Sometimes, a single slide can explain more than a long report. Points and Figures is our way of breaking down what India’s leading companies are telling their shareholders and analysts. We comb through the decks, pull out the charts and data points that actually matter, and highlight the signals behind the numbers—whether about growth plans, margins, new markets, or risks on the horizon.

This is an extension of The Chatter. While The Chatter focuses on management commentary and earnings call transcripts, Points and Figures dives into investor presentations—and soon, even annual reports—to decode what companies are showing, not just what they’re saying.

We go through every major investor presentation so you don’t have to—bringing you the sharpest takeaways that reveal not just what the company is saying, but what it really means for the business, its sector, and the broader economy.

In this edition, we have covered 15 companies across 10 industries.

Financial Services

Multi Commodity Exchange of India

Building Materials

UltraTech Cement

Dalmia Bharat

Engineering & Capital Goods

Premier Energies

Textiles

Borana Weaves

Metals

JTL Industries

Epack Prefab Technologies

Retail

Tribhovandas Bhimji Zaveri Limited (TBZ)

Jindal Stainless

D. P. Abhushan

Services

Gravita India

Chemicals

Tatva Chintan Pharma

Healthcare

Dr. Reddy’s Lab

Software Services

Mphasis

Persistent Systems

Financial Services

Multi Commodity Exchange of India | Mid Cap | Financial Services

Multi Commodity Exchange of India Limited (MCX) offers online trading of commodity derivatives across segments like bullion, industrial metals, energy, and agriculture. It allows for price discovery and risk management, and is known for introducing innovative products like commodity options, bullion index futures, and base metals index futures. MCX focuses on providing participants in the commodity value chain with secure and transparent trade mechanisms while adhering to regulatory standards

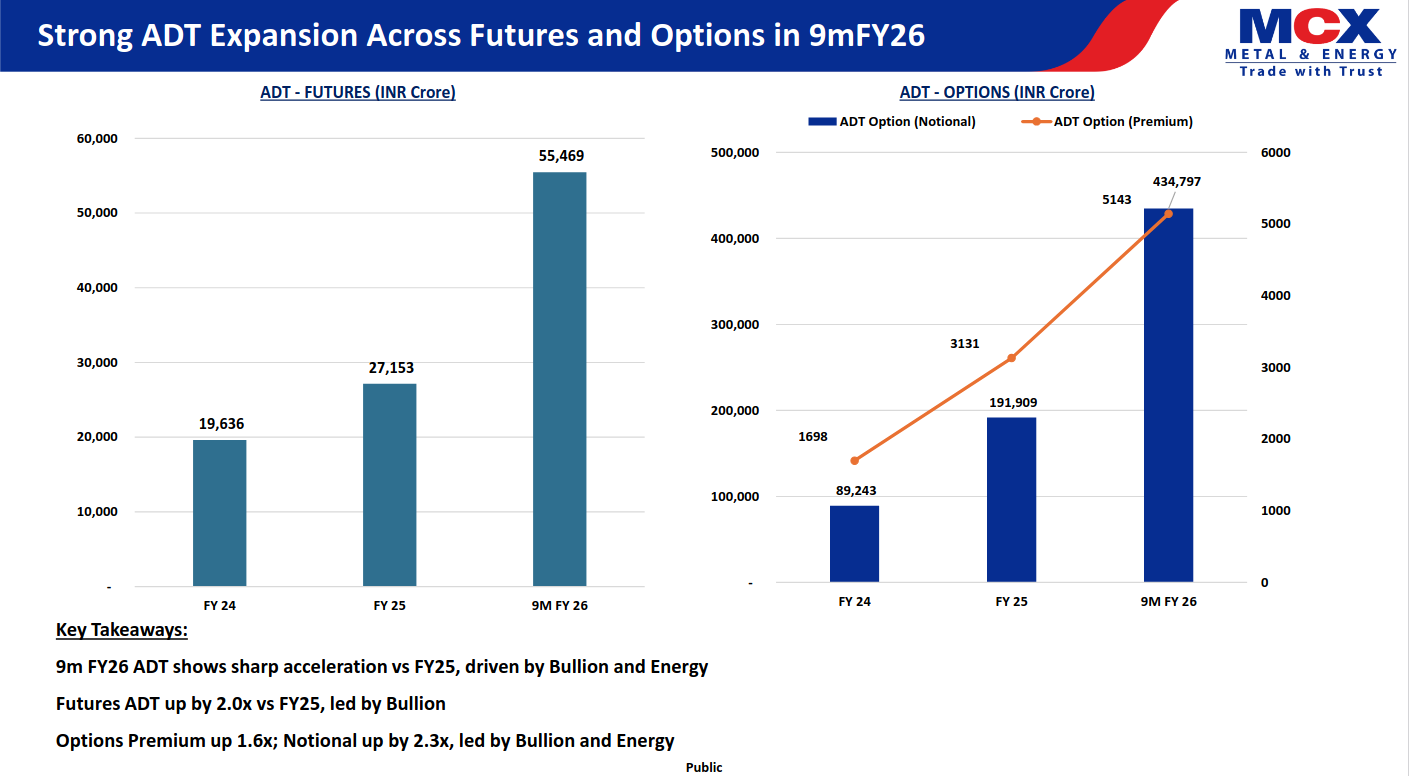

MCX delivered sharp acceleration in average daily turnover during 9M FY26, led by bullion and energy contracts. Futures ADT (Average Daily Turnover) doubled vs FY25, while options saw strong traction with premium up ~1.6× and notional volumes up ~2.3×.

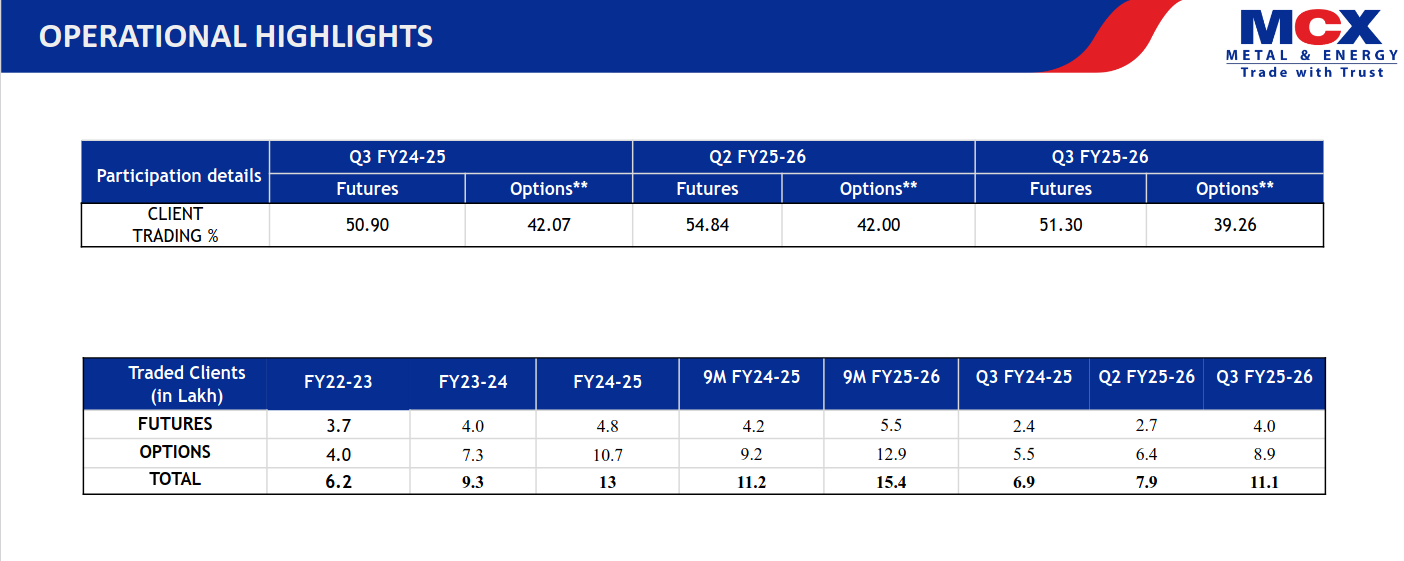

Client participation strengthened across both futures and options, with steady trading intensity despite quarterly volatility. Traded clients increased meaningfully in 9M FY26, driven largely by faster growth in options participation.

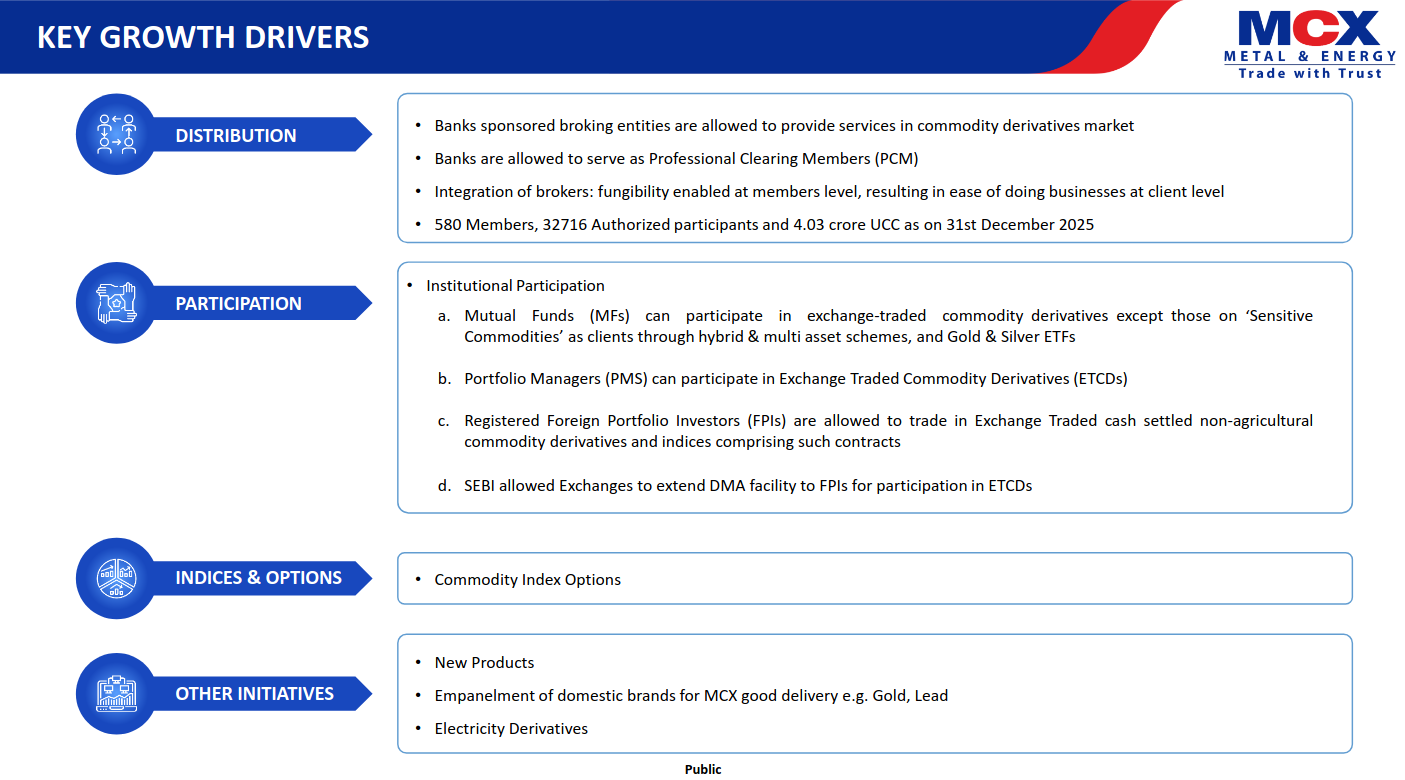

Regulatory changes enabling bank participation, institutional access (MFs, PMS, FPIs), and clearing reforms are structurally expanding the commodity derivatives ecosystem. New products, index options, electricity derivatives, and broader delivery participation add incremental growth levers.

