Sometimes, a single slide can explain more than a long report. Points and Figures is our way of breaking down what India’s leading companies are telling their shareholders and analysts. We comb through the decks, pull out the charts and data points that actually matter, and highlight the signals behind the numbers—whether about growth plans, margins, new markets, or risks on the horizon.

This is an extension of The Chatter. While The Chatter focuses on management commentary and earnings call transcripts, Points and Figures dives into investor presentations—and soon, even annual reports—to decode what companies are showing, not just what they’re saying.

We go through every major investor presentation so you don’t have to—bringing you the sharpest takeaways that reveal not just what the company is saying, but what it really means for the business, its sector, and the broader economy.

In this edition, we have covered 15 companies across 8 industries.

Financial Services

Piramal Finance

SBI Cards and Payment Services Limited

Auto

Maruti Suzuki India Limited

Sona BLW Precision

India Nippon Electricals Ltd

FMCG

Zydus Wellness

Shri Gang Industries & Allied Products

Godfrey Phillips India Limited

Metals

MOIL Limited

Trading

Shiv Texchem

Engineering & Capital Goods

Gala Precision Engineering

Oriental Rail Infrastructure Limited

KEI Industries Limited

Healthcare

Aster DM Healthcare Limited

Real Estate

Prestige Estates

Financial Services

Piramal Finance | Mid Cap | Financial Services

Piramal Finance provides easy access to affordable Housing Finance to realise home-ownership aspirations of millions of Lower and Middle income families in semi-urban and rural India.

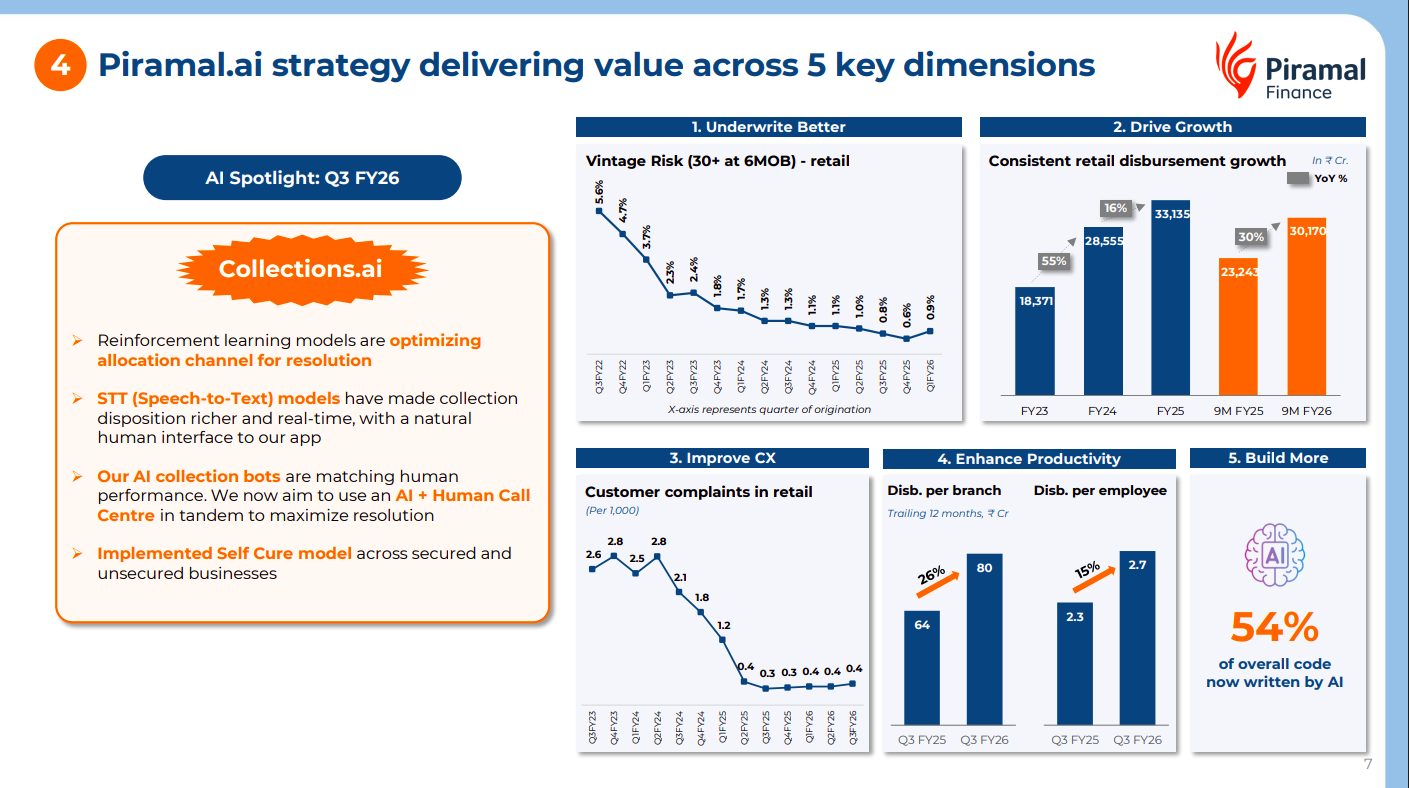

Piramal is integrating AI across underwriting, collections, customer experience, and productivity. Tools like Collections.ai, reinforcement learning models, and speech-to-text systems are improving resolution rates, reducing complaints, boosting disbursement productivity, and enabling AI to generate 54% of internal code.

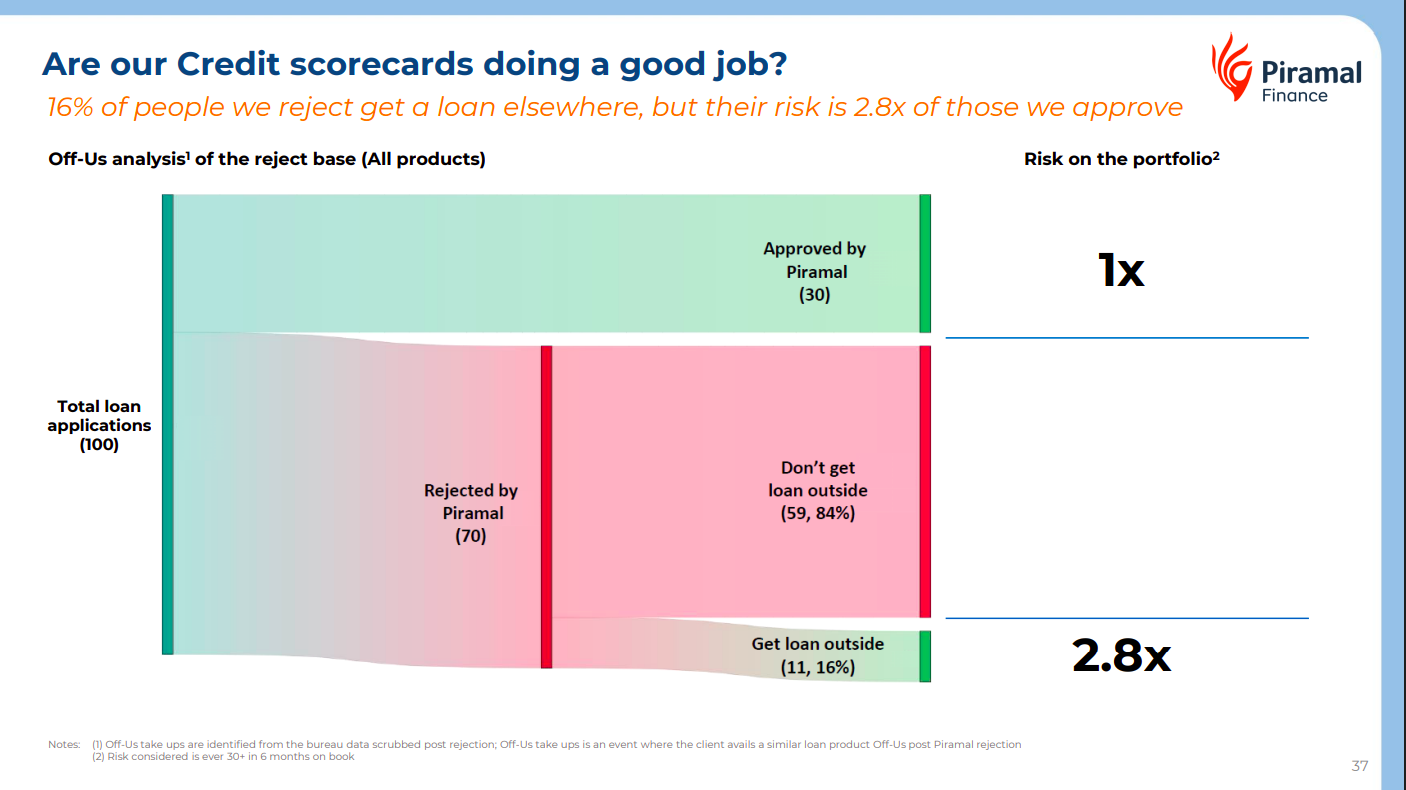

Piramal’s credit scorecards appear effective as only 16% of rejected applicants secure loans elsewhere, and those borrowers show 2.8x higher risk than approved customers. This indicates the company’s underwriting filters are successfully identifying and avoiding higher-risk borrowers.

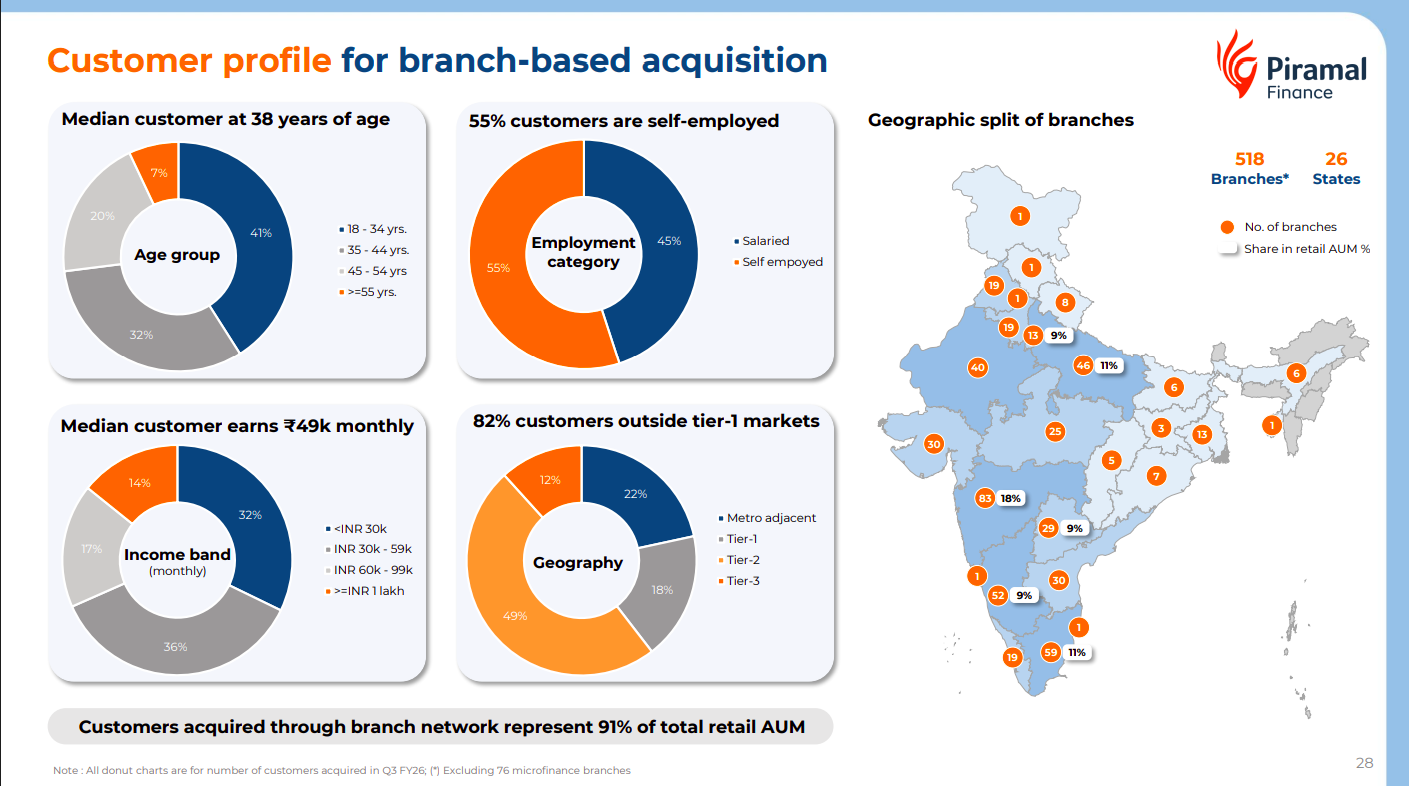

The typical Piramal customer is around 38 years old, earning ~₹49K monthly, with 55% self-employed borrowers. About 82% of customers come from non-tier-1 markets, highlighting the company’s strong focus on semi-urban and emerging markets through its 518-branch network across 26 states.

