Sometimes, a single slide can explain more than a long report. Points and Figures is our way of breaking down what India’s leading companies are telling their shareholders and analysts. We comb through the decks, pull out the charts and data points that actually matter, and highlight the signals behind the numbers—whether about growth plans, margins, new markets, or risks on the horizon.

This is an extension of The Chatter. While The Chatter focuses on management commentary and earnings call transcripts, Points and Figures dives into investor presentations—and soon, even annual reports—to decode what companies are showing, not just what they’re saying.

We go through every major investor presentation so you don’t have to—bringing you the sharpest takeaways that reveal not just what the company is saying, but what it really means for the business, its sector, and the broader economy.

In this edition, we have covered 11 companies across 9 industries.

InvIT

Energy Infrastructure Trust

Logistics

Swan Defence and Heavy Industries

Engineering & Capital Goods

Railtel Corporation Of India

Vikram Solar

Chemicals

EPL Ltd

Software Services

Ceinsys Tech Ltd

Sagility Ltd

Building Materials

Berger Paints India Ltd

Diversified

3M India Ltd

FMCG

Varun Beverages Ltd

Healthcare

Aurobindo Pharma Ltd

InvIT

Energy Infrastructure Trust | Micro Cap | Financial Services

Energy Infrastructure Trust is an India‑based Infrastructure Investment Trust (InvIT) owning and operating a 1,485 km natural gas pipeline and related infrastructure; it transports gas across key consumption hubs, offers imbalance services, and provides stable investor distributions through energy asset income.

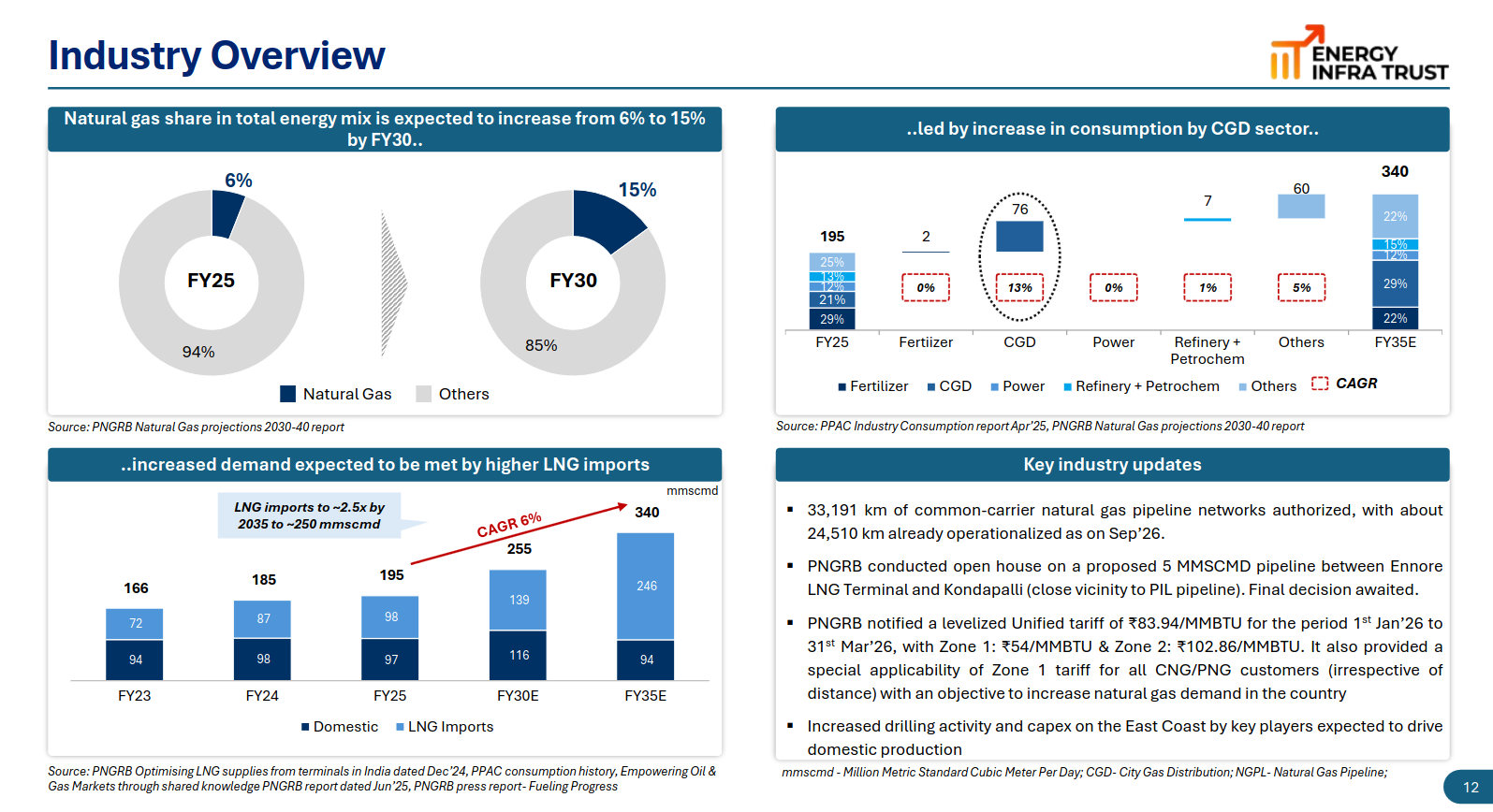

India’s natural gas share in the energy mix is expected to rise meaningfully, driven by strong growth in city gas distribution and industrial demand. This will increasingly be supported by LNG imports and expanding pipeline infrastructure.

The pipeline is a critical link connecting KG Basin gas to key demand centers, with volume growth driven by rising domestic production and LNG integration. Strong downside protection through long-term contracts and a stable dividend track record adds to its investment appeal.

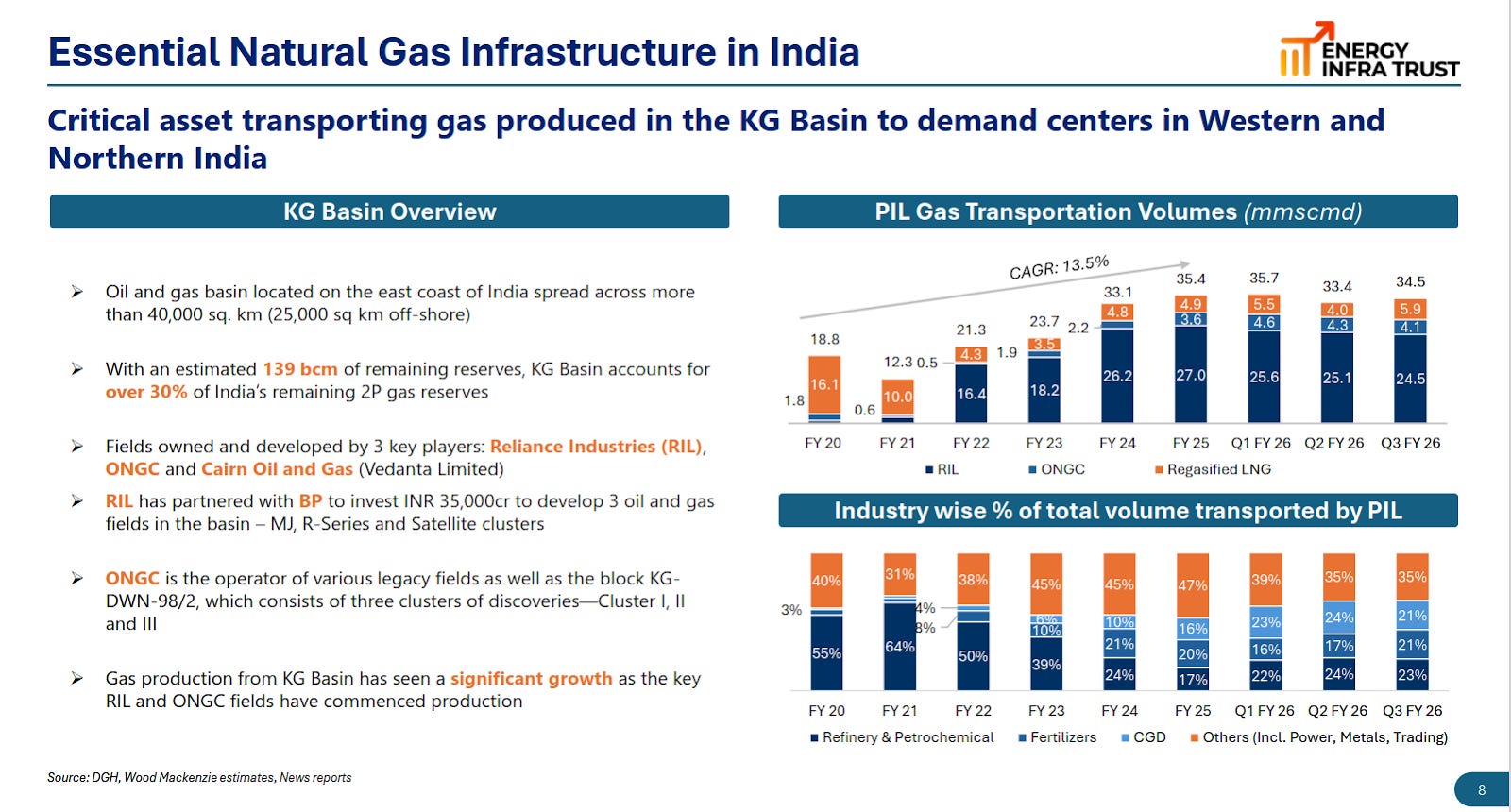

The asset plays a key role in transporting gas from the KG Basin, which holds a significant share of India’s reserves and is seeing rising production. Volumes have grown steadily, supported by increased domestic output and LNG contribution across sectors.

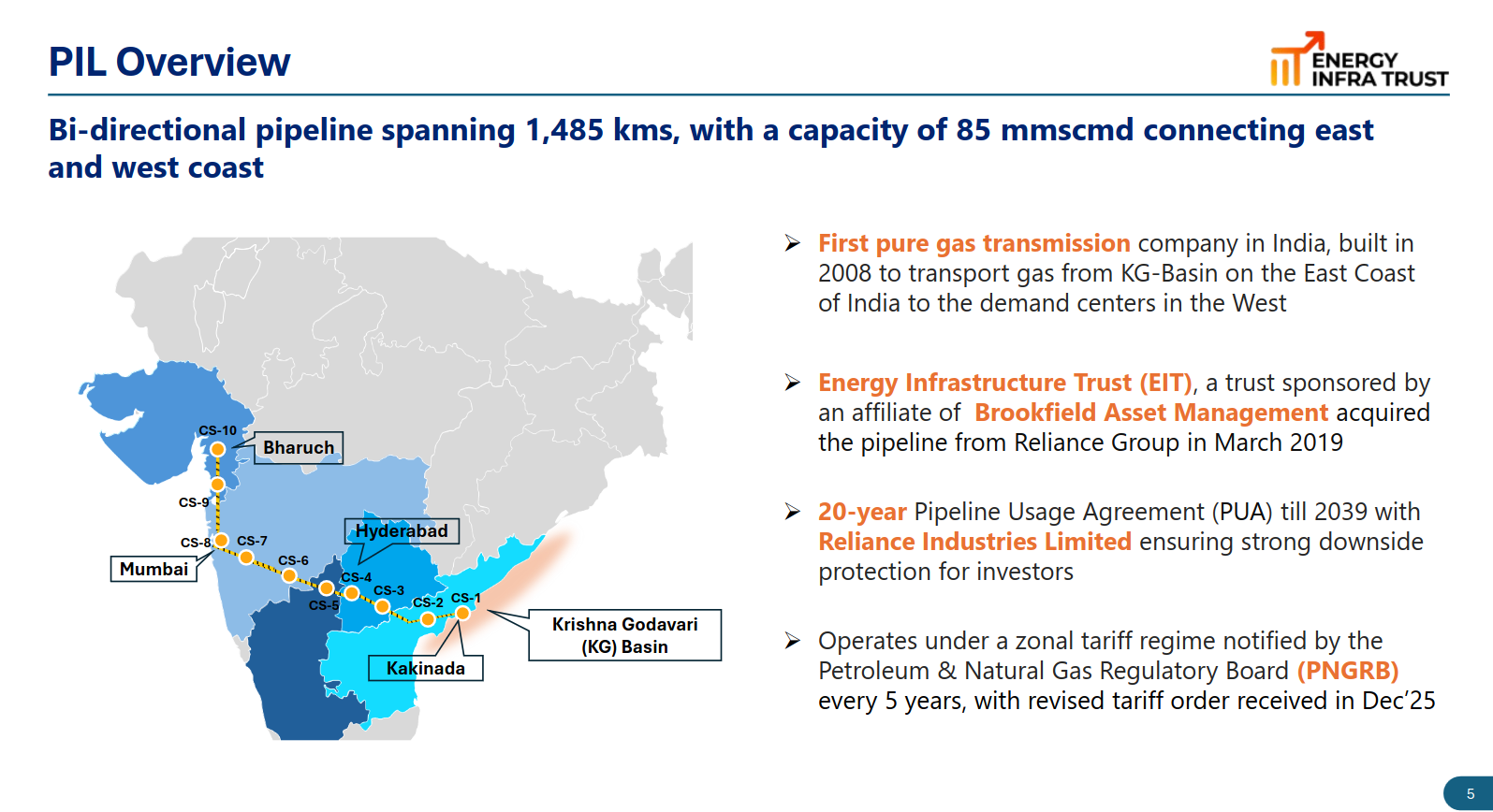

The 1,485 km pipeline connects India’s east and west coasts, enabling efficient gas transmission across regions. Backed by long-term agreements with Reliance and regulated tariffs, the asset offers stable and predictable cash flows.

Logistics

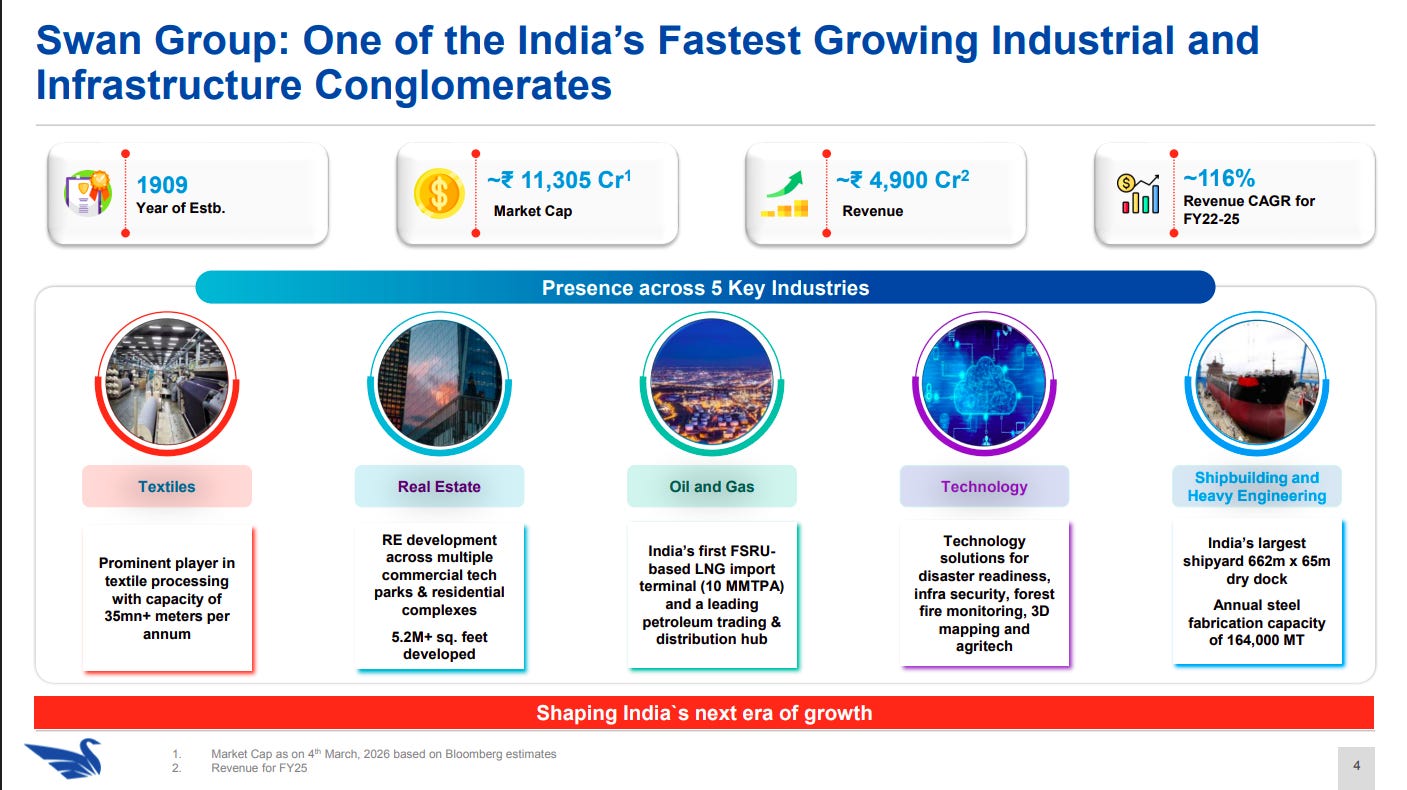

Swan Defence and Heavy Industries | Small Cap | Logistics

Swan Defence and Heavy Industries is currently engaged in the business activity viz. designing and manufacturing of ships primarily for defence sector, commercial shipbuilding, refits, repairs, etc. The Company is having integrated shipbuilding facilities (Shipyard), which is the largest engineering infrastructure in India and also one of the largest in the world.