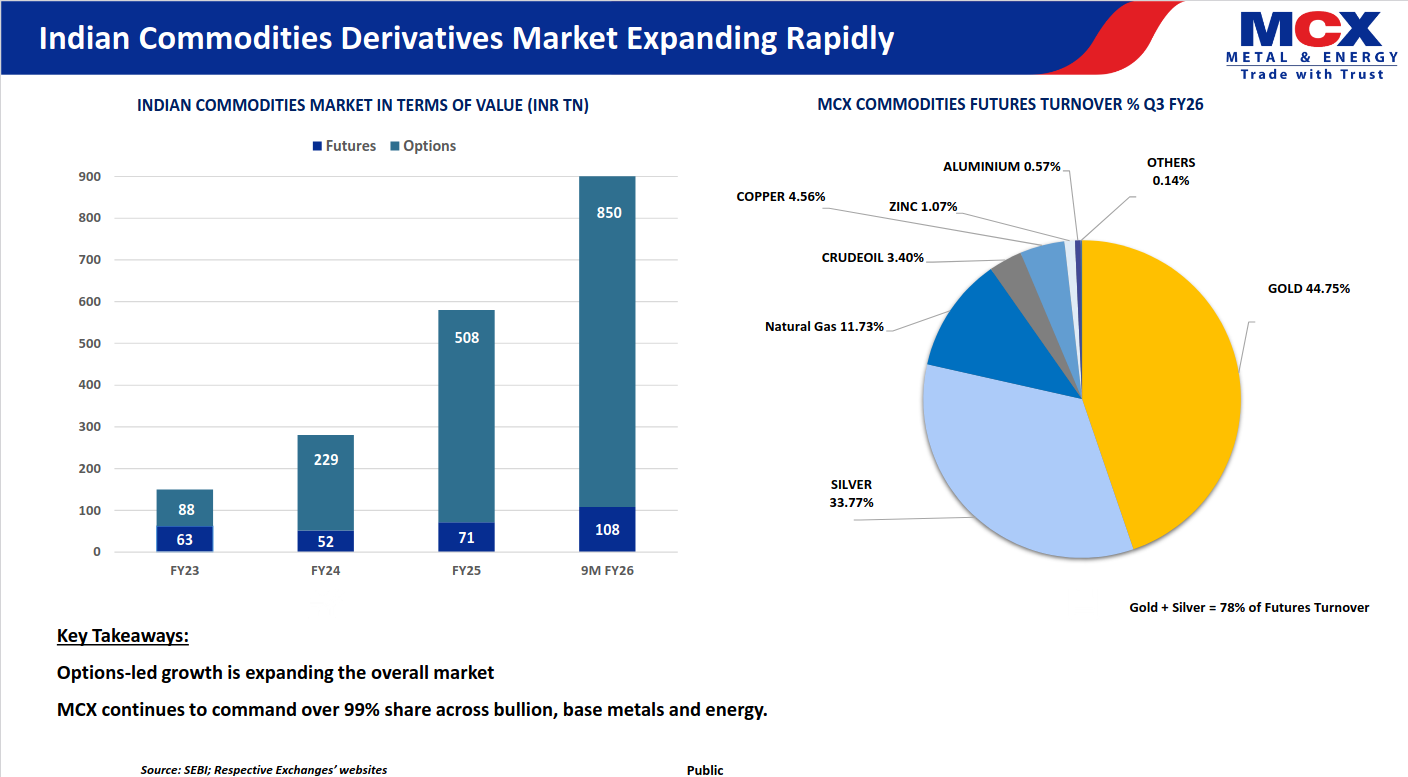

Options-led growth is significantly expanding the overall commodities market value, with MCX maintaining dominant market share across bullion, base metals, and energy. Gold and silver continue to anchor volumes, accounting for ~78% of futures turnover.

Building Materials

UltraTech Cement | Large Cap | Building Materials

UltraTech Cement, part of the Aditya Birla Group, is a leading manufacturer of grey cement, ready mix concrete, and white cement in India. It is the third largest cement producer globally, operating in UAE, Bahrain, Sri Lanka, and India. UltraTech’s Building Products business offers innovative solutions for modern construction projects under the brand Birla White.

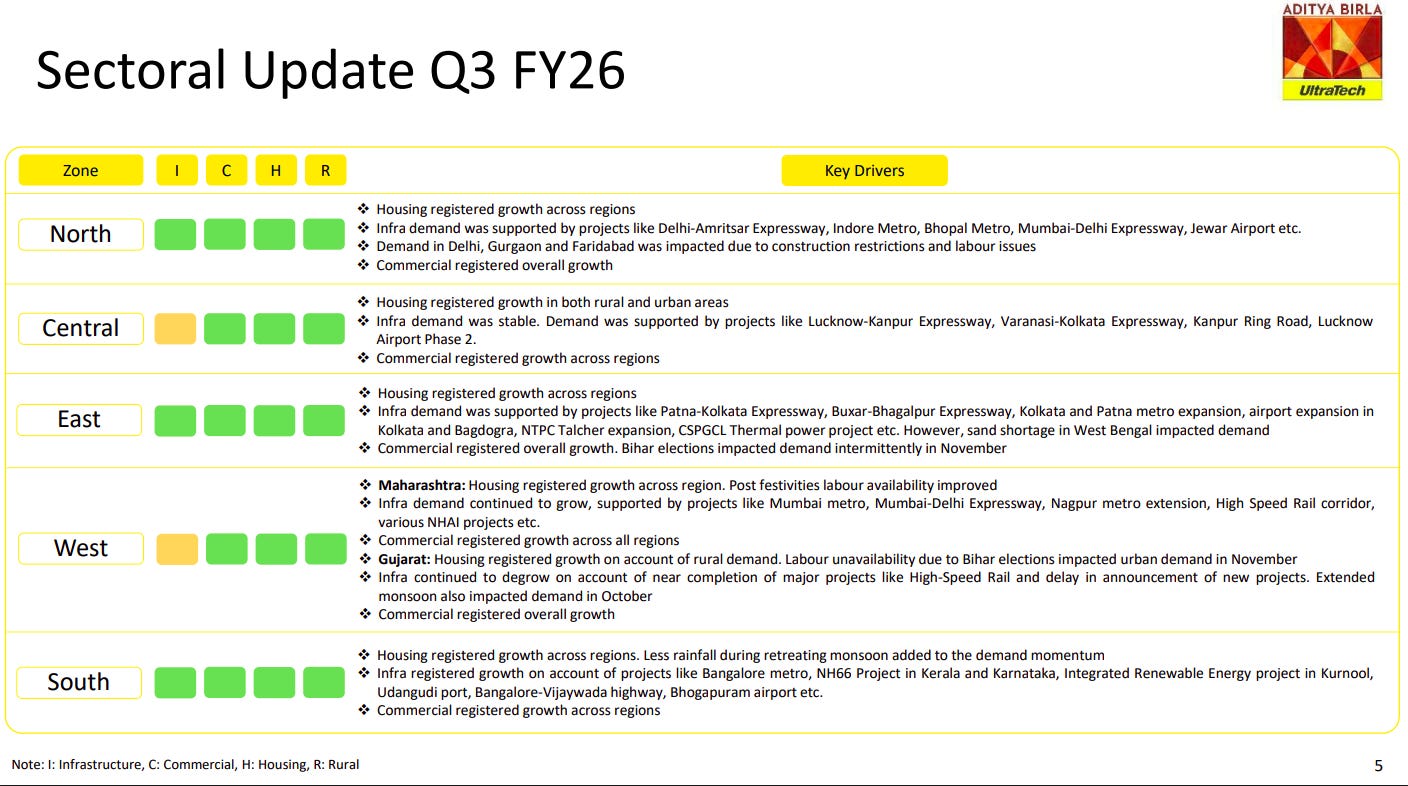

Demand trends remained positive across most regions, supported by housing growth and large infrastructure projects. While localized disruptions impacted certain pockets, commercial and infrastructure activity showed broad-based resilience across zones.

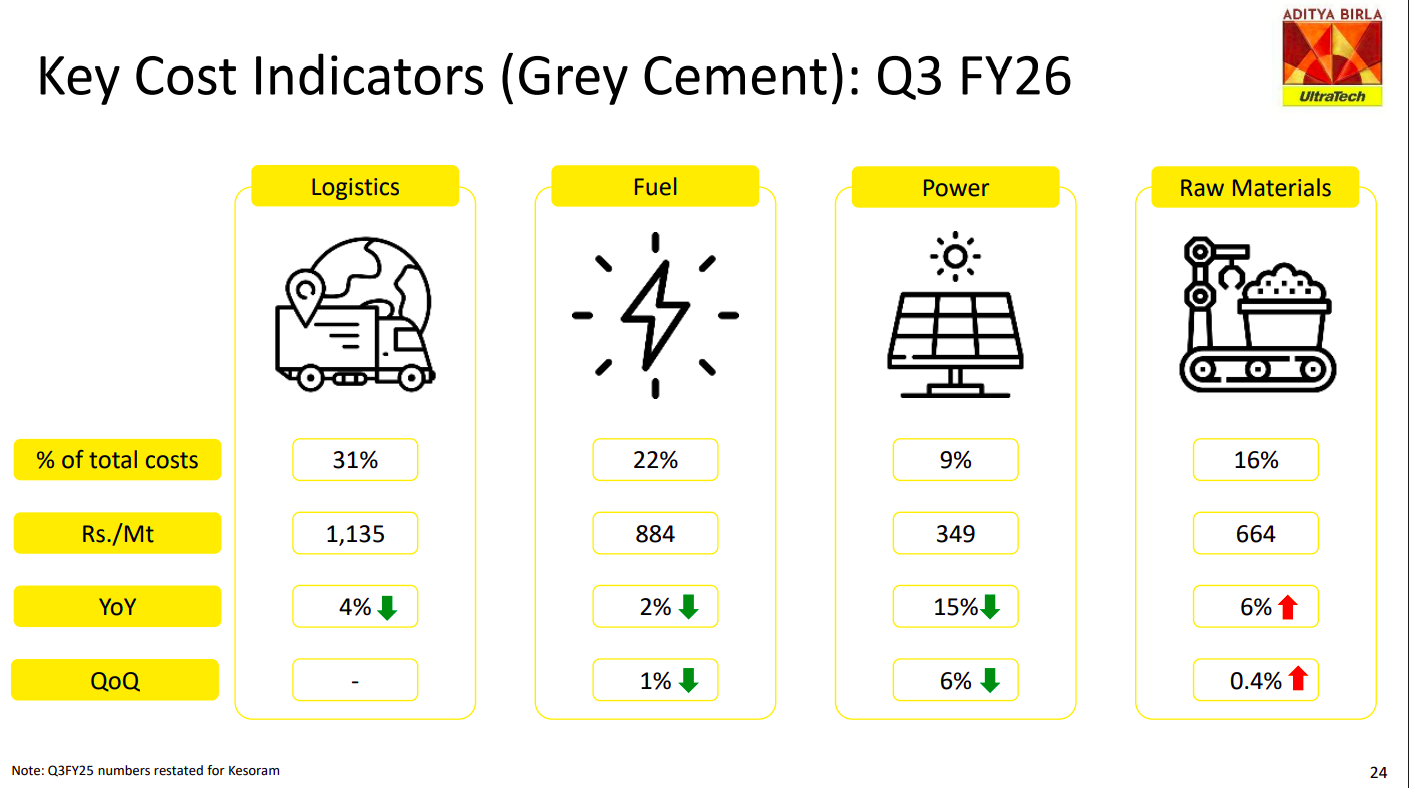

Logistics and fuel remain the largest cost components, together accounting for over 50% of total costs, though both saw YoY moderation. Power costs declined sharply due to efficiency gains, while raw material costs edged up marginally, reflecting input inflation pressures.