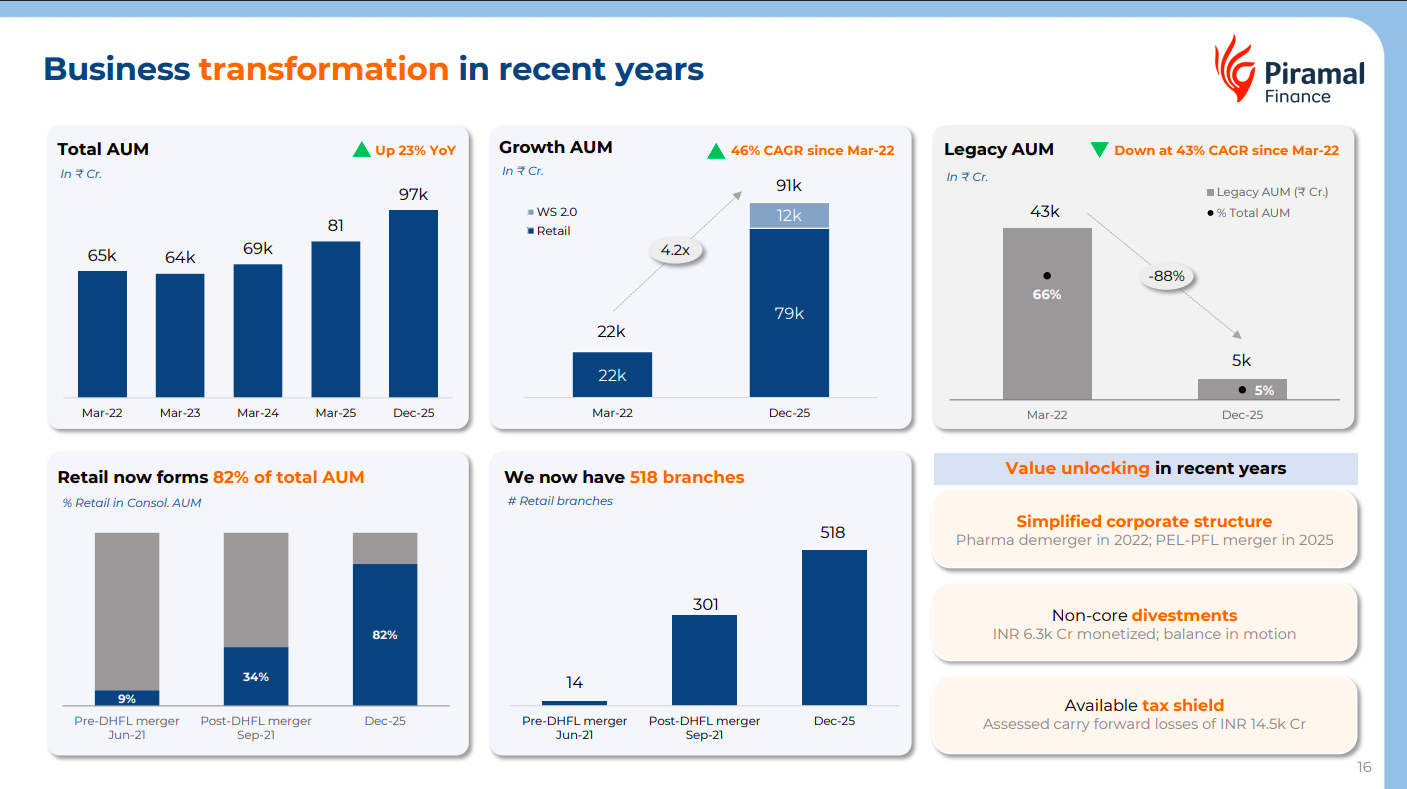

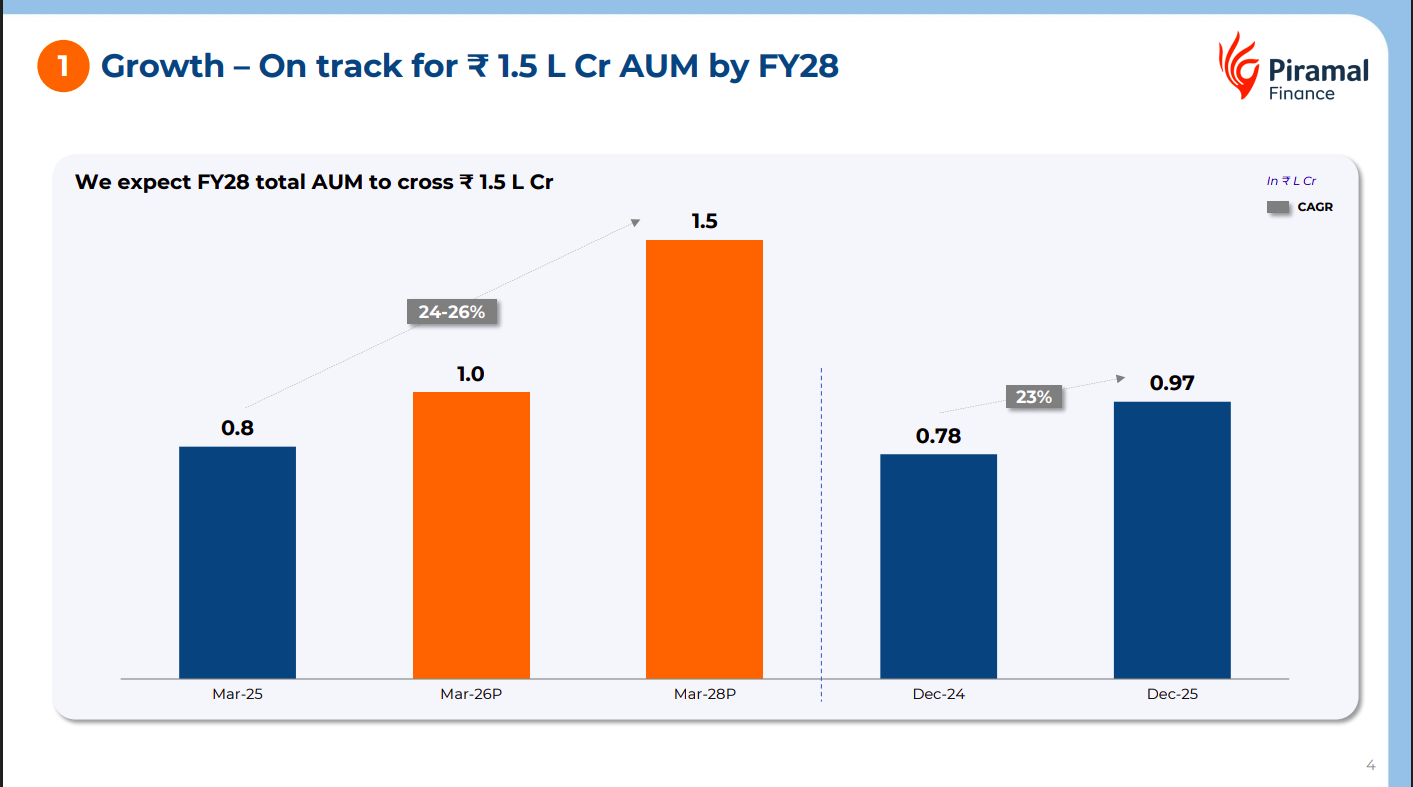

Piramal Finance has significantly transformed its portfolio, with total AUM rising to ₹97K crore (+23% YoY) while legacy AUM has sharply reduced. Retail lending now accounts for 82% of total AUM, supported by rapid branch expansion and strategic restructuring initiatives.

The company aims to reach ₹1.5 lakh crore AUM by FY28, implying a 24–26% CAGR from FY25 levels. Recent momentum shows AUM already growing 23% YoY, indicating the company is broadly on track to meet this growth target.

SBI Cards and Payment Services Limited | Large Cap | Financial Services - Credit Cards

SBI Cards is India’s leading pure-play credit card issuer, offering a wide array of lifestyle and rewards-based products. The company leverages its parent State Bank of India’s massive network for efficient customer acquisition and scale.

A stable revolver mix alongside rising transactor shares indicates card usage is shifting toward convenience rather than borrowing. While this reduces credit risk, it increases reliance on fee-based income to offset capped interest upside.

Rapid UPI spend growth on RuPay cards, especially in Tier 2+ cities, establishes a massive growth vector in small-ticket merchant payments. This expanded digital footprint creates an efficient acquisition funnel for higher-margin credit products.

Spend market share is rebounding significantly faster than card-in-force share, signaling higher transaction intensity. This trend suggests a higher-quality user base that is less prone to inactivity risks.

Auto

Maruti Suzuki India Limited | Large Cap | Auto

Maruti Suzuki is India’s largest passenger vehicle manufacturer, commanding a dominant market share through an extensive distribution network and diverse product range. The company is currently executing a massive capacity expansion plan to double production by 2030 while transitioning its portfolio toward hybrids and electric vehicles.

Doubling production to 4 million units by 2030 reflects a massive bet on India’s structural demand growth. This scale-up is designed to secure a pre-emptive advantage over both domestic and global rivals.

Massive middle-class expansion is shifting the market toward aspirational ownership, moving beyond basic utility. Growth now hinges on capturing these higher-ticket buyers to improve overall profitability.

Reaching the $3,500 income inflection point signals a looming surge in car ownership mirroring China’s historical growth. This environment favors the manufacturer with the largest scale and most aggressive capacity rollout.

India’s low vehicle penetration of 30 per 1,000 people relative to global peers highlights a multi-decade structural growth runway. This massive gap suggests long-term demand will rise steadily as per capita incomes increase.

Sales volumes are shifting decisively from the entry-level Mini segment toward Compacts and SUVs. This shift reflects a favorable product mix evolution that generally supports higher unit economics and margin expansion.

The 2025 GST revision acts as a catalyst for entry-level demand by narrowing the price gap with premium motorcycles. Restoring momentum in this segment is crucial for recharging the customer funnel and maintaining dominant market share.

The rise of SUV market share to nearly 55% reflects a permanent shift toward premium lifestyle choices among Indian buyers. Capturing this high-margin segment is critical to protecting long-term returns as the legacy small-car market matures.

Implementing Battery-as-a-Service and 60% assured buybacks directly addresses consumer concerns regarding high upfront costs and resale value. These aggressive financial measures are vital for securing early EV adopters while charging infrastructure matures.

Sona BLW Precision | Mid Cap | Auto Ancillary

Sona Comstar is a leading global mobility technology company specializing in designing, manufacturing, and supplying precision-forged components like bevel gears, differential case assemblies, and motors for electrified and non-electrified powertrains. It serves automotive and other industries with high-quality, mission-critical systems and bespoke solutions.

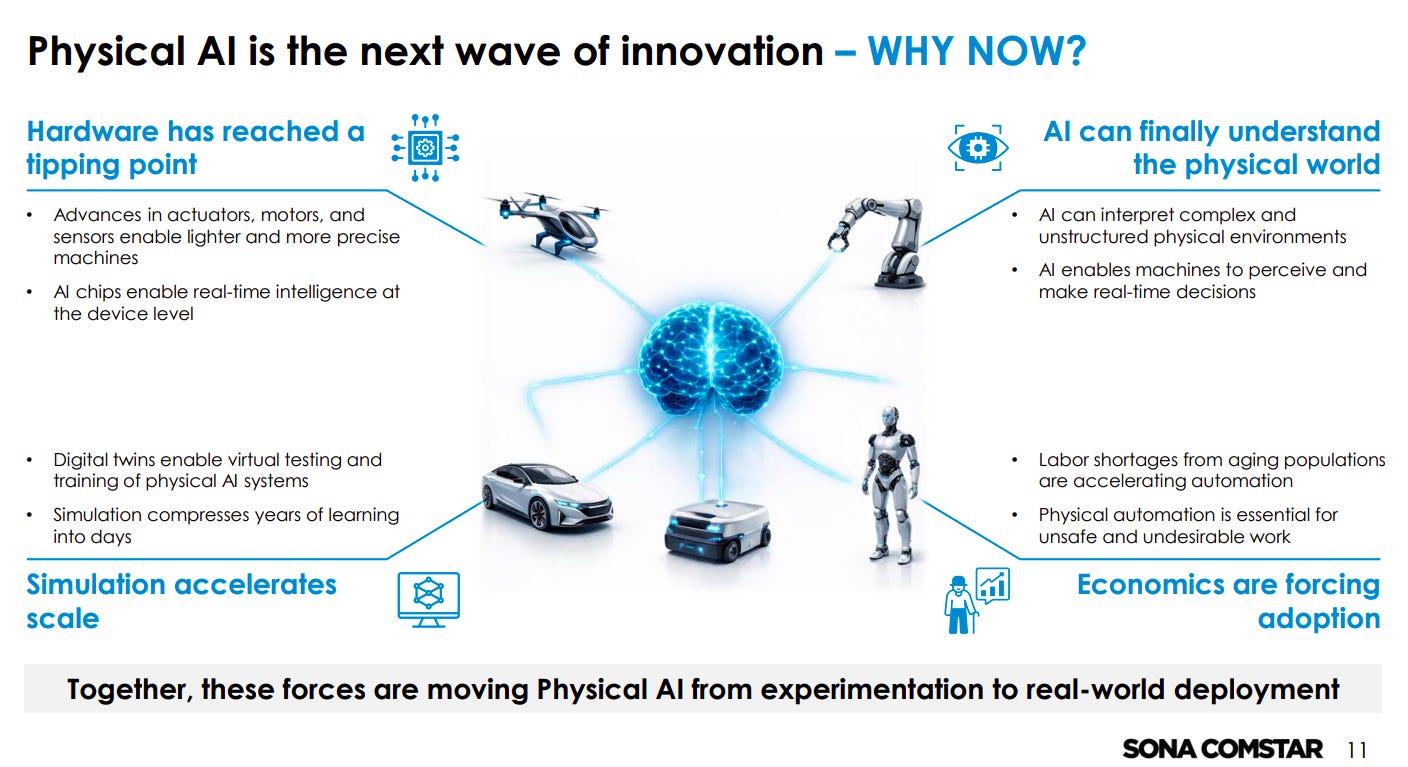

Physical AI is reaching an inflection point driven by advances in hardware (sensors, actuators, AI chips), improved simulation capabilities, and real-time AI perception. At the same time, labor shortages and automation needs are accelerating adoption, pushing Physical AI from experimentation to real-world deployment.

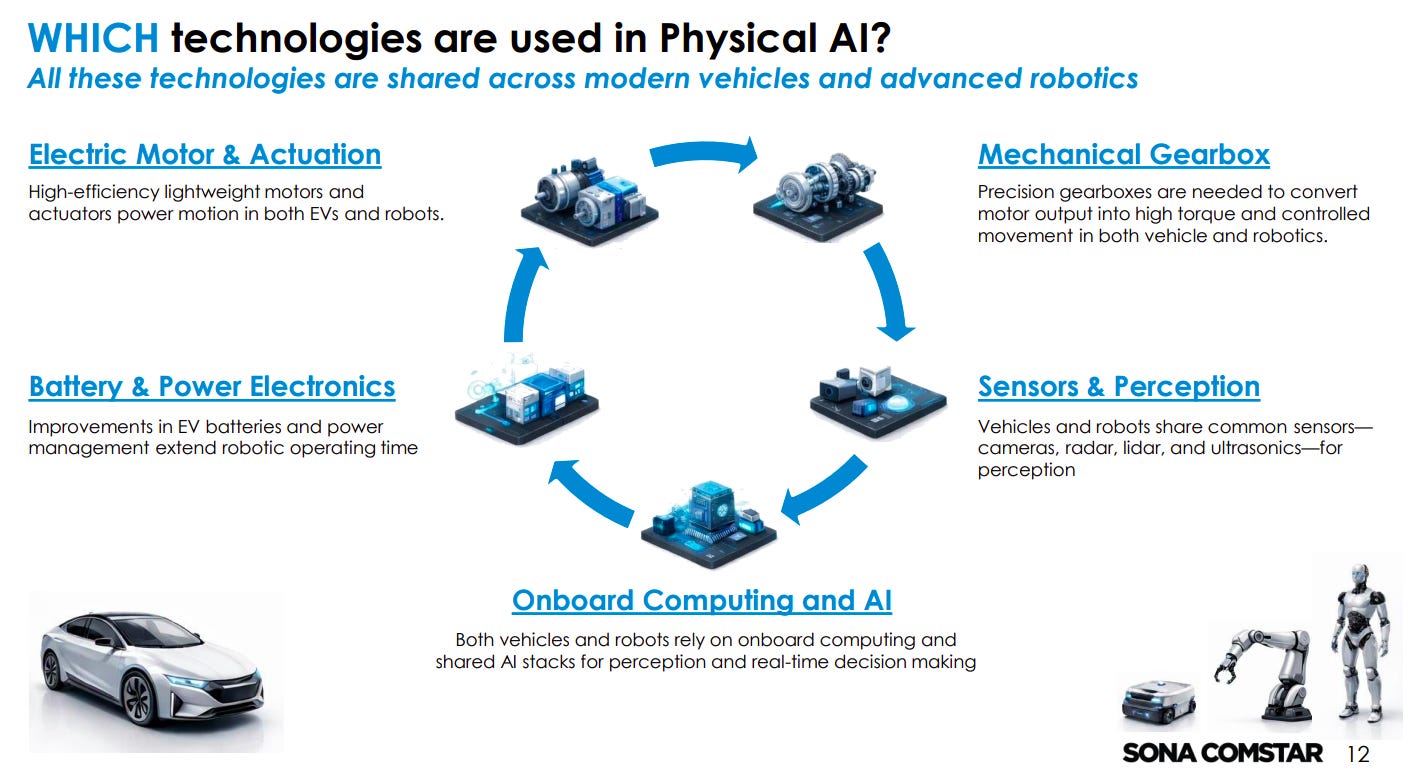

Physical AI relies on a stack of motors & actuation, gearboxes, sensors, batteries, and onboard AI computing, all common across EVs and robotics. These components work together to enable movement, perception, power management, and real-time decision-making.

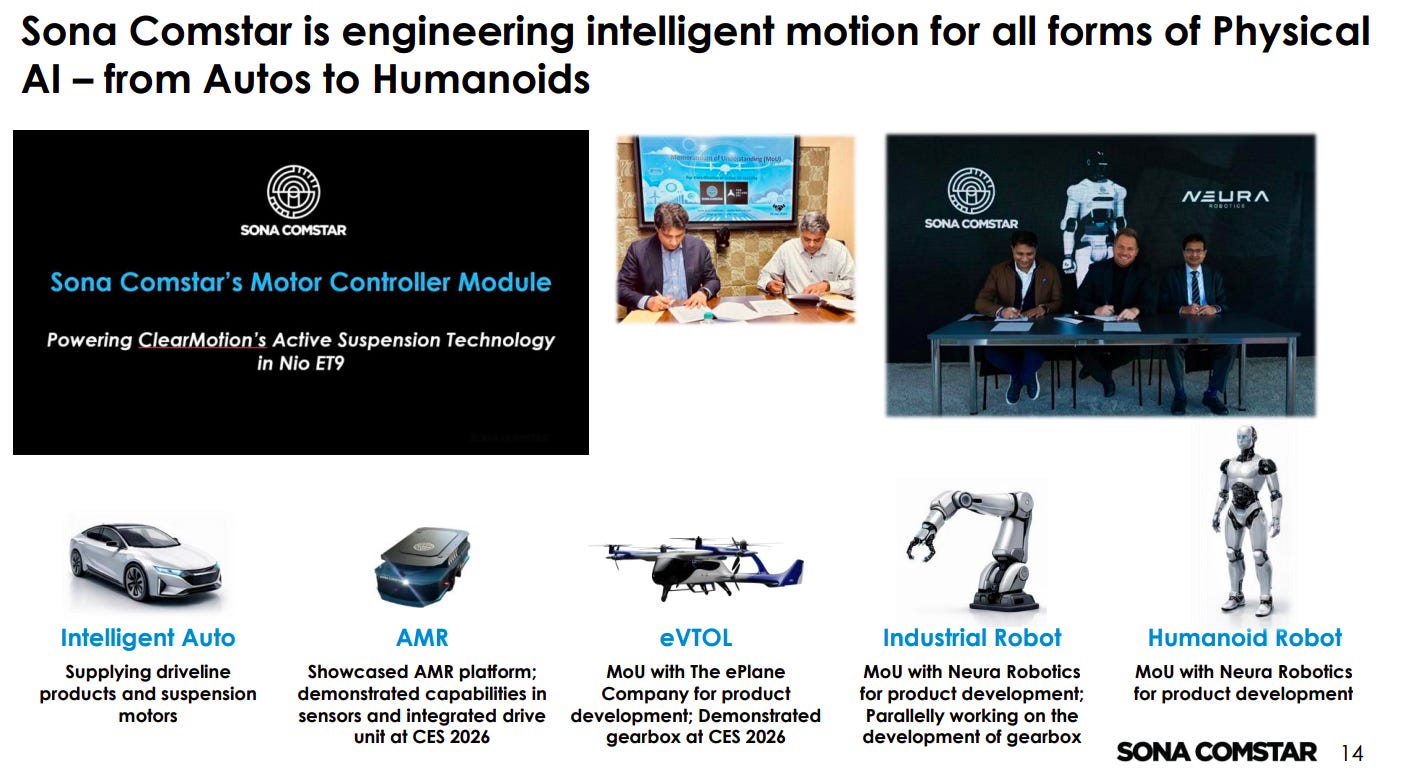

Sona Comstar is positioning itself as a motion and drivetrain enabler across multiple Physical AI applications, including EVs, drones, robots, and humanoids. The company is expanding through partnerships, product development, and showcasing capabilities (e.g., CES 2026).

