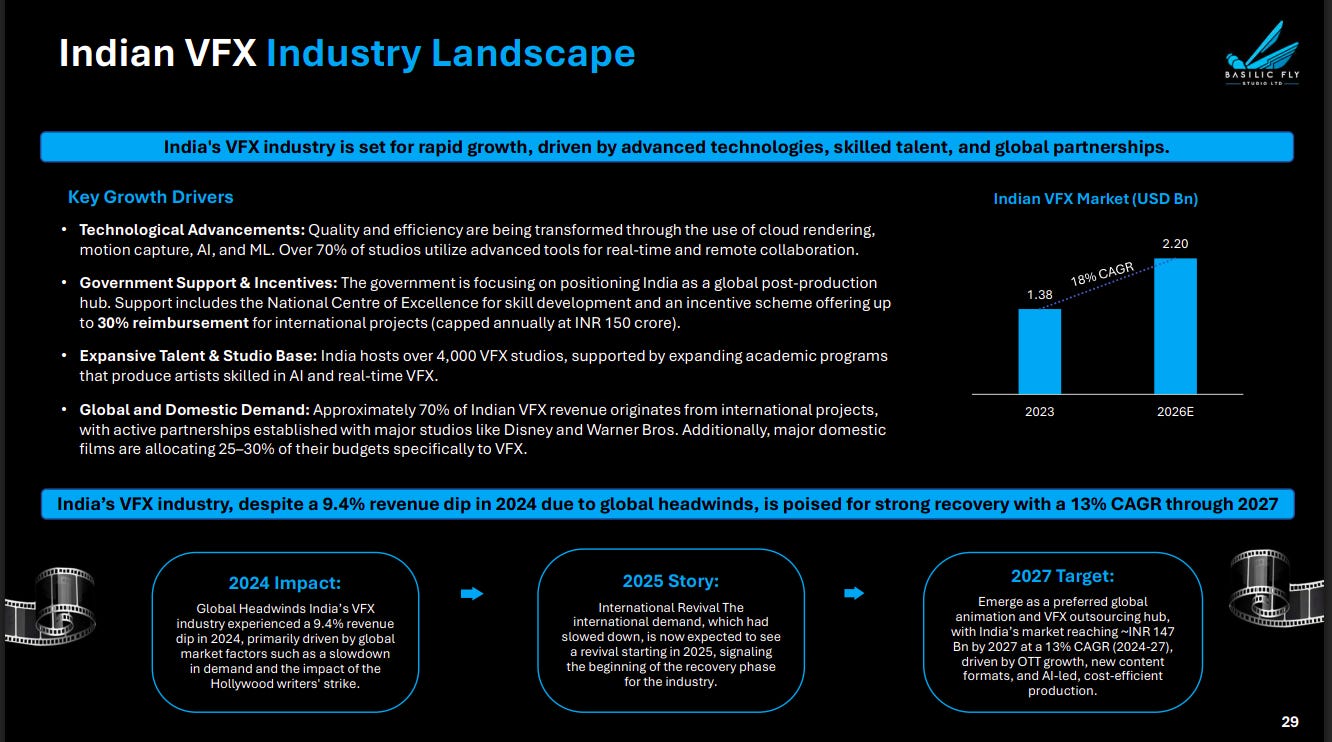

Basilic Fly Studio | Micro Cap | Media & Entertainment

Basilic Fly Studio Limited, a visual effects (VFX) studio based in Chennai, India, delivers high-quality VFX solutions for movies, TV, net series, and commercials. With subsidiaries in Canada and the UK, the company specializes in creating captivating visual experiences for global audiences, showcasing a decade of expertise in the industry since its establishment in 2012.

A services-led VFX company focused on execution for films, OTT, and commercials, with an asset-light and scalable model. Revenue is largely international, with creative work handled overseas and execution delivered from India.

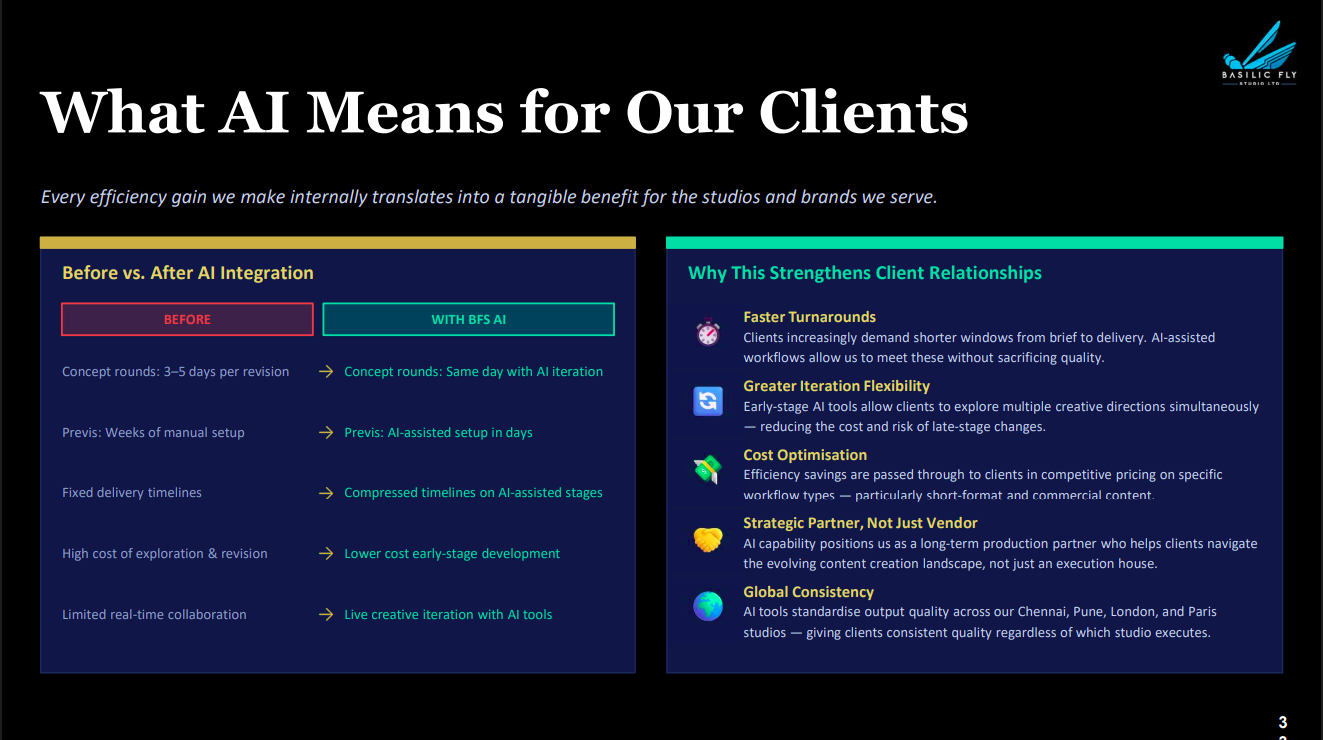

AI significantly compresses timelines, lowers costs, and enables faster creative iteration. This strengthens client relationships by improving efficiency, consistency, and positioning the company as a long-term strategic partner.

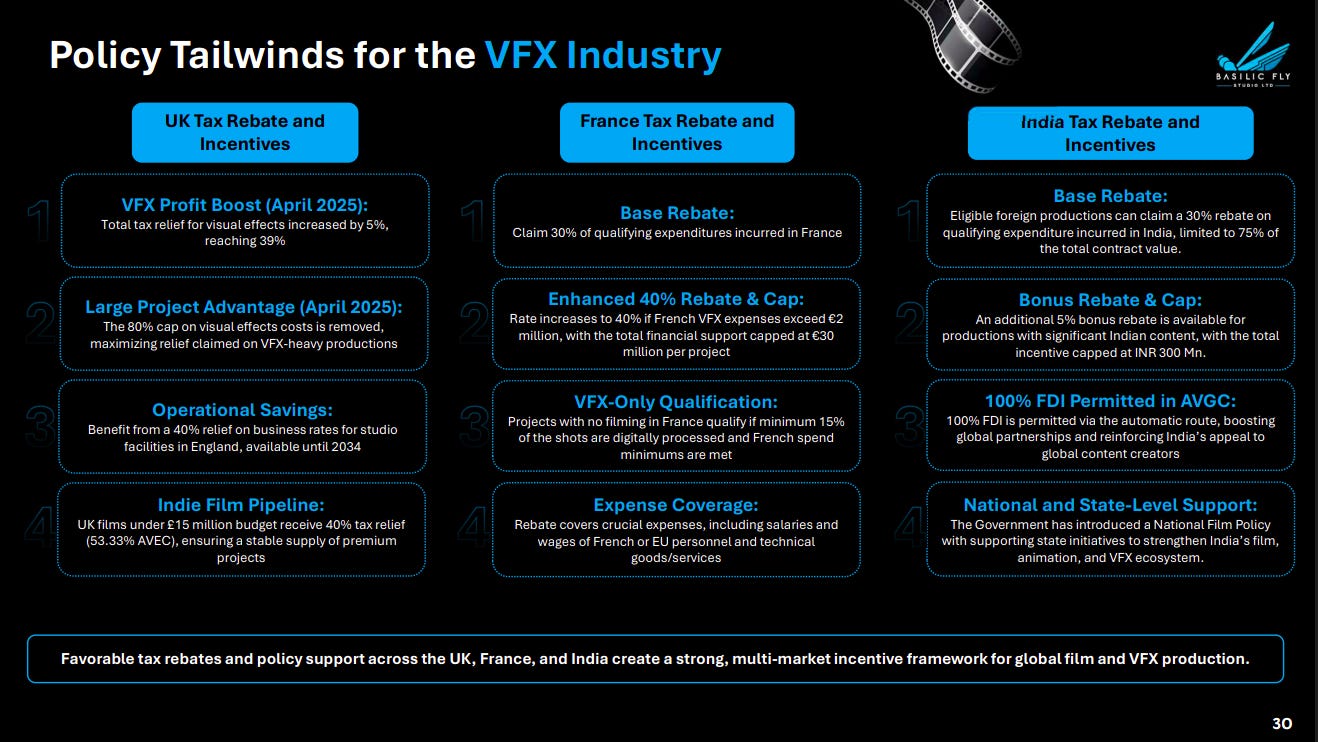

Strong tax incentives across the UK, France, and India are making global VFX production more attractive and cost-efficient. These policies are driving higher project inflows and strengthening multi-country production ecosystems.