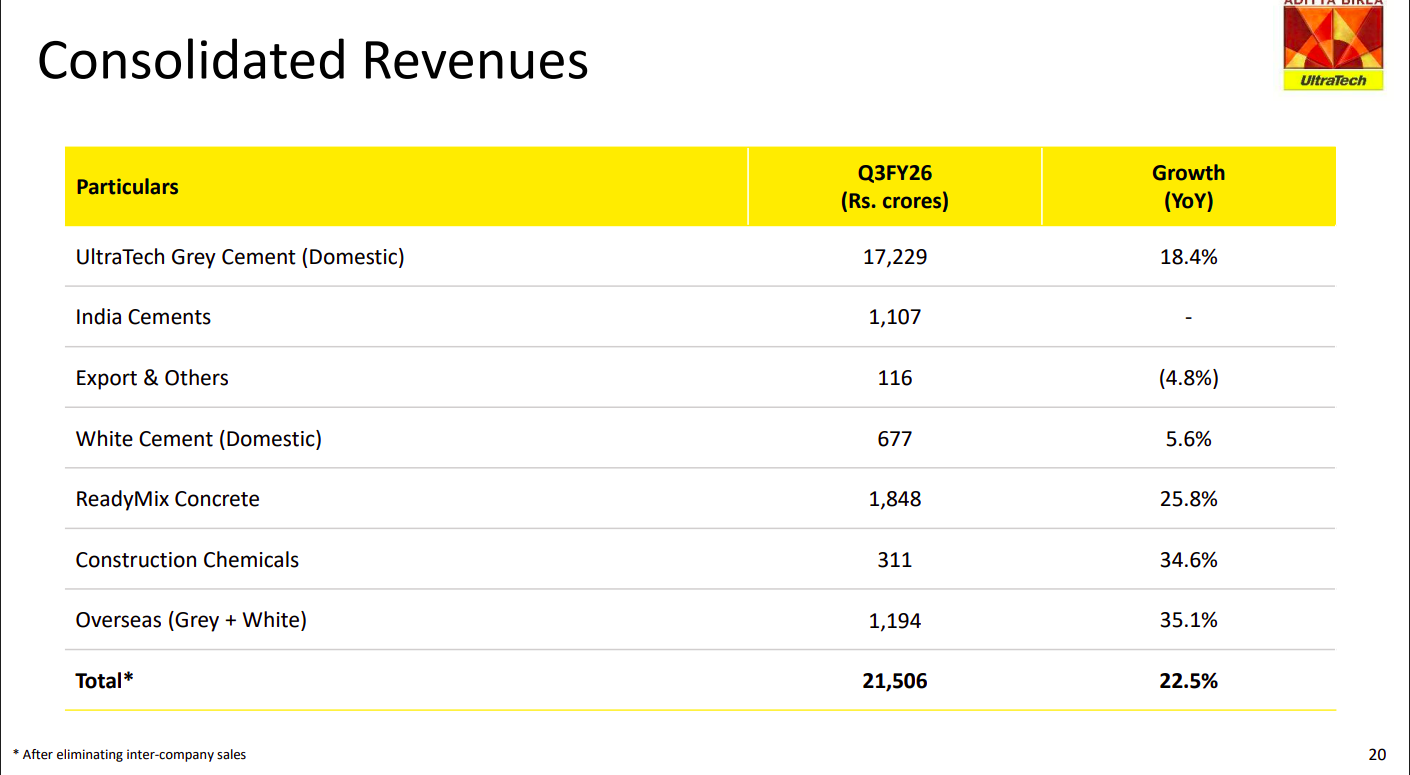

UltraTech reported strong topline growth of 22.5% YoY, led by domestic grey cement, ready-mix concrete, construction chemicals, and overseas operations. Growth was broad-based, with higher value-added segments outpacing core volumes.

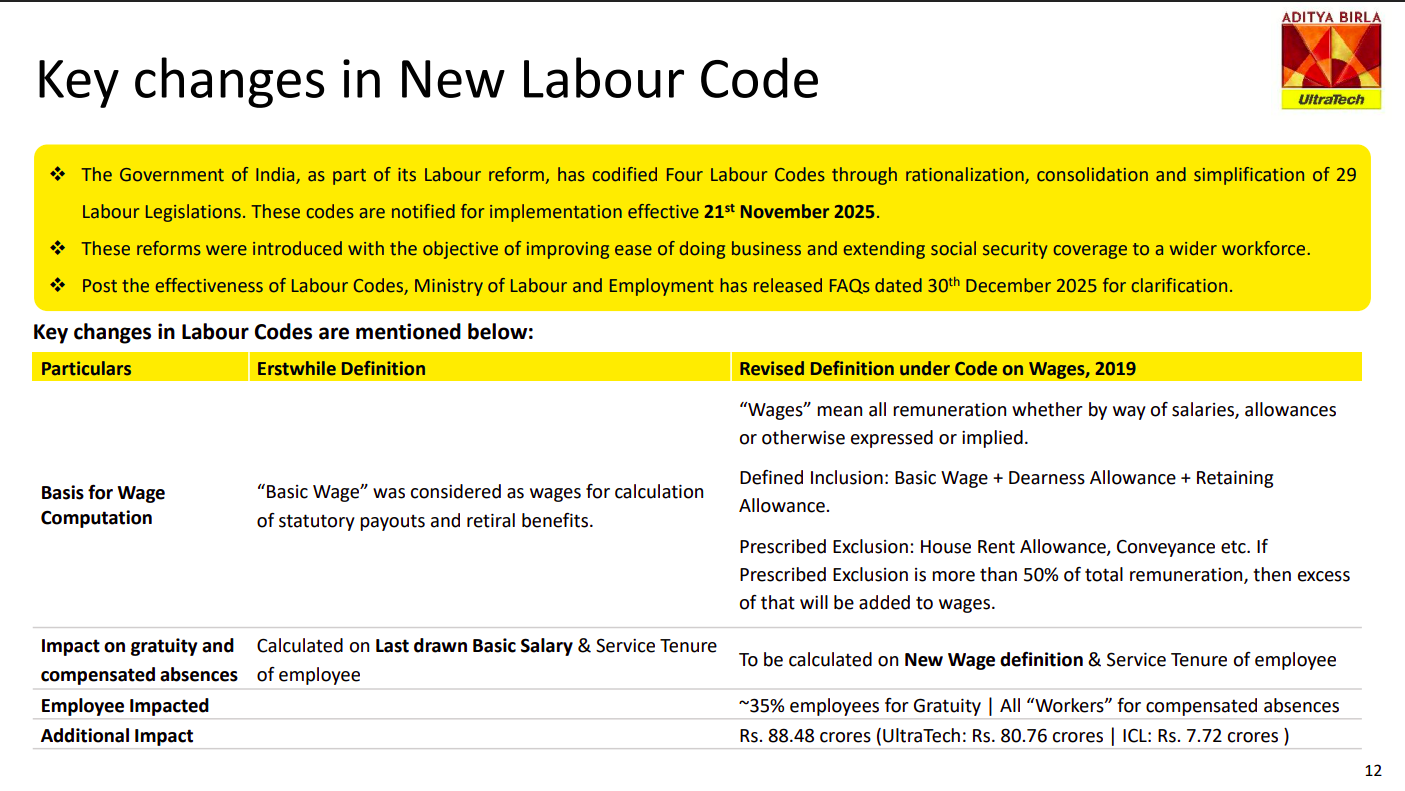

The new labour codes expand the definition of wages, increasing gratuity and compensated absence liabilities for companies. For UltraTech and India Cements, the one-time impact is estimated at ₹88.5 crore, affecting ~35% of employees for gratuity calculations.