The company has consistently evolved its strategy—from EV-focused expansion to adding sensors/software, entering railways, and now robotics. This reflects a stepwise transition from auto components to broader mobility and Physical AI ecosystems.

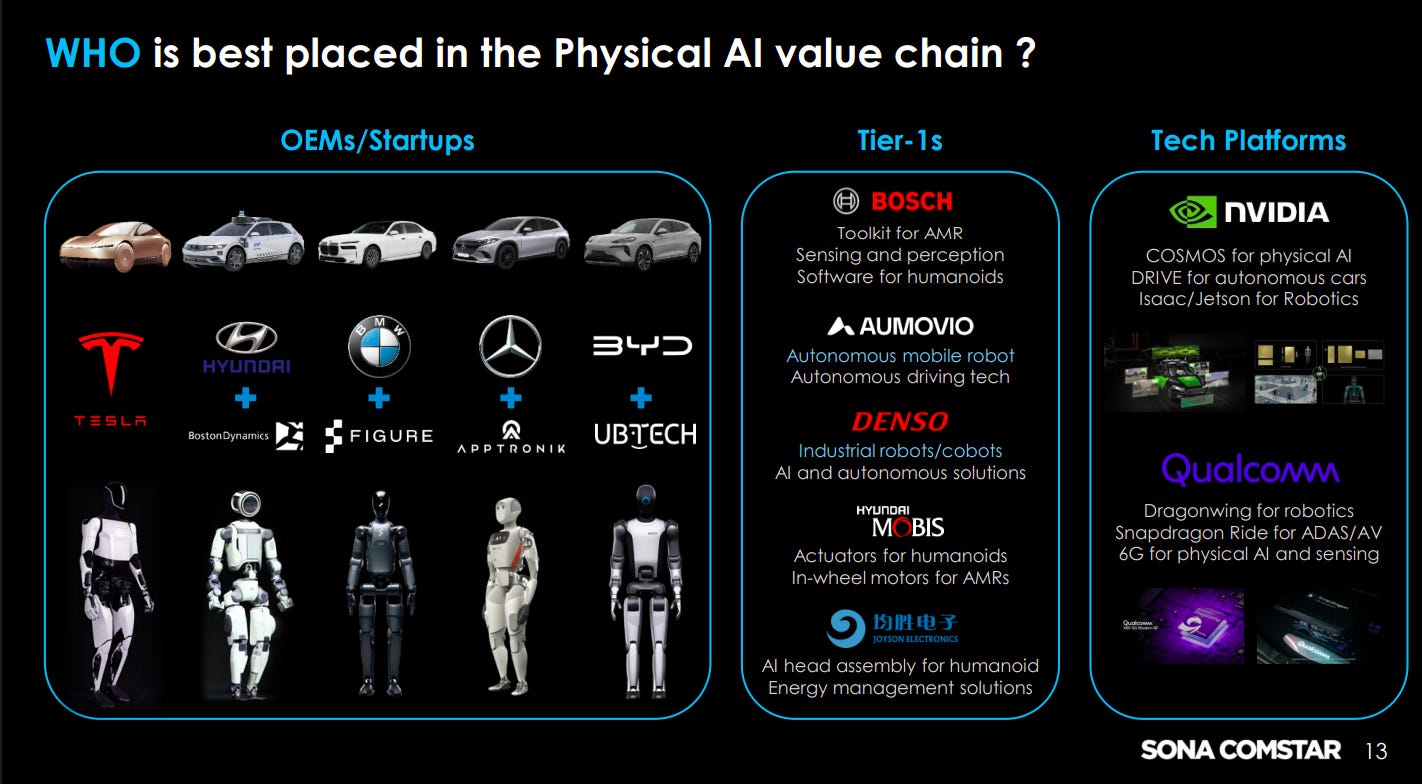

The Physical AI ecosystem spans OEMs/startups (Tesla, BYD, humanoid firms), Tier-1 suppliers (Bosch, Denso), and tech platforms (NVIDIA, Qualcomm). Value creation is distributed across hardware, software, and systems integration, with multiple players competing across layers.

India Nippon Electricals Ltd | Small Cap | Auto Ancillary

India Nippon Electricals Ltd is a leading manufacturer of electronic ignition systems and powertrain components for two-wheelers and three-wheelers. A joint venture with Japan’s Kokusan Denki, the company is actively expanding its portfolio into sensors and electric vehicle controllers.

Domestic revenue concentration at 96% ties company performance strictly to Indian two-wheeler cycles and local policy shifts. This lack of geographic diversity limits valuation upside from global supply chain diversification.

Consistently outgrowing the industry average indicates increasing market share and deeper technical integration with major OEMs. Sustaining this performance requires high R&D intensity to maintain a competitive advantage in the evolving electronic components segment.

The company is positioning itself to capture high growth in the automotive sensor market through increased R&D in electronic solutions for both ICE and electric vehicles. Localization trends and ‘China Plus One’ strategies provide significant tailwinds for scaling production.

FMCG

Zydus Wellness | Small Cap | FMCG

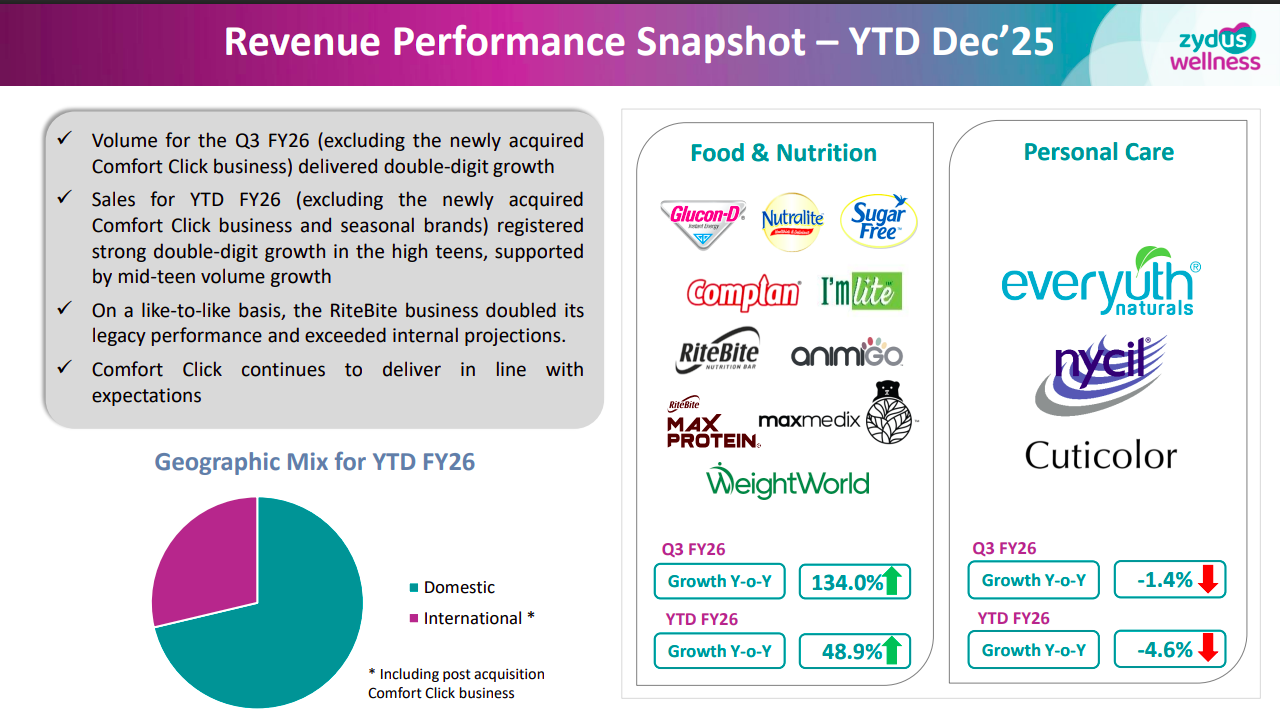

Zydus Wellness Limited offers healthcare, nutrition, and cosmeceutical products to promote well-being. They focus on developing and distributing a wide range of health and wellness products under popular brands like Glucon-D, Complan, Sugar Free, Nycil, Everyuth, and Nutralite, aiming to help people achieve integrated well-being.

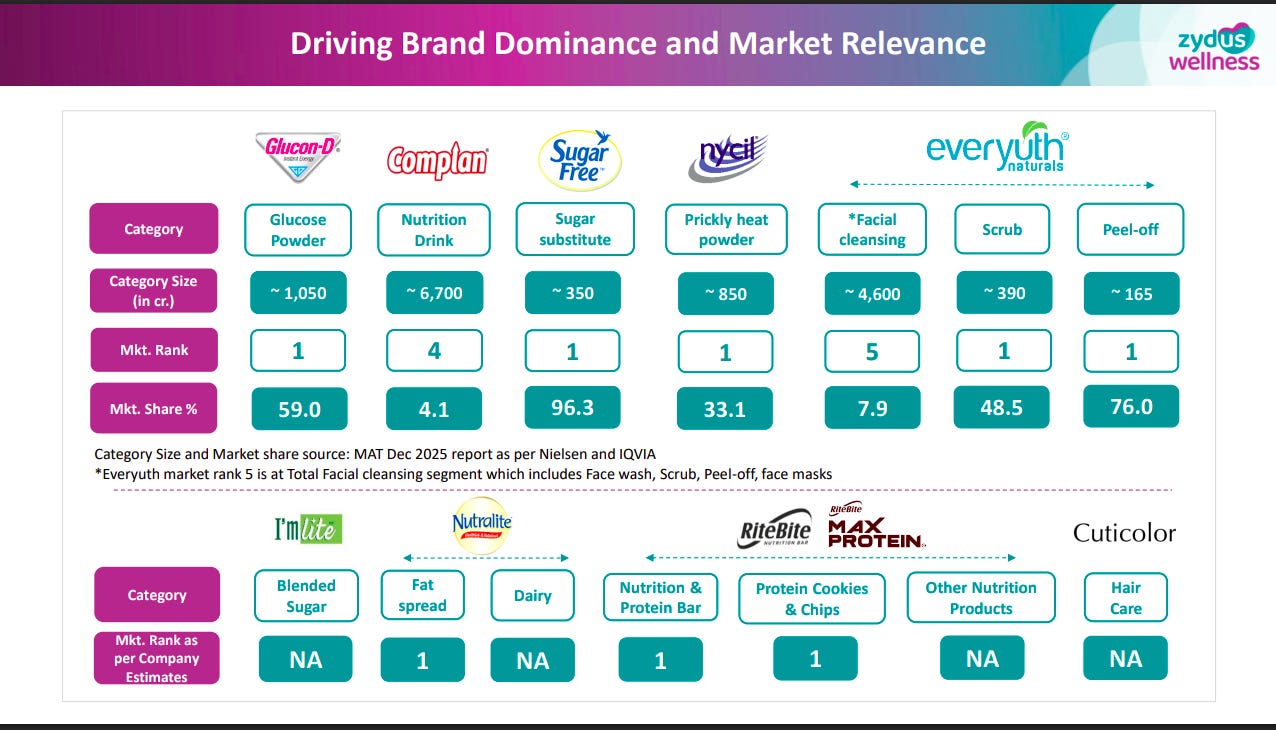

Complan is rebuilding relevance through a core refresh, new user acquisition (toddlers), and adult nutrition expansion. Despite a modest 4.1% market share, the brand is repositioning with relaunches to tap evolving nutrition needs.

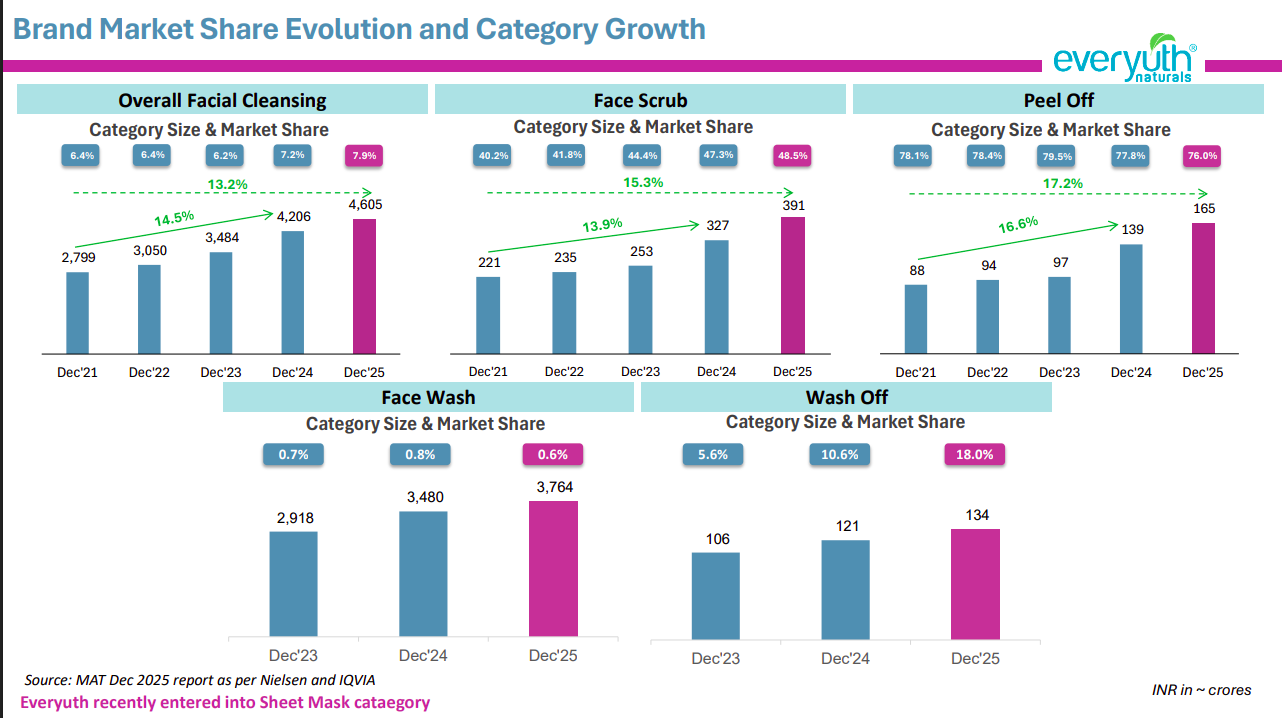

Everyuth continues to lead in high-growth niches like scrubs (48.5%) and peel-offs (76%), while scaling presence in overall facial cleansing (~7.9% share). Categories are expanding at 13–17% CAGR, indicating strong tailwinds in naturals-led skincare.

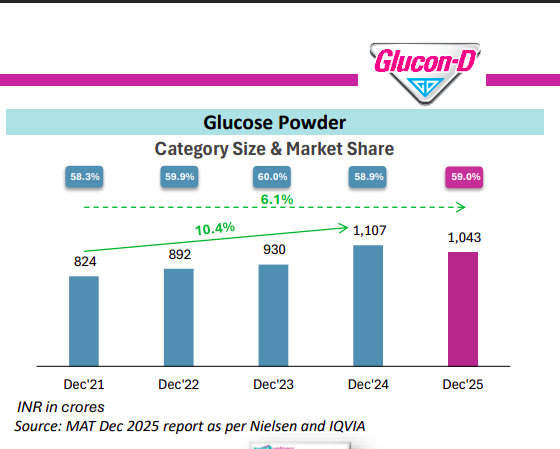

Glucon-D remains a dominant category leader (~59% share) in glucose powders, with steady category expansion (~6% growth). While growth moderated in FY25, leadership position remains intact.

Zydus Wellness has built a diversified portfolio of category leaders—#1 positions in glucose, sugar substitutes, scrubs, and peel-offs. Personal care (Everyuth) is emerging as a high-growth adjacency alongside core nutrition brands.

Food & Nutrition is driving growth with strong double-digit YTD growth (~49%), led by brands like RiteBite and Complan. In contrast, Personal Care remains weak, showing slight declines, indicating a near-term drag on overall performance.