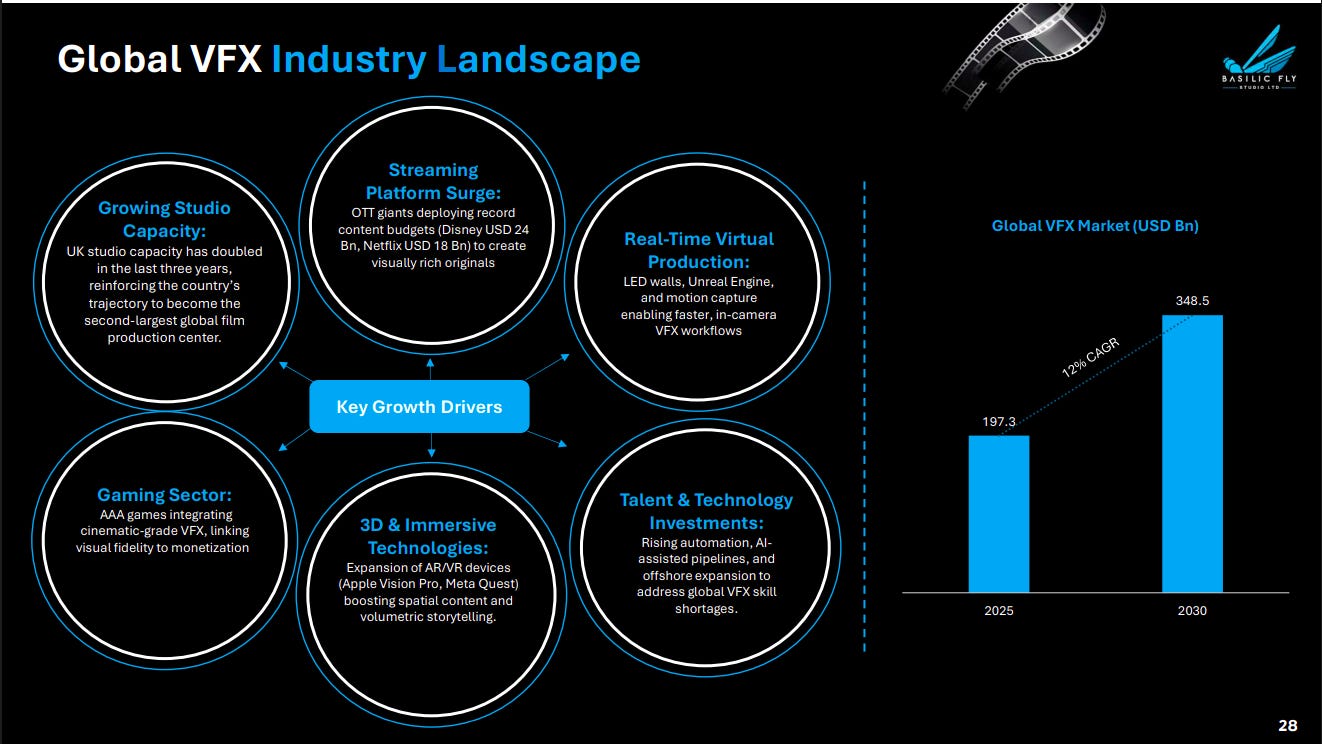

India’s VFX industry is poised for strong growth, supported by talent, cost advantage, and policy support, with ~13% CAGR expected through 2027. After a temporary dip in 2024, demand is recovering on the back of global content revival.

Global VFX demand is expanding rapidly, driven by OTT spending, gaming, real-time production, and immersive technologies. The market is expected to grow at ~12% CAGR, supported by rising content complexity and tech adoption.

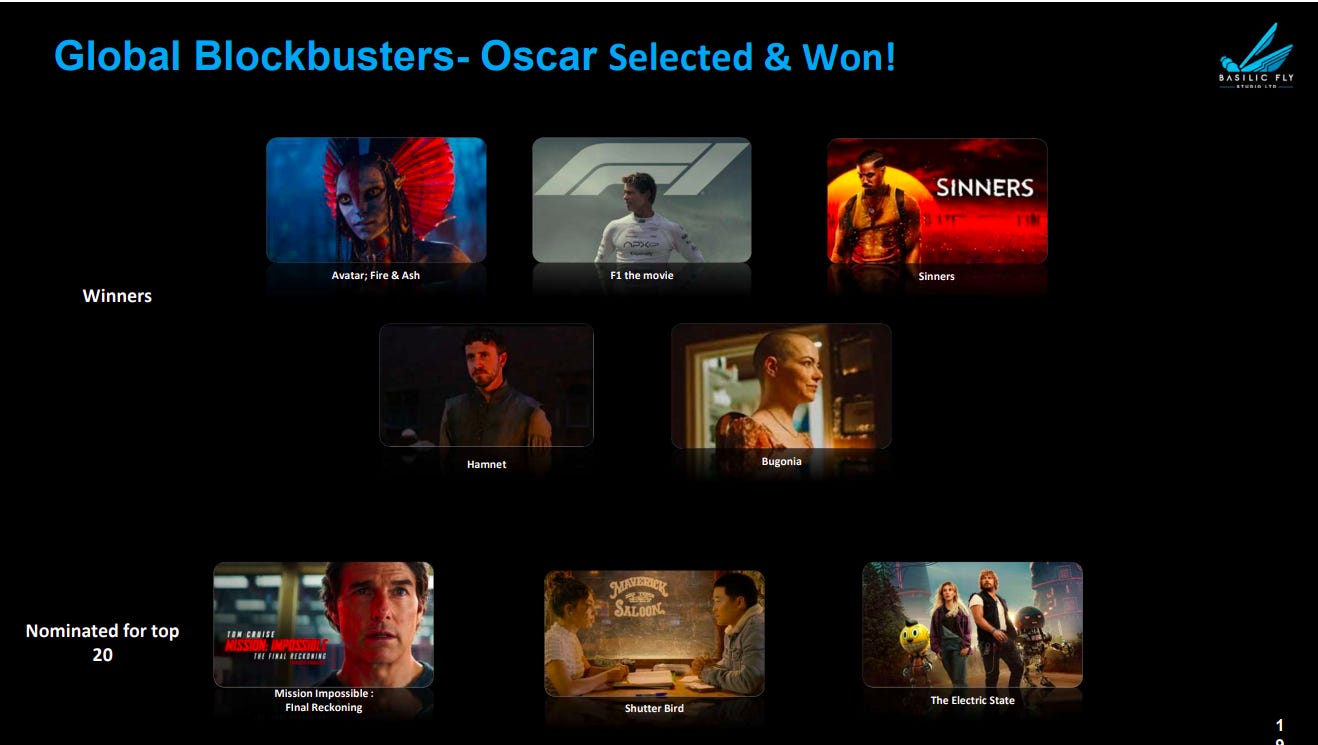

The company has contributed to globally recognized, award-winning projects and major productions. This establishes strong credibility and positions it as a trusted execution partner for high-end VFX work.