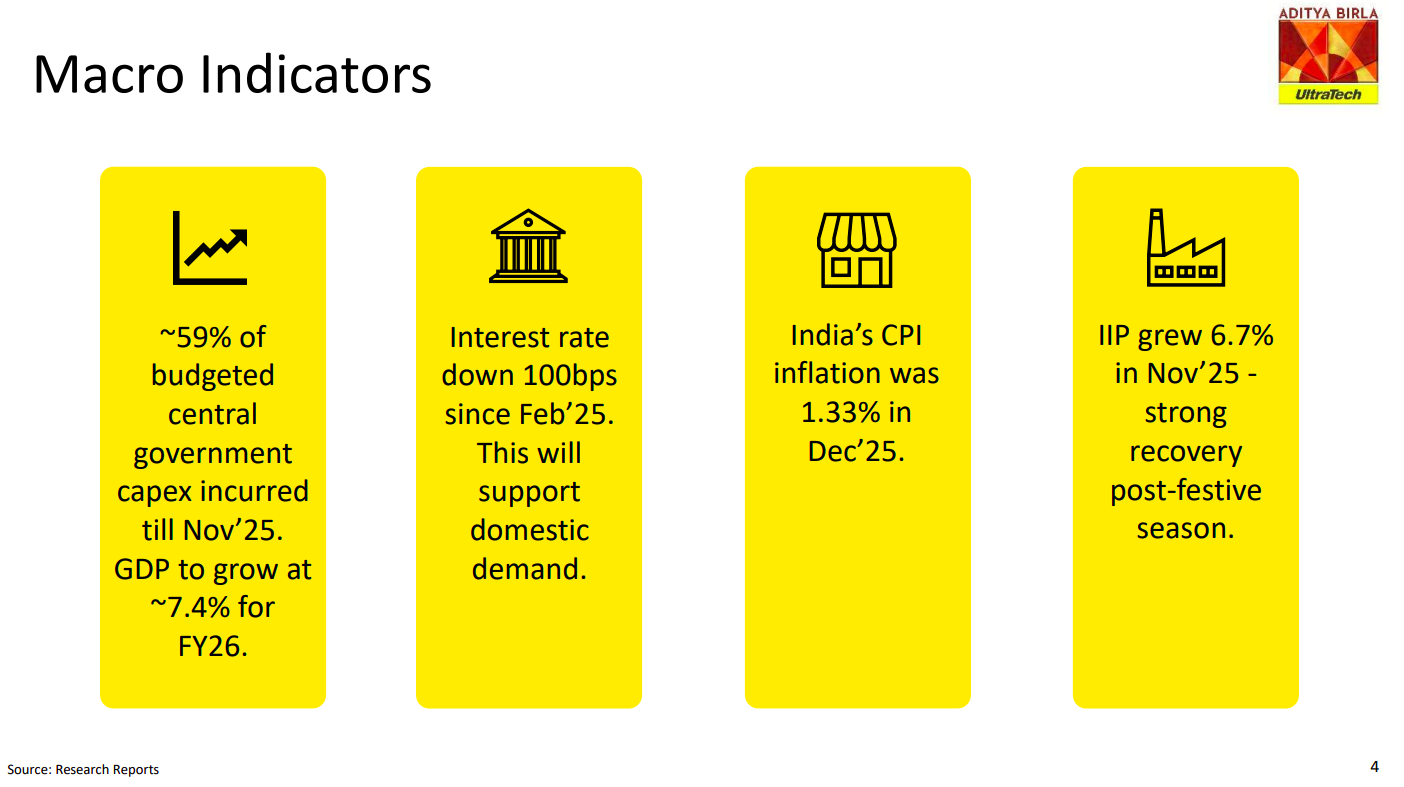

Macro conditions remain supportive with strong government capex execution, easing interest rates, low CPI inflation, and improving industrial activity. These factors are expected to sustain construction demand momentum into FY26.

Dalmia Bharat | Mid Cap | Building Materials

Dalmia Bharat Limited is a prominent cement company in India known for its innovation, excellence, and sustainability. With a focus on low cost and eco-friendly practices, it contributes to national development through quality products and advanced sustainability initiatives. The company offers a diverse product range driven by cutting-edge R&D, emphasizing innovation, quality, and environmental responsibility. Serving both individual consumers and institutional clients, it specializes in tailored cement solutions for unique engineering and construction requirements.

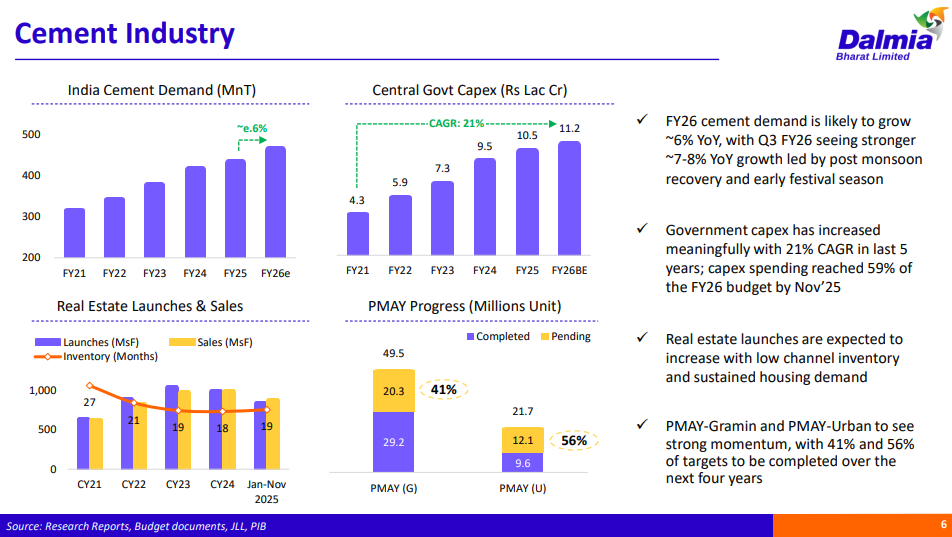

Cement demand is expected to grow around 6% year-on-year in FY26, with Q3 showing stronger momentum thanks to the monsoon recovery and festival season. Government spending on infrastructure has been climbing steadily—capex grew at 21% CAGR over the last five years and made up 59% of the FY26 budget by November 2025. On the housing front, real estate launches are picking up as inventory levels drop, and government housing schemes like PMAY-Gramin and PMAY-Urban are making solid progress, with 41% and 56% of their targets already completed.

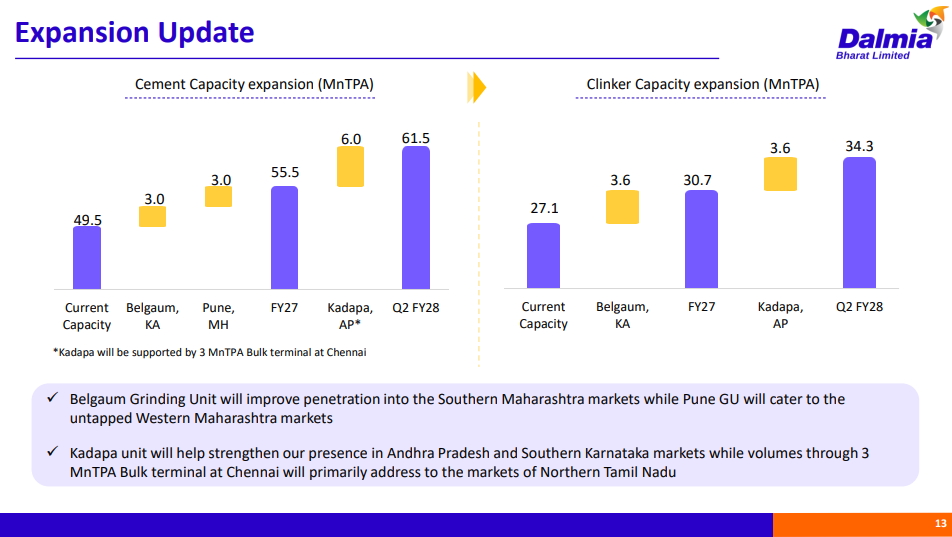

Dalmia Bharat is ramping up both cement and clinker capacity through multiple expansions. Current cement capacity of 49.5 MnTPA will jump to 61.5 MnTPA by Q2 FY28, with new units coming up in Belgaum and Pune in Karnataka and Maharashtra, plus a major expansion in Kadapa, Andhra Pradesh. On the clinker side, capacity will grow from 27.1 MnTPA to 34.3 MnTPA over the same period. The Belgaum grinding unit targets southern Maharashtra, while Pune focuses on untapped western Maharashtra markets, and the Kadapa unit—supported by a 3 MnTPA bulk terminal in Chennai—will strengthen their presence in Andhra Pradesh, southern Karnataka, and northern Tamil Nadu.

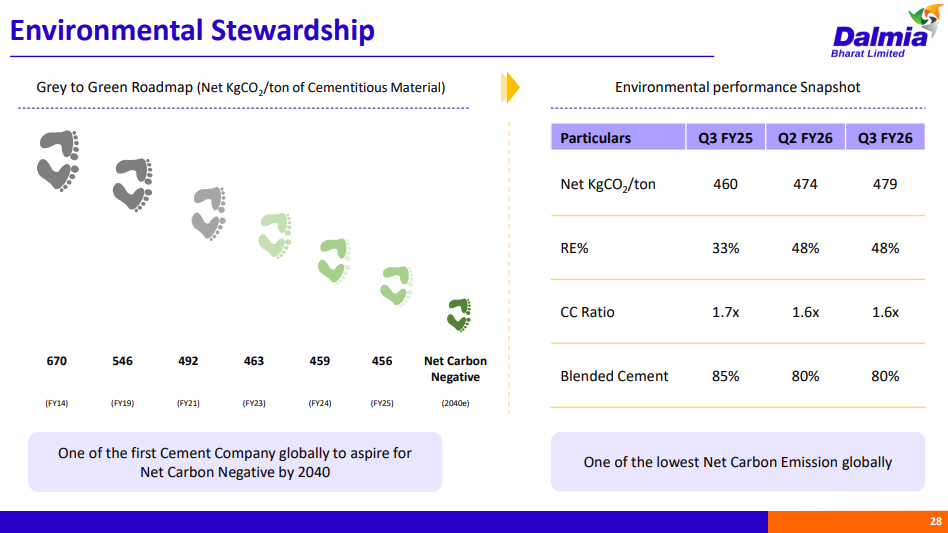

Dalmia Bharat is working toward becoming net carbon negative by 2040, with emissions already dropping from 670 kg CO₂/ton in FY14 to 456 kg CO₂/ton in FY25. Recent quarterly performance shows net emissions have improved from 460 kg CO₂/ton in Q3 FY25 to 479 kg CO₂/ton in Q3 FY26. The company has increased its renewable energy mix to 48% and maintained a clinker-to-cement ratio of 1.6x, while keeping blended cement at 80% of production. These numbers place Dalmia among the lowest carbon emitters globally in the cement industry.

Engineering & Capital Goods

Premier Energies | Mid Cap | Engineering & Capital Goods

Premier Energies trades solar modules, cells, wafers, and accessories while also undertaking construction projects. The company is expanding into aluminium frames, inverters, and battery storage systems to enhance its integrated product offerings. This diversification supports its goal of becoming a comprehensive clean technology platform, improving profitability and supply chain resilience.