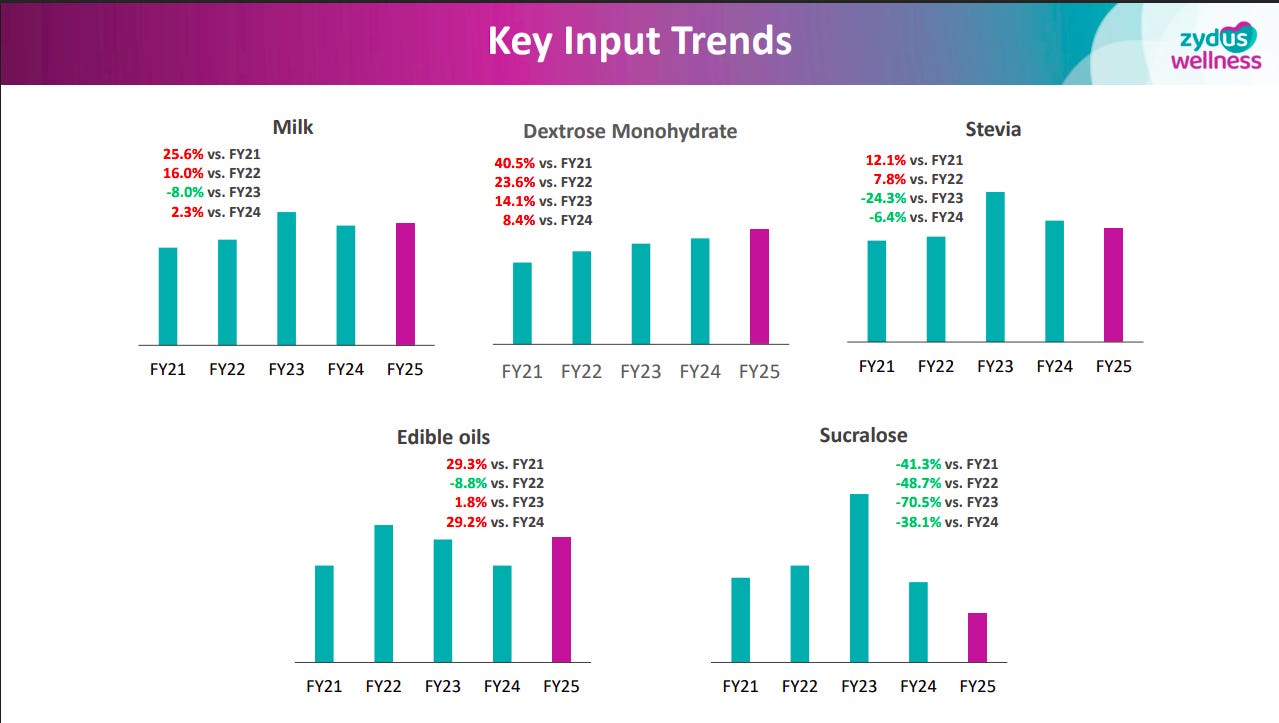

Input costs remain volatile—milk, dextrose, and edible oils saw inflation spikes, while sucralose prices corrected sharply. This mixed cost environment has implications for margin recovery and pricing strategies.

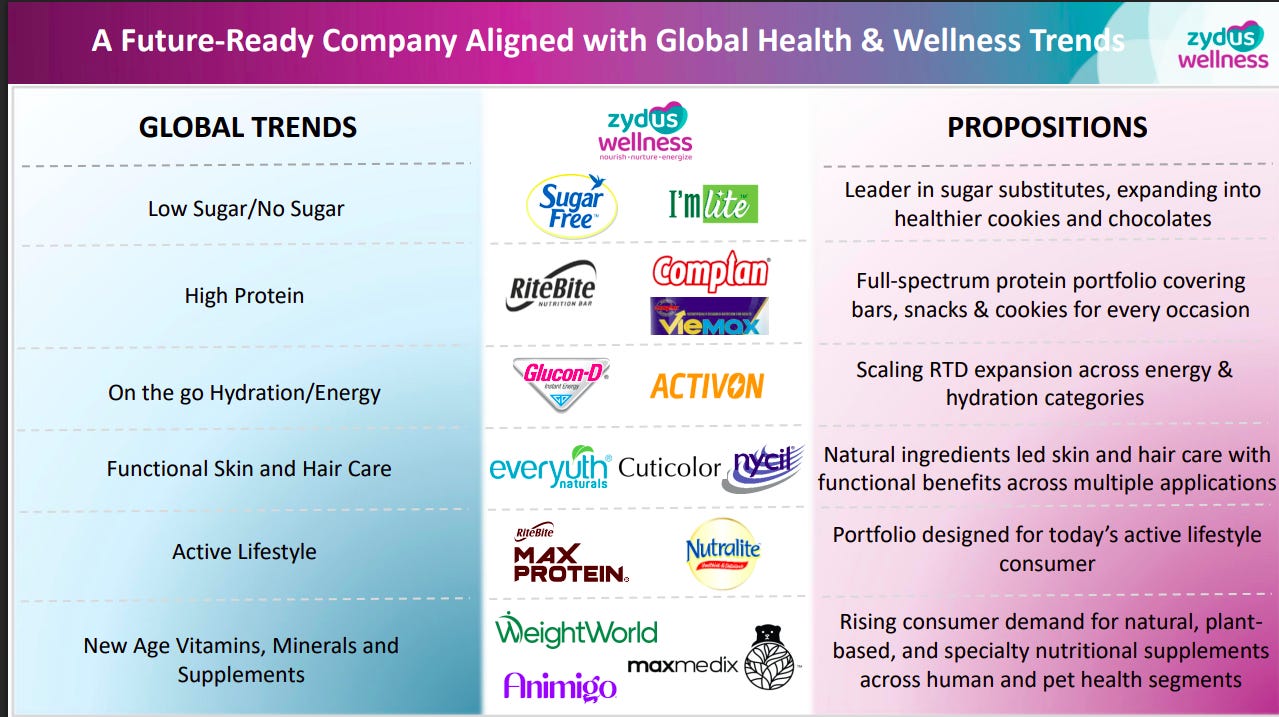

Zydus is aligning with structural trends like low sugar, high protein, functional nutrition, and natural personal care. The strategy focuses on premiumization, portfolio expansion, and tapping health-conscious consumption across categories.

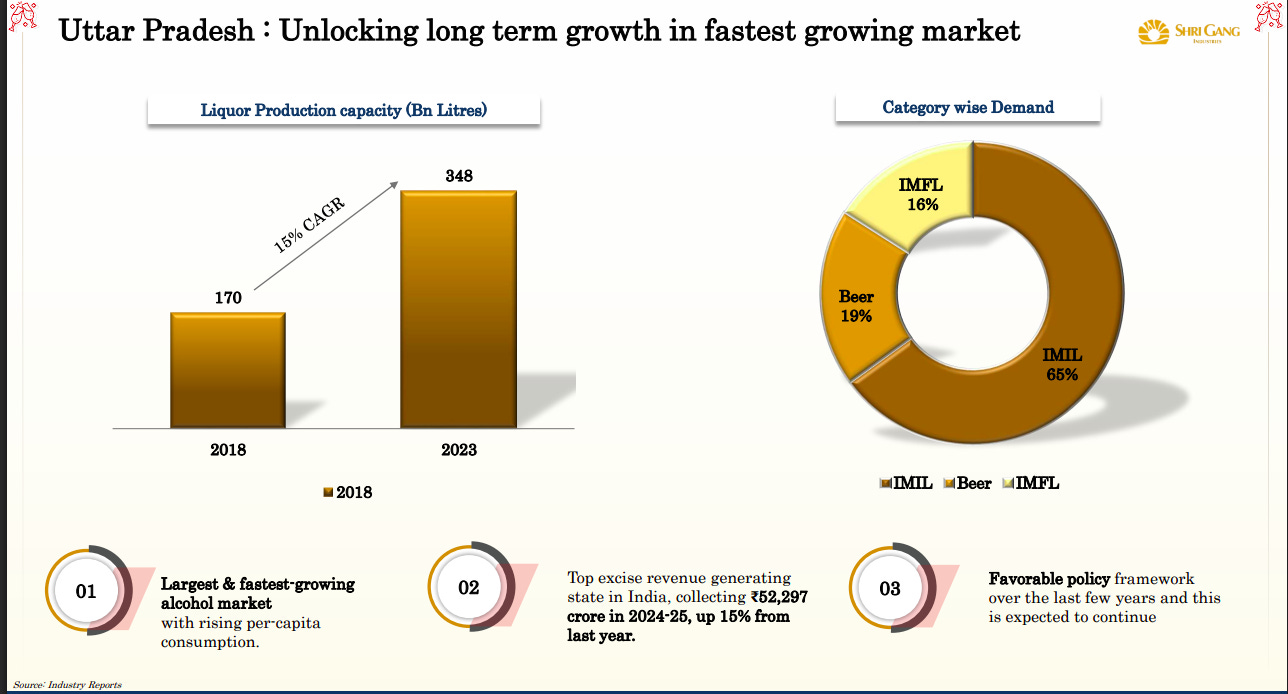

Shri Gang Industries & Allied Products | Nano Cap | FMCG

Shri Gang Industries and Allied Products Limited engages in the manufacture and sale of vanaspati, refined oils, and bakery shortenings. The company offers its products under the ‘Apna’ and ‘Mr. Baker’ brand names. The company markets its products primarily in the state of Uttar Pradesh in India.

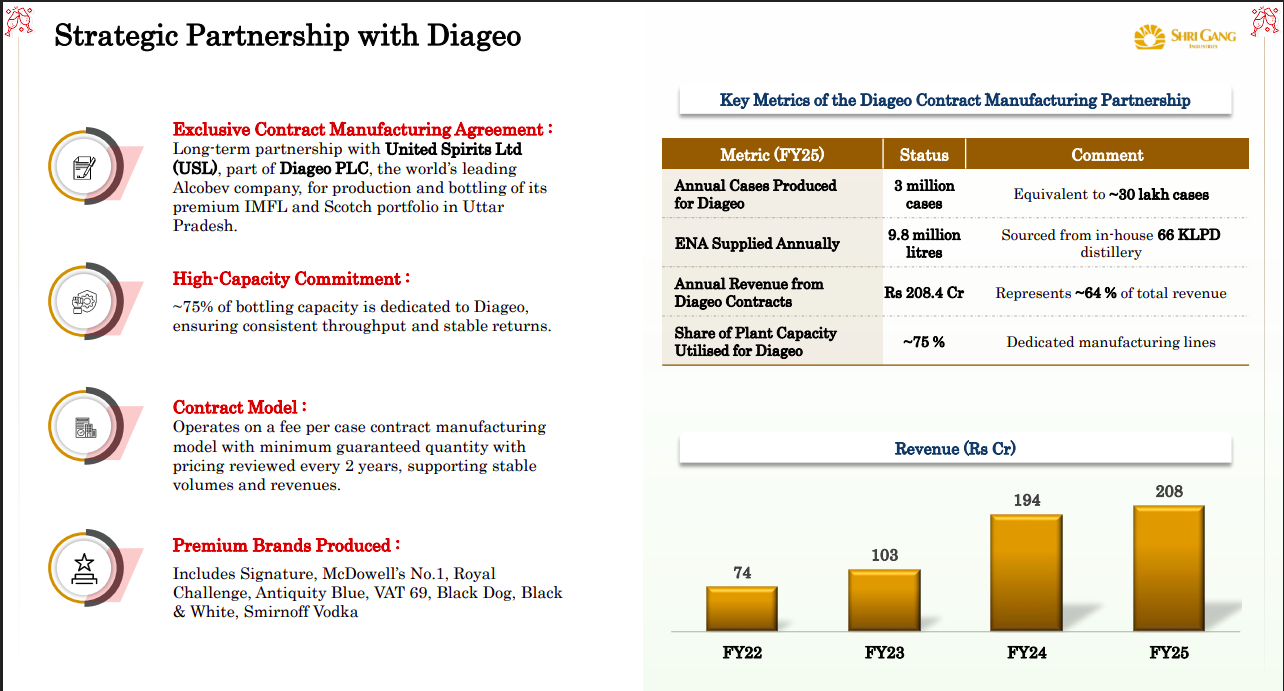

Shri Gang Industries has a long-term, exclusive contract manufacturing tie-up with Diageo (USL), anchoring its business with stable, high-volume demand. ~75% of capacity is dedicated to Diageo, with a fee-based model and minimum guarantees, driving predictable revenues and strong utilization.

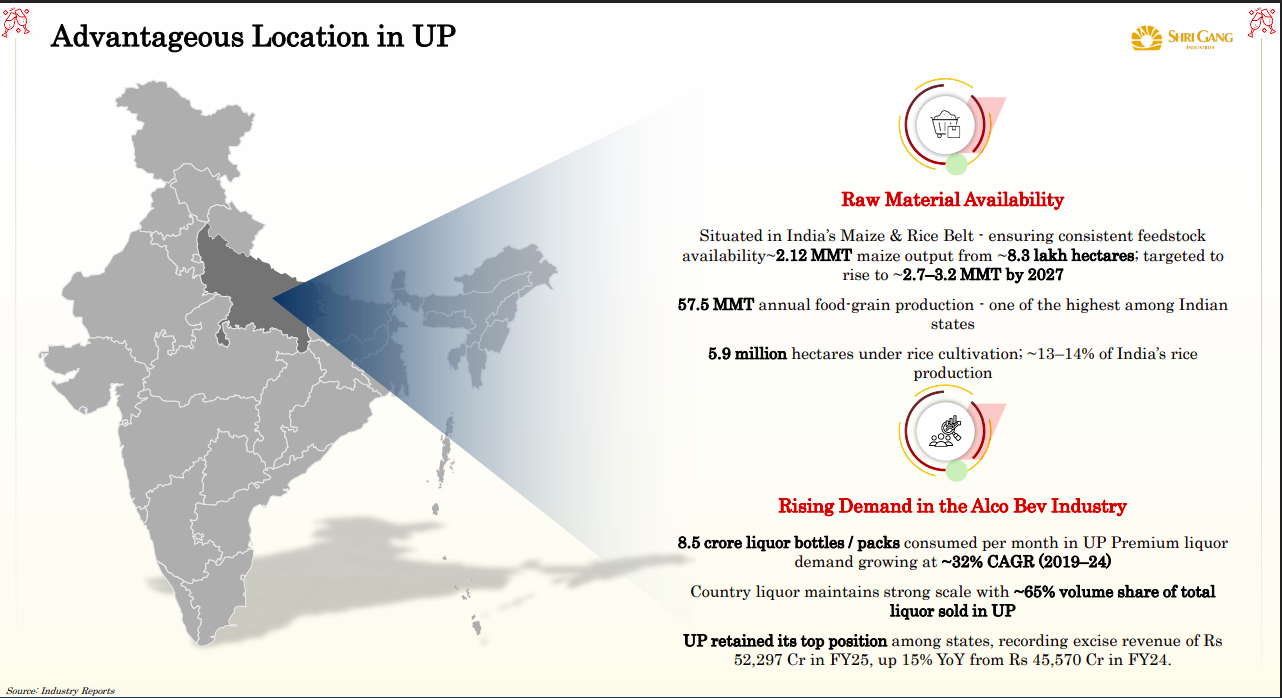

UP is India’s largest and fastest-growing liquor market, with production capacity growing at ~15% CAGR and strong excise-led policy support. IMIL dominates (~65% share), but premiumization (IMFL + beer) is steadily rising, creating a multi-layer demand expansion opportunity.

The company benefits from a strategic location in India’s key maize and rice belt, ensuring reliable and cost-efficient feedstock access. Coupled with strong demand growth (~32% CAGR in premium segments), this creates a structural advantage in both input sourcing and end-market consumption.

Godfrey Phillips India Limited | Mid Cap | Tobacco Products

Godfrey Phillips India is a major tobacco manufacturer with a diversified portfolio spanning cigarettes, unmanufactured tobacco exports, and confectionery items. The company operates through flagship brands and an exclusive partnership with Philip Morris International to distribute Marlboro in India.

Tobacco accounts for 99% of sales, concentrating regulatory and excise tax risks. This dependency makes cash flows vulnerable to policy changes despite the company’s strong pricing power.

Exports now contribute 23% of revenue, acting as a strategic hedge against domestic regulatory volatility. The segment leverages low production costs to build resilient, dollar-linked revenue streams.

Monthly cigarette volumes reached 2.1 billion, a massive structural scale-up from 775 million five years ago. This growth confirms successful brand penetration and a shift toward organized tobacco.