Auto Ancillary

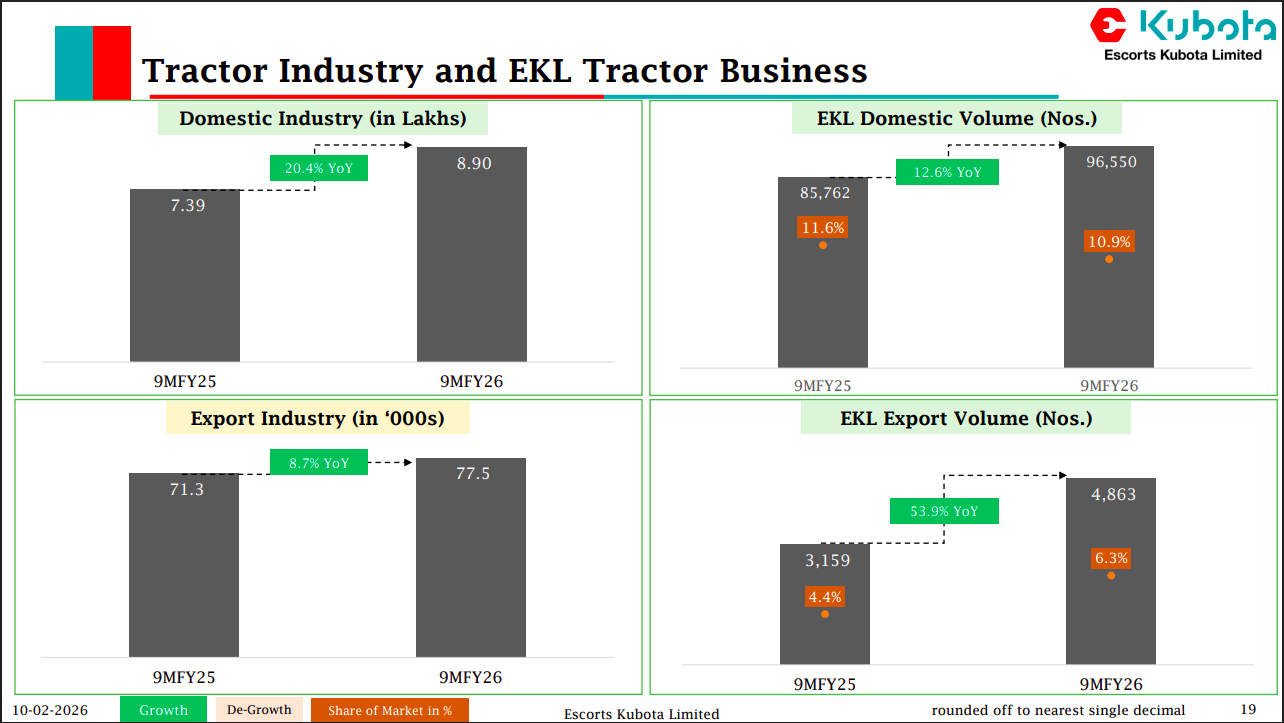

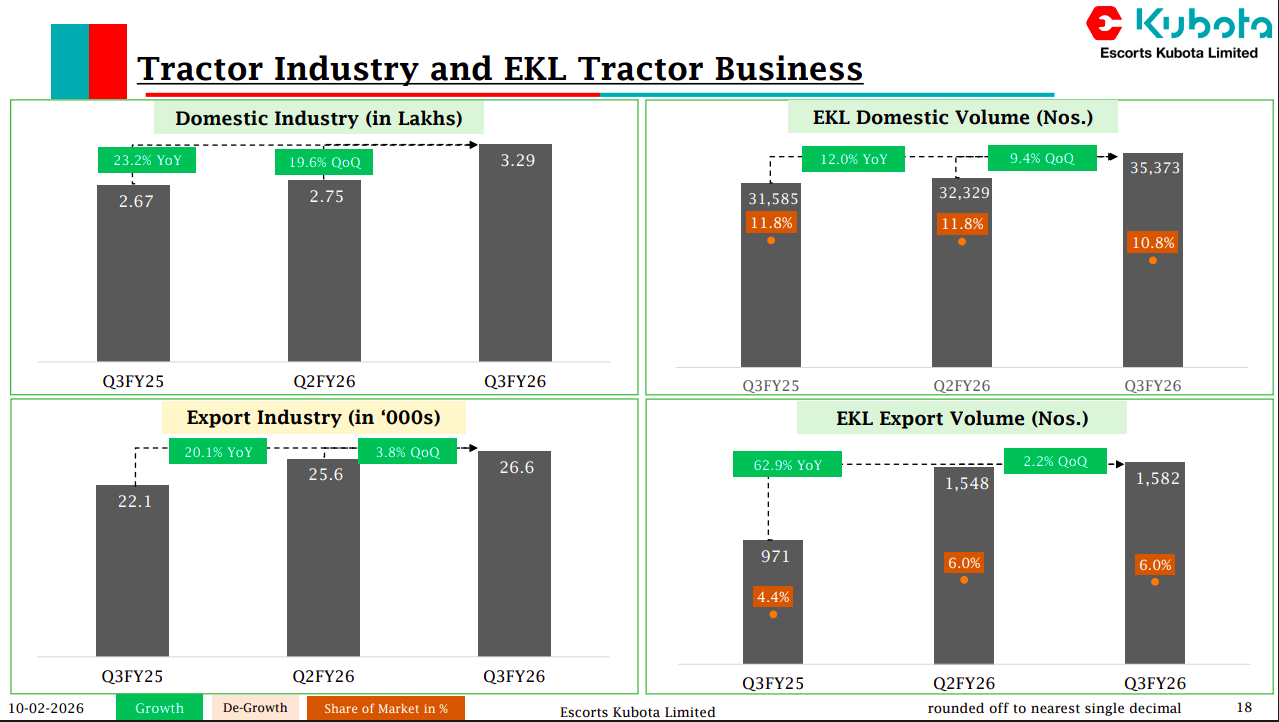

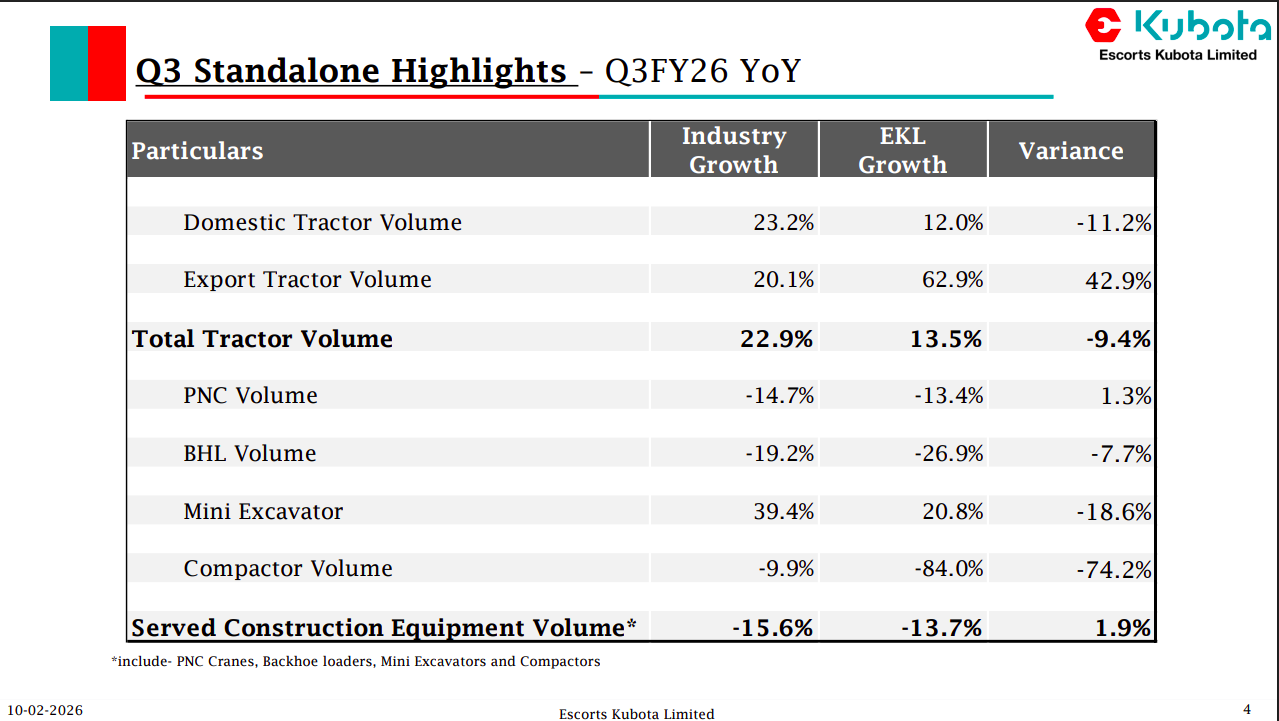

Escorts Kubota | Mid Cap | Auto Ancillary

Escorts Kubota Limited, formerly Escorts Limited, is a leading engineering company in India specializing in farming and construction equipment.Their diverse product range includes agricultural tractors, engines, earth moving equipment, railway components, automobile parts, and more.

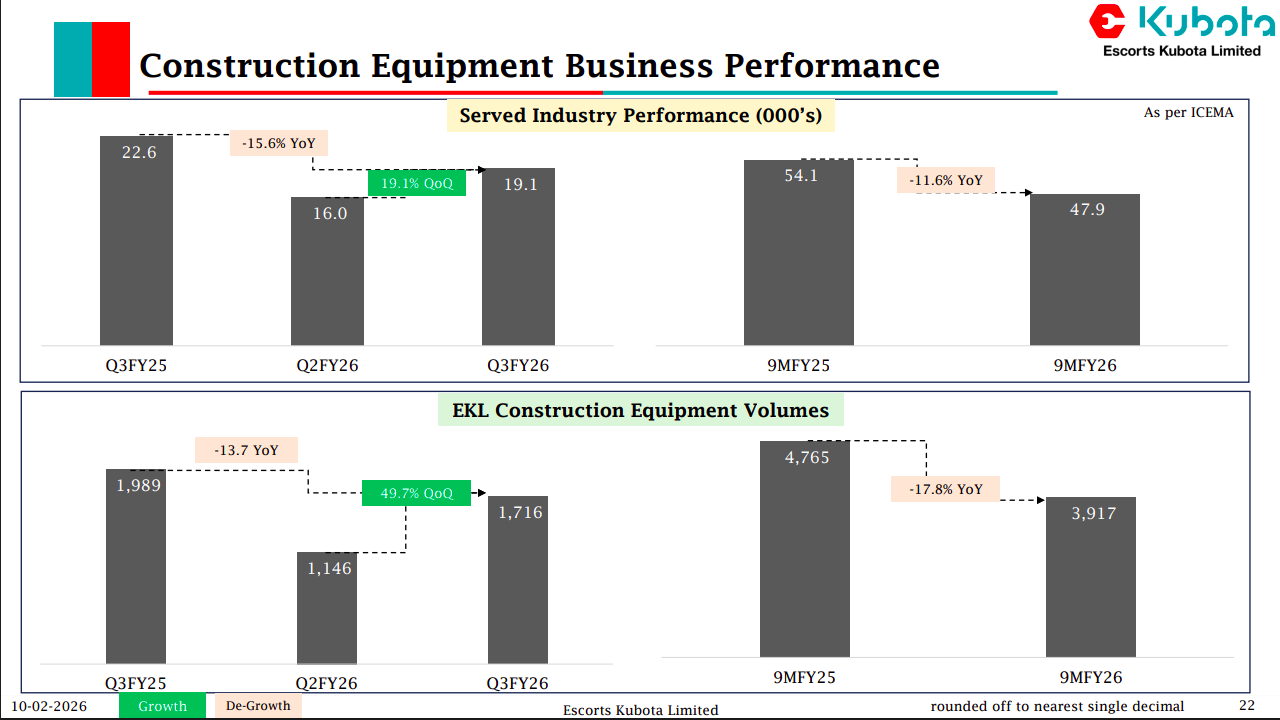

Industry demand remains weak YoY, though sequential recovery is visible in Q3. EKL volumes mirror this trend—sharp QoQ rebound but still lower on a YoY basis, indicating a gradual recovery phase.