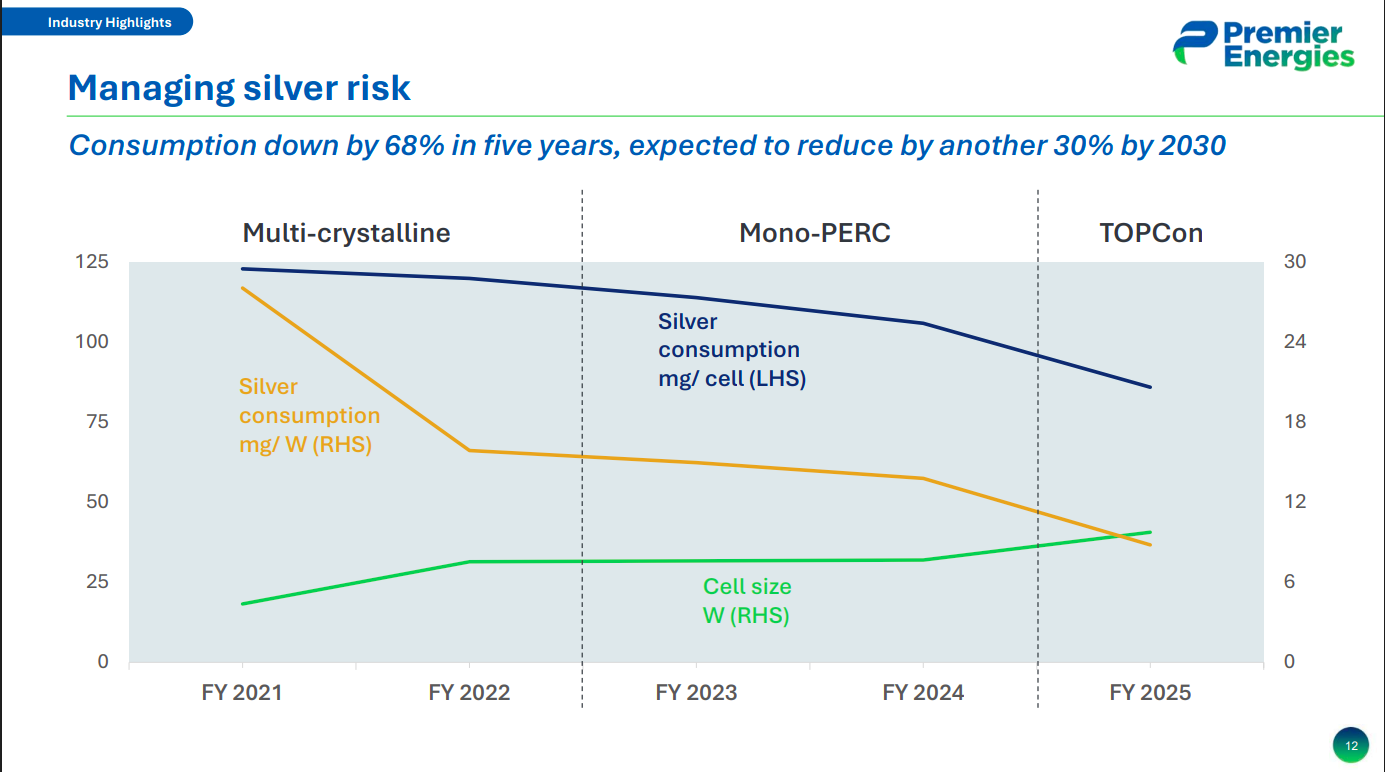

Silver consumption per solar cell has fallen sharply (~68% over five years) due to technology shifts from multi-crystalline to Mono-PERC and TOPCon. Ongoing efficiency gains and larger cell sizes are expected to reduce silver usage by another ~30% by 2030, lowering cost volatility risk.

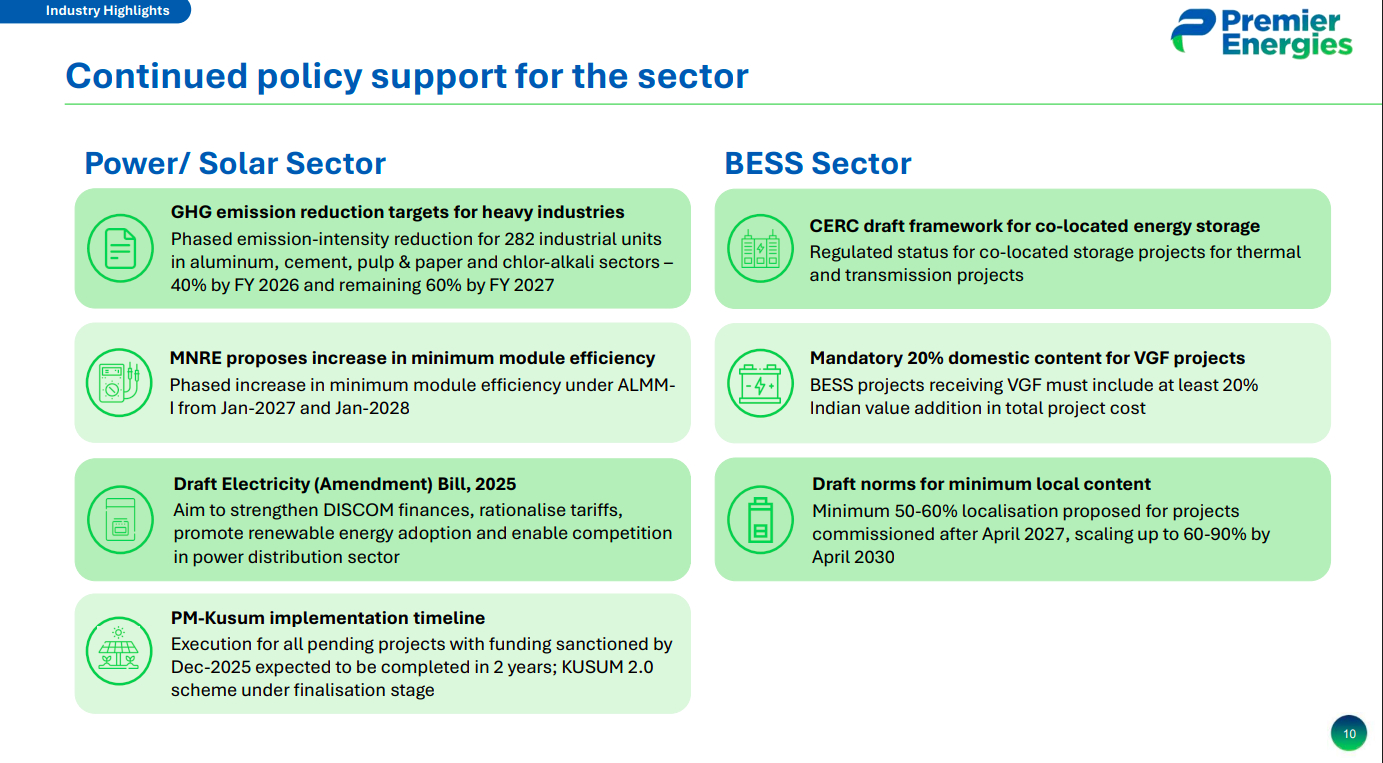

Strong regulatory backing across solar and BESS is driving long-term visibility, including tighter emission norms, higher module efficiency standards, and DISCOM reforms. Domestic content mandates and localisation targets further strengthen India’s renewable manufacturing ecosystem.

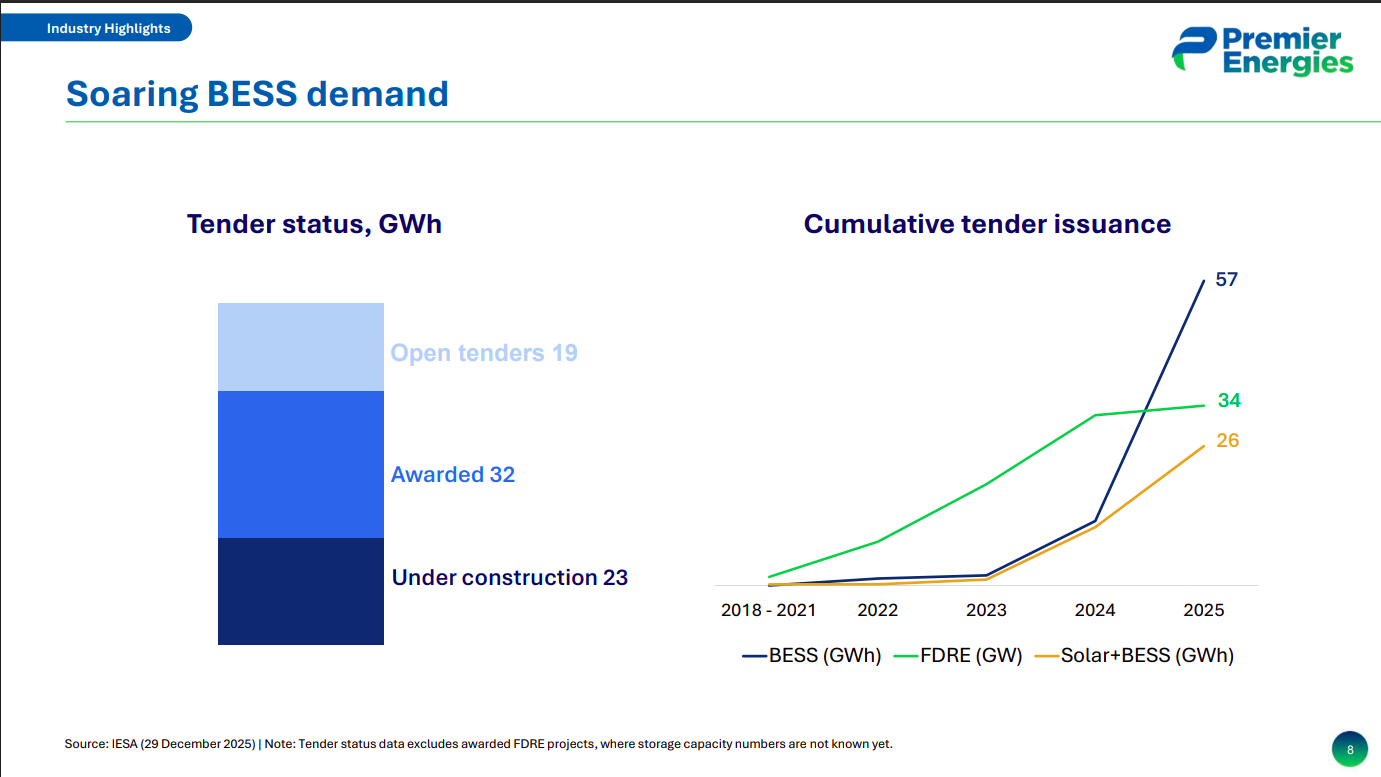

Battery energy storage demand is accelerating rapidly, with cumulative tenders scaling sharply and a healthy pipeline across awarded, under-construction, and open projects. Growth is being driven by FDRE tenders and solar-plus-storage deployments.