Metals

MOIL Limited | Small Cap | Metals

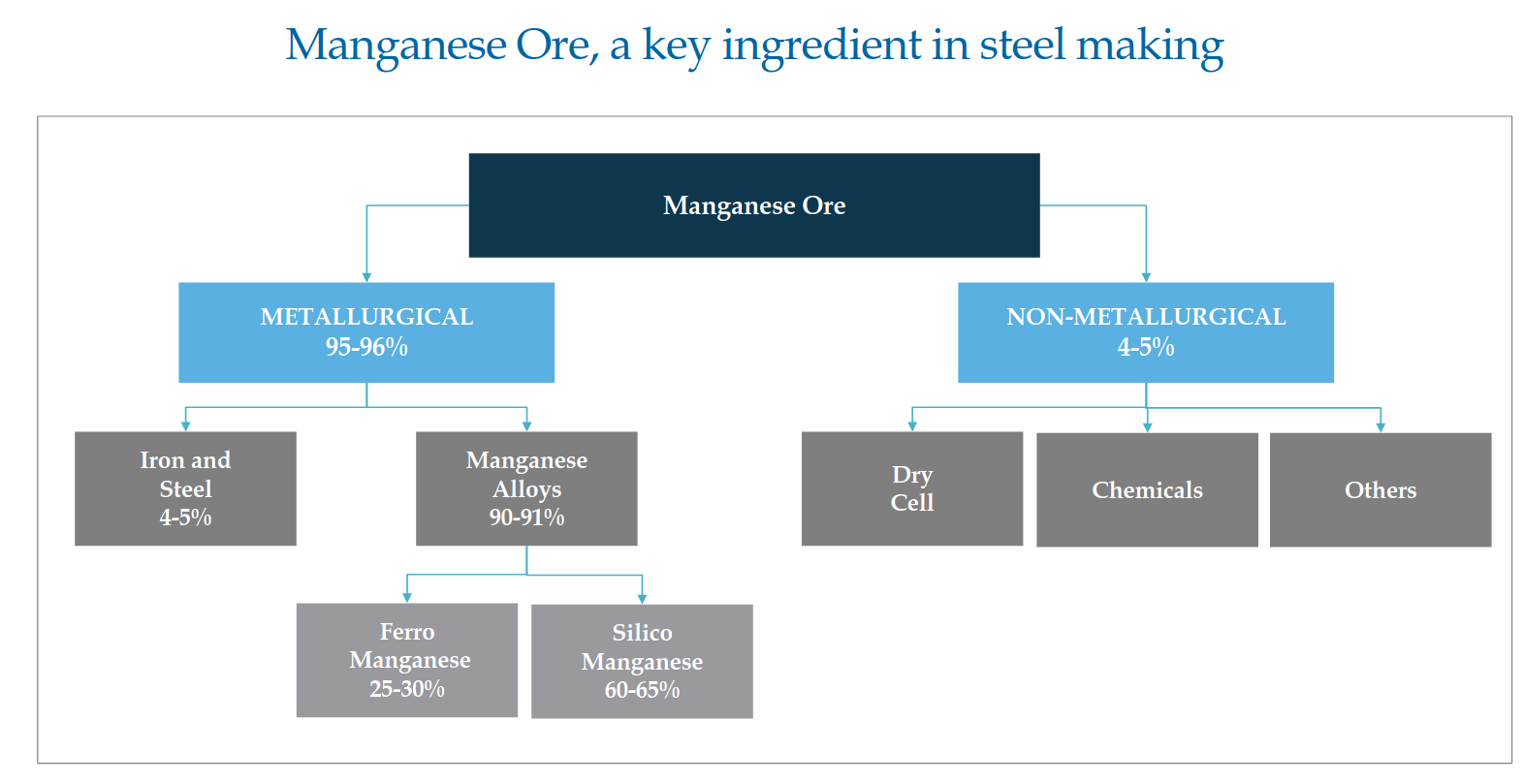

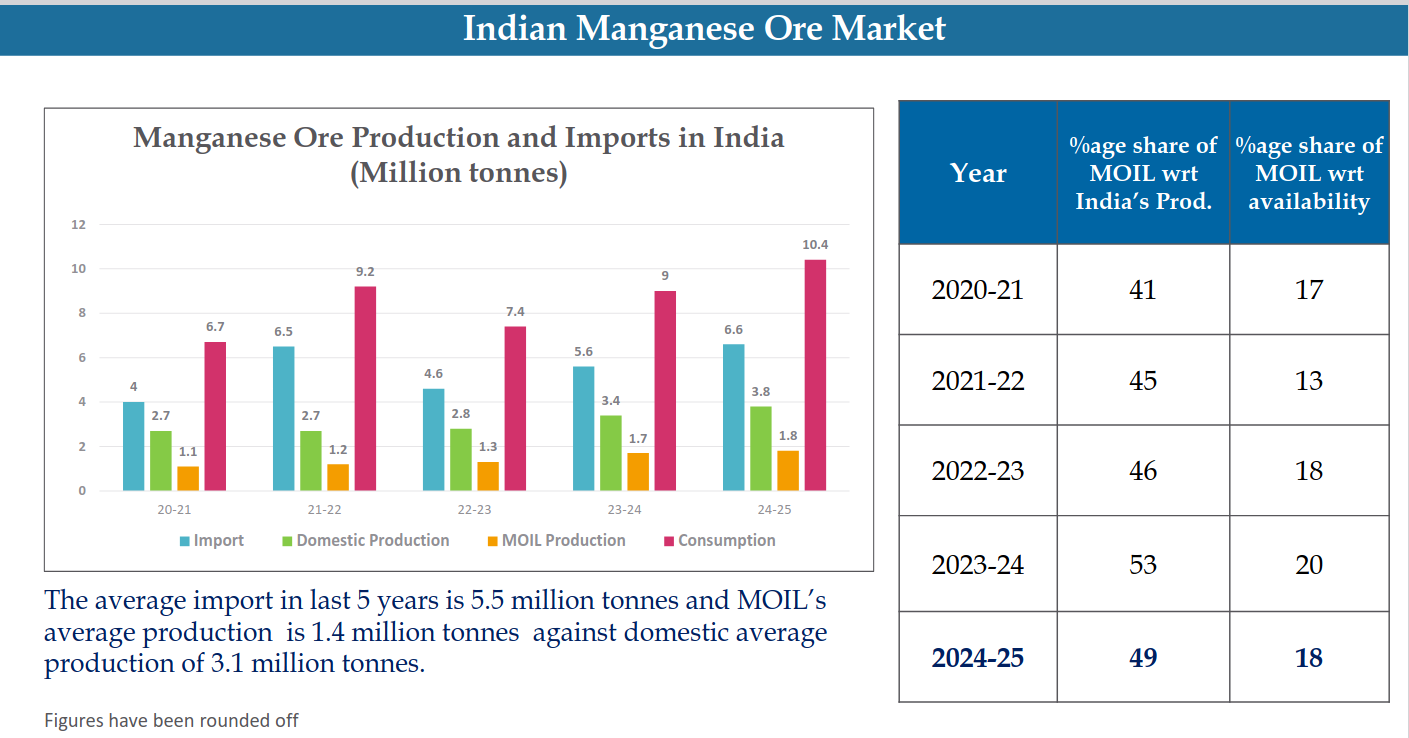

MOIL Limited, a Schedule ‘A’ Miniratna Category-I Company, is a leading producer of different grades of Manganese Ore in India. Their product range includes High Grade Ores, Medium grade ore, Blast furnace grade ore, and Dioxide for various industries. MOIL fulfills half of India’s dioxide ore requirement and has also ventured into renewable energy with wind farms in Madhya Pradesh.

~95–96% of manganese demand is metallurgical (steel & alloys), with ferro and silico manganese forming the bulk of consumption. This makes the sector a direct proxy on steel cycle and infrastructure demand.

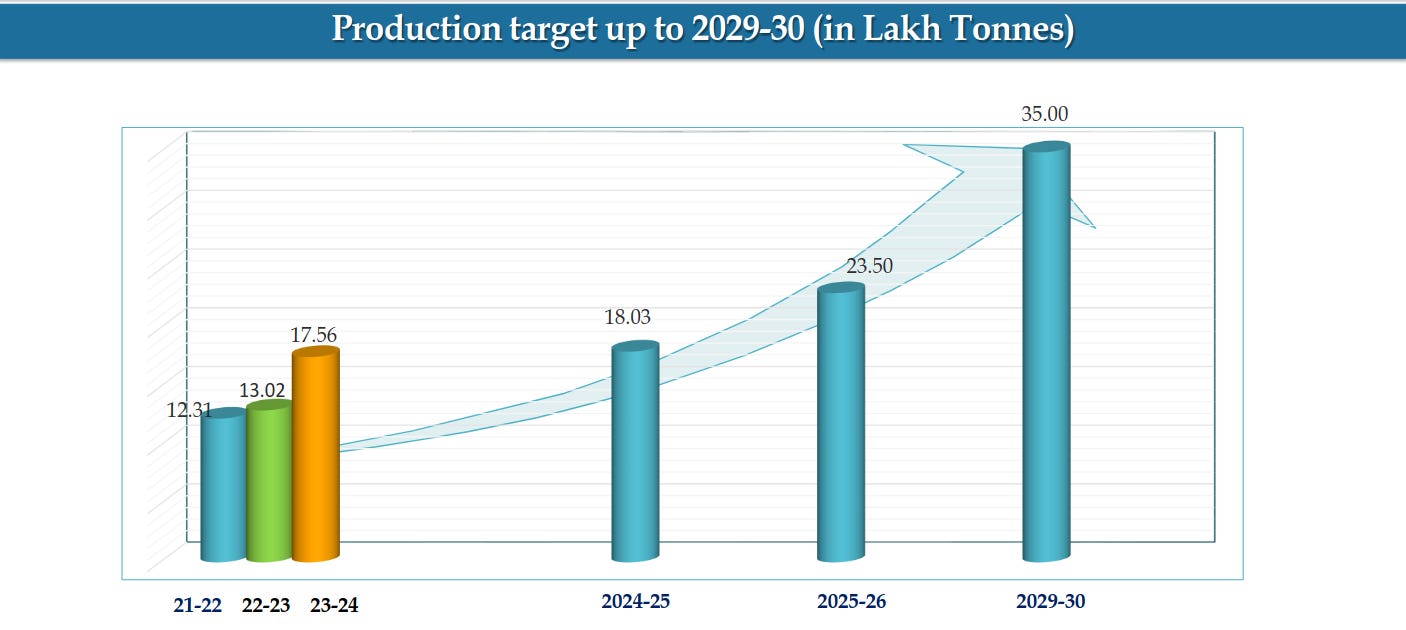

India’s manganese ore production is targeted to scale from ~12–18 lakh tonnes historically to 35 lakh tonnes by FY30, implying a strong ramp-up trajectory. This reflects capacity expansion and rising domestic demand visibility, likely driven by steel and alloy consumption.

India remains structurally import-dependent (~5.5 MT average imports) despite steady domestic production growth. MOIL dominates domestic supply (~45–53% share), but the gap between consumption and production highlights a persistent supply deficit.

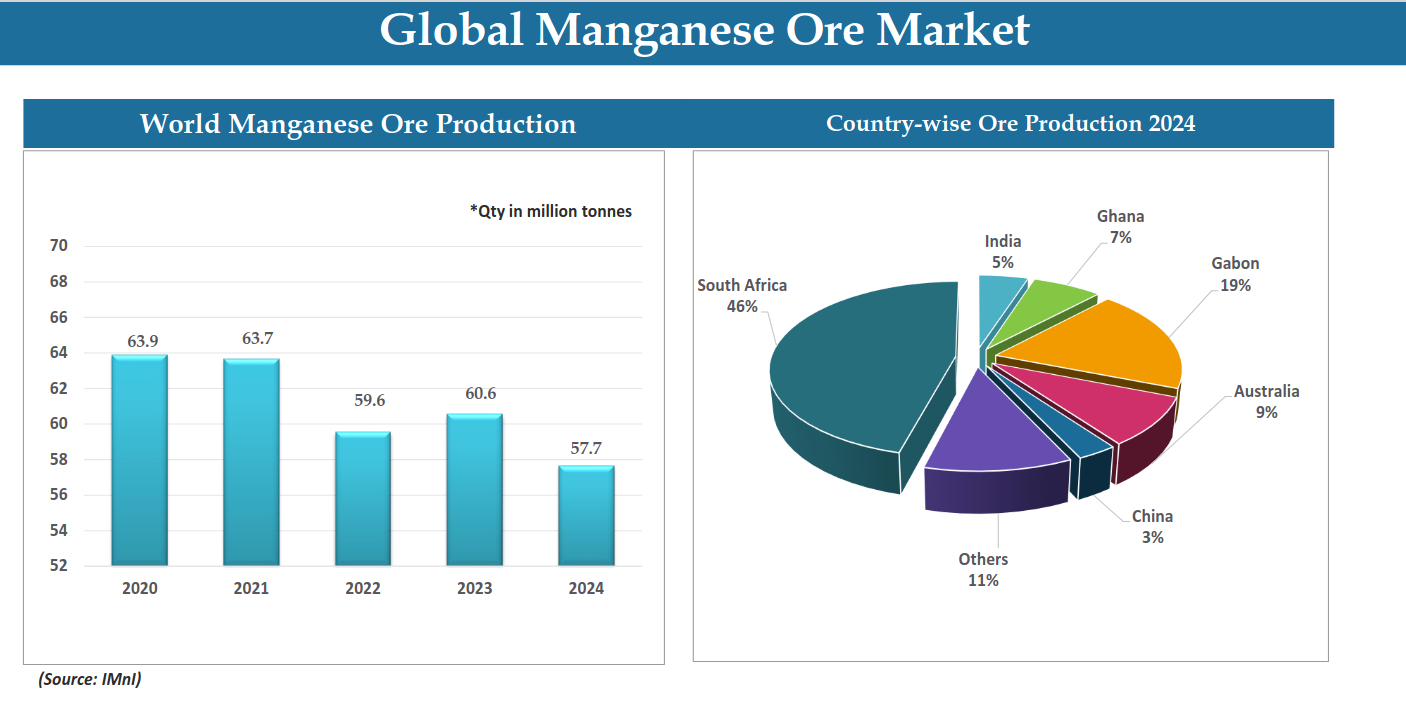

Global manganese supply is highly concentrated, with South Africa (~46%) and Gabon (~19%) dominating production, while India contributes only ~5%. This concentration creates supply-side risks and pricing power cycles globally.

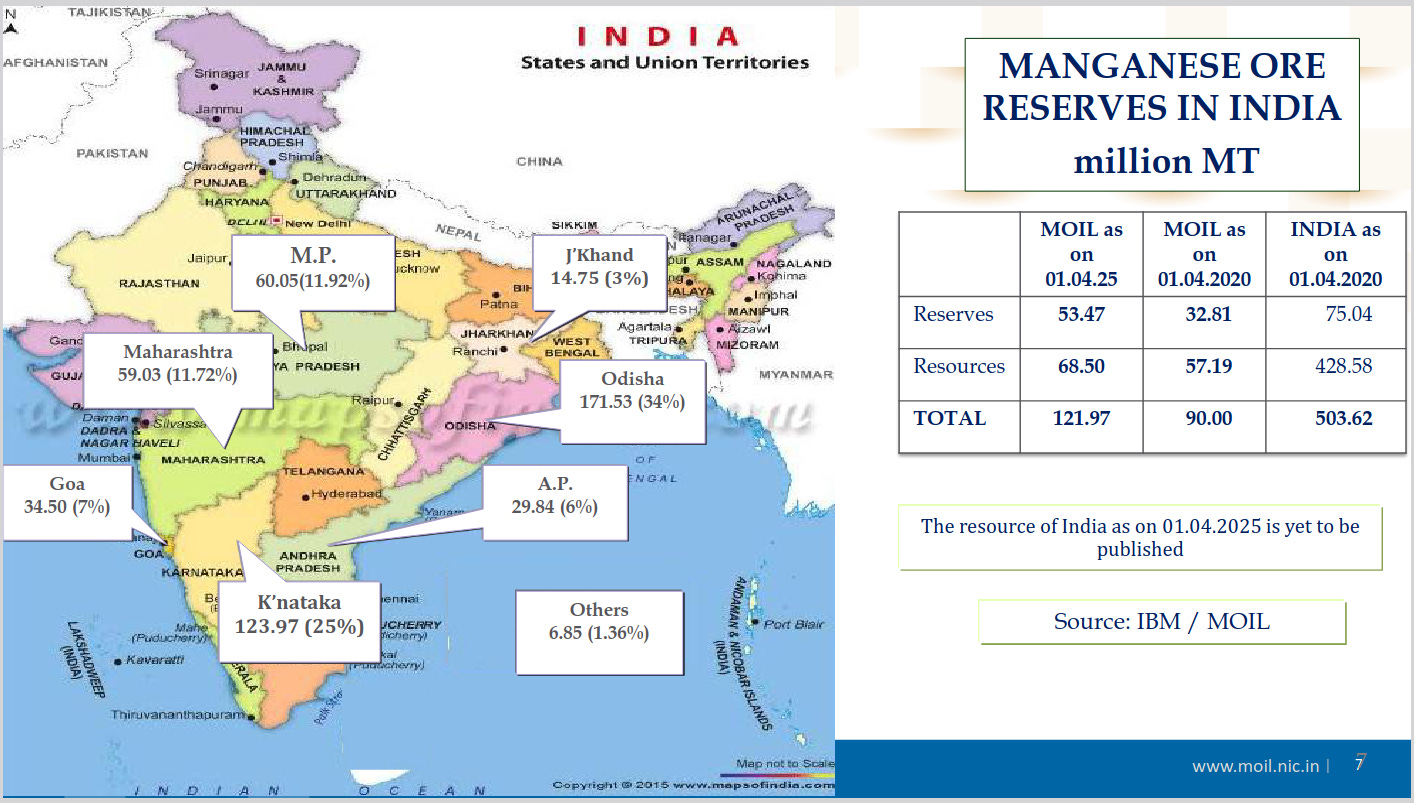

Manganese reserves are heavily concentrated in Odisha (~34%), Karnataka (~25%), and MP/Maharashtra (~12% each). MOIL has significantly expanded its reserve base, strengthening its strategic positioning in domestic supply.