Swan Group is a diversified infrastructure conglomerate with strong growth momentum (~116% revenue CAGR), operating across textiles, real estate, energy, technology, and shipbuilding. Its multi-sector presence and scale position it well to capitalize on India’s infrastructure and industrial growth.

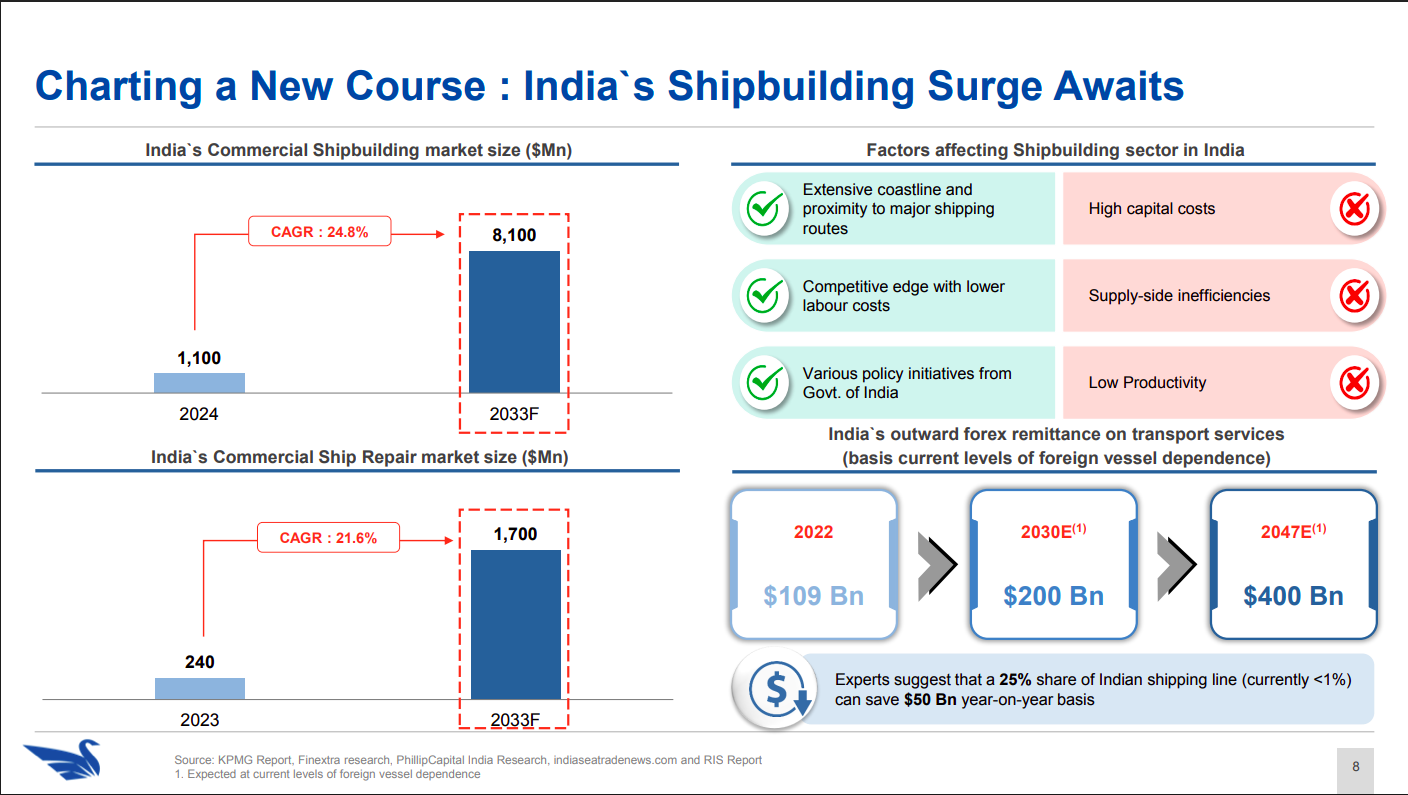

India’s ship repair market is expected to grow to ~$1.7 bn by 2033, driven by defence needs, commercial fleets, and regional demand. Both domestic and international opportunities create strong long-term visibility for ship repair players.

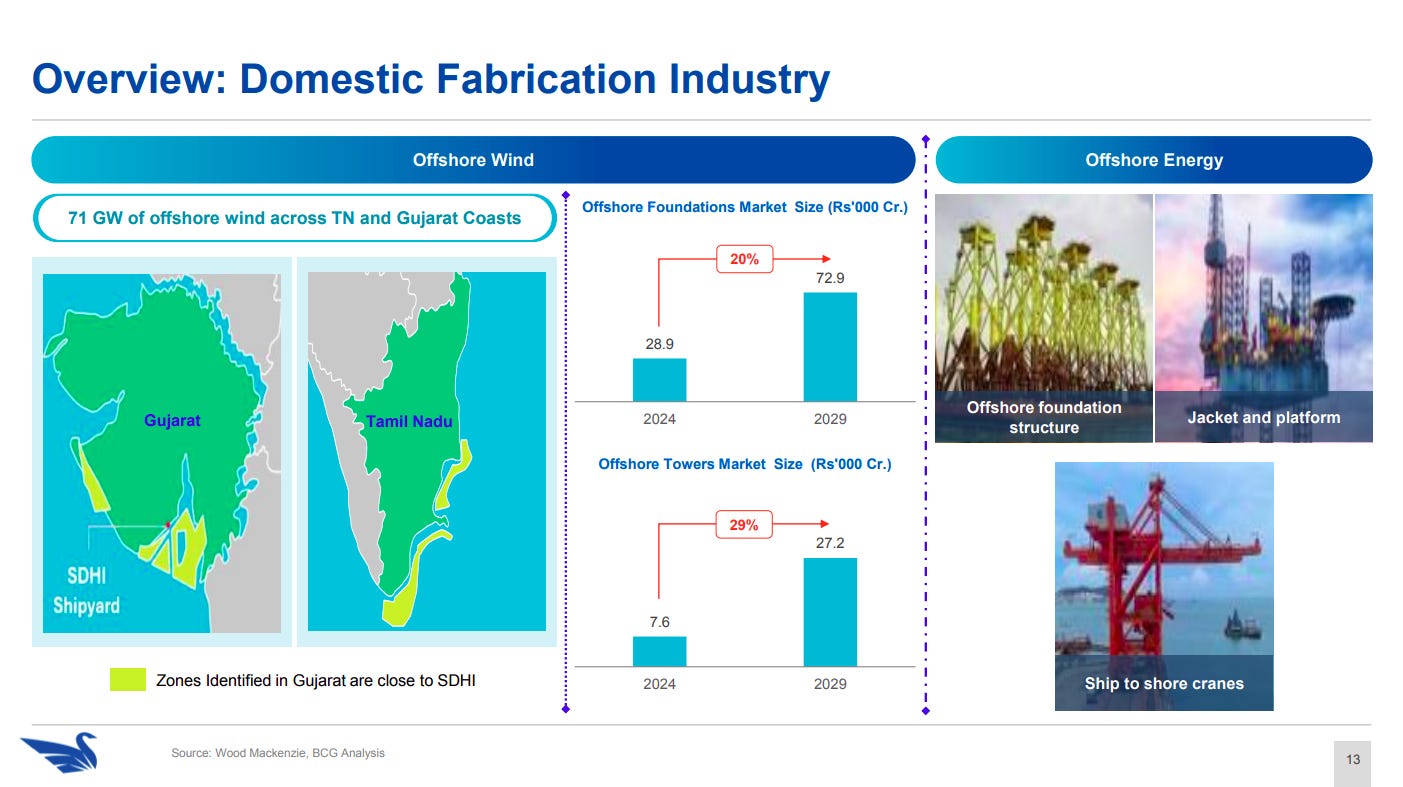

Offshore wind and energy fabrication present a large upcoming opportunity, with strong growth in foundations and tower markets. Strategic coastal locations and proximity to projects enhance execution advantages.

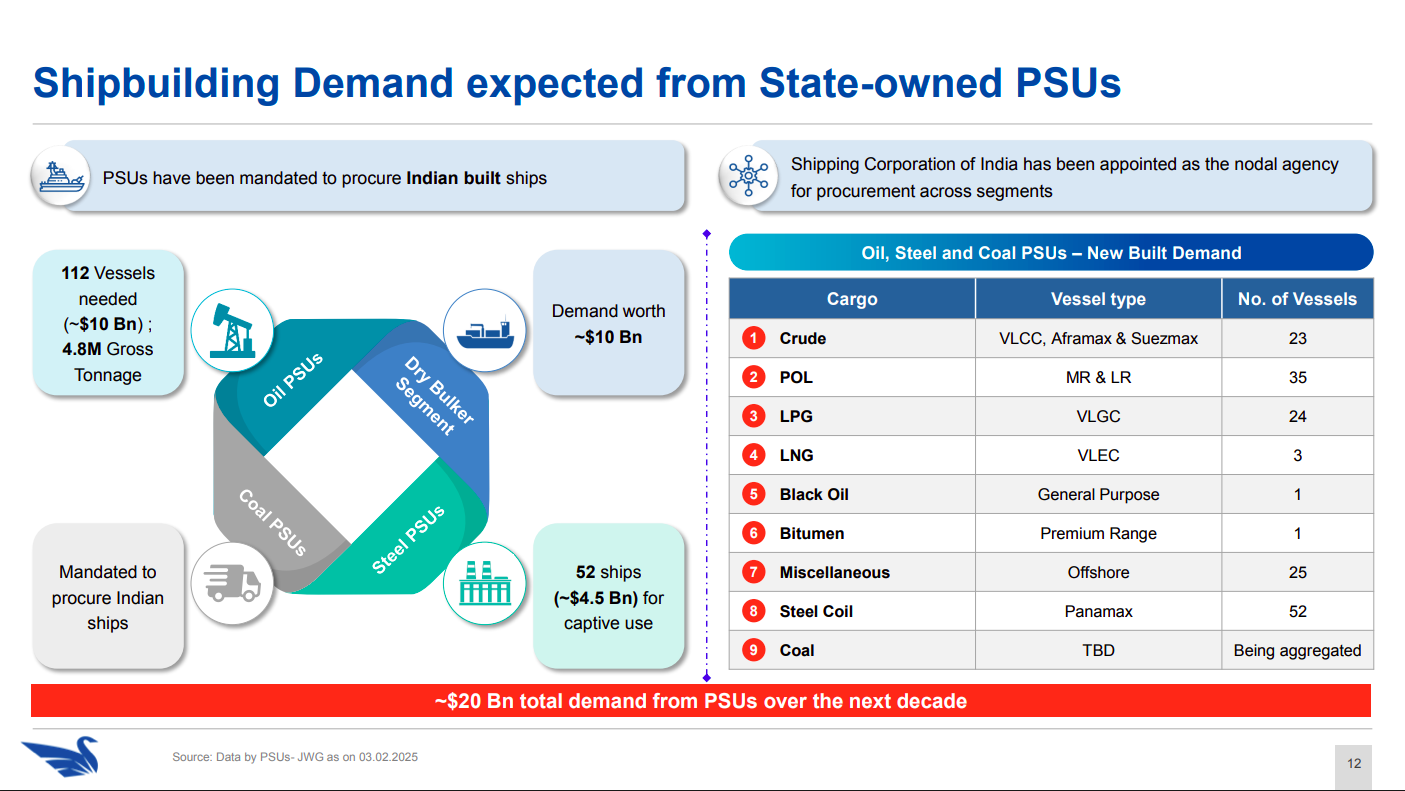

Government-led PSU demand (~$20 bn over the next decade) provides strong order visibility, driven by oil, steel, and logistics requirements. Mandatory domestic sourcing further strengthens the opportunity for Indian shipyards.