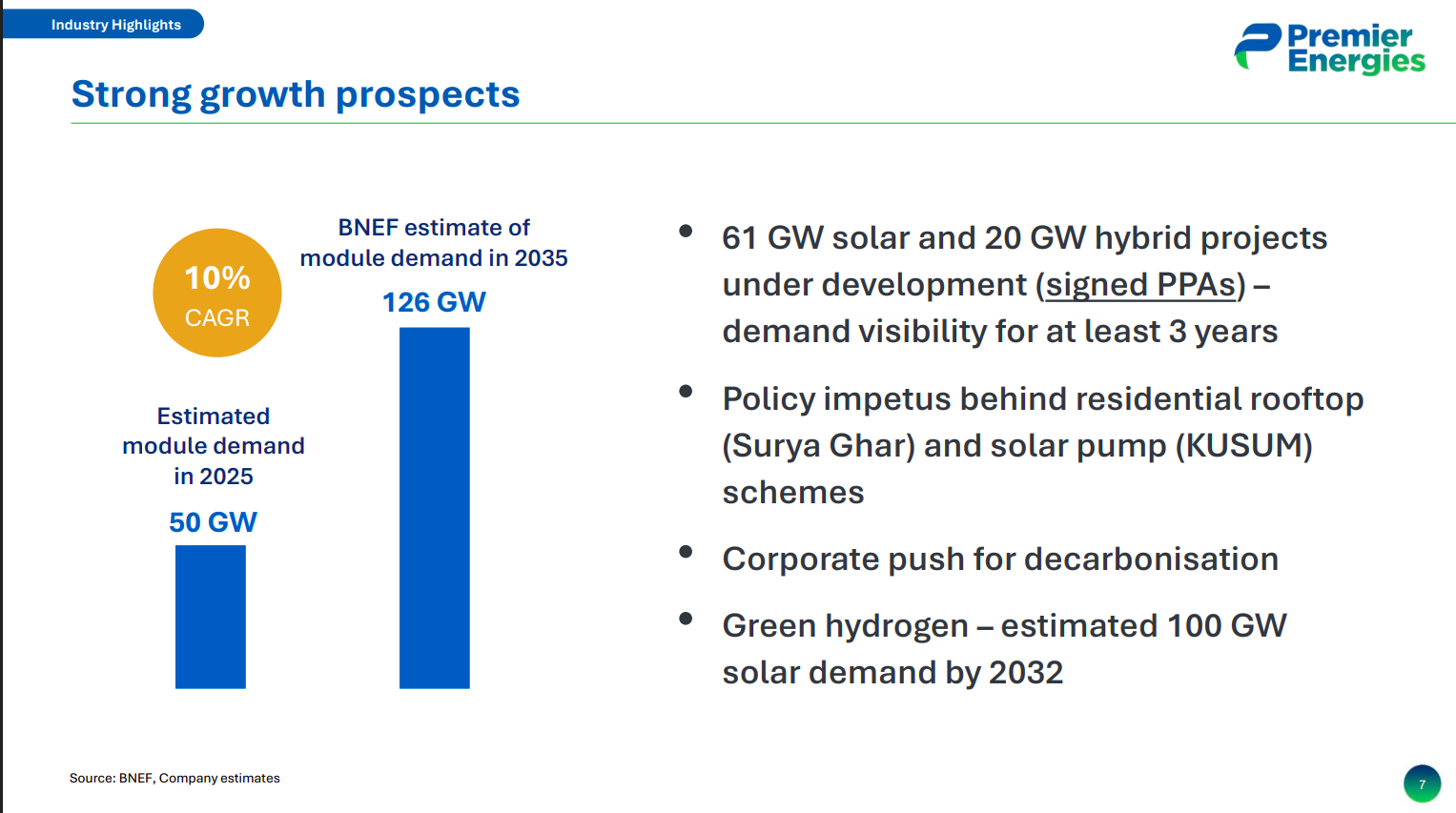

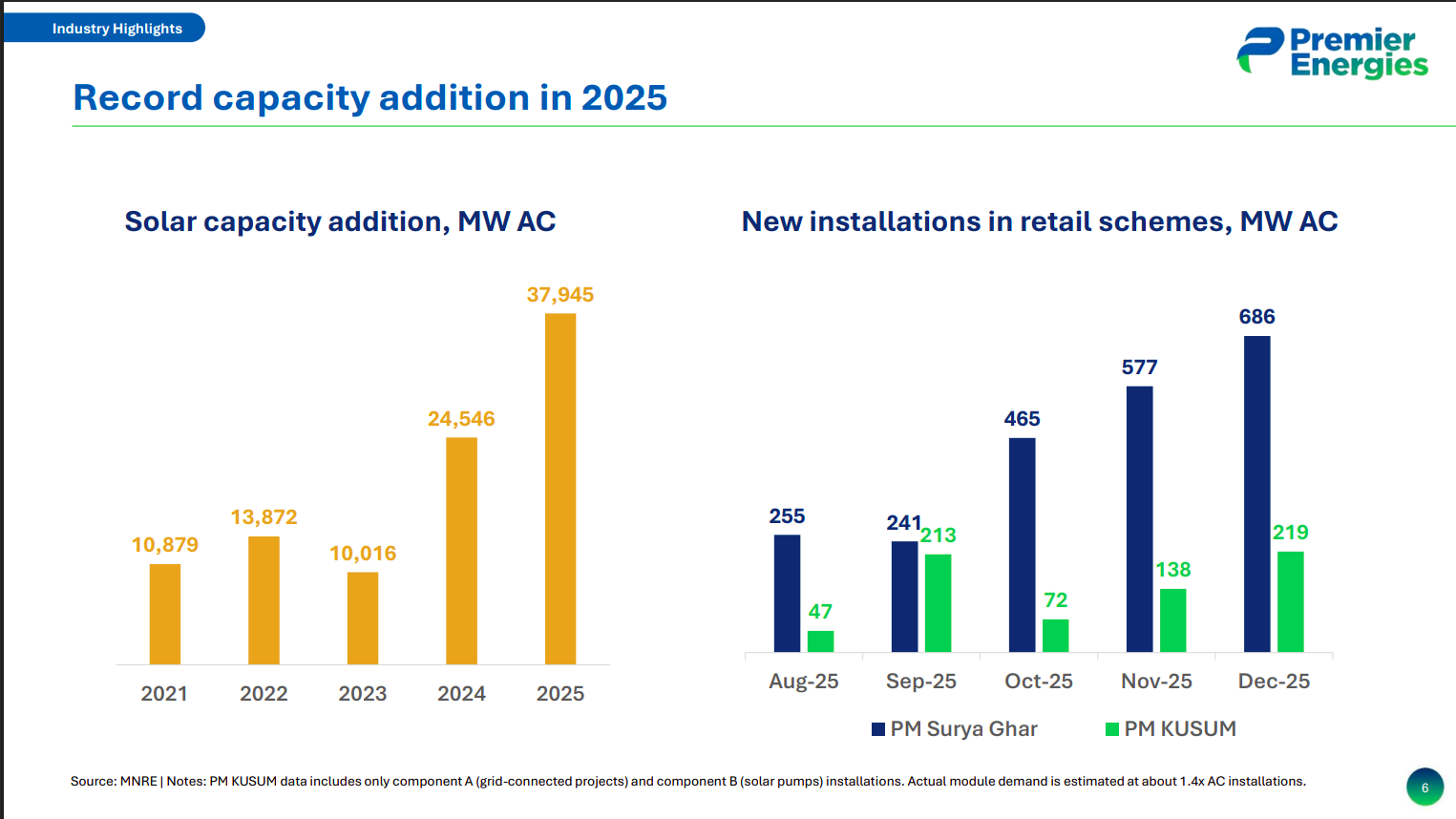

India’s solar module demand is expected to grow at ~10% CAGR, rising from ~50 GW in 2025 to ~126 GW by 2035. Signed PPAs, rooftop solar schemes, decarbonisation commitments, and green hydrogen projects provide multi-year demand visibility.

India added a record ~38 GW of solar capacity in 2025, marking a sharp acceleration versus prior years. Retail schemes like PM Surya Ghar and PM KUSUM are gaining momentum, driving sustained module demand into 2026.

Textiles

Borana Weaves | Micro Cap | Textiles

Borana Weaves, a textile manufacturer in Surat, specializes in producing unbleached synthetic grey fabric. This fabric is a crucial material for industries like fashion, traditional textiles, technical textiles, home decor, and interior design, serving as a base for dyeing and printing processes.

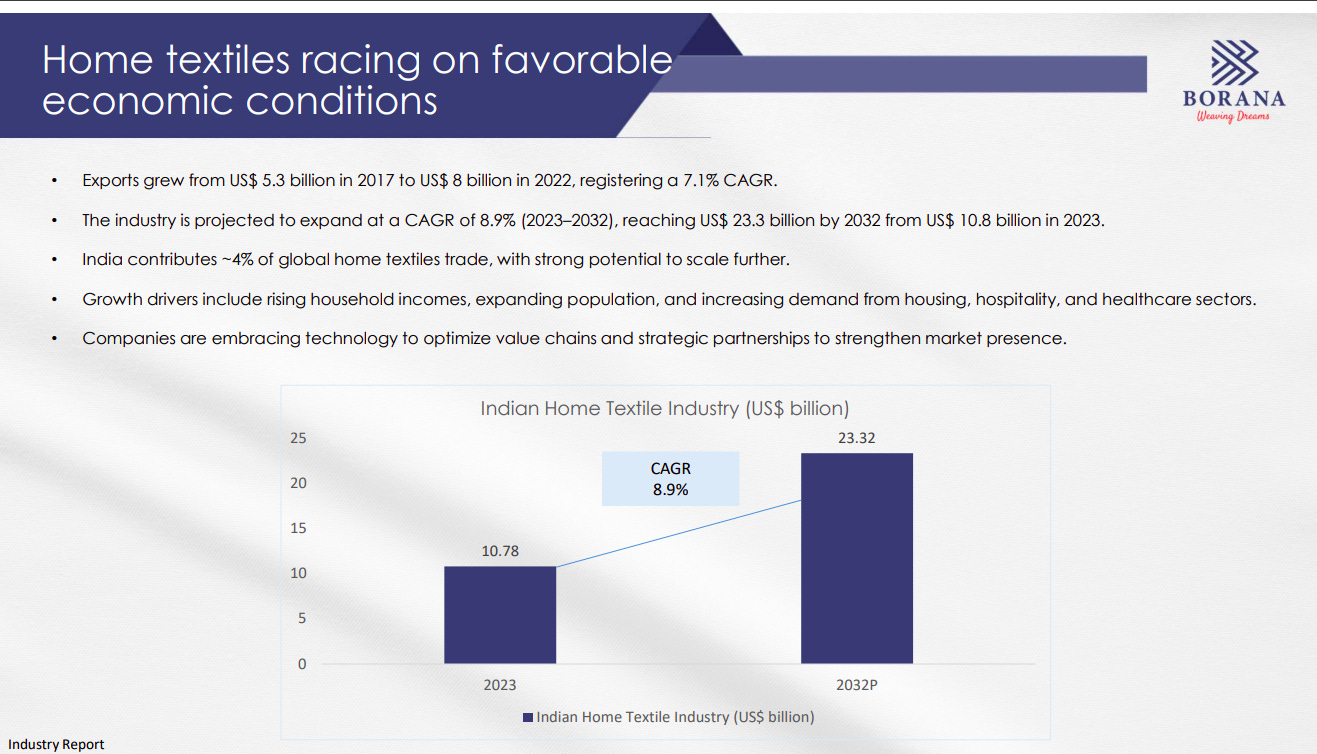

India’s home textile industry is scaling rapidly, with exports growing at ~7% CAGR and the market projected to reach US$23.3 bn by 2032 at ~8.9% CAGR. Rising incomes, housing, hospitality, and healthcare demand are key growth drivers.