Domestic tractor industry saw strong growth (~20%+), while EKL grew at a slower pace, leading to market share moderation. Exports, however, were a key positive with strong double-digit growth for EKL.

Industry growth remained robust both YoY and QoQ, supported by rural demand. EKL delivered steady growth but lagged industry in domestic volumes, while exports continued to outperform strongly.

EKL underperformed the industry in domestic tractors but significantly outperformed in exports. Construction equipment segments remained weak overall, though declines were broadly in line with industry trends.

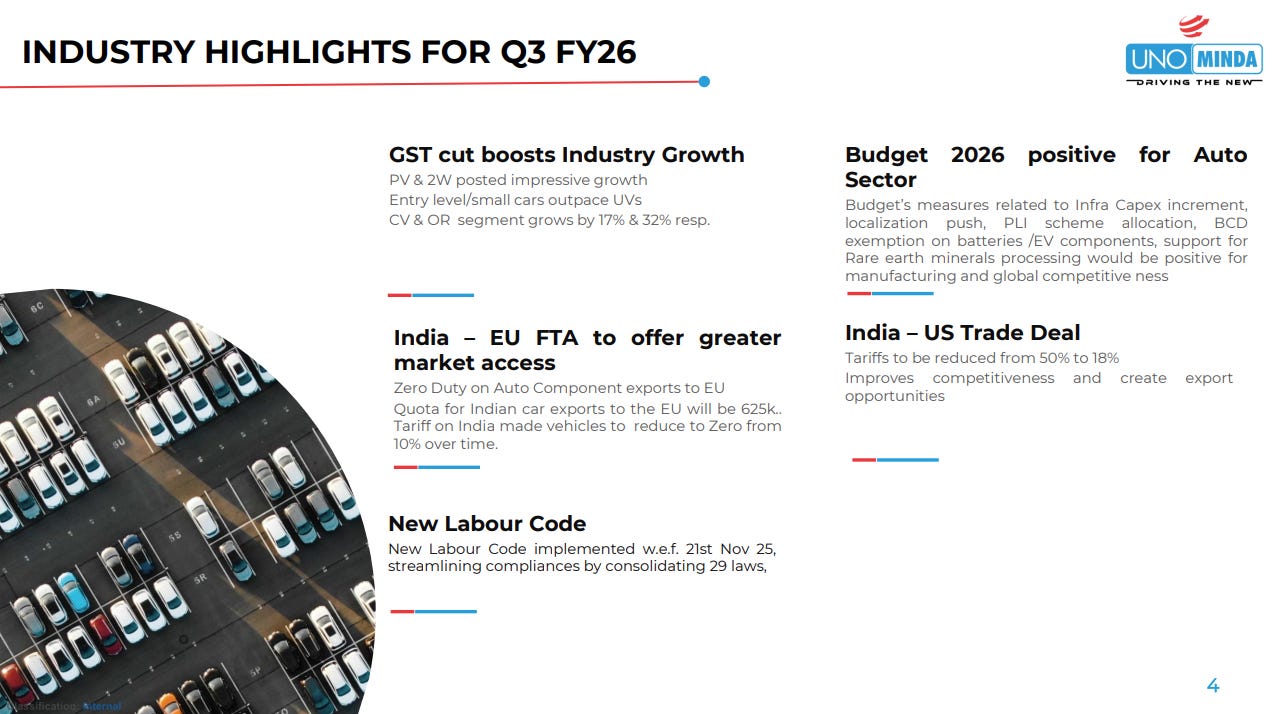

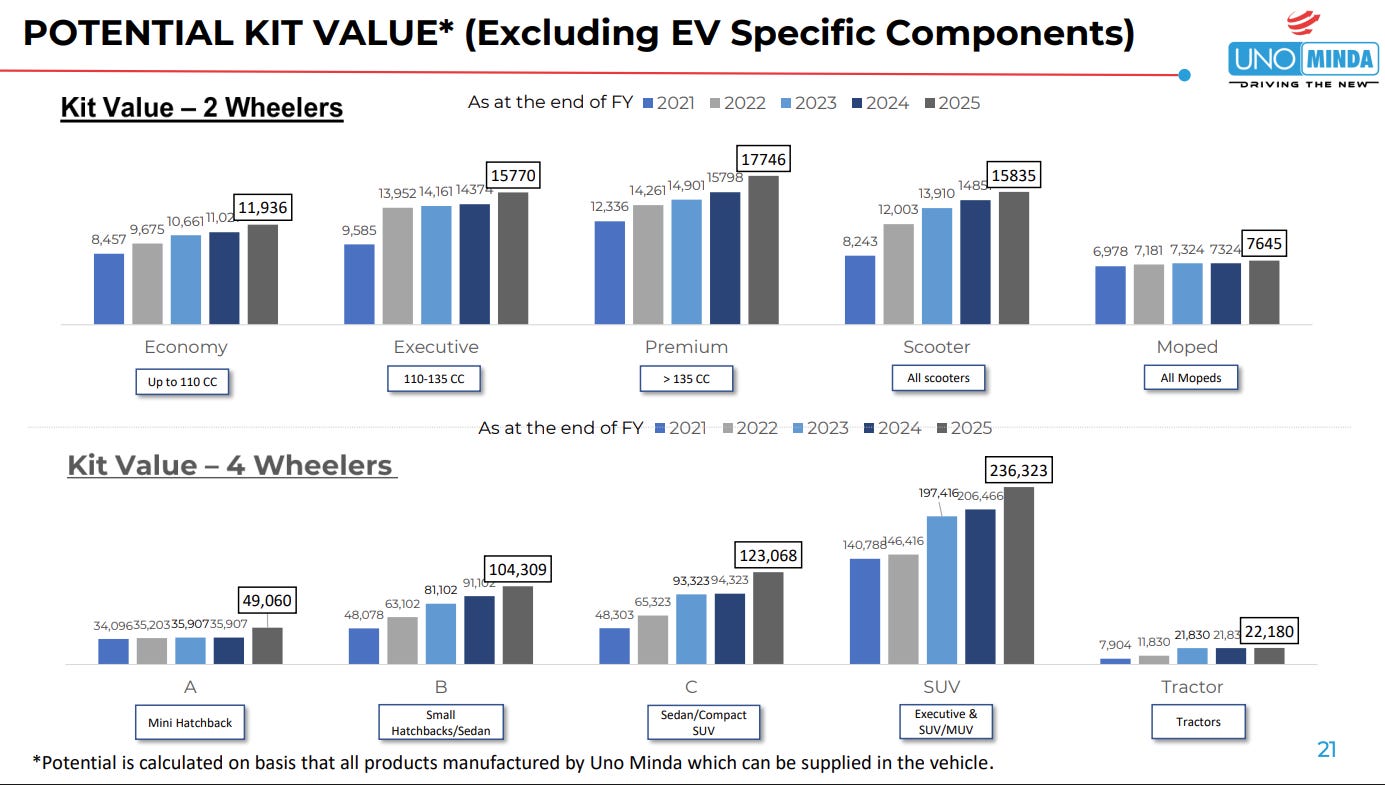

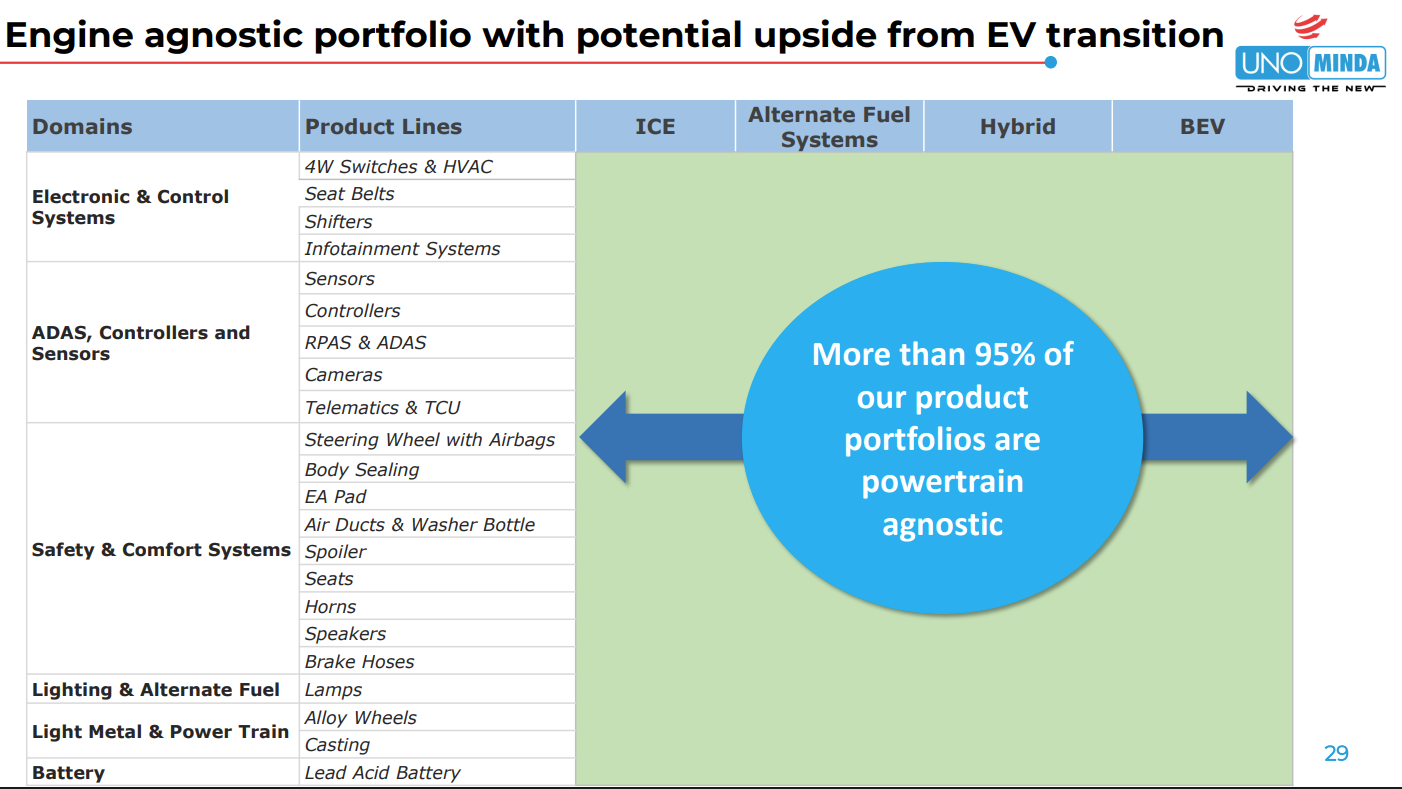

UNO Minda Ltd. | Mid Cap | Auto Ancillary

Uno Minda specializes in producing and trading auto components like lighting, alloy wheels, horns, seating systems, seatbelts, switches, sensors, controllers, handle bar assemblies, and wheel covers. It serves markets in two-wheelers, three-wheelers, and four-wheelers both domestically and internationally, offering a wide range of automotive solutions.

Multiple tailwinds are aligning for the auto sector—GST cuts and strong growth in PV/2W and CV segments are driving demand, while policy support through Budget 2026, PLI incentives, and localization pushes is strengthening the manufacturing ecosystem. At the same time, trade agreements with the EU and US are opening up export opportunities, even as regulatory changes like the new labour code aim to streamline operations, collectively creating a more supportive environment for sustained industry growth.