Trading

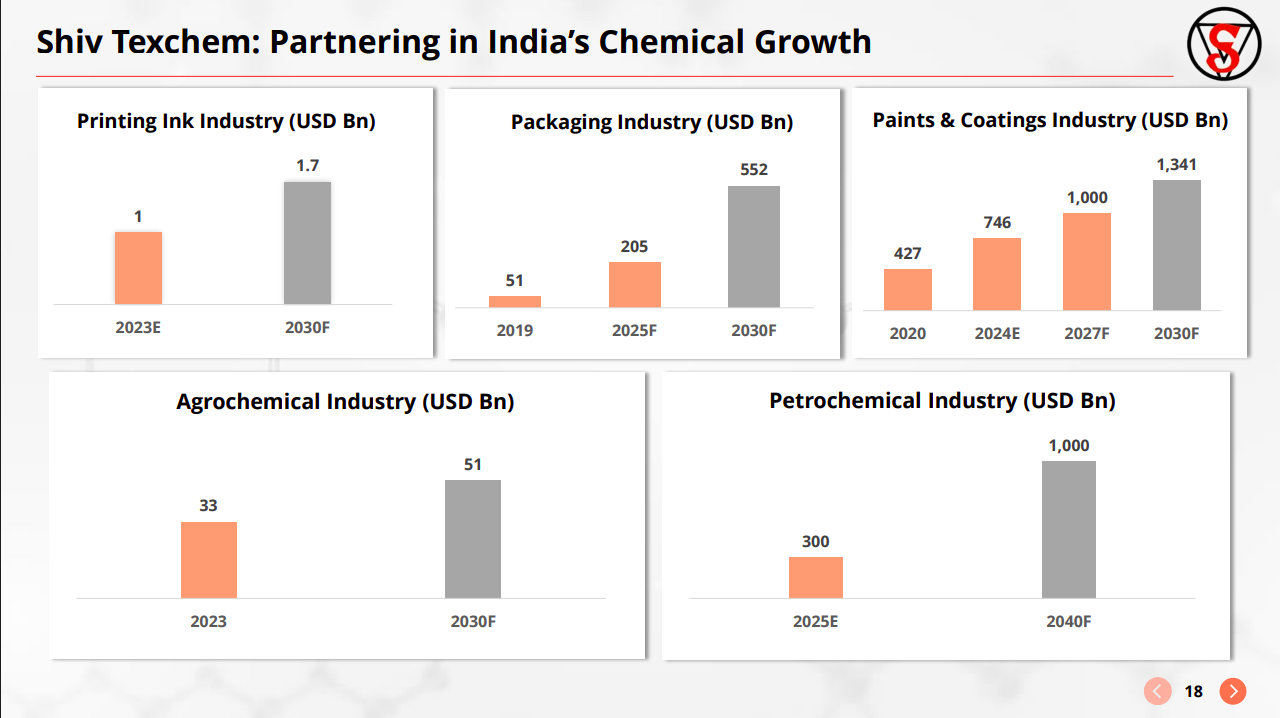

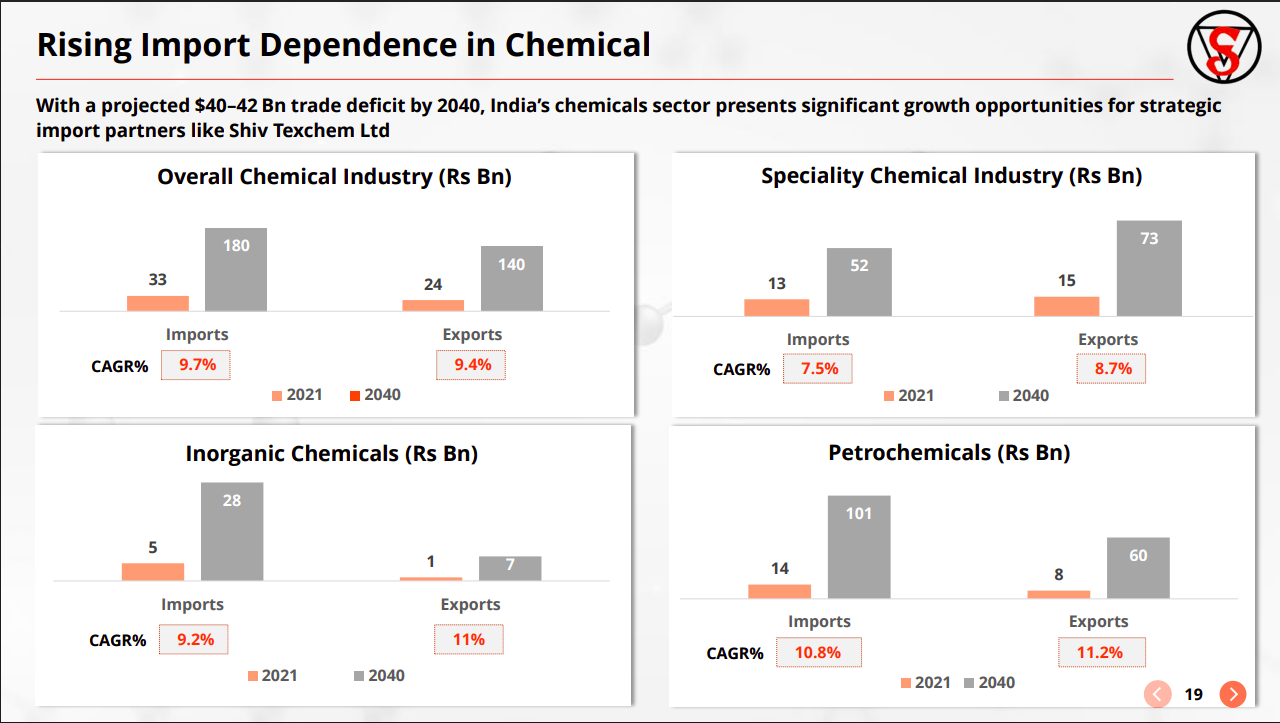

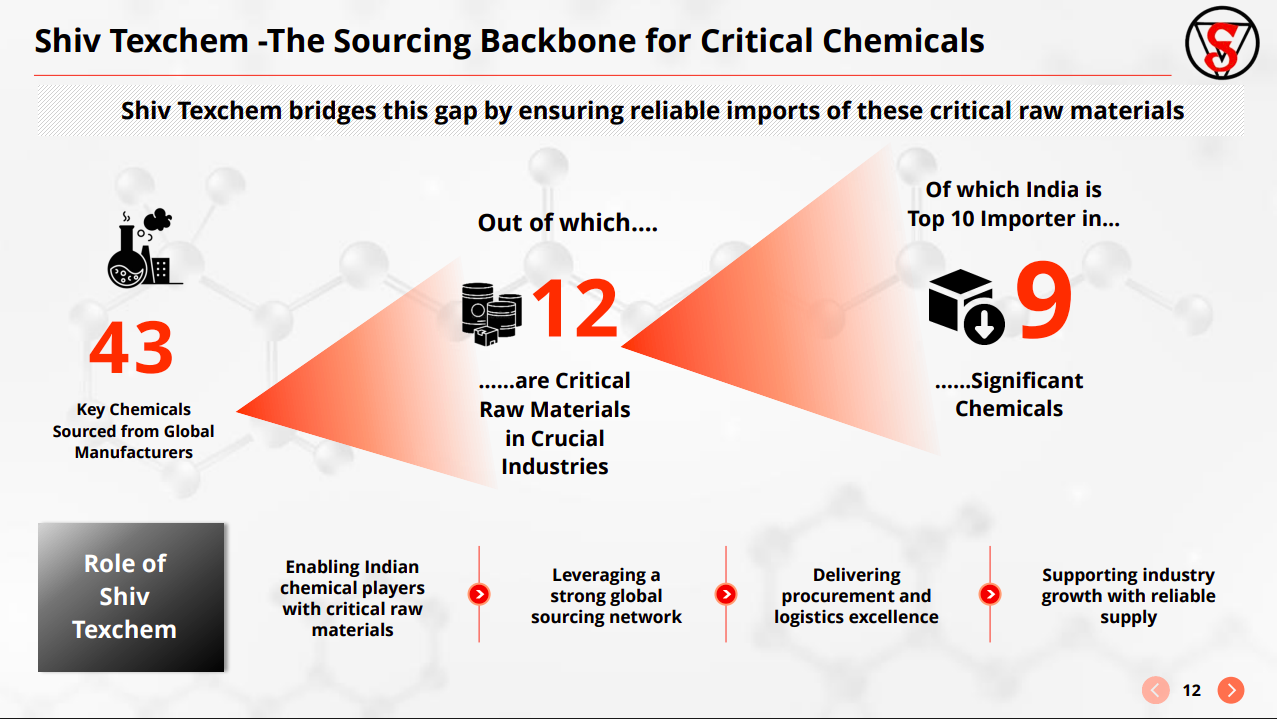

Shiv Texchem | Nano Cap | Trading

Shiv Texchem Ltd. imports and distributes specialty hydrocarbon chemicals — including acetyls, aromatics, glycols, and ketones — sourced from over 60 global suppliers and supplied to more than 650 Indian customers across the paints, pharma, and polymer industries.

The company is leveraged to structurally growing sectors—paints, packaging, agrochemicals, petrochemicals, and inks, all expected to see strong multi-year expansion. This creates sustained demand visibility for sourced chemicals.

India’s chemical sector is expected to see significant growth in imports (~9–11% CAGR), with a widening trade deficit. This structurally increases the role of import-focused sourcing intermediaries like Shiv Texchem.

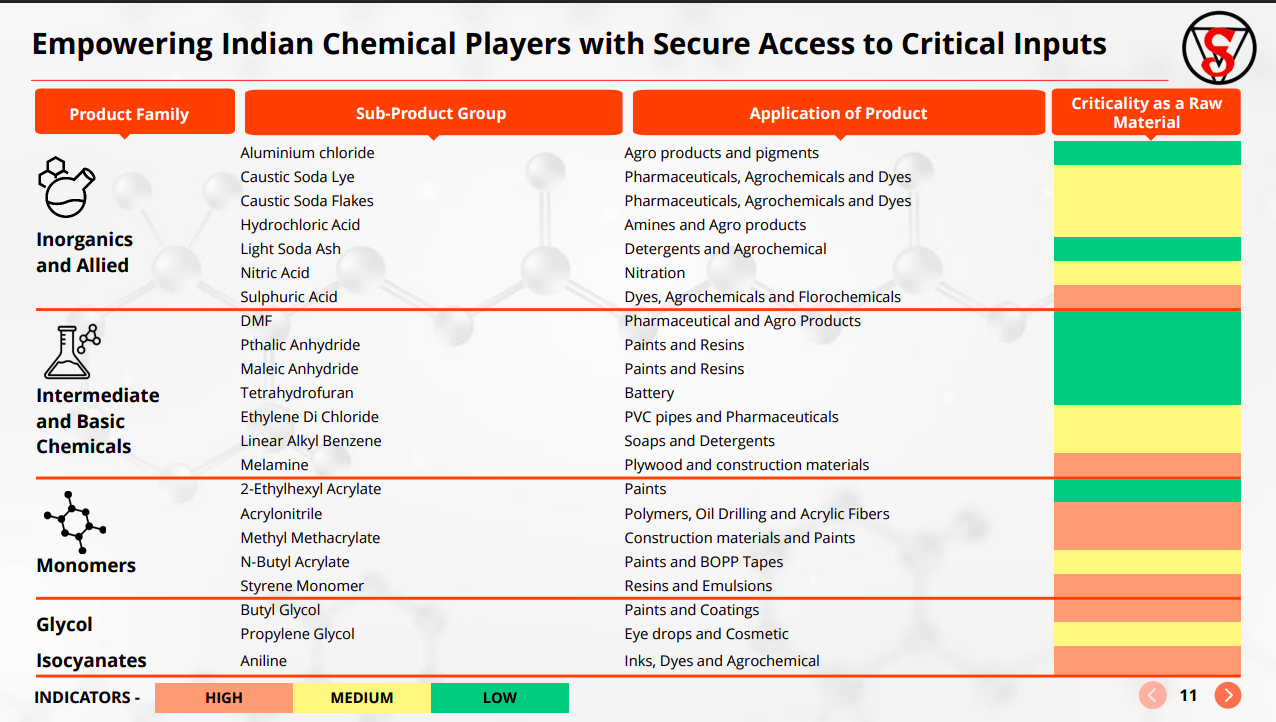

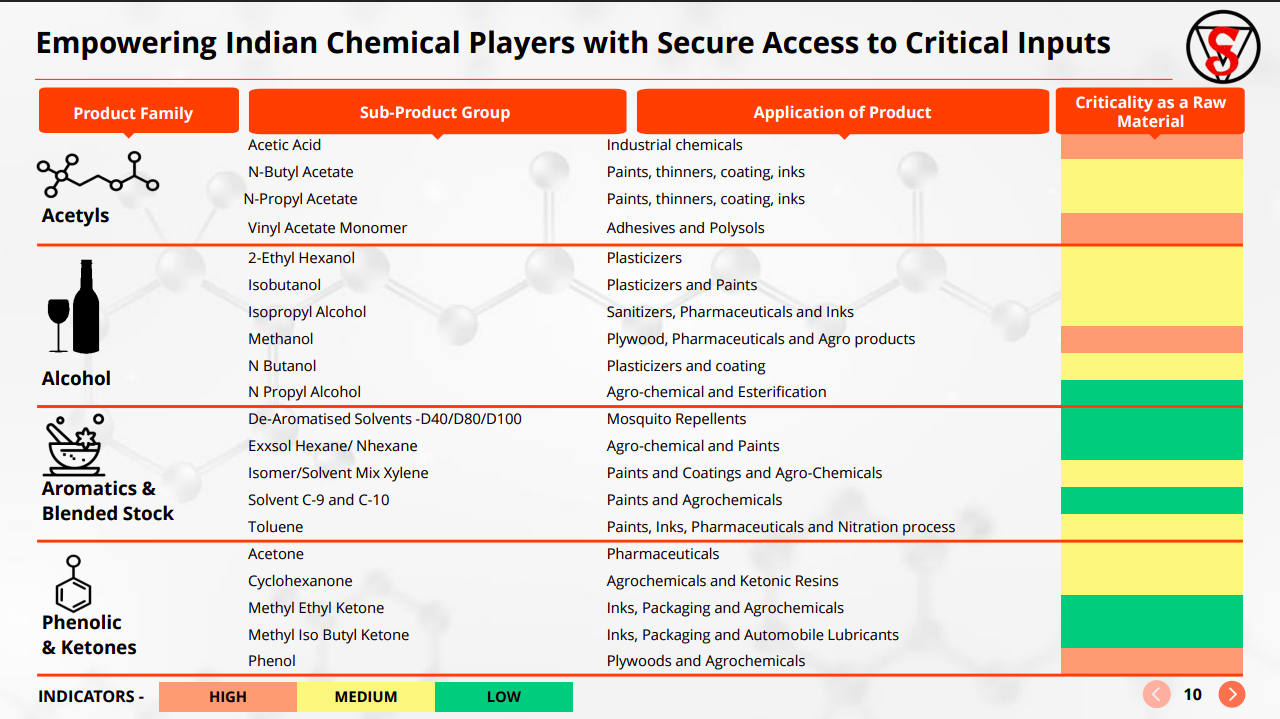

Shiv Texchem operates across a wide basket of essential chemicals spanning inorganics, intermediates, monomers, and glycols, supplying critical inputs to pharma, agrochemicals, paints, and construction. Many of these inputs have high supply criticality, reinforcing the importance of reliable sourcing.

The portfolio extends into acetyls, alcohols, aromatics, and ketones, which are key building blocks for coatings, adhesives, plastics, and pharma. This positions the company at the center of multiple downstream industrial value chains.

Shiv Texchem bridges India’s supply gap by sourcing 43 key chemicals globally, including 12 critical raw materials, with India being a top importer in several. The model is built on global sourcing, logistics execution, and supply reliability.