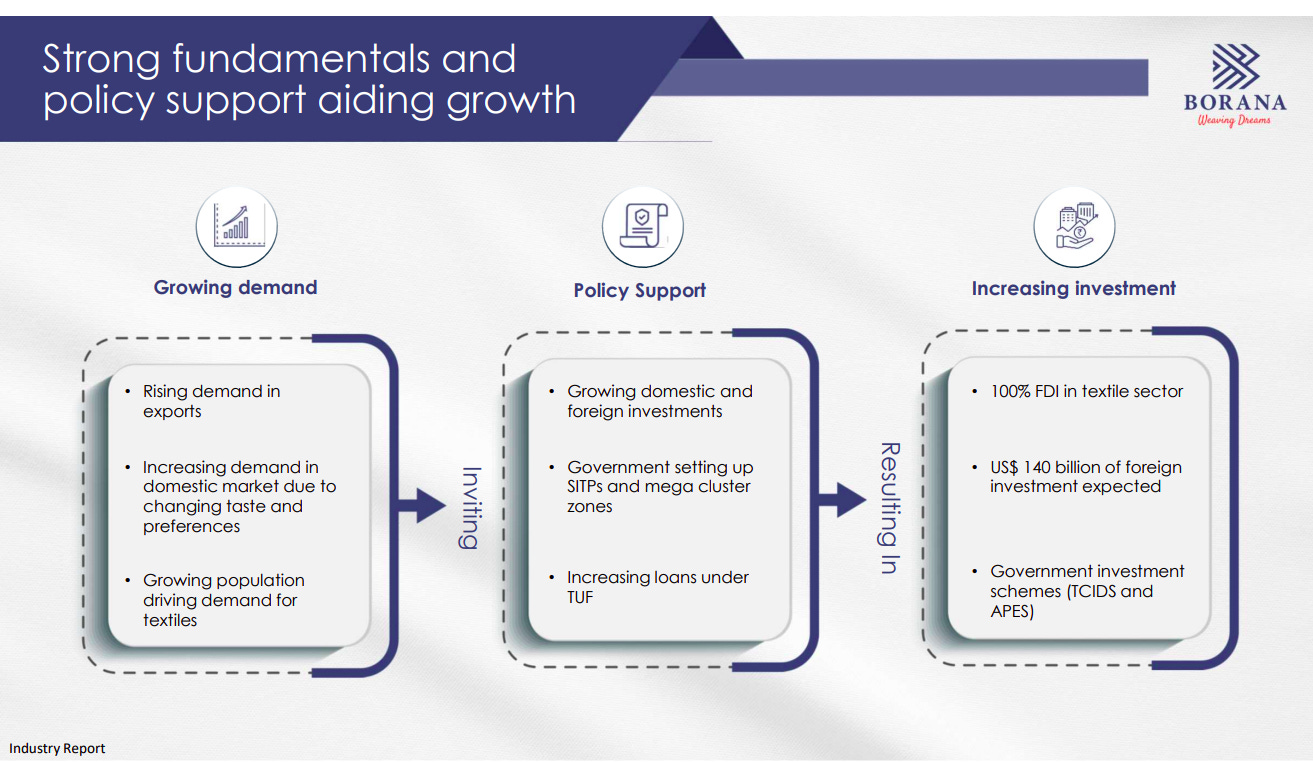

Growth is supported by rising export and domestic demand, backed by government initiatives like SITPs, mega clusters, and easier access to finance. Policy support and 100% FDI are driving sustained investment inflows into the textile sector.

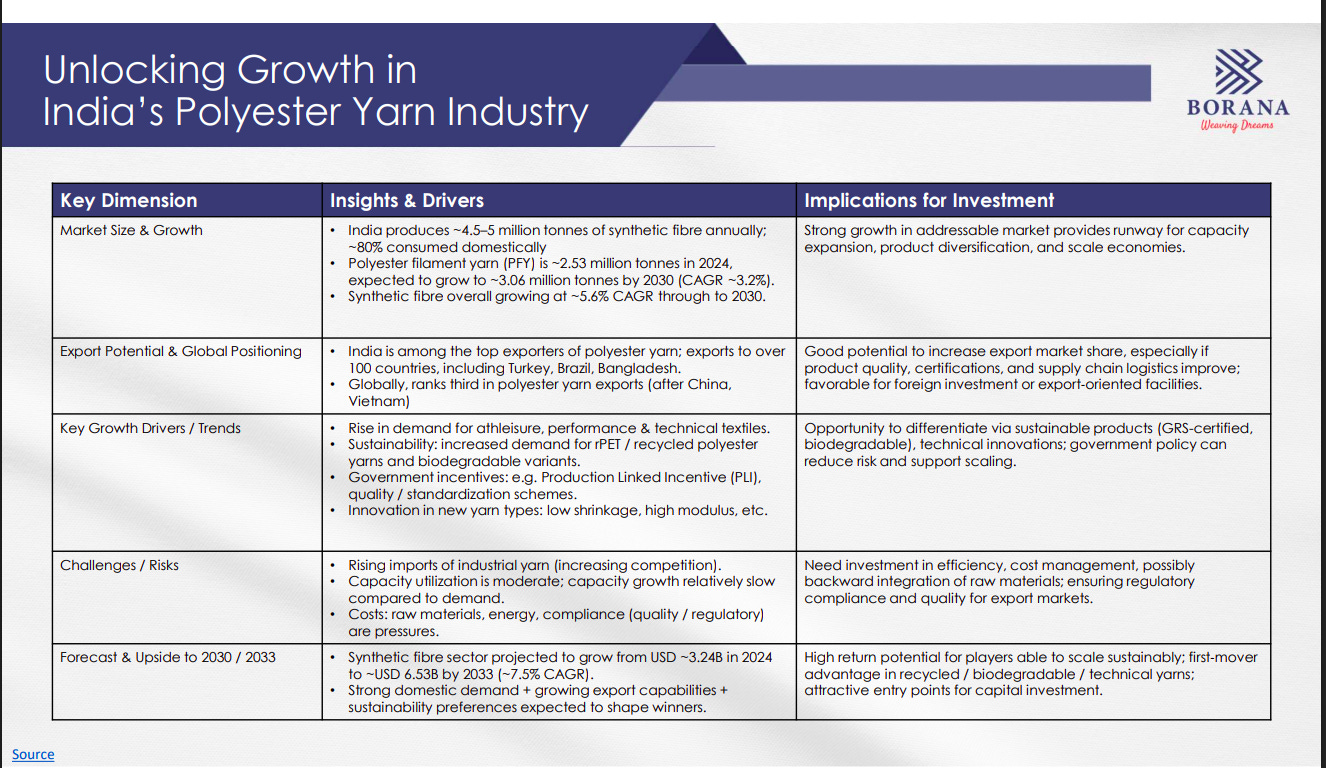

India is a leading global producer and exporter of polyester yarn, with steady demand growth driven by athleisure, technical textiles, and sustainability trends. Opportunities lie in recycled and specialty yarns, while cost efficiency and scale remain critical.

Borana’s portfolio spans unbleached synthetic greige fabric and PTY yarn, serving apparel, home textiles, and industrial applications. This diversified application base reduces concentration risk and supports stable demand across cycles.