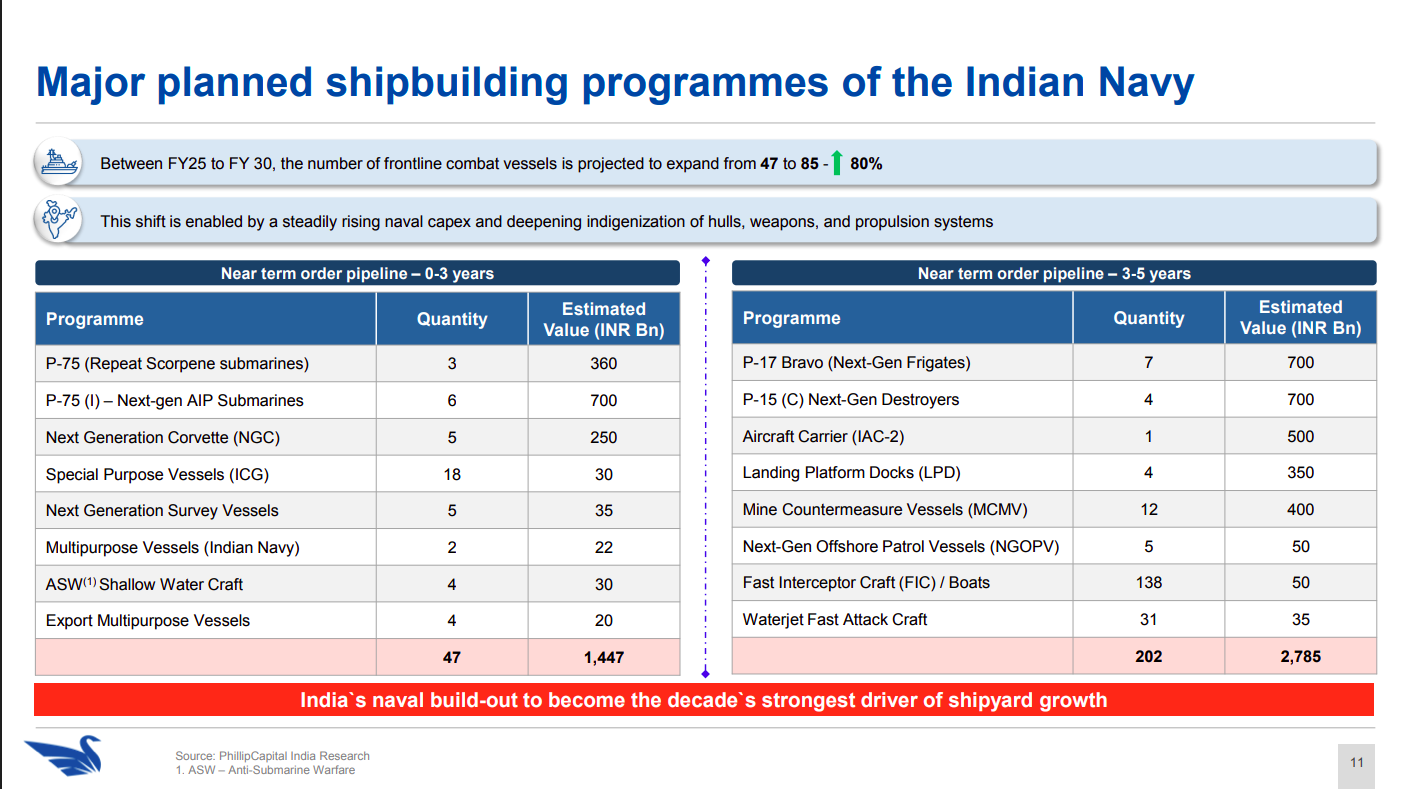

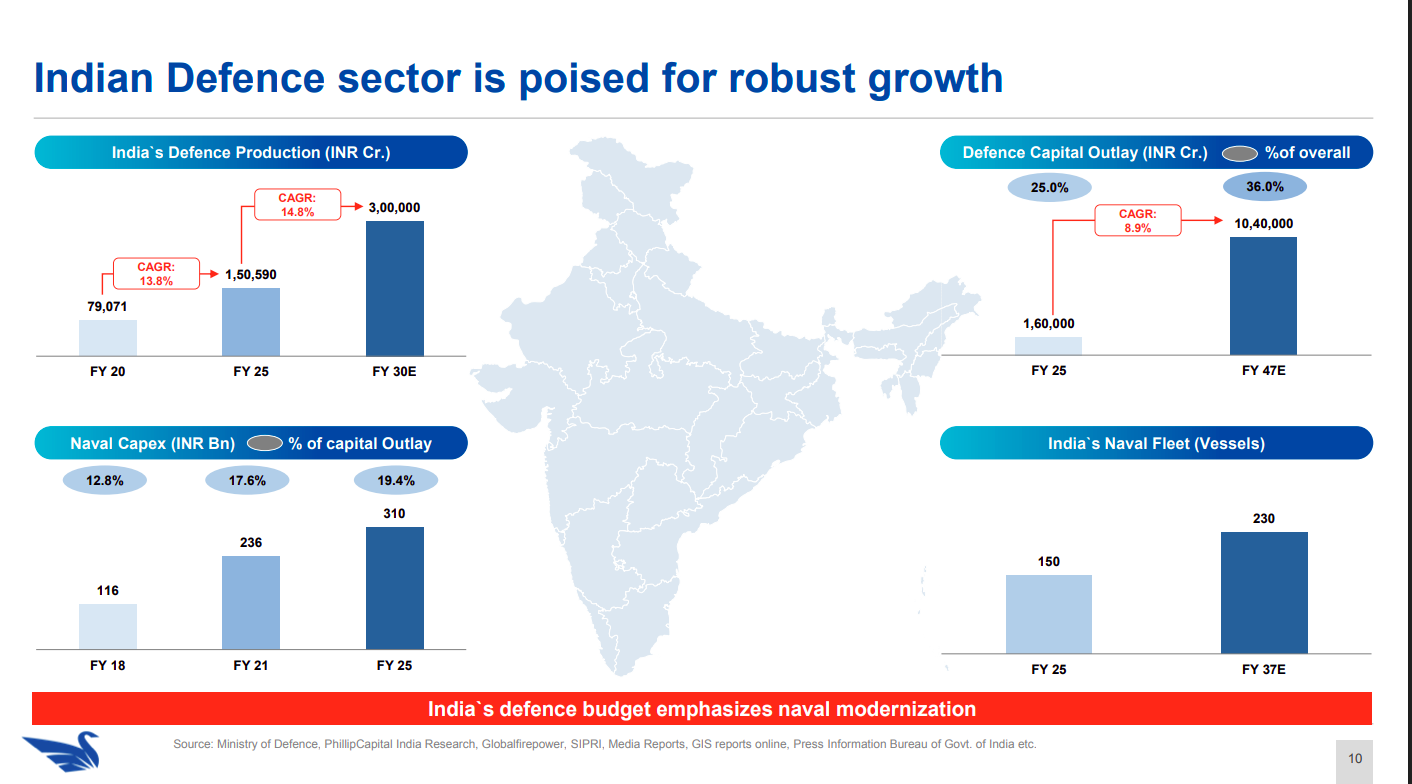

India’s naval expansion (47 to 85 vessels by FY30) creates a large, multi-year order pipeline across submarines, frigates, and support vessels. This positions defence shipbuilding as a key long-term growth driver.

Defence production and capex are set for strong growth, with increasing allocation toward naval modernization. Rising fleet size and sustained budget support provide long-duration visibility for shipbuilders.

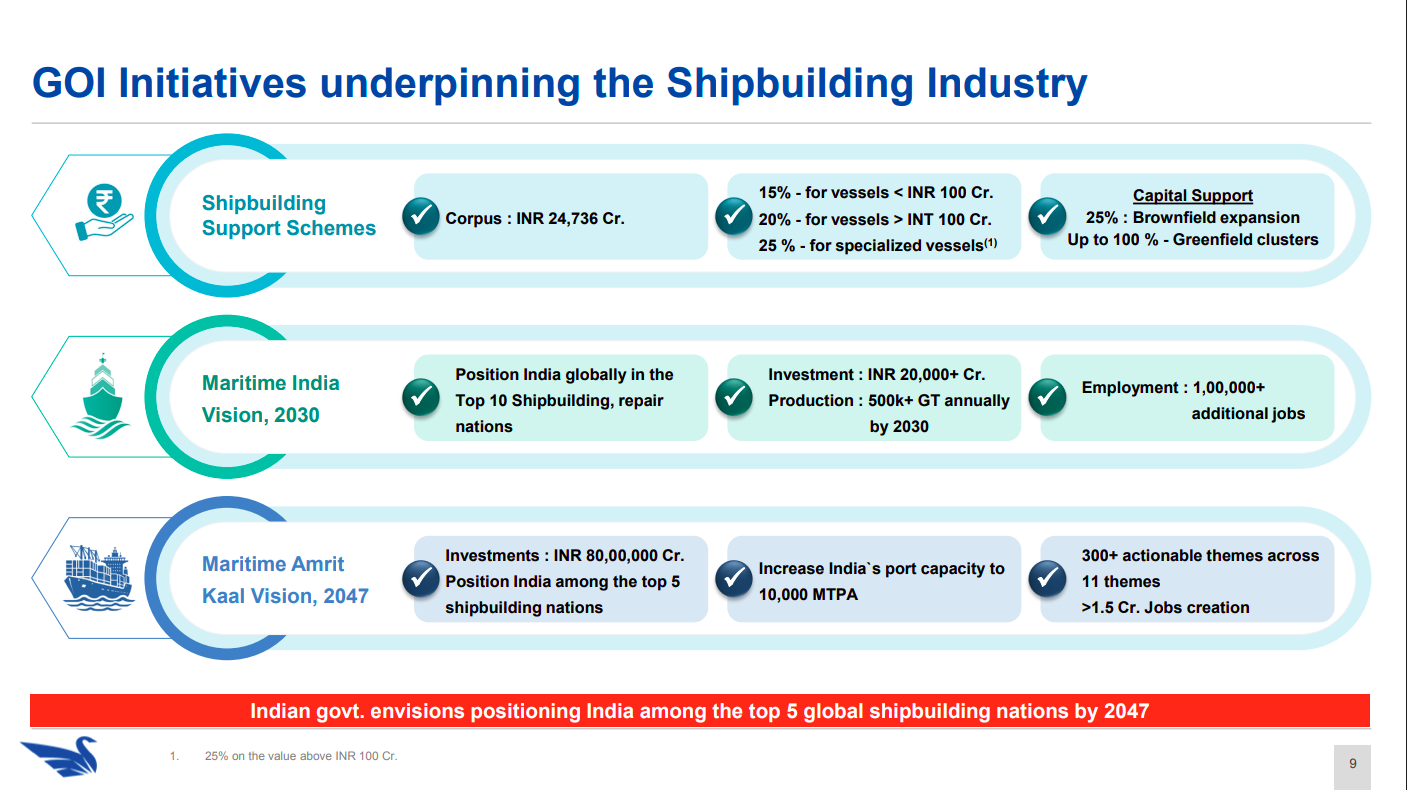

Policy support through subsidies, incentives, and long-term maritime visions (2030, 2047) aims to position India among top global shipbuilding nations. Large investments and job creation plans strengthen the ecosystem.

India’s commercial shipbuilding and repair markets are expected to grow at strong double-digit CAGRs (~25%+), supported by policy push and cost advantages. Increasing localization can significantly reduce forex outflows.

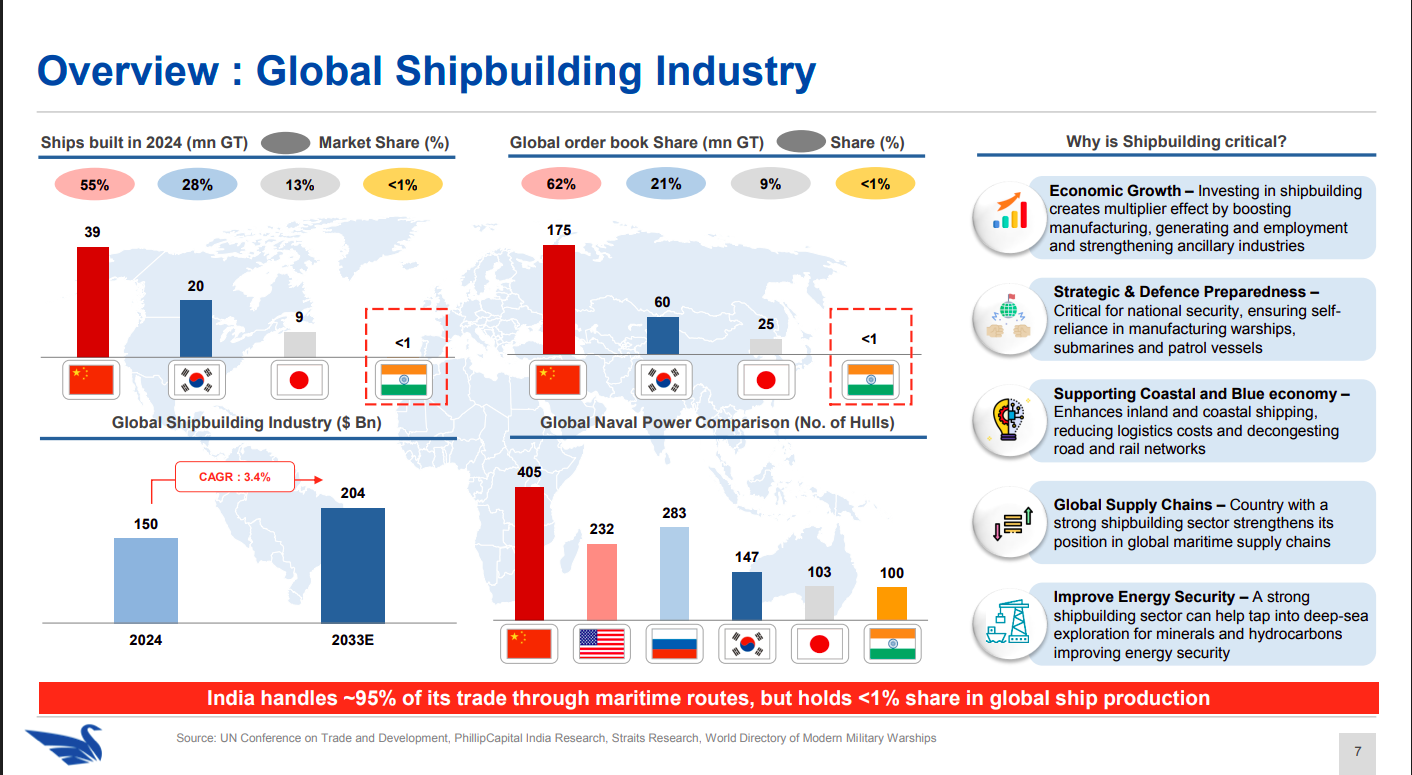

Global shipbuilding is dominated by China, Korea, and Japan, with India holding <1% share despite handling ~95% of trade via sea. This highlights a massive opportunity for India to scale its shipbuilding capabilities.

Engineering & Capital Goods

Railtel Corporation Of India | Small Cap | Engineering & Capital Goods

Railtel Corporation Of India Limited is a major neutral telecom infrastructure provider in India. It offers high-capacity DWDM technology and MPLS network to meet critical communication needs of Indian Railways and other clients. The company also manages data centers in Gurugram, Haryana and Secunderabad, Telangana for hosting essential applications.

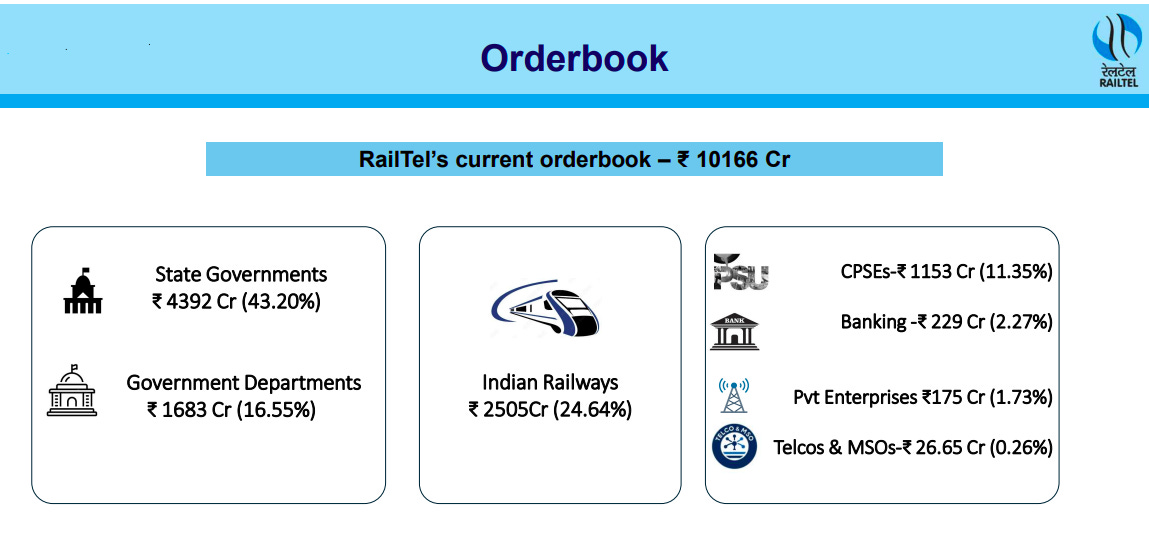

RailTel has a strong orderbook of ₹10,166 Cr, largely driven by government clients, with state governments and Indian Railways forming the bulk. This provides high revenue visibility and stability given the public-sector focus.

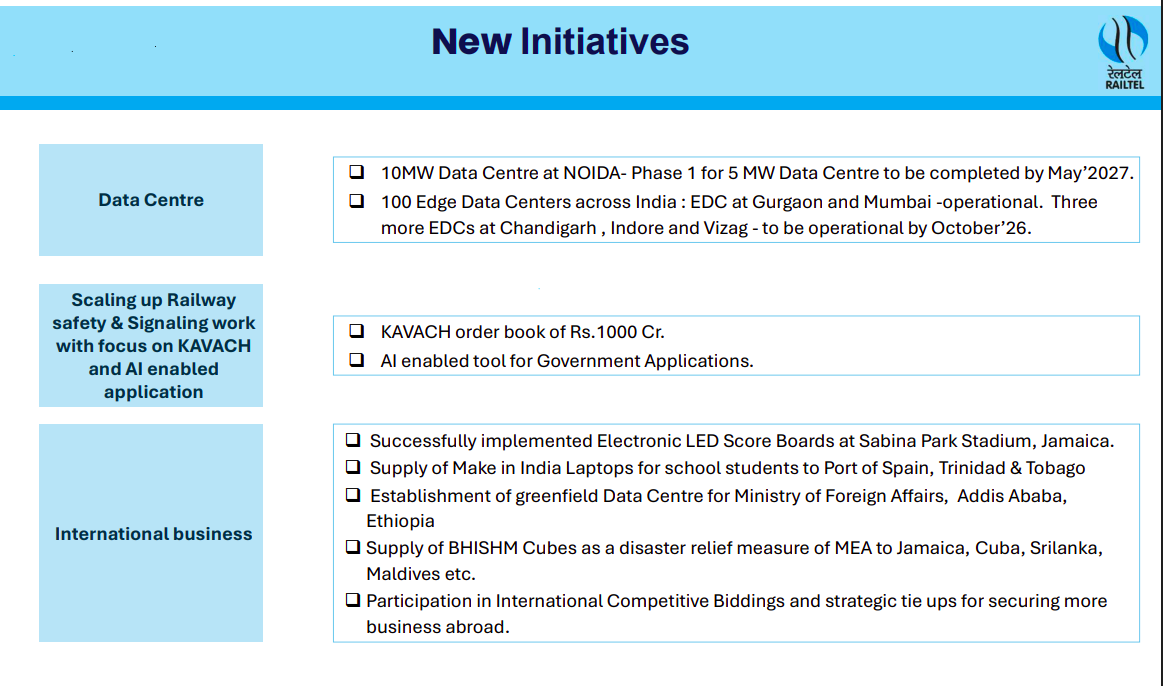

RailTel is expanding into data centres, AI-led railway safety (KAVACH), and global projects, diversifying beyond core telecom. These initiatives open new growth avenues while strengthening its digital and international presence.