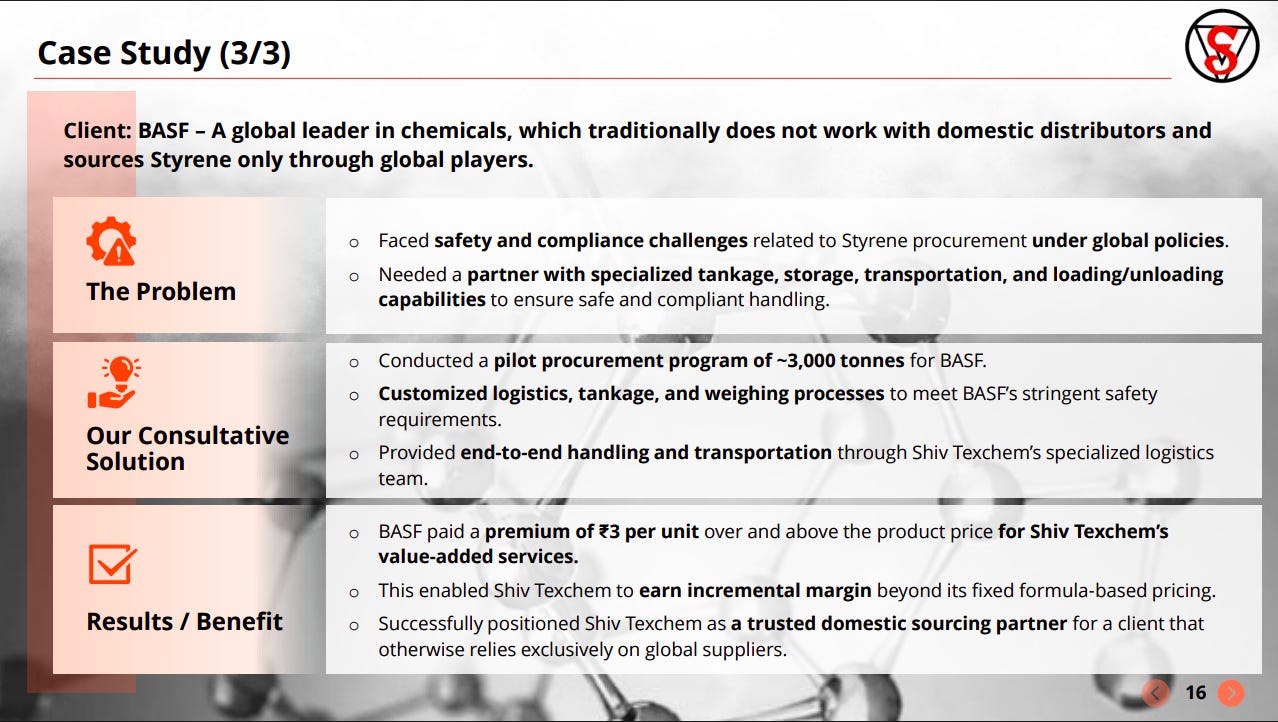

For a global major like BASF, Shiv Texchem delivered specialized logistics and compliance-led sourcing, enabling safe handling of styrene. This led to premium pricing and higher margins, showcasing value-added capabilities beyond trading.

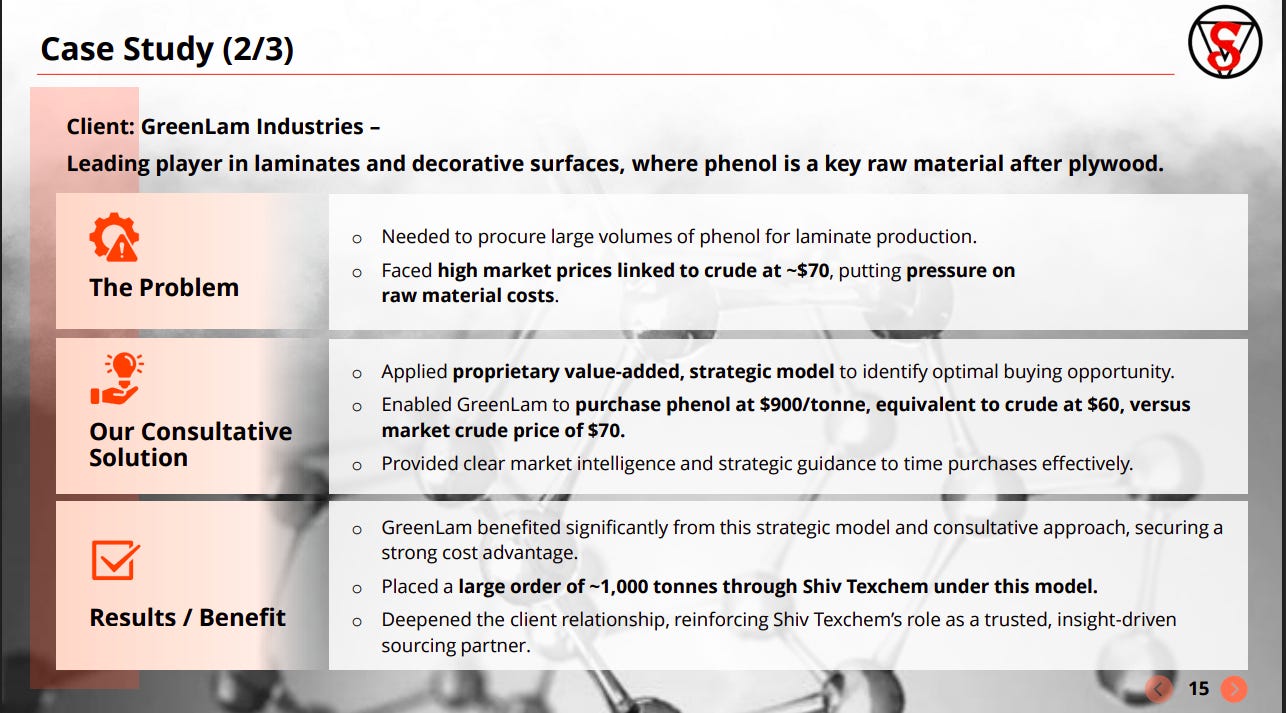

By leveraging market intelligence and timing strategies, Shiv Texchem helped GreenLam procure phenol at lower effective prices. This created cost advantages for the client while deepening long-term relationships and volumes.

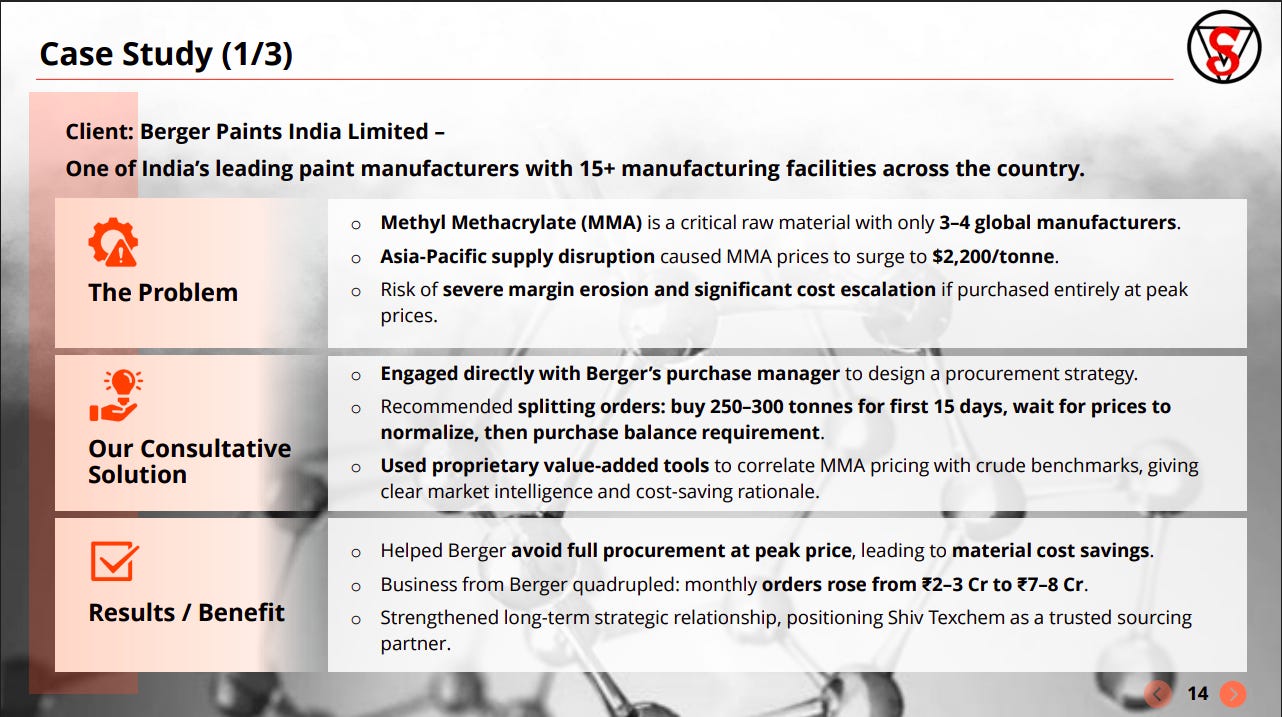

During a supply shock in MMA, Shiv Texchem’s procurement strategy (staggered buying + price benchmarking) helped Berger avoid peak pricing. This resulted in cost savings and a 3–4x scale-up in business volumes.