Uno Minda’s content per vehicle continues to rise across segments, with kit values steadily increasing in both 2Ws and 4Ws, especially in premium motorcycles and SUVs. This reflects a clear shift towards premiumization and higher feature intensity, allowing the company to capture more value per vehicle even without relying on EV-specific components.

Uno Minda’s portfolio is largely powertrain-agnostic (>95%), meaning most of its products remain relevant across ICE, hybrid, and EV platforms—reducing disruption risk from the EV transition. This positions the company to ride the shift to electrification without needing a complete portfolio overhaul, while still benefiting from incremental EV-specific opportunities.

Healthcare

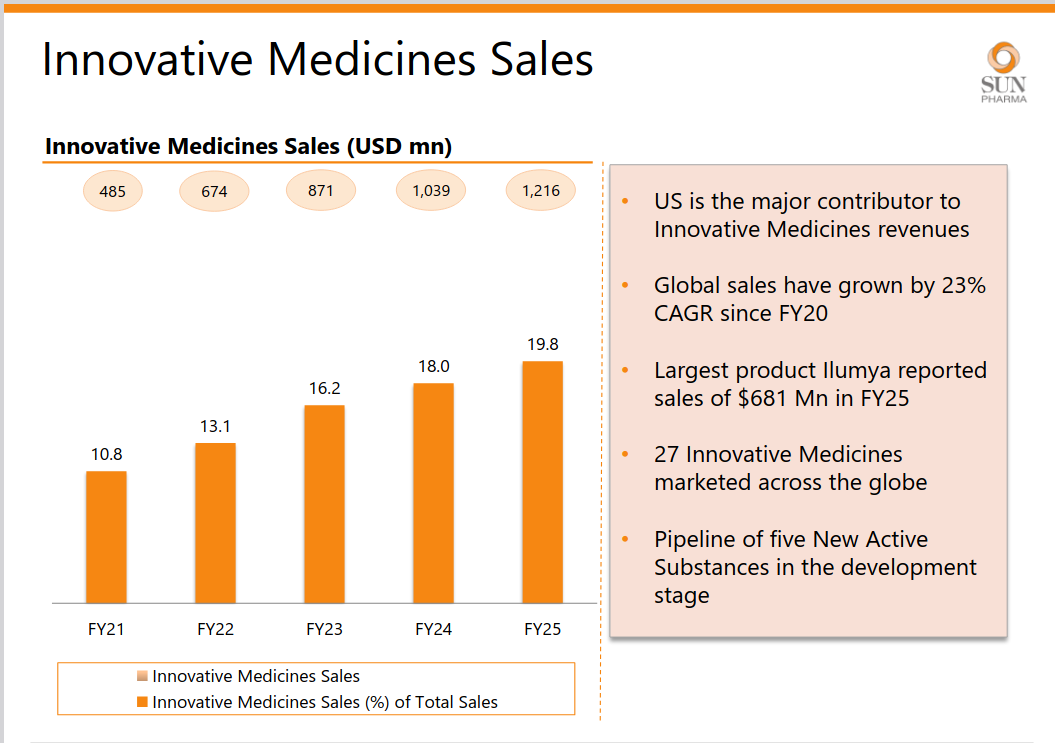

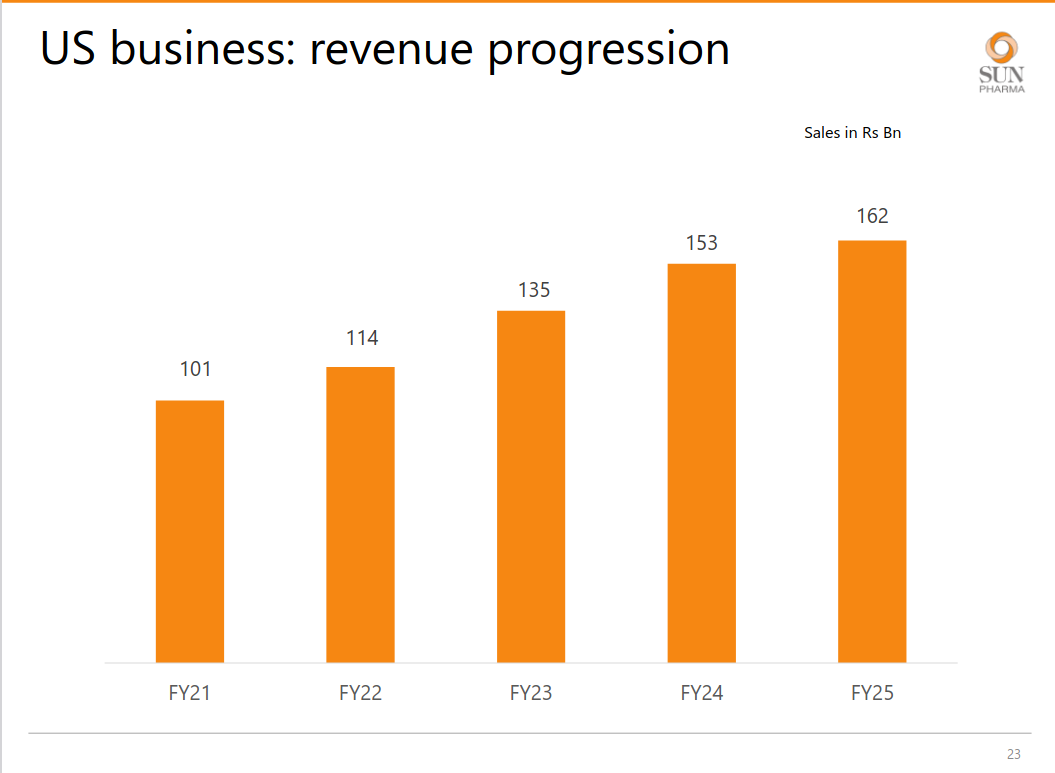

Sun Pharmaceutical Industries | Large Cap | Healthcare

Sun Pharmaceutical Industries Limited is a leading specialty generic pharmaceutical company in India, known for delivering high-quality products at affordable prices. With a diverse portfolio covering a wide range of therapies, the company manufactures and markets various formulations, including generics, branded generics, specialty products, OTC medications, ARVs, APIs, and intermediates

Innovative medicines are a key growth driver, with strong double-digit growth (~23% CAGR since FY20) and rising contribution to overall sales. The US remains the primary market, with Ilumya leading the portfolio and a healthy pipeline supporting future growth.

US revenues have grown steadily from ₹101 bn to ₹162 bn over FY21–FY25, reflecting strong execution in specialty and innovative products. This remains the company’s most important and consistent growth engine.