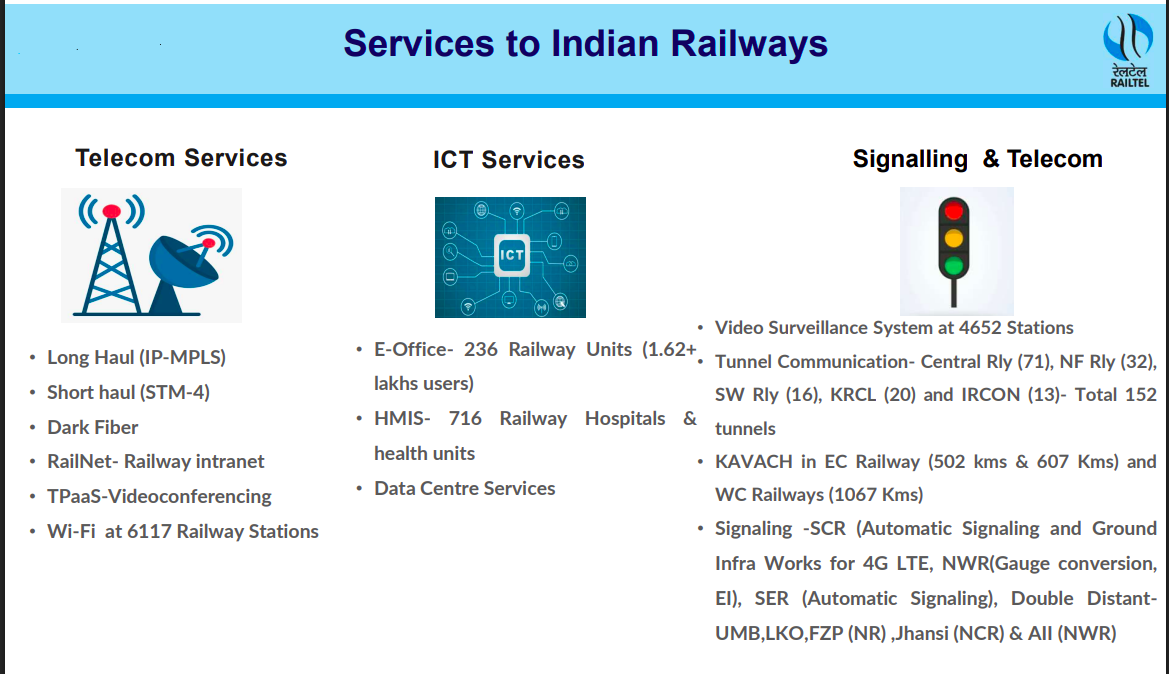

RailTel plays a critical role across telecom, ICT, and signalling for Indian Railways, including Wi-Fi, surveillance, and KAVACH deployment. Its deep integration into railway operations creates strong entry barriers and recurring demand.

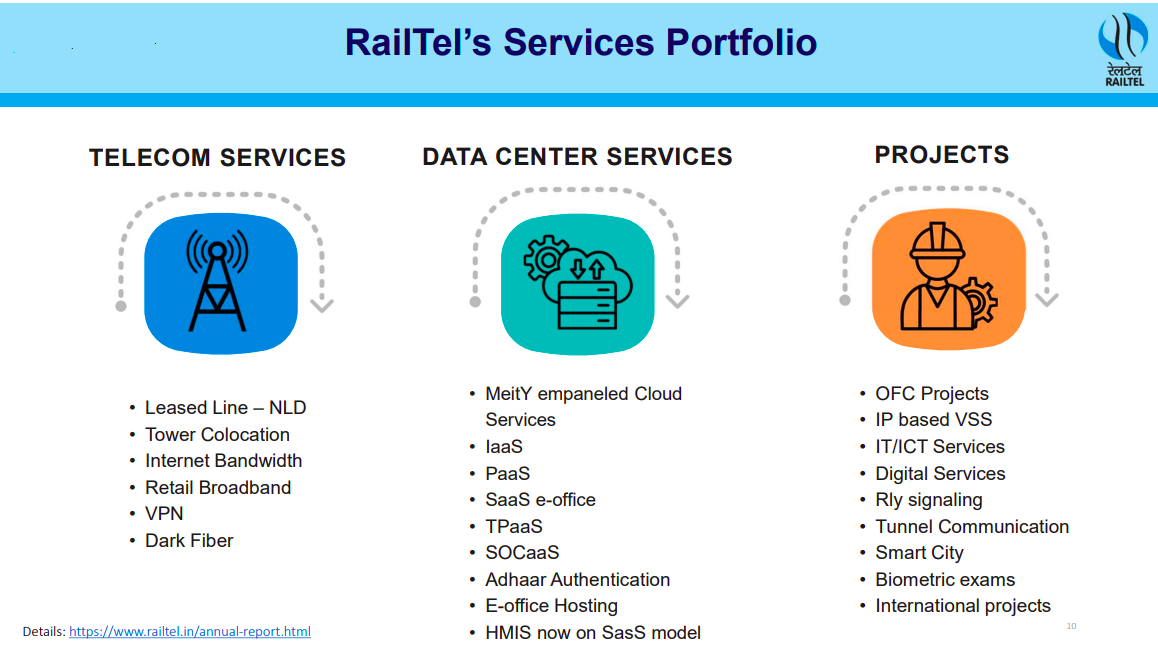

The company offers a diversified portfolio spanning telecom, cloud/data centres, and turnkey projects like smart cities and signalling. This broad capability positions RailTel as a full-stack digital infrastructure player.

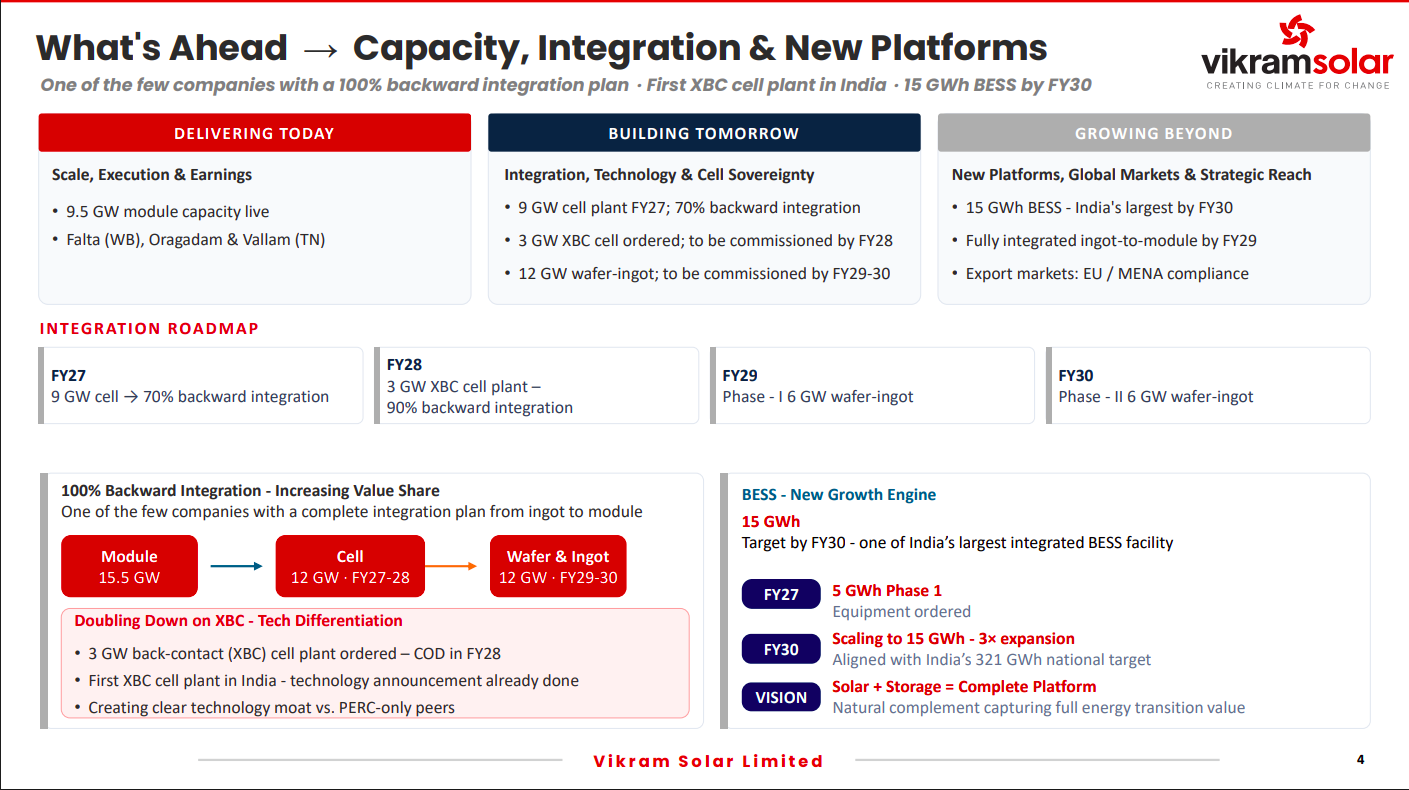

Vikram Solar | Small Cap | Engineering & Capital Goods

Vikram Solar and its subsidiaries specialize in manufacturing and selling solar photovoltaic modules and systems. Their product portfolio includes a variety of monocrystalline silicon-based modules such as PERC modules, N-Type modules, and HJT modules, available in bifacial or monofacial configurations.

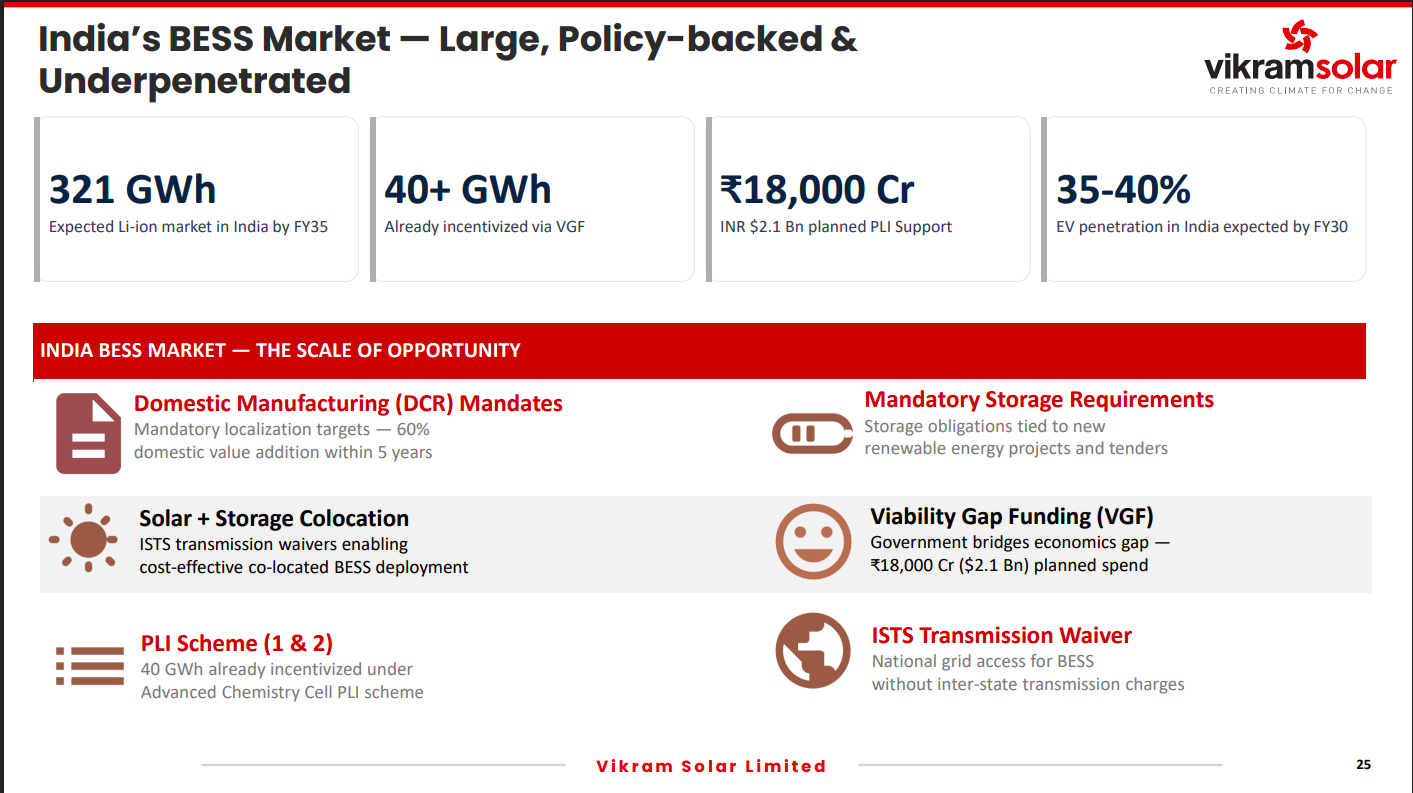

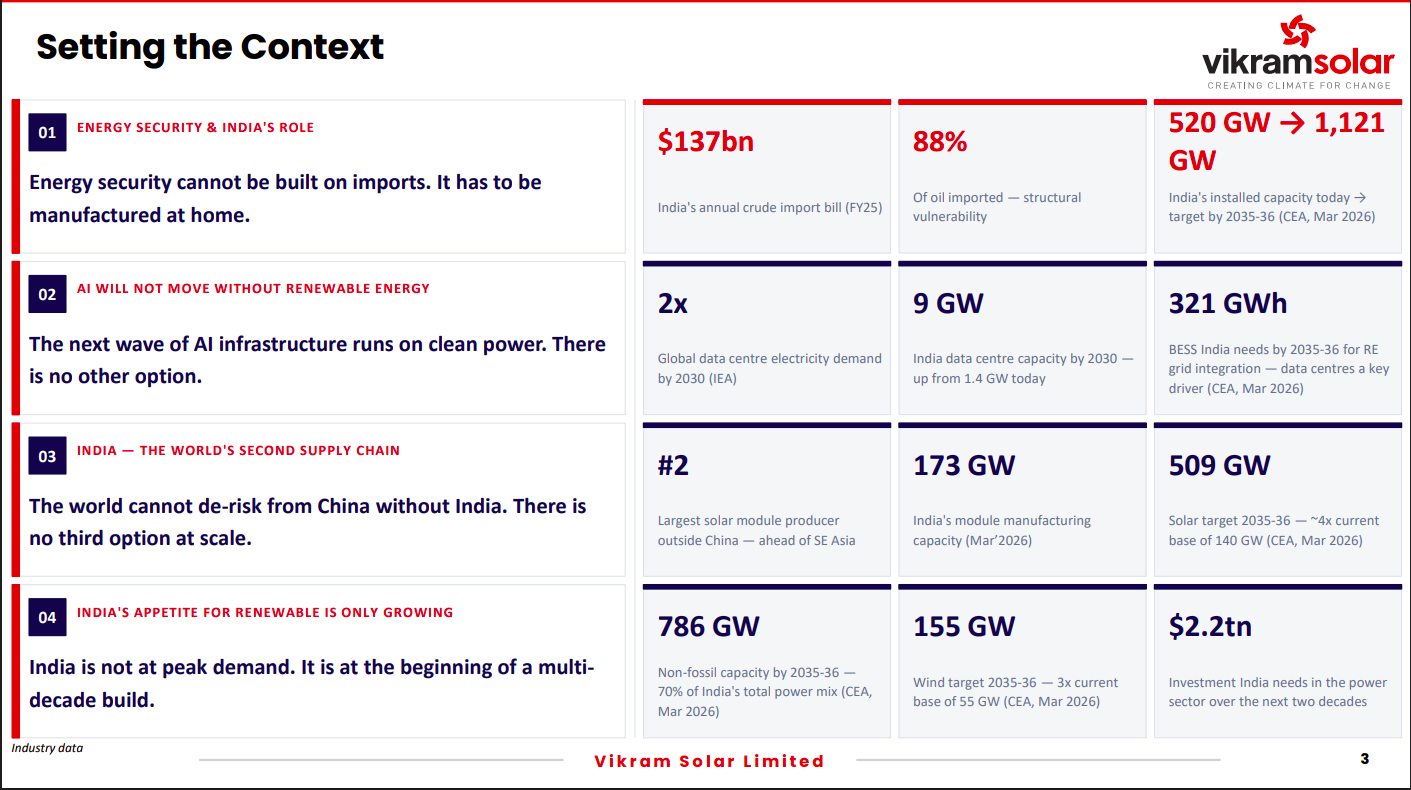

India’s battery storage market is large (~321 GWh by FY35) and strongly policy-backed through PLI, VGF, and storage mandates. Low current penetration and rising EV + renewable demand create a significant long-term opportunity.