Engineering & Capital Goods

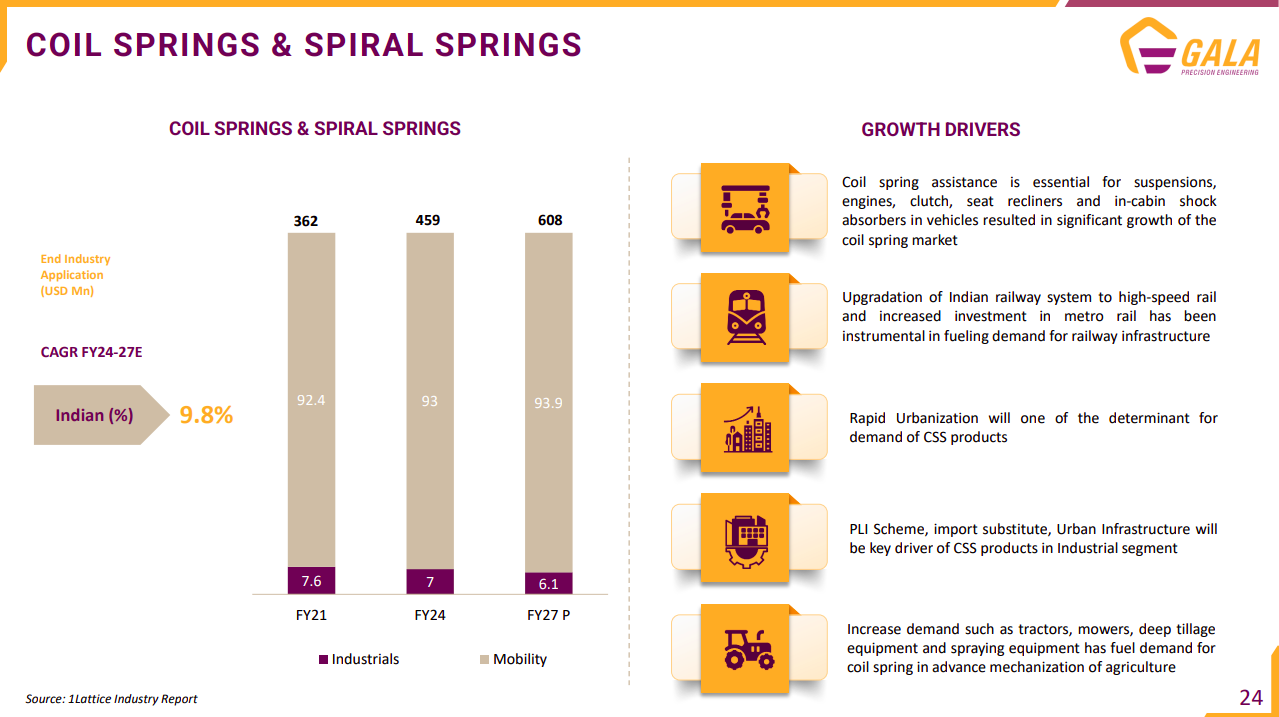

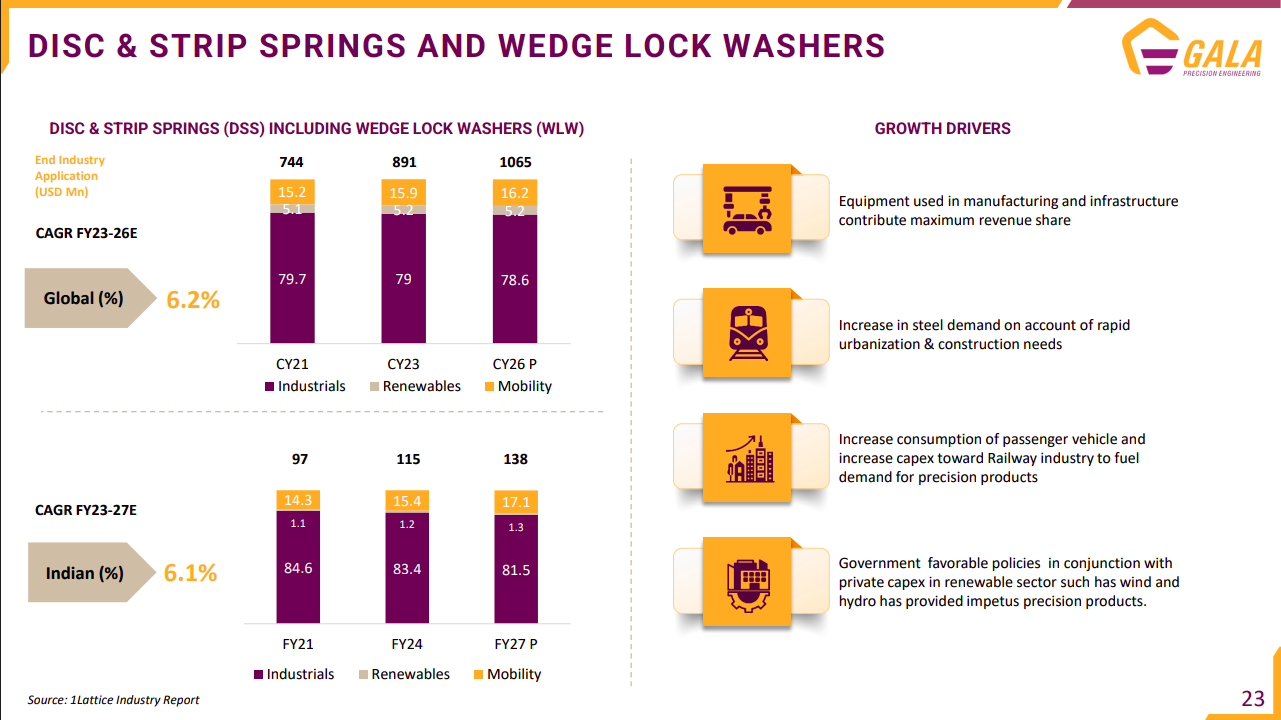

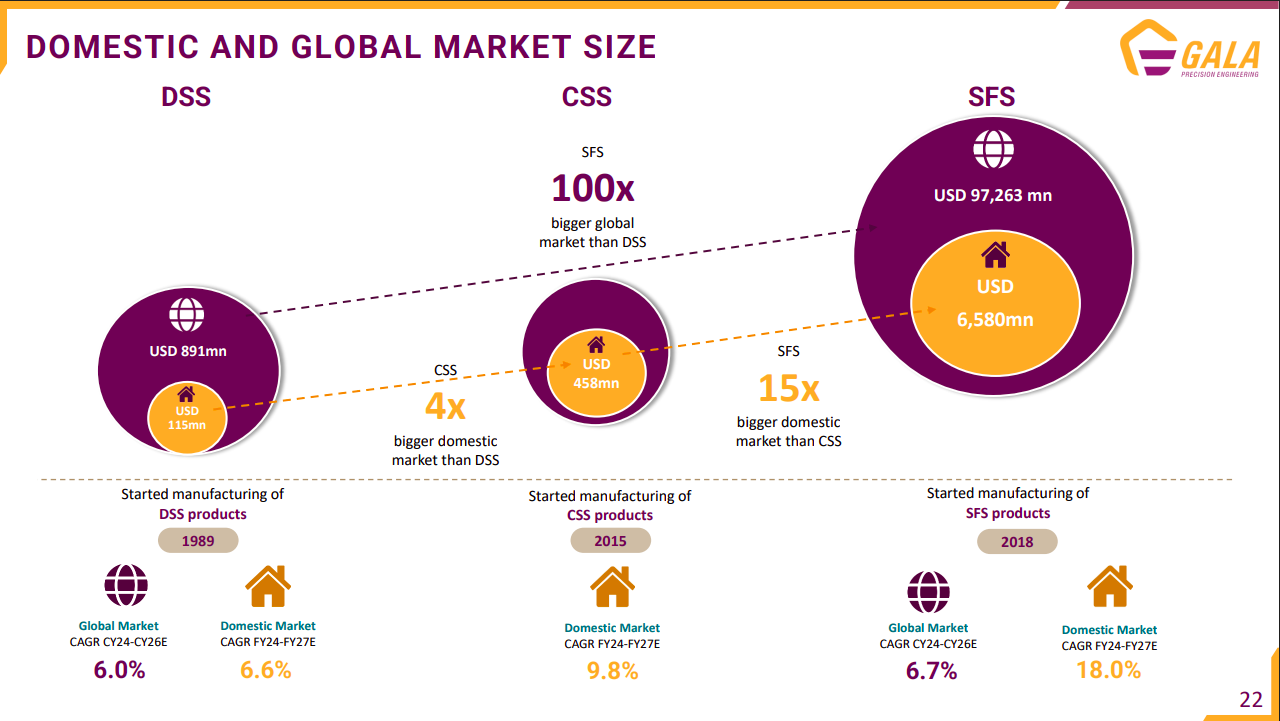

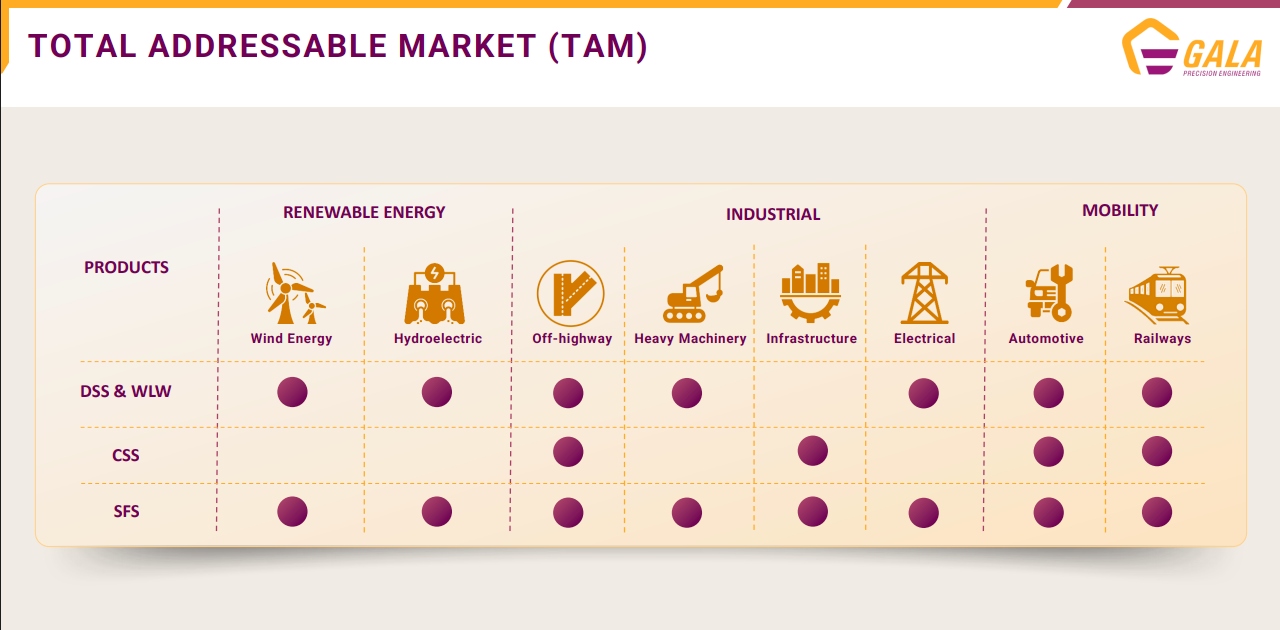

Gala Precision Engineering | Micro Cap | Engineering & Capital Goods

Gala Precision Engineering Ltd. manufactures high-quality technical springs and high-tensile fasteners. It serves the renewable energy, mobility, and industrial sectors.

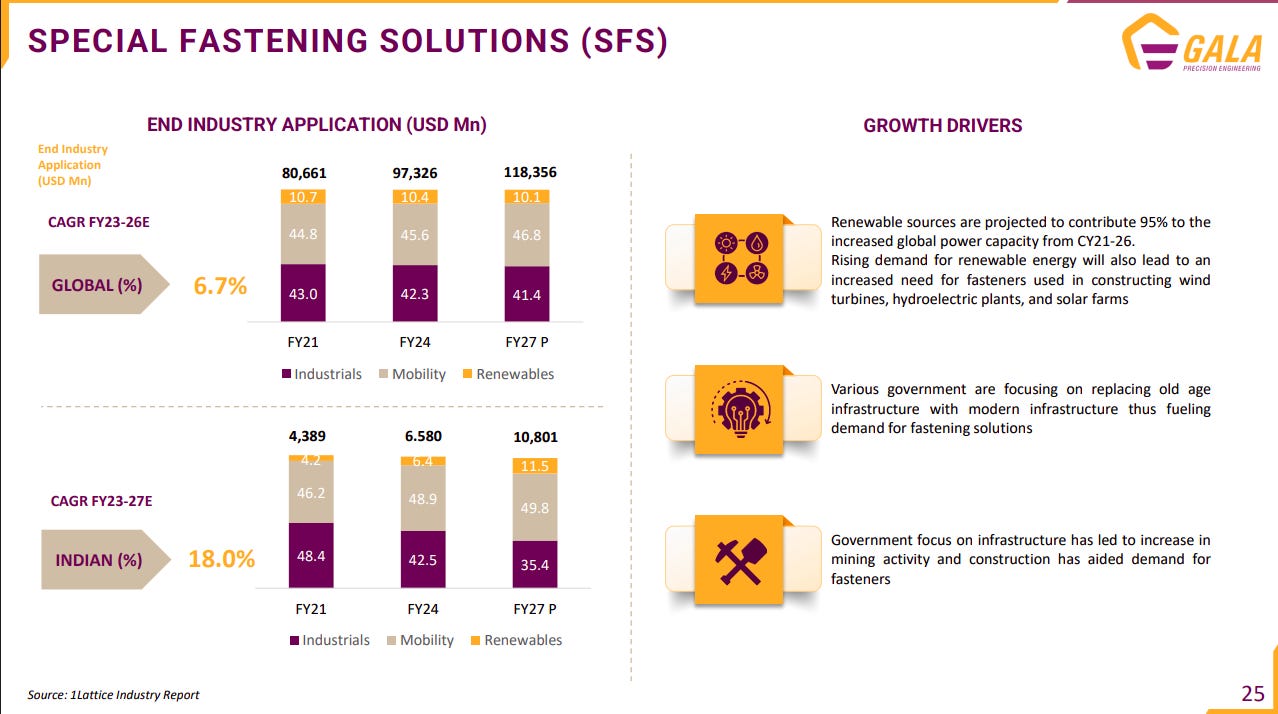

SFS is the largest and fastest-growing segment, with India growing at ~18% CAGR vs ~6–7% globally. Growth is driven by renewables, infrastructure upgrades, and mining/construction demand, making it a key structural opportunity.

CSS is a mobility-heavy segment (~90%+ exposure) growing at ~9–10% CAGR in India. Demand is supported by auto components, rail capex, urbanization, and farm mechanization.

DSS is a stable, industrial-led segment (~6% CAGR) with strong linkage to manufacturing, infrastructure, and steel demand cycles. Mobility and renewables provide incremental growth levers.

SFS is structurally the largest opportunity—~100x the size of DSS globally and ~15x CSS domestically. This highlights a clear portfolio shift opportunity toward higher TAM segments.

GALA’s product portfolio spans renewables, industrials, and mobility, with SFS having the widest application coverage. This diversified exposure provides multi-cycle growth optionality.

The company operates across the value chain—from steel inputs to precision components (DSS, CSS, SFS)—serving critical applications in wind, infrastructure, heavy machinery, and autos. This enables deep integration with end-use industries.

GALA has built strong relationships across renewables (Vestas, GE), industrials (Schneider, L&T), and mobility (Schaeffler, Wabtec). This diversified client base supports revenue visibility and credibility across sectors.

Oriental Rail Infrastructure Limited | Small Cap | Engineering & Capital Goods

Oriental Rail Infrastructure manufactures rolling stock components, interiors, and freight wagons for Indian Railways and private logistics operators. The company is strategically transitioning into high-technology smart wagons and recurring-revenue leasing models to diversify its earnings profile.

Moving into wagon leasing shifts the business model toward stable annuity revenues, reducing the impact of volatile manufacturing tender cycles. This transition provides predictable long-term cash flows and higher-margin growth.

A record ₹2.9 lakh crore railway budget for FY27 signals a multi-year commitment to modernization, providing long-term demand visibility. This structural growth supports more confident capacity expansion and capital allocation.

National Rail Plan targets for fleet doubling indicate a long-term structural upgrade cycle beyond immediate government spending. This strategy balances stable freight demand with higher margins from premium passenger interiors.

KEI Industries Limited | Mid Cap | Electrical Engineering & Capital Goods

KEI Industries Limited is a leading manufacturer of wires and cables, offering a diverse product range from EHV to LT cables, house wires, and stainless steel wire. The company is forward-integrated into EPC services and has a strong presence in both domestic and international markets.

KEI’s retail sales are growing significantly, now accounting for over 50% of total sales. This shift reflects a strategic focus on direct consumer engagement, which could lead to higher margins and more predictable demand.

KEI Wires & Cables is poised to benefit from robust industry growth, driven by power transmission and building wires, which account for half the market. Government initiatives and rising demand from construction and renewable energy sectors ensure strong long-term prospects.

India’s cables and wires market is set for significant growth, aiming to reduce import reliance and boost domestic production. Focus on high-demand segments like power cables and building wires, along with export expansion, signals a strategic shift towards self-sufficiency and global competitiveness.

The growing demand for cables and wires is fueled by infrastructure development, including data centers, cloud computing, and digital transformation. Government investments in renewable energy and power transmission ensure a durable demand environment for the industry.

KEI Wires & Cables is strategically aligned with the surge in renewable energy and EV adoption, which drive substantial demand for cables and wires. The company’s focus on energy storage and transmission infrastructure positions it well for sustained growth and higher margins.

The National Electricity Plan outlines India’s ambitious targets for power expansion, including renewable energy goals and infrastructure investments. This plan underscores the industry’s role in supporting India’s energy transition and economic growth, providing a clear roadmap for future demand.

Healthcare

Aster DM Healthcare Limited | Mid Cap | Healthcare

Aster DM Healthcare is a major integrated healthcare provider operating a network of hospitals and clinics across India. The company is currently executing a large-scale merger with Quality Care India to significantly expand its bed capacity and specialty care reach.

A massive pipeline of over 4,000 additional beds signals a shift toward aggressive regional scale and market leadership. The primary investment risk involves managing the gestation costs of new facilities without diluting near-term group returns.

Inpatient revenue per patient grew 17% as the cluster shifted toward high-complexity specialties like oncology and neurosciences. This move toward tertiary care improves unit economics and builds a stronger competitive moat across mature facilities.

Margin improvement from 7.9% to 13.2% in the Andhra and Telangana cluster indicates that newer assets are successfully absorbing fixed costs. This turnaround trajectory is critical for reaching company-wide profitability benchmarks.

Utilizing 30-year leases for major greenfield projects reflects an asset-light strategy that prioritizes medical technology over land ownership. This model reduces upfront capital requirements but requires sustained high occupancy to cover long-term lease obligations.

Real Estate

Prestige Estates | Mid Cap | Real Estate

Prestige Estate Projects specializes in real estate development, construction, leasing commercial properties, and property management. The company operates across residential, commercial, retail, hospitality, and services, leveraging an integrated model for consistent performance, innovation, and resilience during market fluctuations.

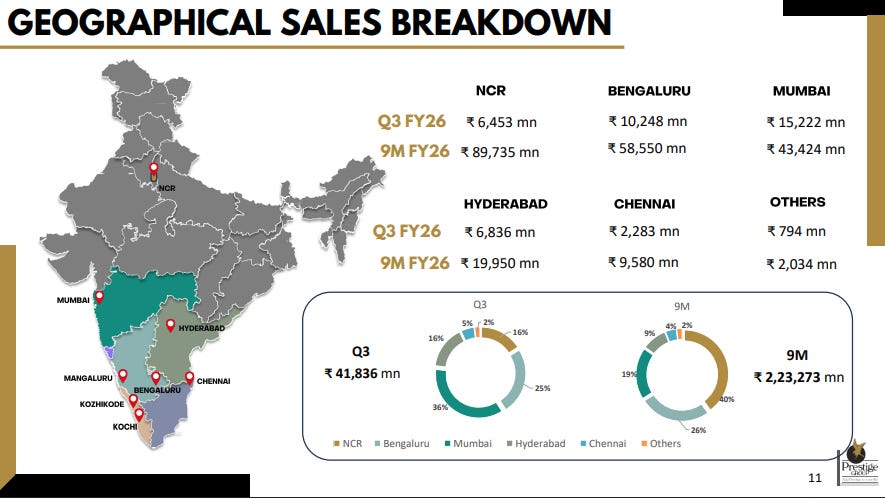

Sales are concentrated in Mumbai and Bengaluru, which together contribute the largest share across both Q3 and the nine-month period, with NCR also forming a meaningful portion. Other cities like Hyderabad and Chennai contribute moderately, while the rest remain a small part of the overall mix.

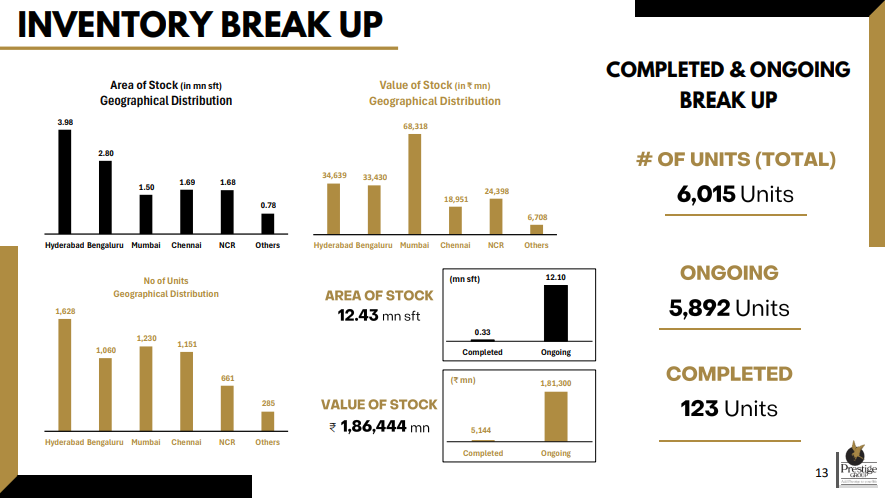

Inventory is largely concentrated in Hyderabad and Bengaluru by area, while Mumbai leads in value, with total inventory at 12.43 mn sq ft worth ₹1,86,444 mn. Most of this is tied to ongoing projects, with 5,892 out of 6,015 units still under development and only a small portion completed.

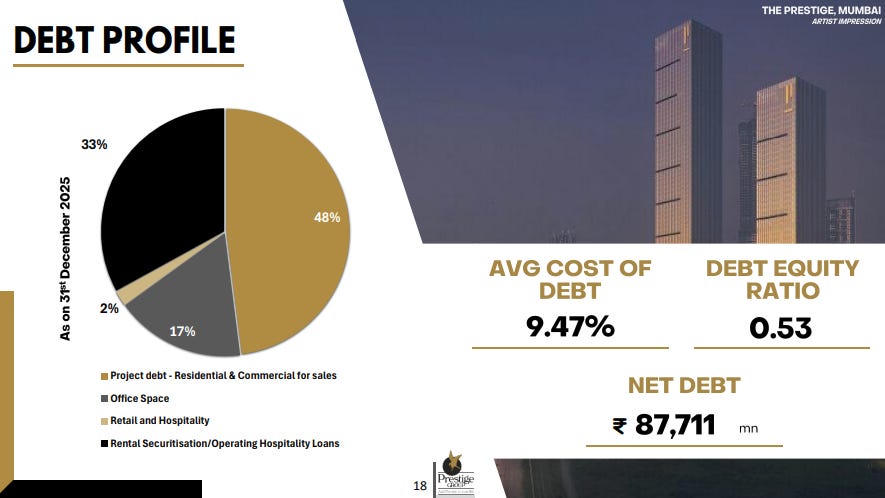

Debt is largely concentrated in project-related borrowings, making up nearly half of the total, with the remainder spread across office assets and rental/hospitality loans. The average cost of debt stands at 9.47%, with a debt-to-equity ratio of 0.53 and net debt at ₹87,711 million.

That’s it for now! Your feedback will really help shape how Points and Figures evolves. Drop it down in the comments below!

Quotes in this newsletter were curated by Meher & Vignesh.

Disclaimer: We’ve used AI tools in filtering and cleaning up the quotes from the images so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Points and Figures is run by the same team that creates The Daily Brief and Aftermarket Report.