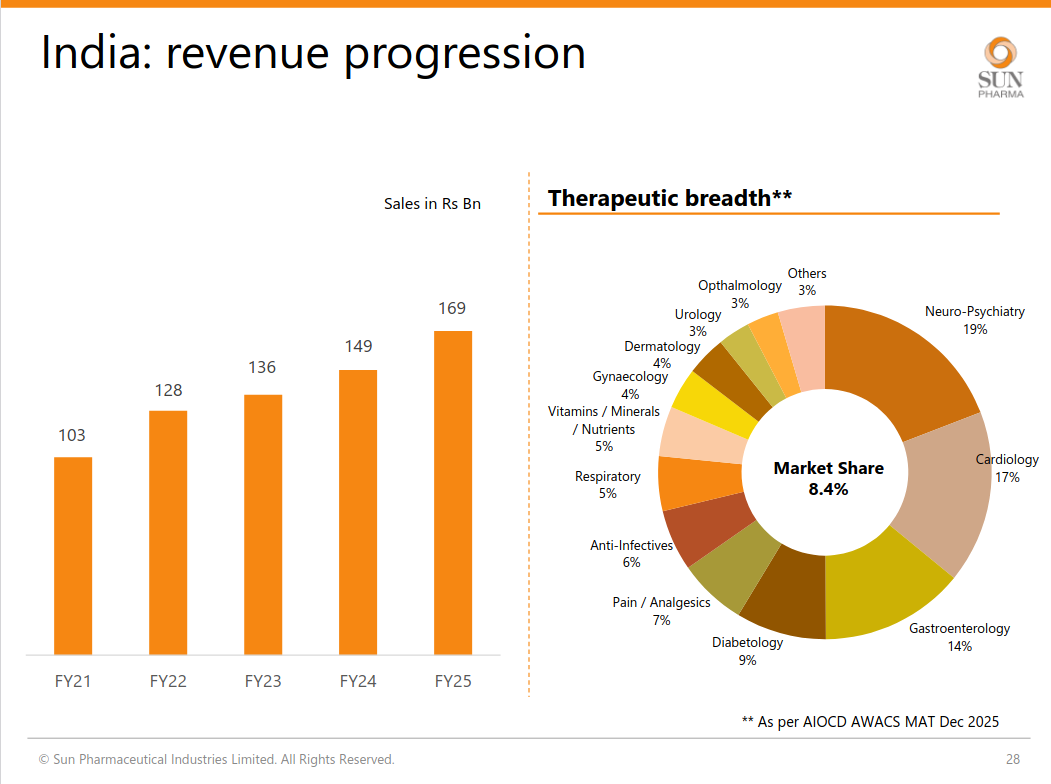

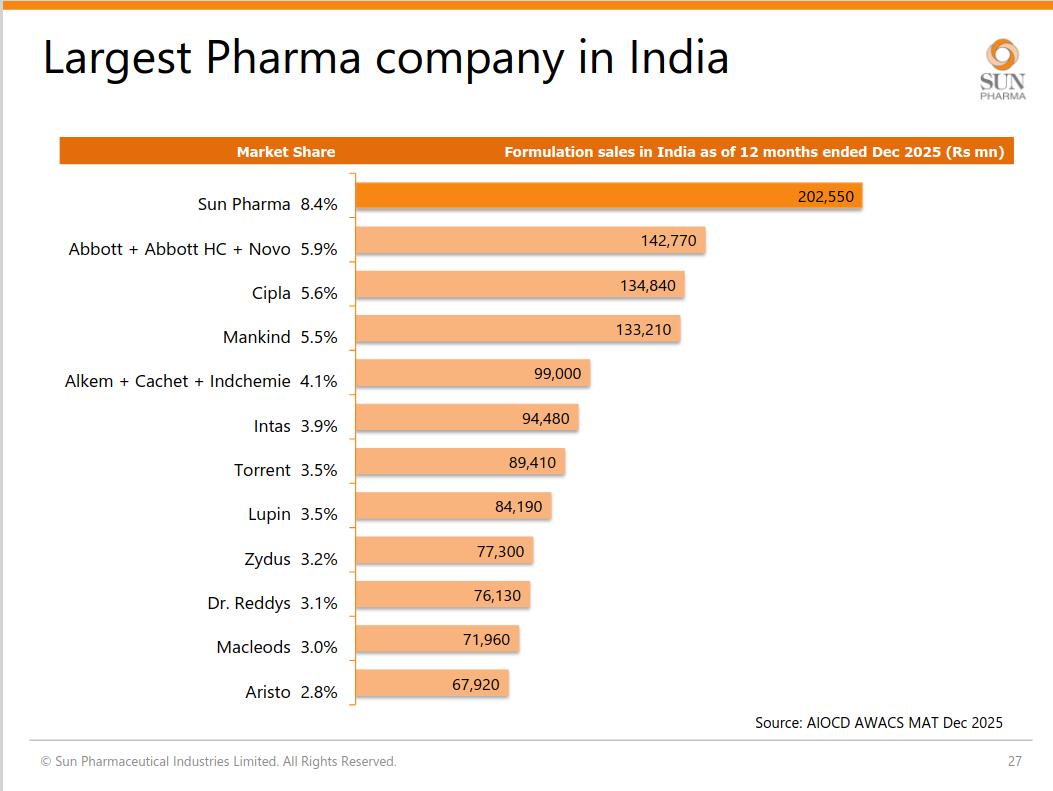

India revenues have shown consistent growth, supported by a diversified therapy mix and strong presence across chronic segments. Sun Pharma maintains leadership with ~8.4% market share, underpinned by broad therapeutic coverage.

Sun Pharma leads the Indian pharma market with a clear gap over peers, driven by scale, strong domestic formulations business, and wide portfolio reach. Its leadership position reinforces pricing power and distribution strength.

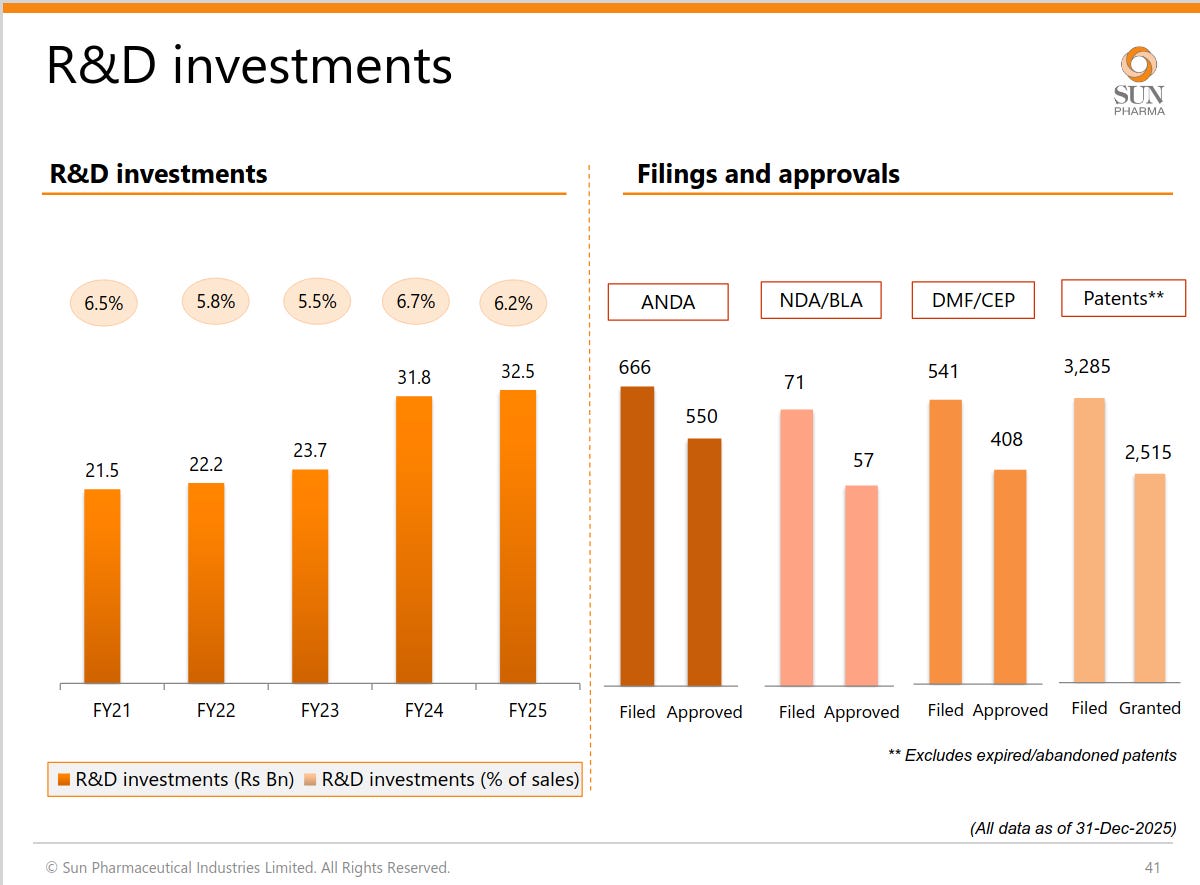

R&D spend has steadily increased to over ₹32 bn, maintaining ~6% of sales, indicating continued focus on innovation. A strong pipeline of filings, approvals, and patents supports long-term product launches and growth visibility.

Cement

JK Cement Ltd. | Mid Cap | Building Materials

JK Cement focuses on producing eco-friendly cement and allied products, aiming to reduce environmental impact while maintaining affordability and customer satisfaction. Their portfolio reflects a commitment to sustainability, responsible sourcing, and a greener future in the cement industry.