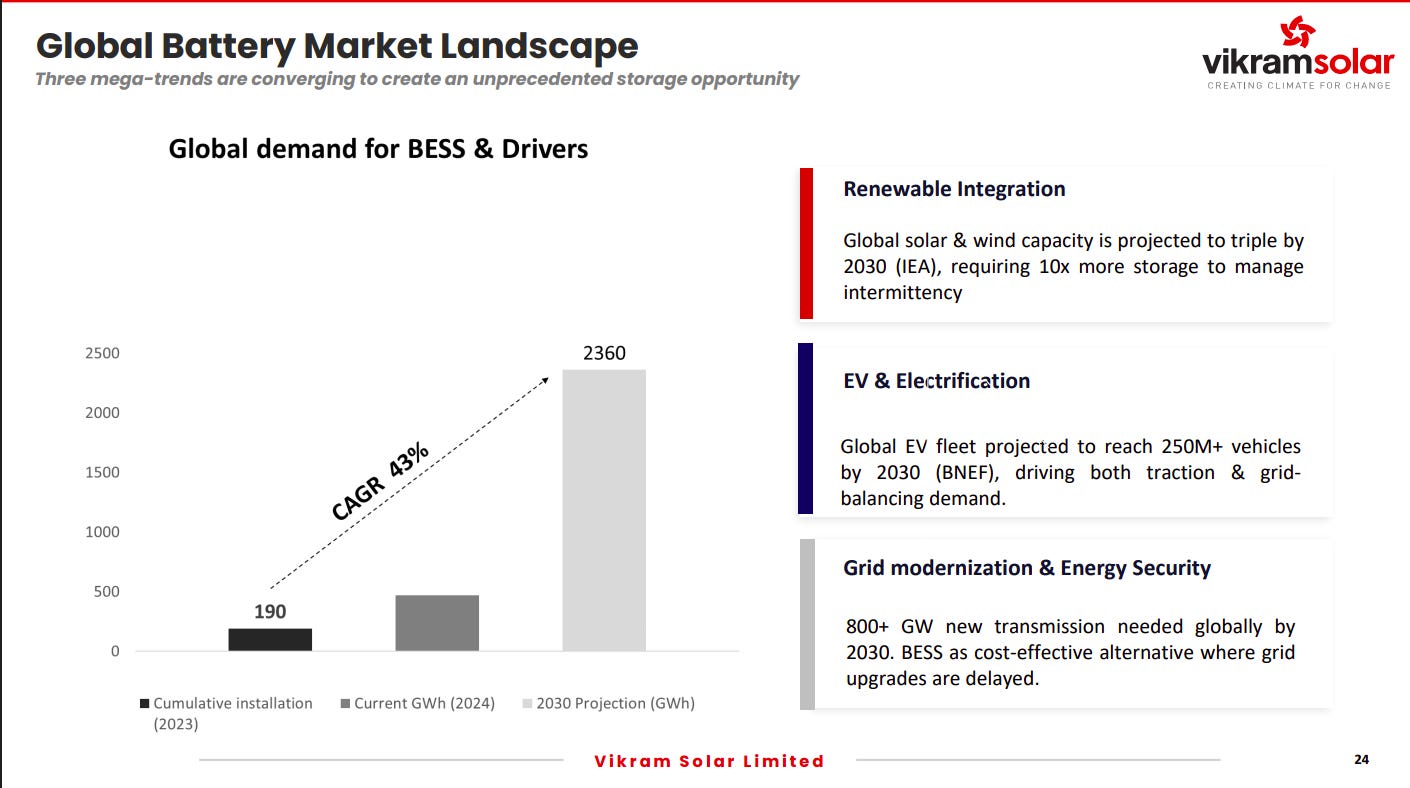

Global BESS demand is set for explosive growth (~43% CAGR), driven by renewable integration, EV adoption, and grid modernization. Storage is becoming essential to manage intermittency and ensure energy security.

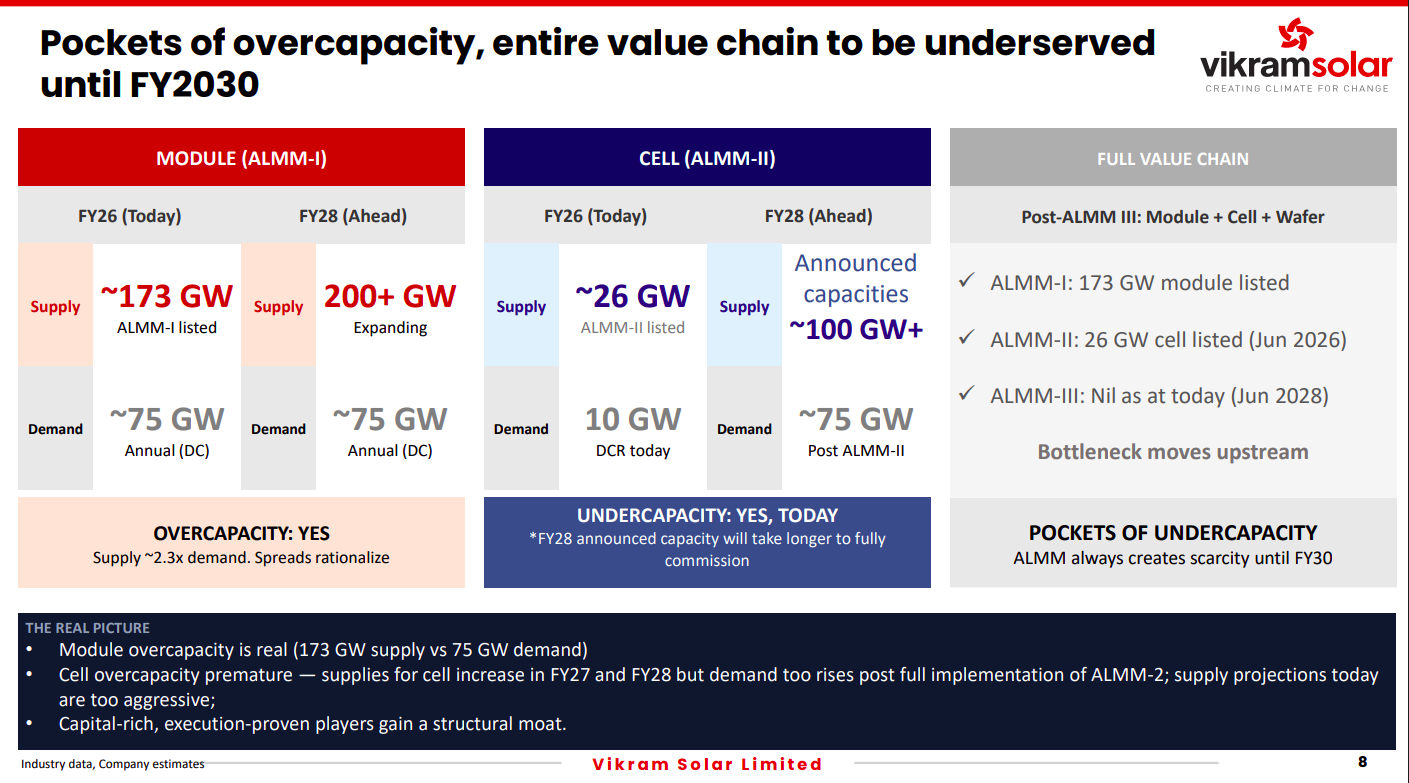

While module capacity is currently oversupplied (~2.3x demand), upstream segments like cells remain underpenetrated. Over time, bottlenecks shift upstream, favoring integrated players with execution capabilities.

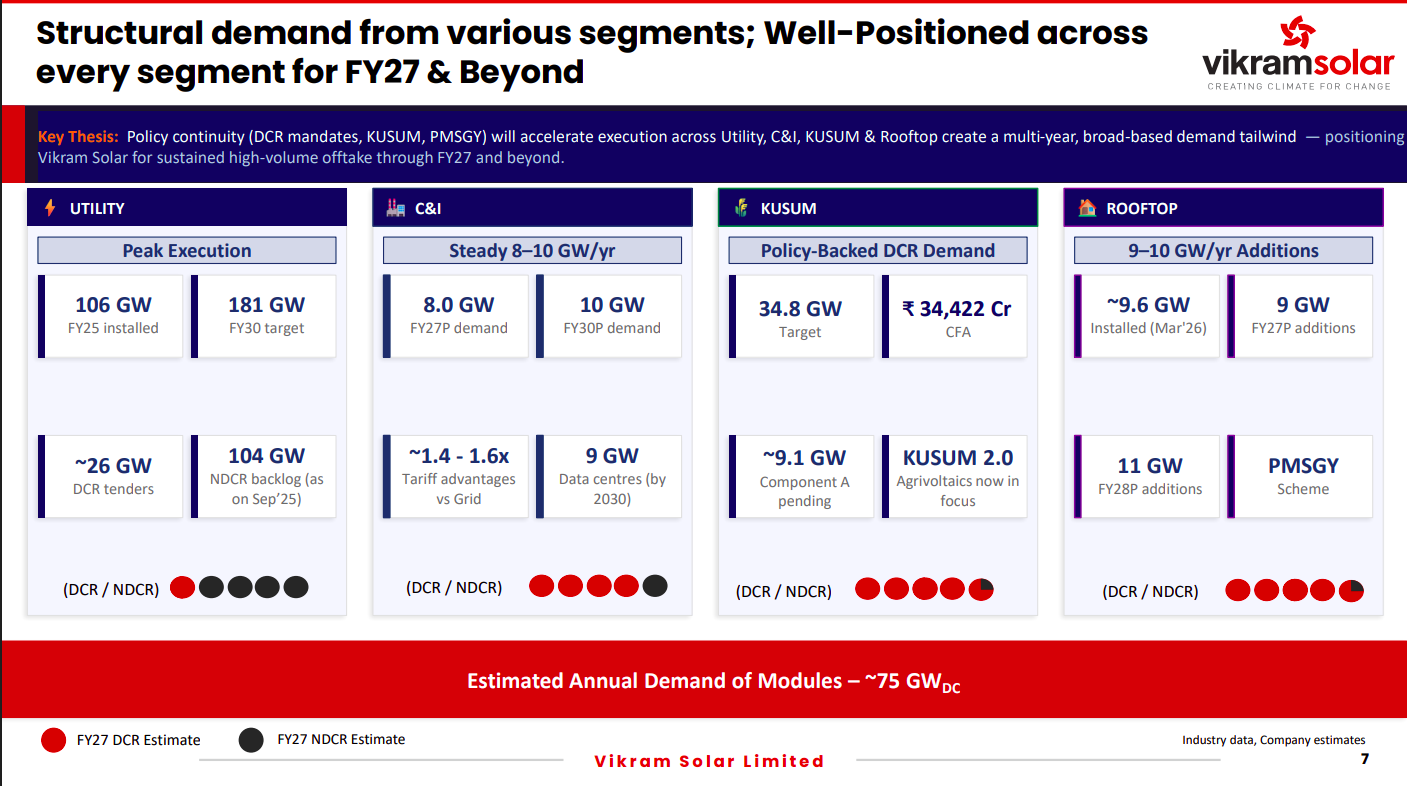

Demand is broad-based across utility, C&I, rooftop, and government programs like KUSUM, ensuring multi-year visibility. Annual module demand of ~75 GW highlights a strong, sustained volume opportunity.

The company is building full backward integration from modules to cells and wafers, alongside scaling BESS to 15 GWh by FY30. This positions it as a fully integrated energy solutions player with global ambitions.

India’s energy transition is driven by energy security, rising AI/data centre demand, and global supply chain shifts. Massive renewable targets and infrastructure investments create a long-duration growth runway.

Chemicals

EPL Limited | Small Cap | Chemicals

EPL Limited, formerly Essel Propack Limited, is a global company specializing in manufacturing laminated plastic tubes for FMCG and Pharma sectors. They produce packaging materials like collapsible tubes and laminates for Beauty & Cosmetics, Health & Pharmaceuticals, Food, Home, and Oral care products, along with offering packaging solutions and ancillary services.

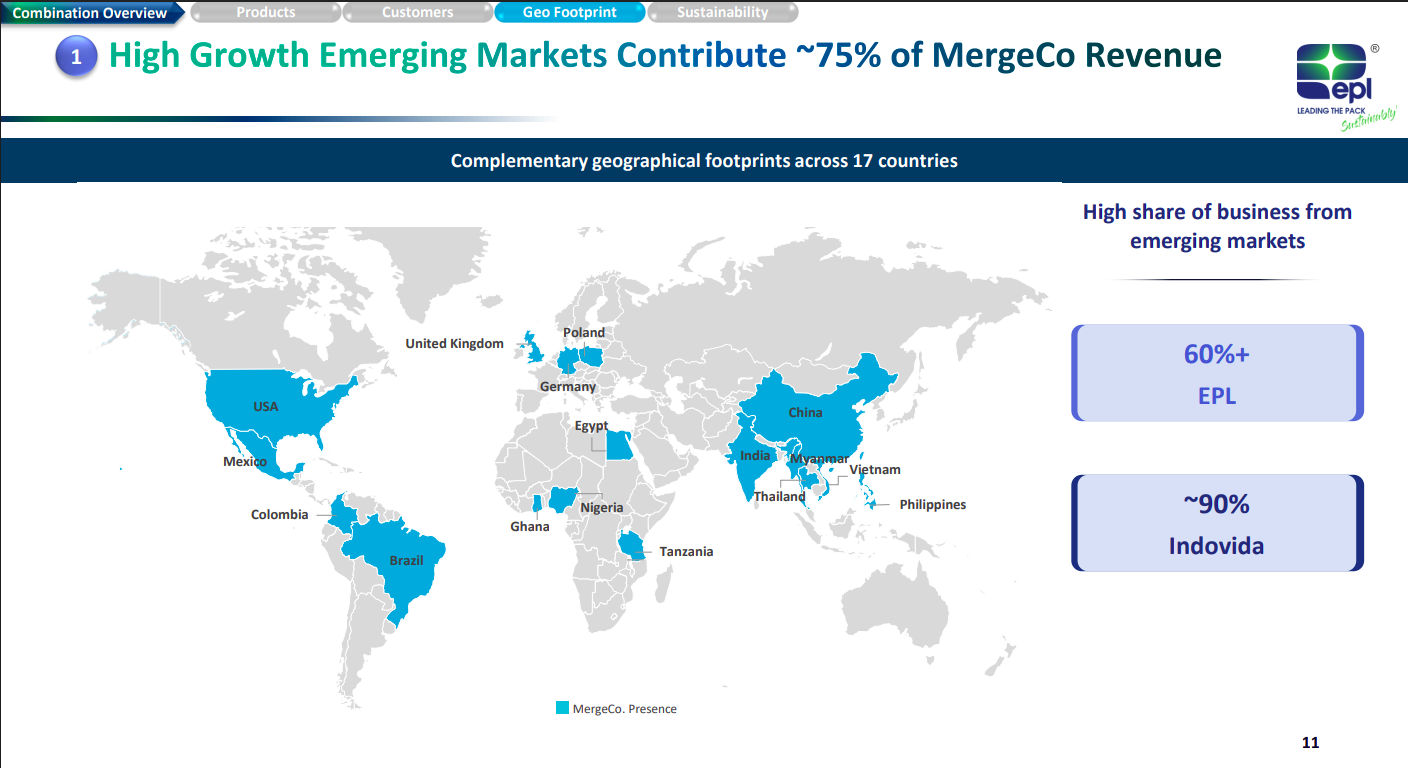

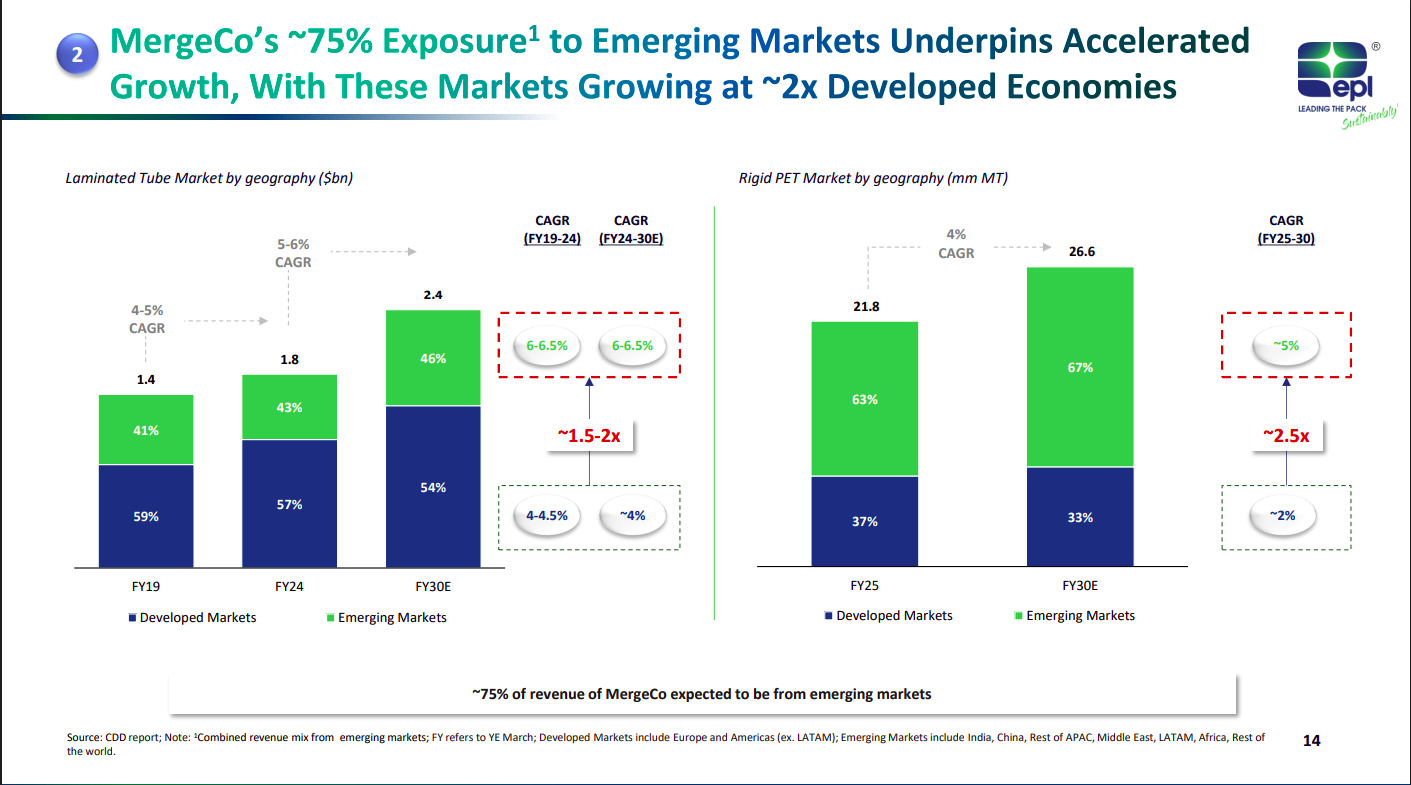

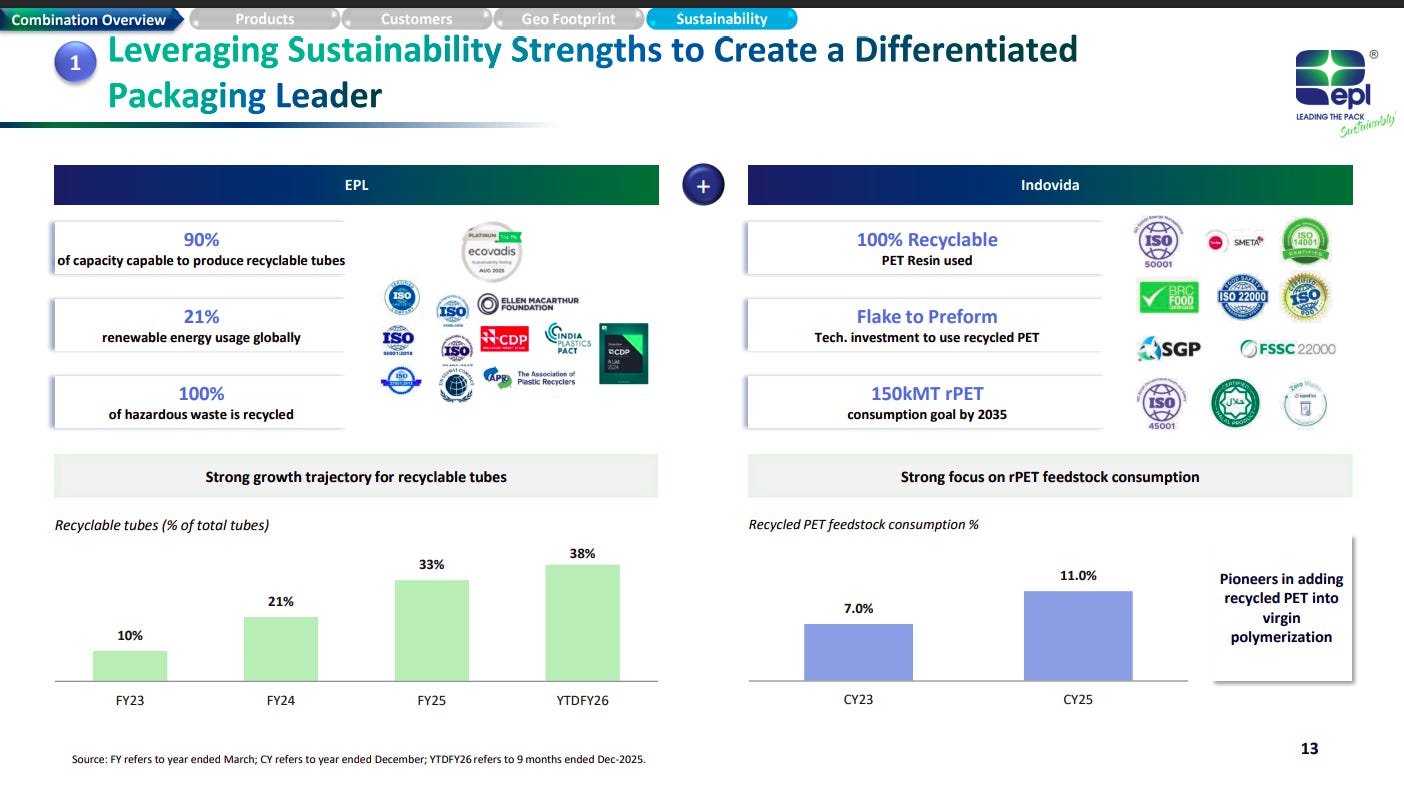

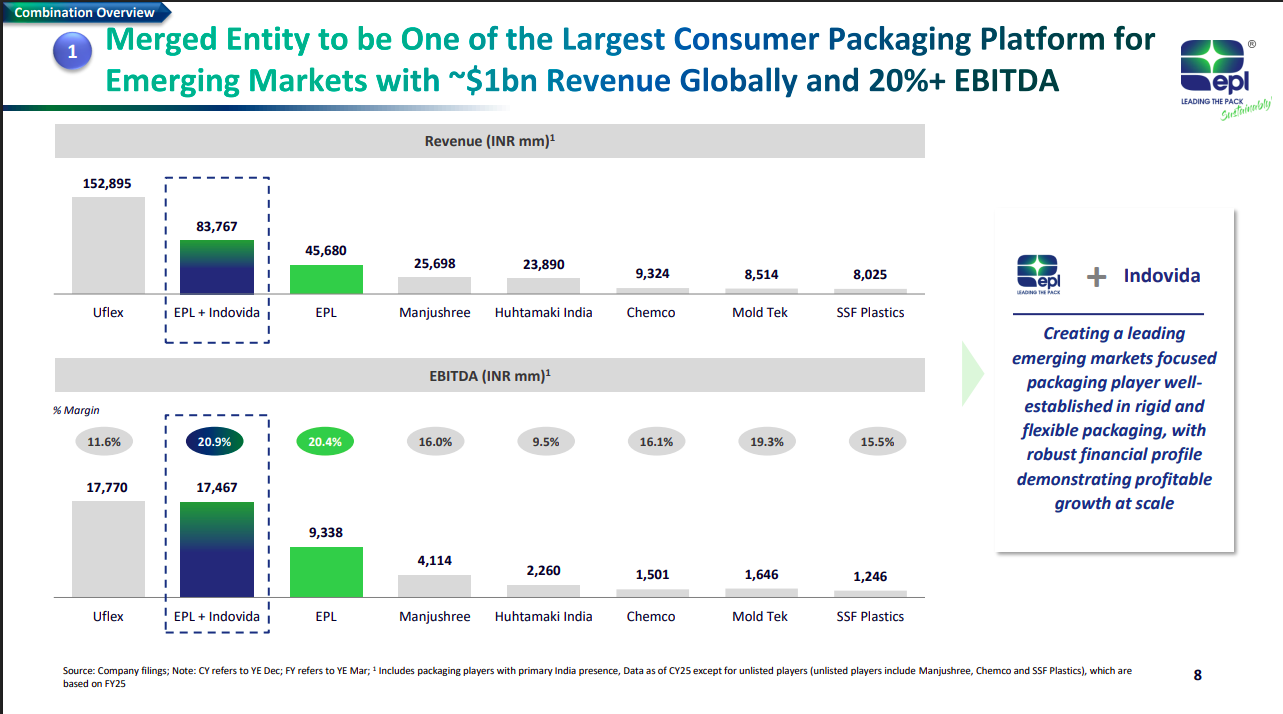

The merged entity derives ~75% of its revenue from high-growth emerging markets, with strong presence across 17 countries. Both EPL and Indovida have a heavy tilt towards these regions, positioning the business for structurally higher growth.

Emerging markets are growing ~1.5–2.5x faster than developed markets across both laminated tubes and rigid PET. This growth differential underpins sustained revenue expansion for the merged entity.

EPL and Indovida bring strong sustainability credentials, including high recyclable output and increasing use of recycled PET. This positions the company well for regulatory shifts and evolving customer preferences.

The combined entity serves a wide range of global FMCG leaders across oral care, beauty, and pharma. Strong relationships with marquee clients enhance revenue stability and cross-selling opportunities.

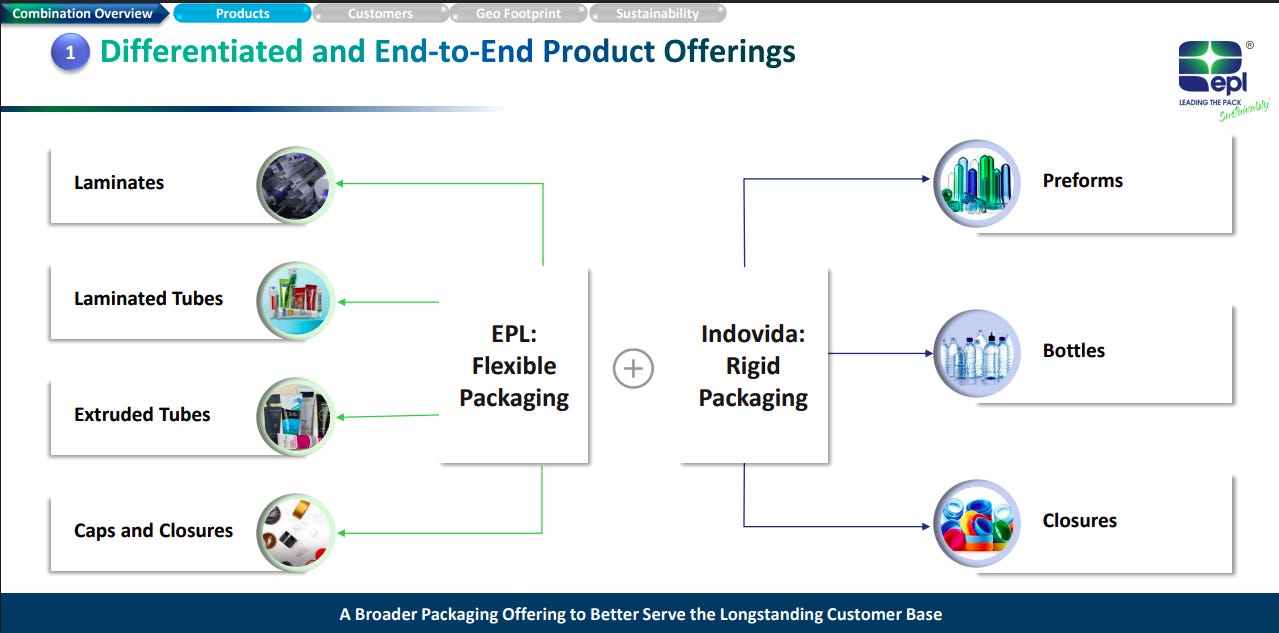

The merger creates an end-to-end packaging platform, combining flexible packaging (EPL) with rigid packaging (Indovida). This broadens offerings across tubes, laminates, bottles, and preforms.

The merged entity becomes one of the largest emerging market-focused packaging players with ~$1bn revenue and 20%+ EBITDA margins. This scale, combined with profitability, supports strong growth visibility.

Software Services

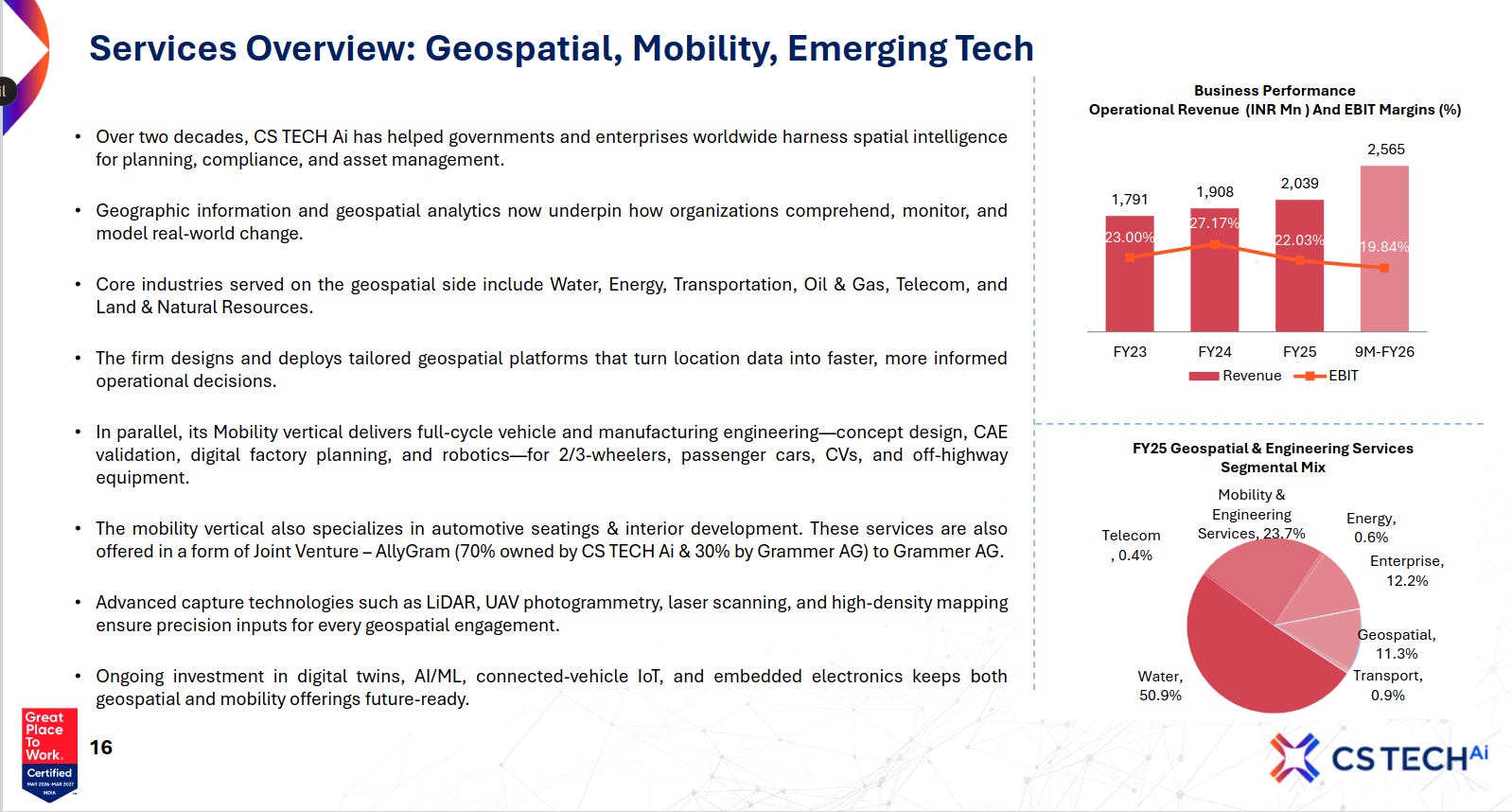

Ceinsys Tech Ltd. | Small Cap | Software Services

Ceinsys Tech Ltd.is a specialist in GIS & is an Engineering services solution provider company, servicing clients across a range of corporate and government segments helping improve their engineering efficiency, support global footprint and improve competitiveness..The company also in the business activities of WP, EES.