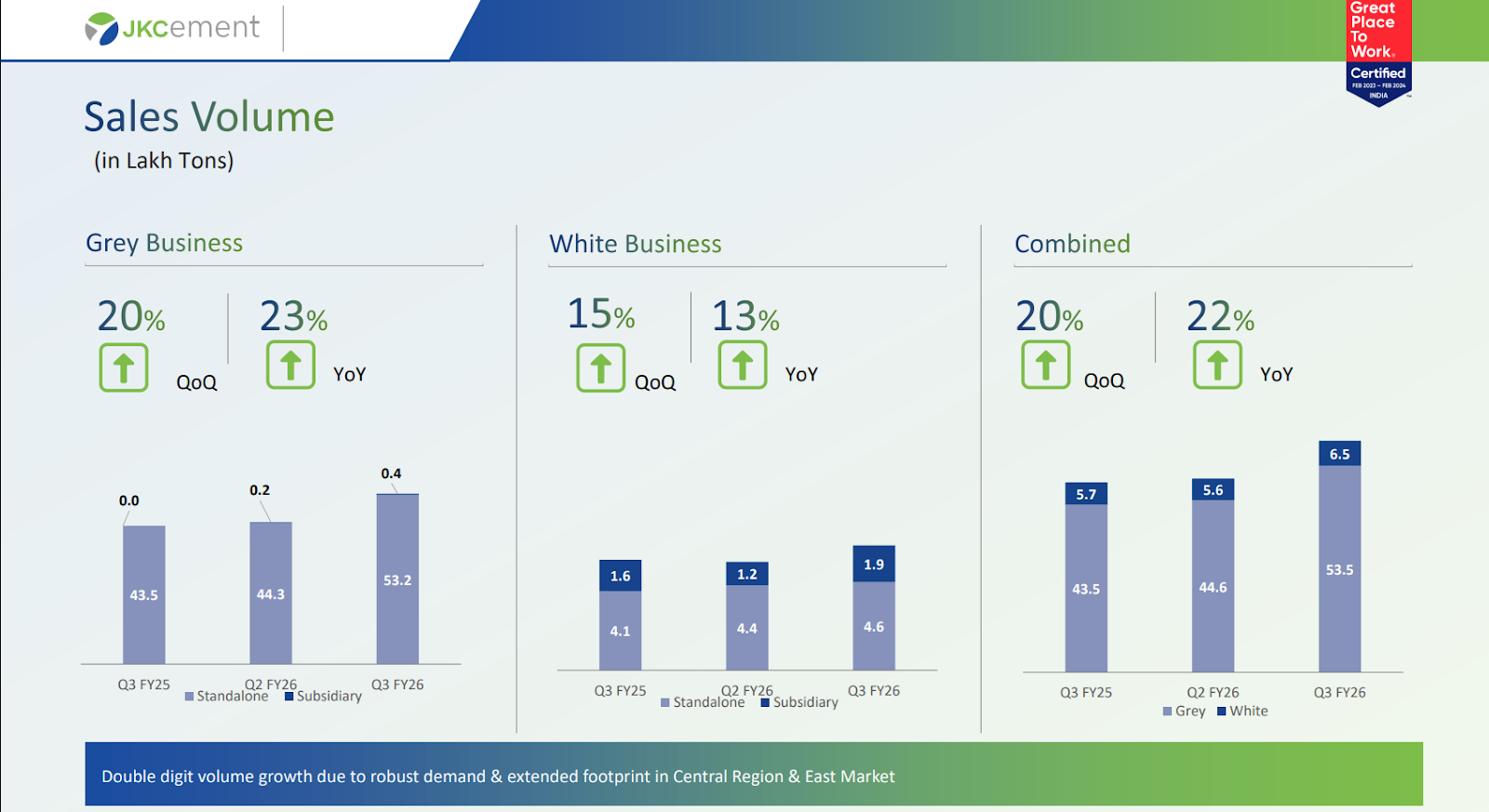

JK Cement is seeing broad-based volume growth across both grey and white cement segments, with grey cement continuing to drive the bulk of volumes and growth (strong double-digit YoY), while the white cement business, though smaller, is also scaling steadily. This highlights a balanced portfolio where grey provides scale and demand-led growth, and white adds niche, higher-value expansion.

Pet coke prices—one of the key cost drivers for cement—have largely stabilised after earlier volatility, trending in a narrow range in recent months. This suggests cost pressures are easing, which should support margin recovery if pricing holds.

Steel

JSW Steel | Large Cap | Iron & Steel

JSW Steel is a leading Indian integrated steel manufacturer with a global presence and a wide range of value-added products. The company focuses on efficient production through large-scale plants and is aggressively pivoting toward green steel and renewable energy.

The 2.5GW renewable energy investment signals a move to insulate steel production costs from volatile coal and grid pricing. This energy independence protects margins from inflation and supports high-value green steel exports.

Targeting 51.5 mtpa capacity by FY31 aims for domestic market dominance through aggressive scale. Integration with group infrastructure and energy assets creates a captive ecosystem that supports margin protection and cross-segment growth.

India crossing the 100kg per capita consumption threshold marks a structural pivot toward accelerated long-term domestic steel demand. This transition provides a durable volume growth runway that is less dependent on volatile global export markets.

Expanding into high-value electrical steel decouples revenue from volatile commodity cycles while tapping into the energy transition. This shift into specialty products builds a technical moat that supports superior profitability through various economic cycles.

The 50:50 joint venture for BPSL enables a ₹37,000 crore deleveraging while facilitating a capacity expansion to 10mtpa. This partnership leverages JFE’s capital and technology to drive growth without overextending the parent balance sheet.

Securing 1.6 billion tonnes of iron ore and coking coal assets in Australia and Mozambique insulates JSW from global raw material shocks. Vertical integration is the essential defense for protecting unit economics as production capacity doubles.

Scaling the influencer network to 111,000 partners allows for greater demand control at the fabricator and contractor level. This retail-centric approach improves pricing power and provides volume stability against cyclical institutional demand.

China’s sustained export surge continues to act as a structural ceiling on regional steel prices regardless of local demand. This forces a strategic reliance on volume growth and cost leadership to protect margins against volatile global spreads.