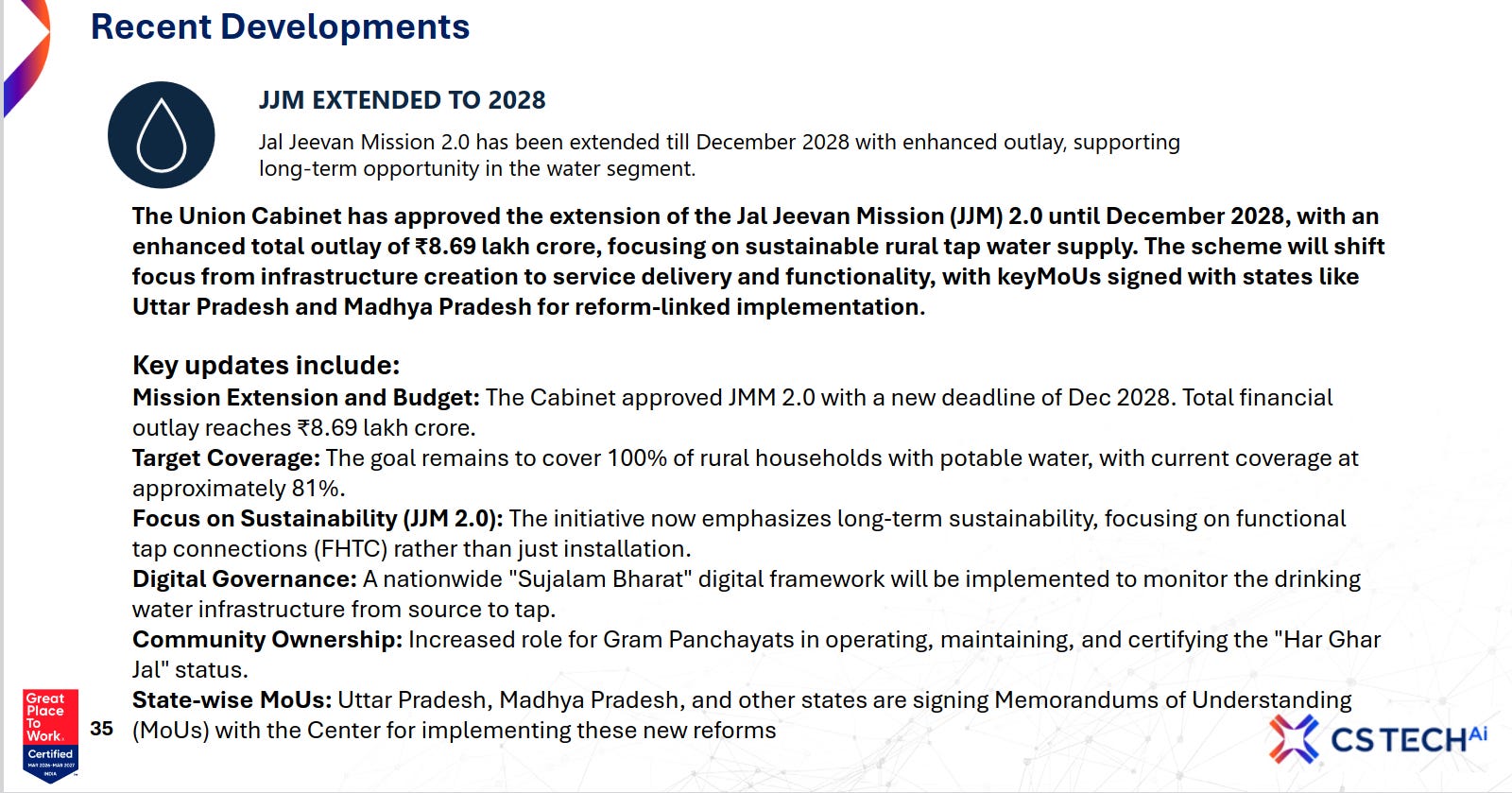

The Jal Jeevan Mission has been extended to 2028 with a ₹8.69 lakh crore outlay, shifting focus from infrastructure creation to sustainable service delivery. This ensures long-term visibility in the water segment with stronger governance and state-level execution.

CS Tech AI caters to a wide mobility spectrum—from passenger and commercial vehicles to off-highway and 2/3 wheelers. Its offerings span interiors, structures, and electrical systems, enabling full-stack engineering capabilities.

The company serves diverse sectors including water, energy, infrastructure, oil & gas, transportation, and telecom. Its solutions range from digital twins and GIS to project management and operational analytics.

CS Tech AI combines geospatial intelligence with mobility engineering to deliver end-to-end solutions across industries. Strong revenue growth with stable margins is supported by a diversified segment mix, led by water and mobility services.

Sagility Limited | Small Cap | Software Services

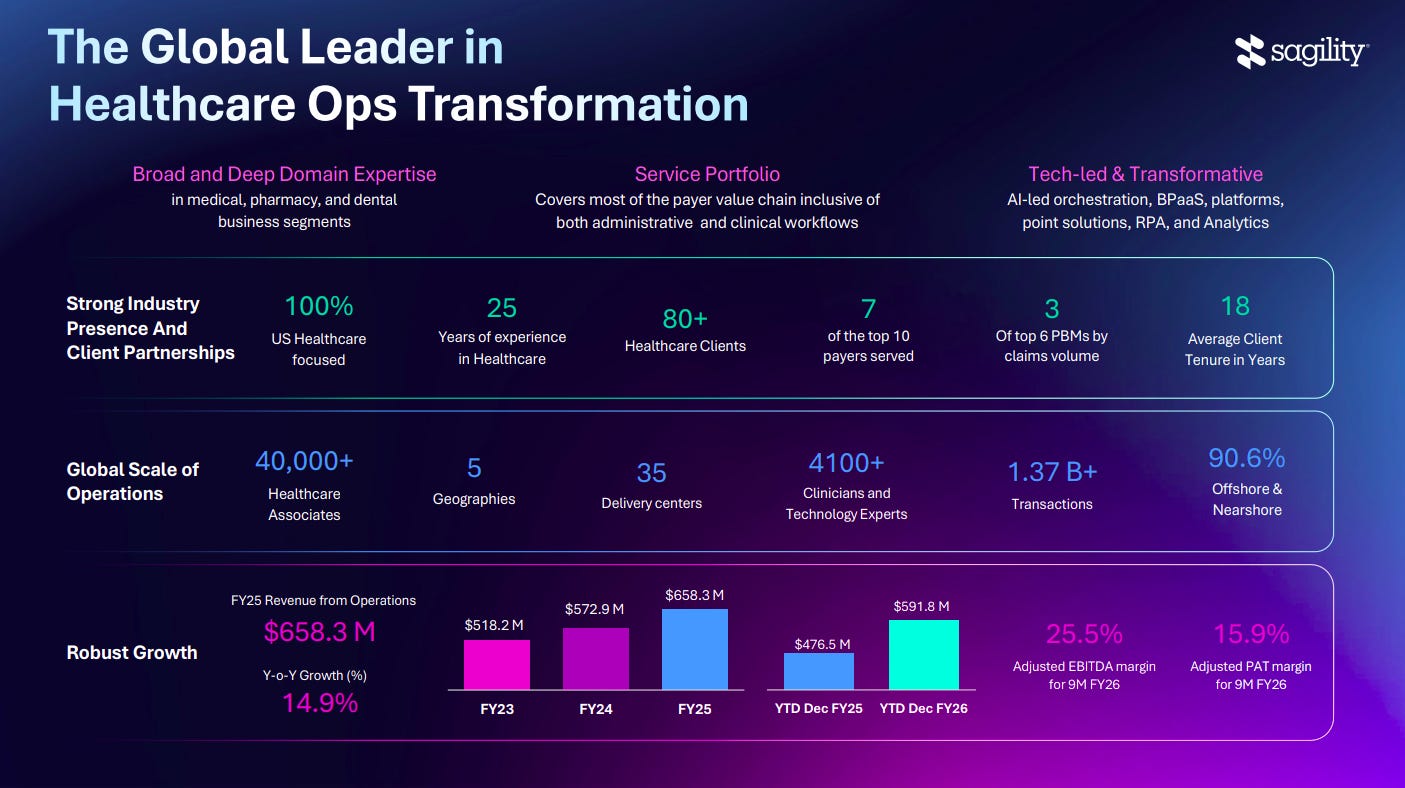

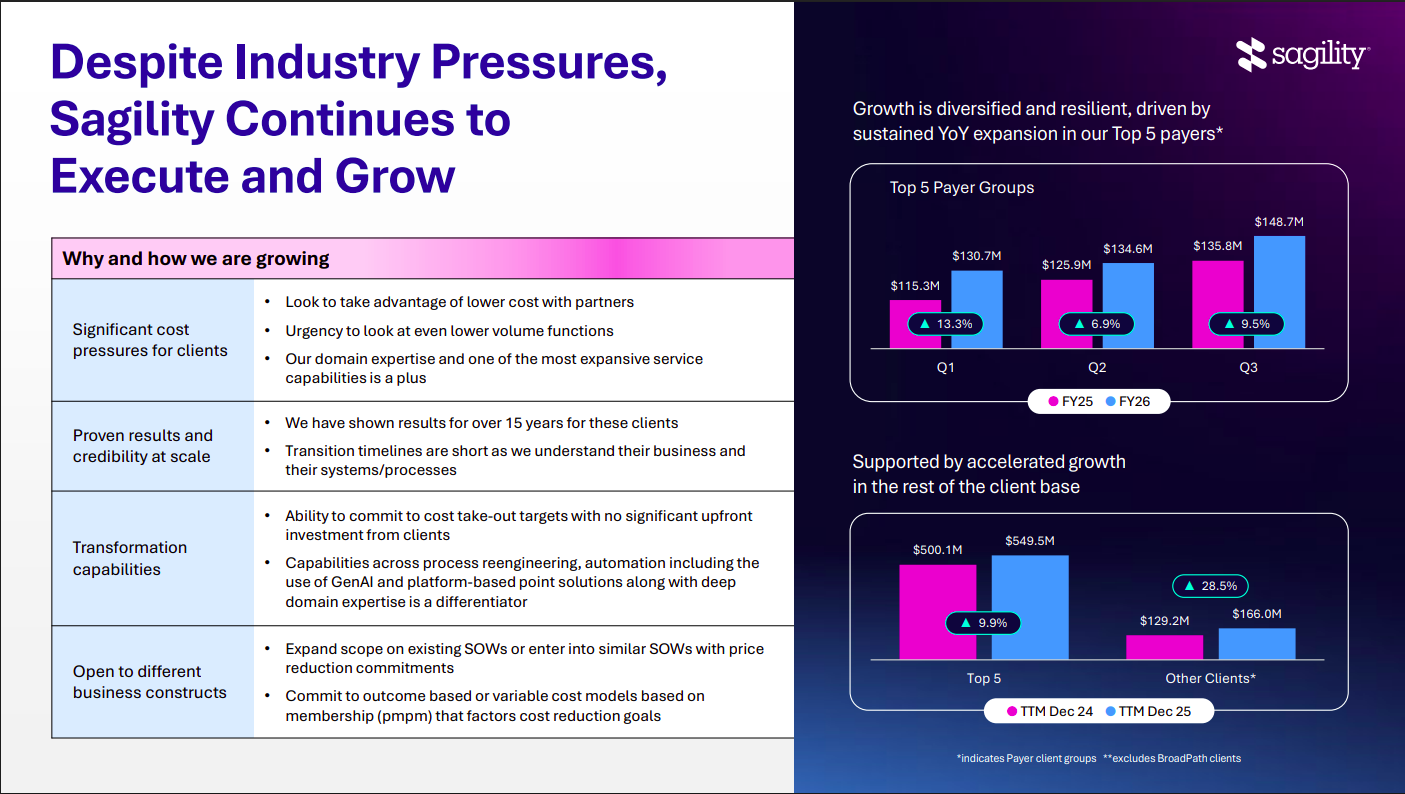

Sagility India is a pure-play healthcare focused services provider offering technology-enabled business solutions to clients in the U.S. healthcare industry. Their clientele includes Payers such as U.S. health insurance companies and Providers like hospitals, physicians, and medical devices companies.

Sagility is a scaled healthcare operations player with deep domain expertise, strong client relationships, and global delivery capabilities. Consistent growth, strong margins, and a tech-led transformation approach position it well for long-term expansion.

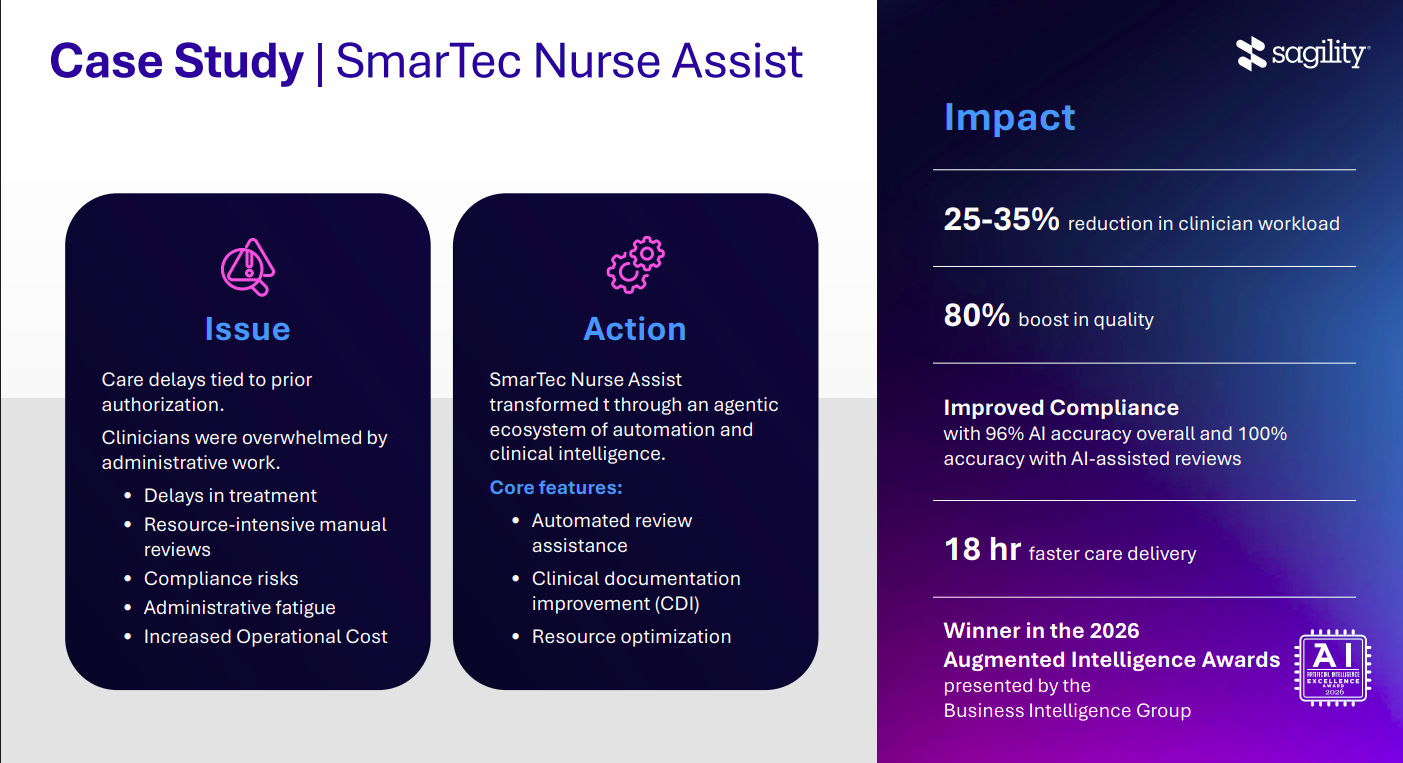

Automation-led clinical support reduced administrative burden and improved care efficiency, addressing delays from prior authorization processes. The solution delivered measurable impact with lower clinician workload, higher accuracy, and faster care delivery.

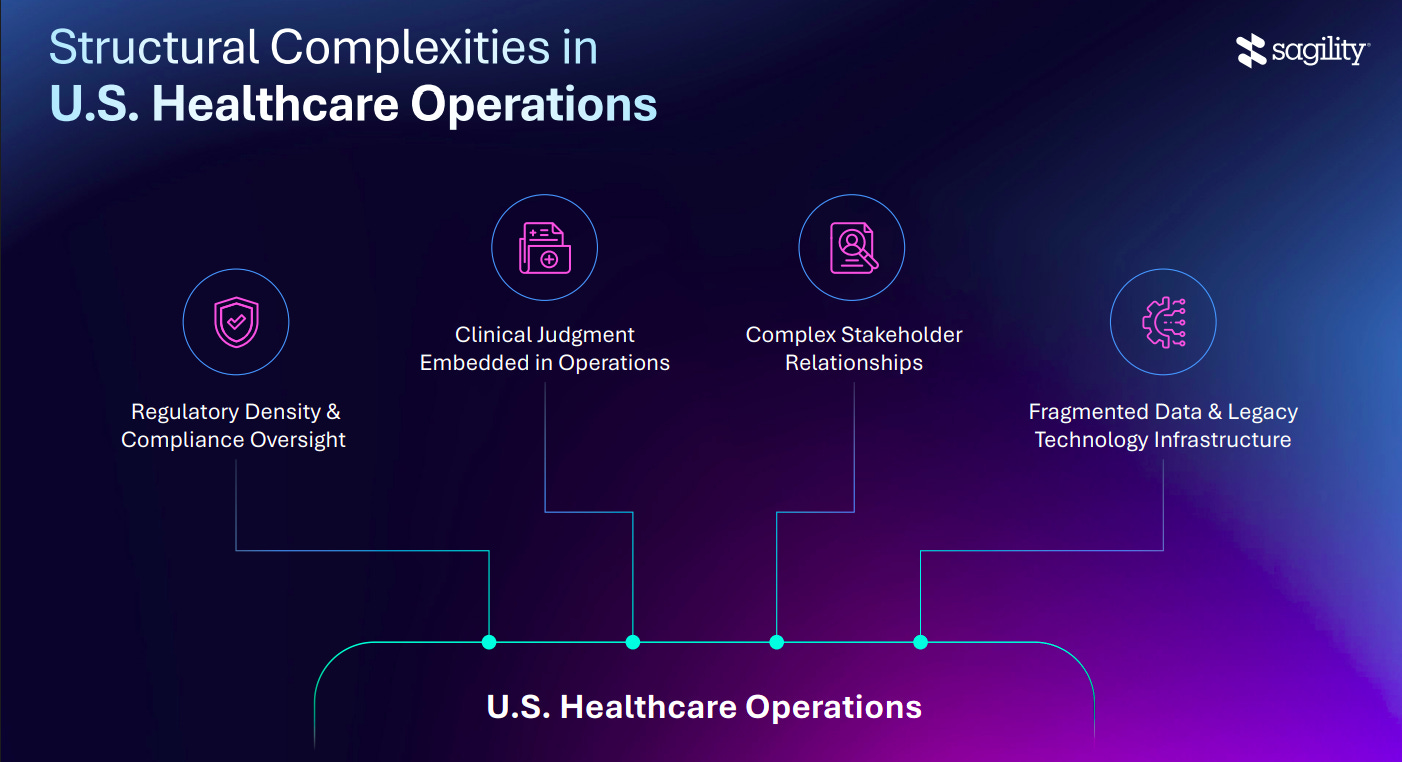

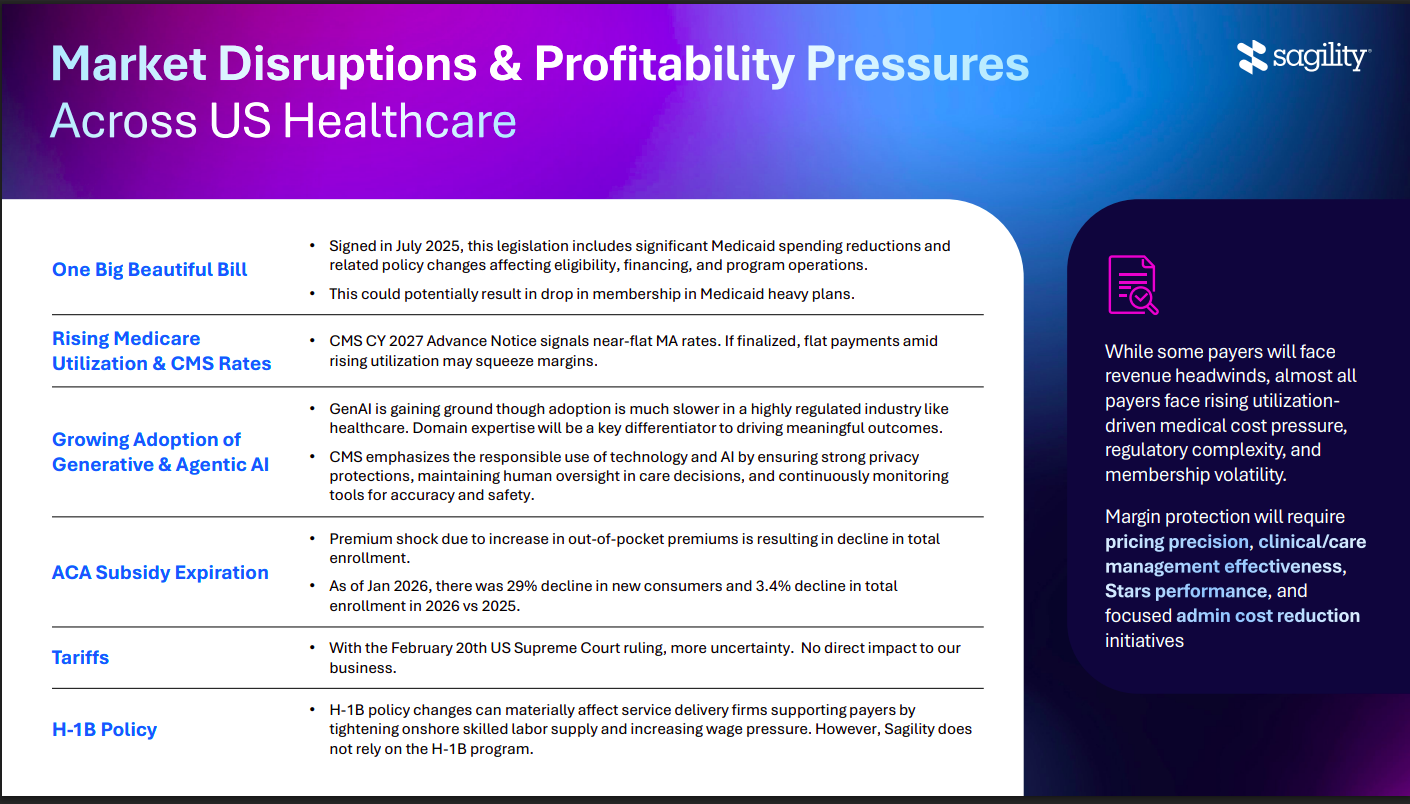

U.S. healthcare operations are inherently complex due to regulatory intensity, embedded clinical decision-making, fragmented data systems, and multiple stakeholders. These structural challenges make efficiency and automation critical.

Sagility continues to grow by leveraging cost efficiency, deep domain expertise, and long-standing client relationships. Its ability to deliver transformation-led outcomes with flexible commercial models drives sustained client expansion.

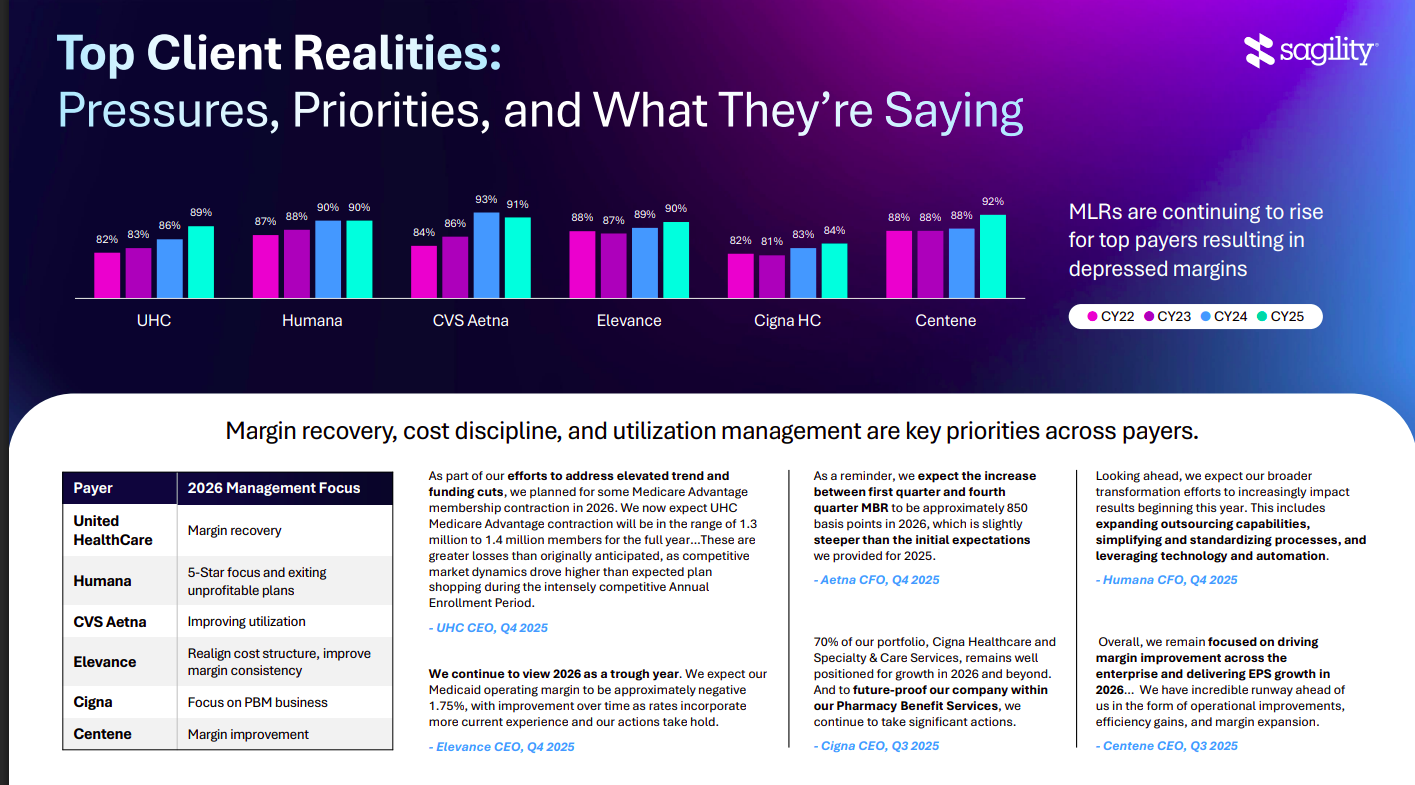

Rising medical loss ratios and cost pressures are pushing payers to prioritize margin recovery, cost discipline, and utilization management. Transformation and operational efficiency remain central themes across large clients.

Regulatory changes, rising utilization, and policy shifts are creating margin pressure across U.S. healthcare. At the same time, AI adoption, pricing discipline, and cost optimization are becoming key levers for profitability.

Building Materials

Berger Paints India Limited | Large Cap | Paints

Berger Paints is India’s second-largest paint manufacturer, providing a diverse range of decorative and industrial coating solutions. The company maintains a vast distribution network and is actively expanding its footprint in construction chemicals and home waterproofing.

Strong performance in the auto sector is currently masking muted growth in general industrial and infrastructure coatings. This concentration increases risk if car sales peak before broader industrial demand recovers.

Elevated competitive intensity signals a shift toward defending market share against new entrants. Sustained spending on branding and distribution indicates margins will remain constrained as the company prioritizes volume and reach over near-term profitability.

Diversified

3M India Limited | Large Cap | Diversified

3M India is a diversified technology company that develops science-based solutions across safety, industrial, healthcare, electronics, and consumer sectors. It operates as a subsidiary of the global 3M Company, leveraging localized manufacturing and R&D to serve the Indian market.

PBT margins rose to 19.3% as growth in higher-margin Healthcare and Consumer segments outpaced the cyclical Transportation business. This favorable mix shift improves earnings quality and reduces sensitivity to industrial cycles.

Securing technical ‘spec-ins’ at the design stage in automotive and medical sectors creates a multi-year technical moat. This deep customer integration protects future margins and ensures superior pricing power.

Expanding the Ranjangaon plant serves as a lead indicator for projected demand growth in the domestic automotive and industrial sectors. Scaling local production further optimizes logistics costs and tax efficiency.

FMCG

Varun Beverages Limited | Large Cap | Beverages

Varun Beverages is the largest franchisee for PepsiCo products outside the United States, managing a vast manufacturing and distribution network. The company operates across India and multiple African territories, leveraging a highly integrated business model to drive market share in beverages and snacks.

Aggressive expansion across Africa and a 23% volume CAGR are successfully diversifying the business beyond its Indian base. This international growth de-risks the portfolio against local weather volatility while capturing high-potential emerging markets.

Acquiring Twizza and entering the alcoholic beverage segment marks a strategic pivot to reduce long-term dependency on PepsiCo. These moves structurally evolve the company by adding higher-margin categories and non-PepsiCo brand management.

The shift to a 59% low- and no-sugar product mix reflects a strategic move toward health-conscious segments. This portfolio evolution helps mitigate future sugar tax risks while supporting long-term growth in premium categories.

Healthcare

Aurobindo Pharma Limited | Large Cap | Healthcare

Aurobindo Pharma is a global pharmaceutical leader specializing in generic formulations and Active Pharmaceutical Ingredients across several key therapeutic areas. The company maintains a significant presence in regulated markets like the US and Europe while expanding its pipeline into complex biosimilars.

Potential removal of Phase 3 trials for biosimilars structurally reduces R&D costs and capital intensity. This regulatory shift improves unit economics for scaling the company’s 15-product biologic pipeline.

A massive pipeline of 879 ANDAs provides a broad base for volume-driven revenue stability. Expanding the specialty and injectable portfolio helps protect overall margins from the price erosion typical of standard oral generics.

That’s it for now! Your feedback will really help shape how Points and Figures evolves. Drop it down in the comments below!

Quotes in this newsletter were curated by Meher & Vignesh.

Disclaimer: We’ve used AI tools in filtering and cleaning up the quotes from the images so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Points and Figures is run by the same team that creates The Daily Brief and Aftermarket Report.

Rather than sending all companies analysis in single mail, split it daily one company only so that reader will have time to read and assimilate the details and also to do further research if he wants.