Retail

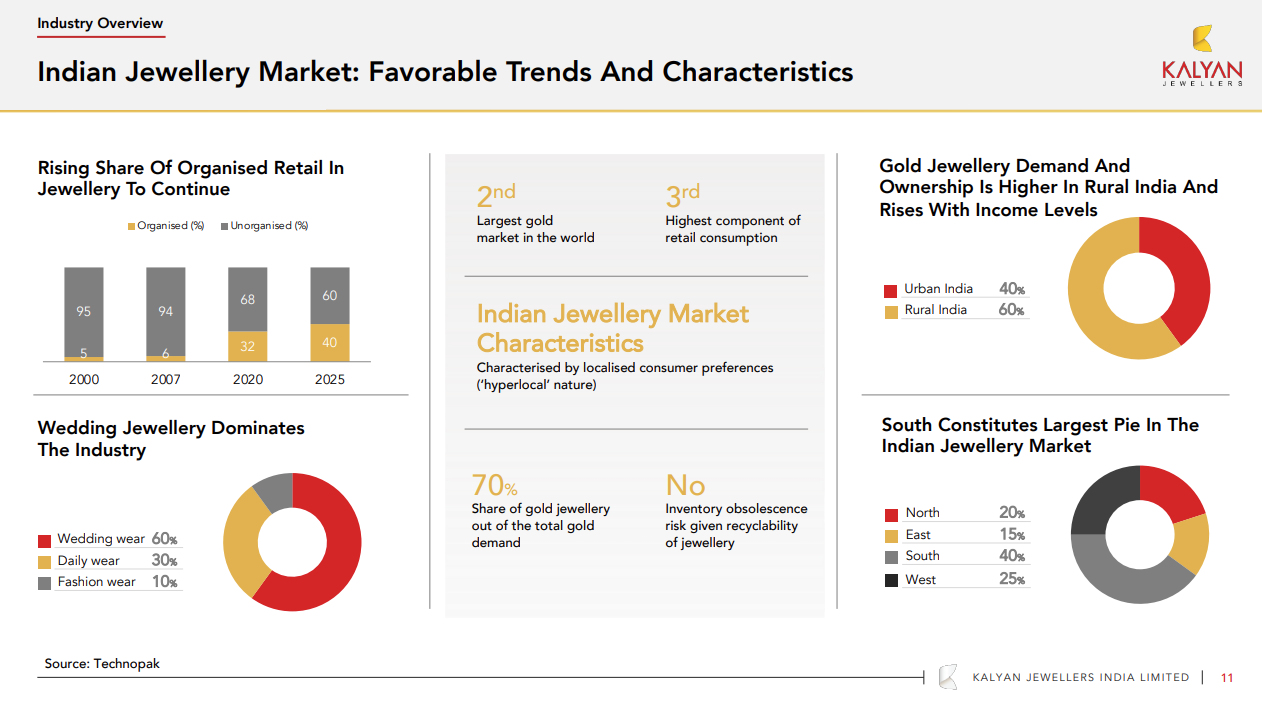

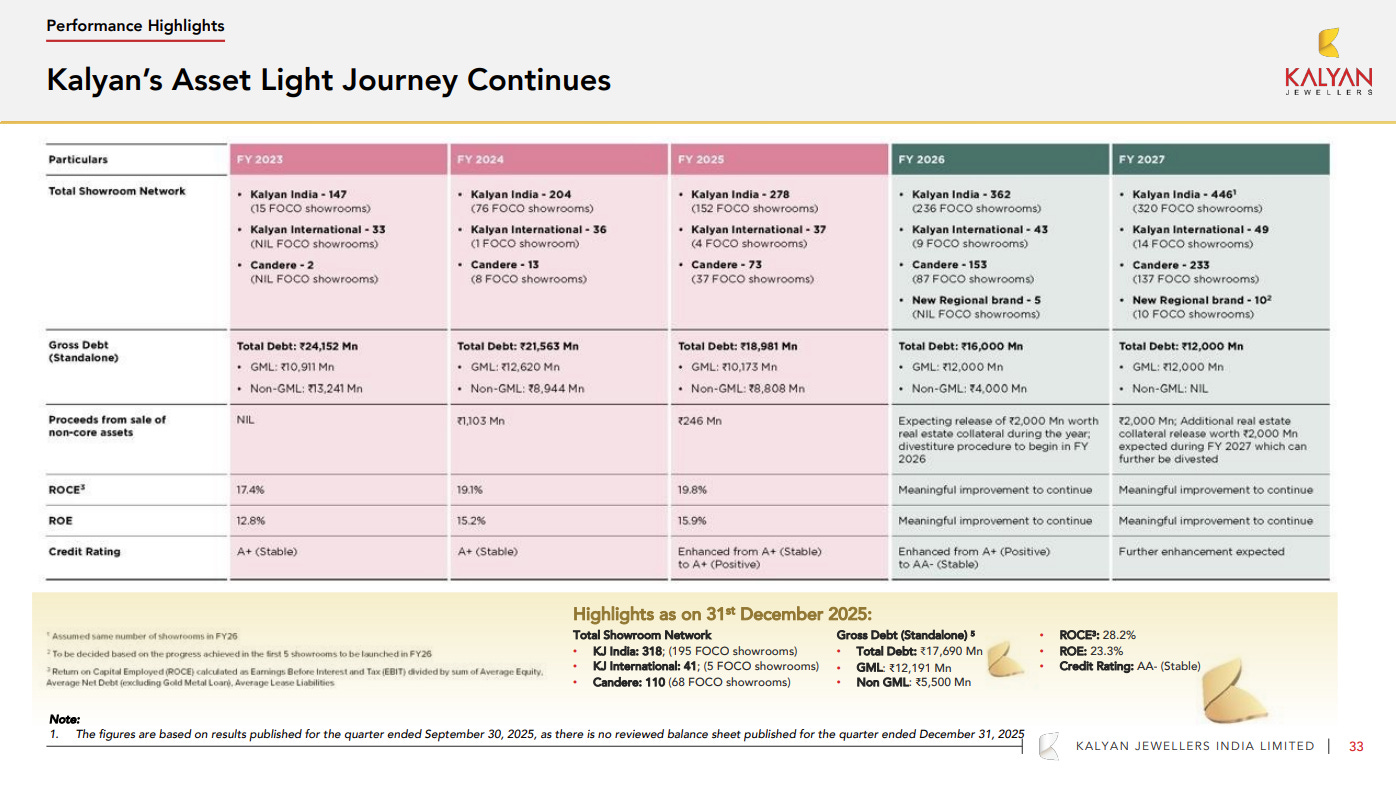

Kalyan Jewellers | Mid Cap | Retail

Kalyan Jewellers India Limited, one of the largest jewellery companies in India, started in 1993 and has since expanded across the country. They offer a wide range of jewellery products catering to special occasions like weddings, their highest-selling category, as well as daily wear. The company focuses on understanding customers’ preferences by utilizing local market expertise and region-specific marketing strategies.

India’s jewellery market is still largely driven by wedding-led demand (~60%), with gold remaining deeply tied to cultural consumption, especially outside urban centres. What stands out is the disproportionate weight of rural India (~60% of demand) and the south commanding the largest regional share (~40%), highlighting how growth is anchored in non-metro, tradition-led markets rather than discretionary urban spending.

Kalyan is building a multi-brand, multi-product portfolio to cater to distinct customer segments—from wedding-focused collections (Muhurat) to aspirational (Mudhra, Rang), regional staples (Aishwaryam), and studded jewellery (Nimah, Tejasvi, Ziah, Hera). This segmentation allows it to target diverse price points and occasions, widening its addressable market while strengthening relevance across both premium and value-conscious customers.

Kalyan’s expansion is increasingly being driven by an asset-light FOCO model, allowing it to scale its showroom network rapidly (especially via Candere and new formats) while bringing down debt and improving return ratios. The shift is visible in rising ROCE/ROE and declining standalone debt, indicating that growth is becoming more capital-efficient rather than balance-sheet heavy.

Vishal Mega Mart Limited | Mid Cap | Retailing

Vishal Mega Mart is a value-focused hypermarket chain specializing in fashion, general merchandise, and FMCG products across India. The company leverages a high mix of private labels and a vast store network to target value-conscious consumers in Tier I, II, and III cities.

Expanding hyperlocal delivery to 723 stores and a 55% surge in digital users signals a rapid omnichannel pivot. Using physical stores as fulfillment hubs counters quick-commerce threats while maintaining superior unit economics.

Aviation

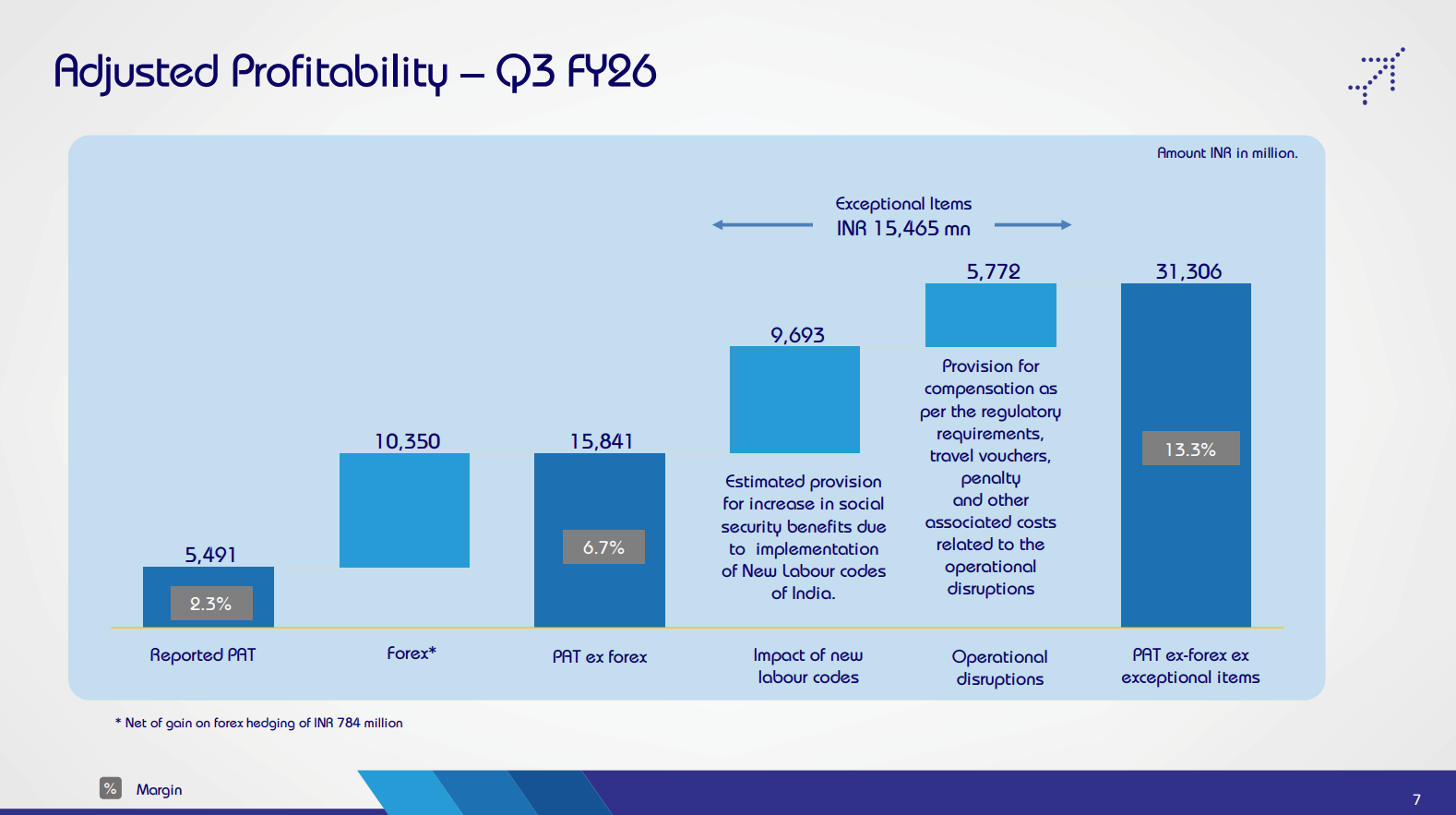

Interglobe Aviation Ltd. (Indigo) | Large Cap | Aviation

InterGlobe Aviation is a company operating in the aviation industry in India, specializing in low-cost carrier (LCC) services. Their primary activities include air transportation for passengers and cargo, along with providing associated services such as in-flight sales, aircraft maintenance engineering, and advanced pilot training.

A big chunk of IndiGo’s weak headline profitability this quarter comes from exceptional items (~₹15.5 bn)—largely one-off provisions and disruption-related costs. Strip these out, and profits jump sharply, showing that the core business is far stronger than reported numbers suggest.

That’s it for now! Your feedback will really help shape how Points and Figures evolves. Drop it down in the comments below!

Quotes in this newsletter were curated by Meher, Kashish & Vignesh.

Disclaimer: We’ve used AI tools in filtering and cleaning up the quotes from the images so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Points and Figures is run by the same team that creates The Daily Brief and Aftermarket Report.