Metals

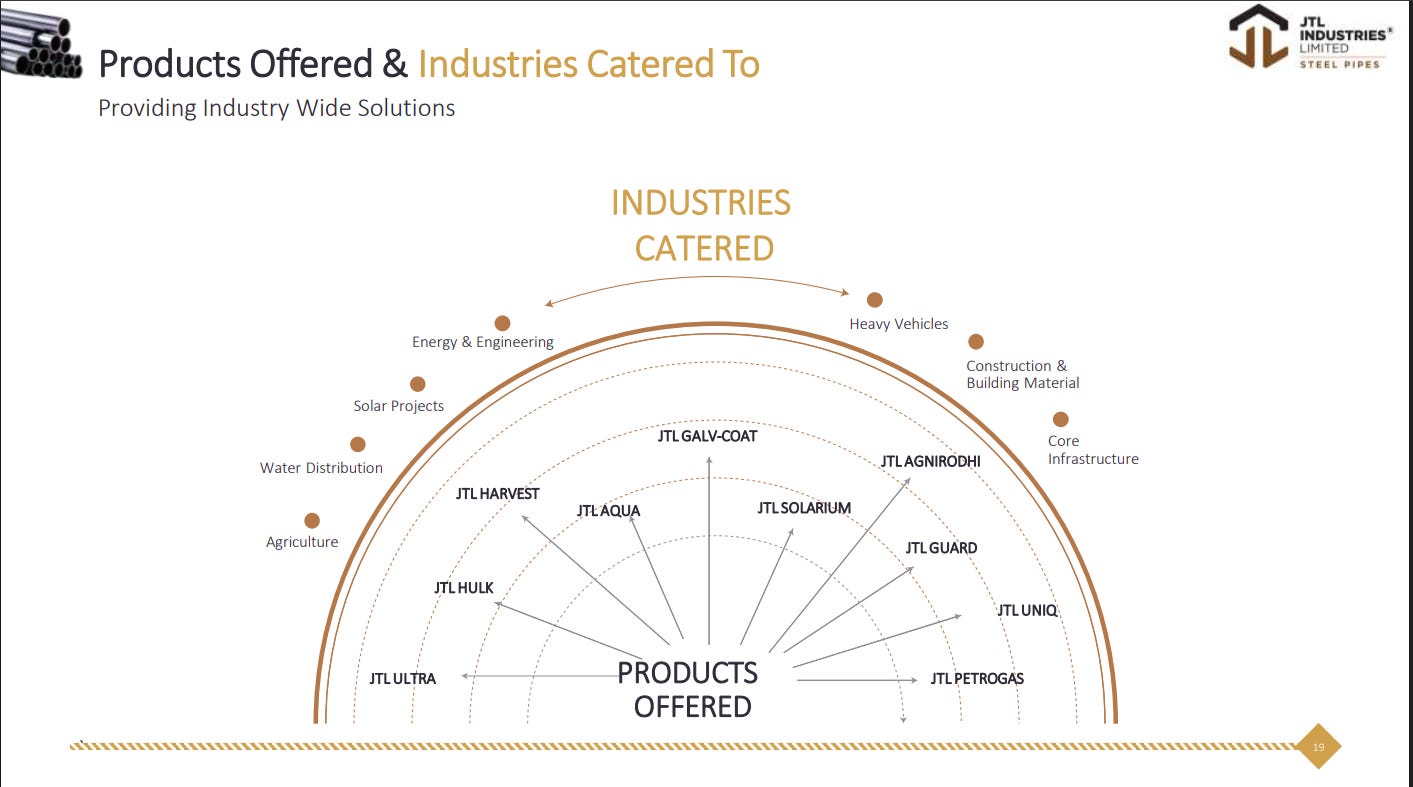

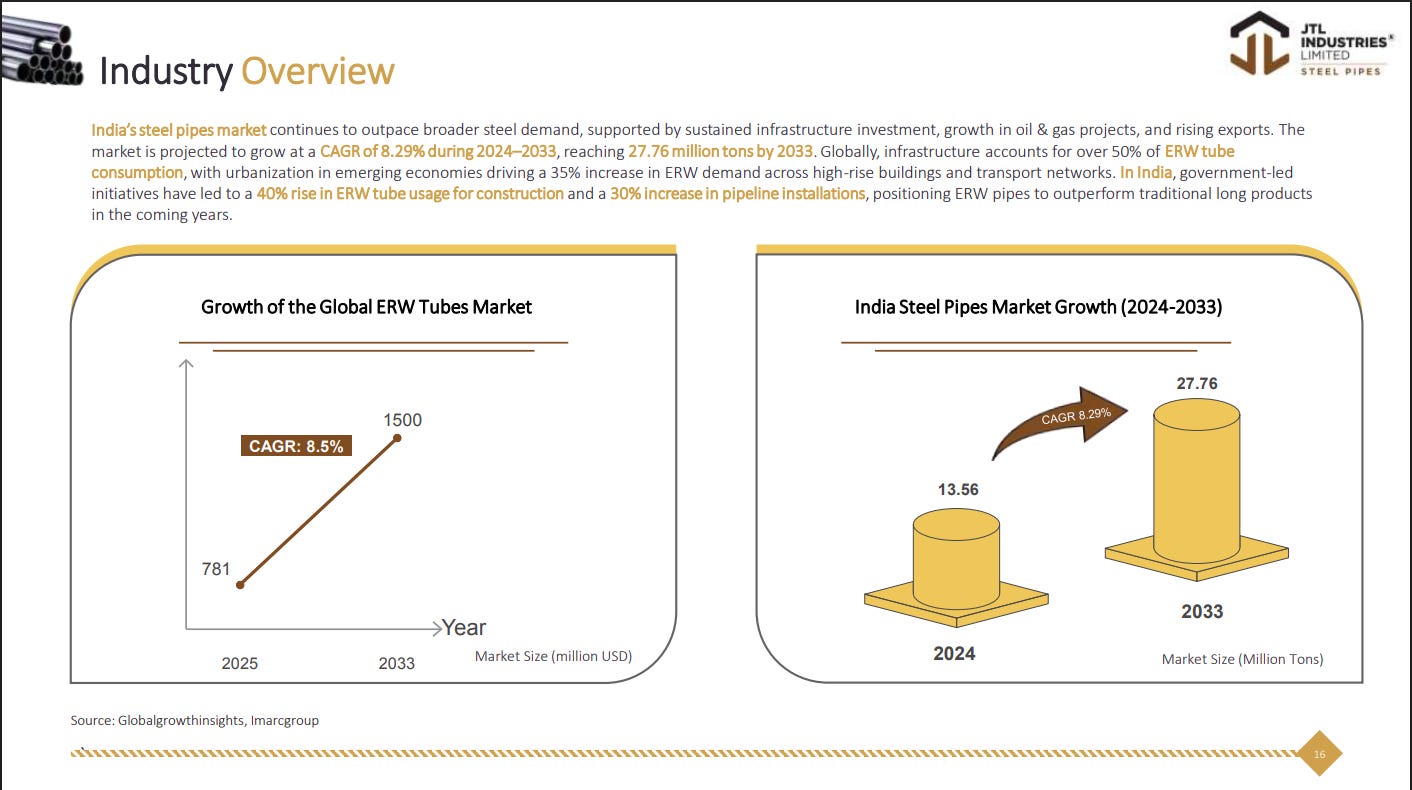

JTL Industries | Small Cap | Metals

JTL Infra Limited, an India-based company, specializes in manufacturing and selling ERW Black and Galvanized steel pipes, Tubes, hollow sections, and structural steel for engineering and construction projects. Their product range includes galvanized steel tubes, scaffolding fittings, hollow sections, LTZ sections, and mild steel angles/channels. They also provide logistics, packaging, quality assurance, and production services.

JTL offers a diversified product portfolio across galvanised, structural, precision, and specialty steel pipes. These products cater to a wide range of industries including infrastructure, construction, energy, agriculture, water, solar, and heavy engineering.

Demand for structural steel tubes is being driven by sustained government-led infrastructure spending across warehousing, metros, airports, water supply, housing, and railways. Large national programs are creating long-term volume visibility for ERW and steel pipe players.

India’s steel pipes market is expected to grow at ~8% CAGR through 2033, outpacing broader steel demand. Strong infrastructure spend, rising ERW adoption in construction and pipelines, and export growth are structural drivers supporting long-term industry expansion.

JTL operates with large-scale manufacturing capacity, supported by backward integration and six modern facilities across India. A strong pan-India and global footprint, wide distributor network, and deep SKU portfolio underpin its leadership in steel pipes.

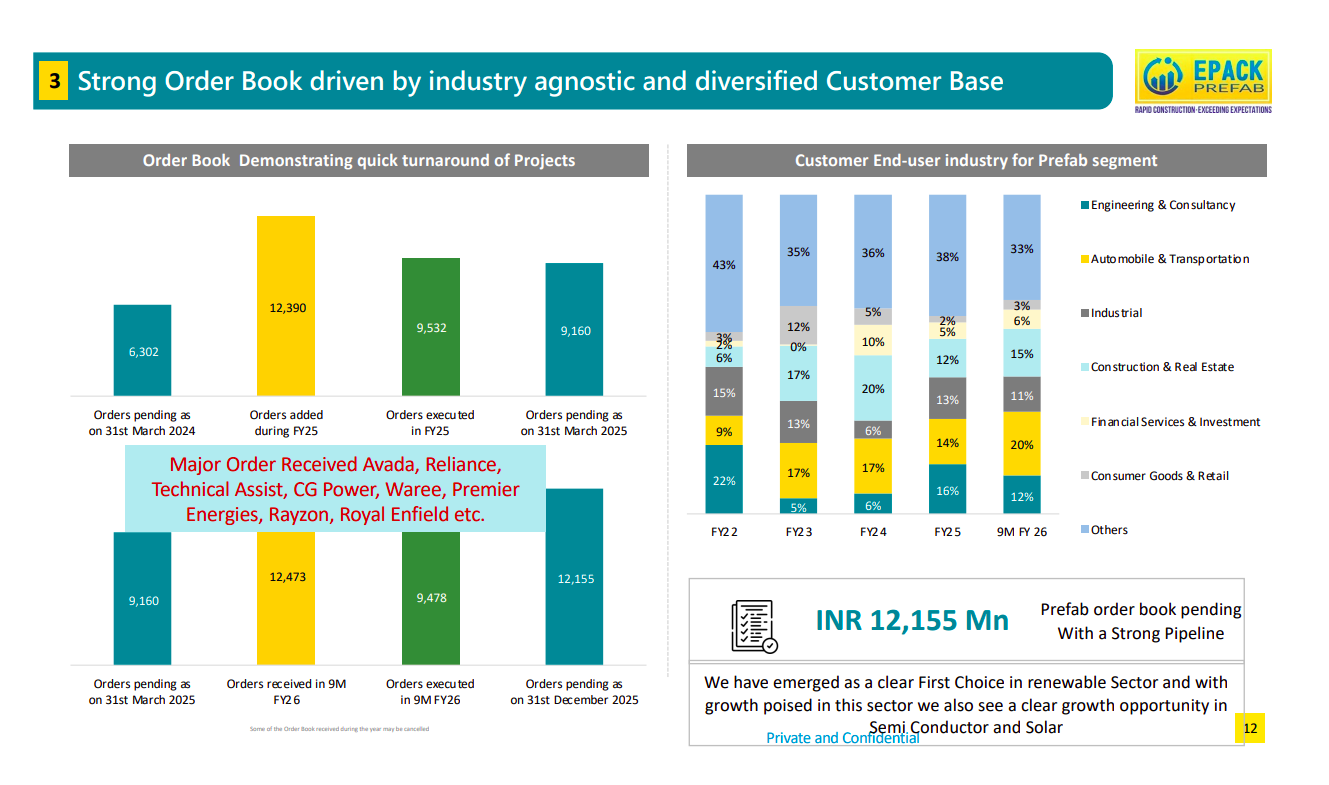

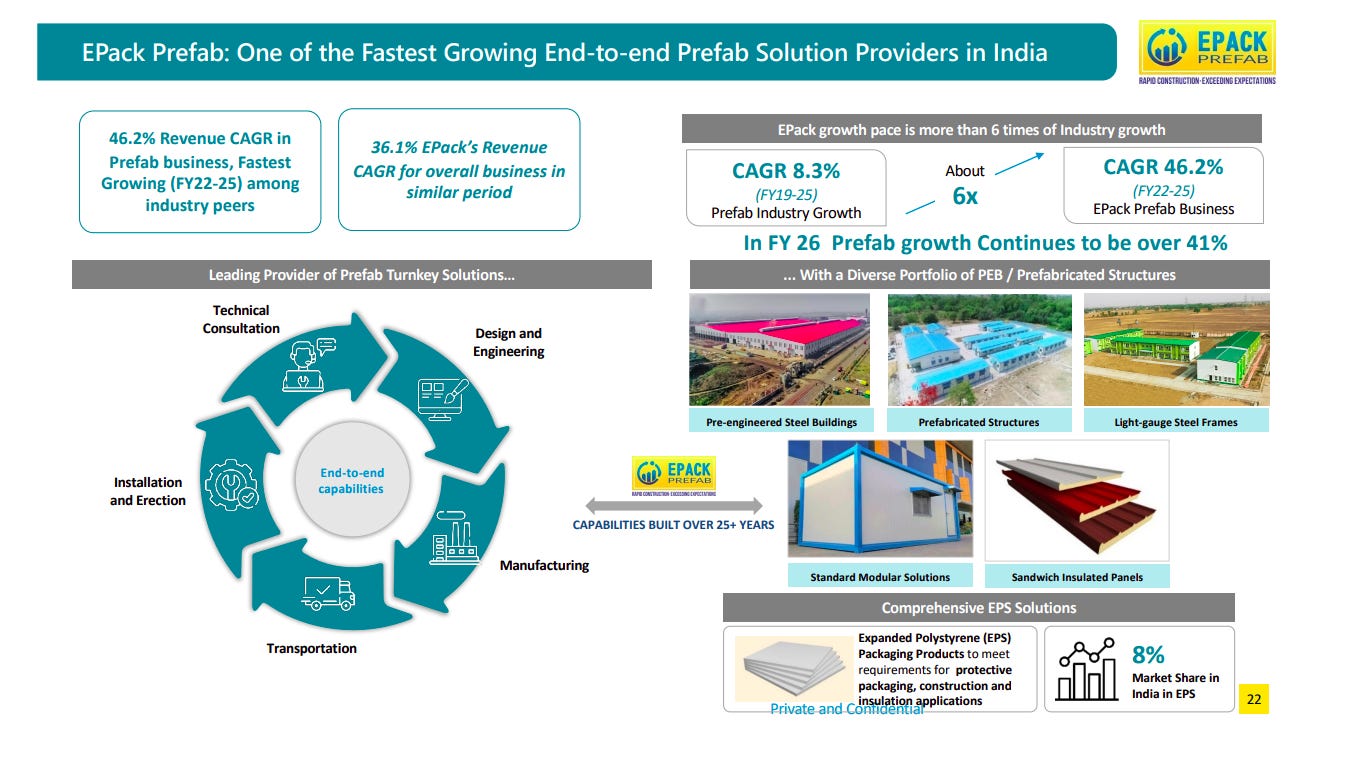

Epack Prefab Technologies | Small Cap | Metals

Epack Prefab Technologies, established in 1999, operates in two key sectors: Pre-Fab and EPS Packaging. It provides turnkey solutions for pre-engineered steel buildings and structures, and manufactures EPS products for insulation and packaging. With multiple manufacturing units and design centres, the company serves industries such as construction, packaging, and consumer goods, delivering high-quality, cost-effective solutions worldwide.

EPack Prefab’s order book reflects fast project execution and strong repeat demand across industries, with orders added and executed quickly each year. A diversified end-user mix and marquee clients support a robust pending order book of ₹12,155 mn and a strong pipeline.

EPack has delivered ~46% revenue CAGR in its prefab business (FY22–25), far outpacing industry growth. Its end-to-end turnkey capabilities and wide prefab portfolio position it as a scaled, integrated solutions provider.

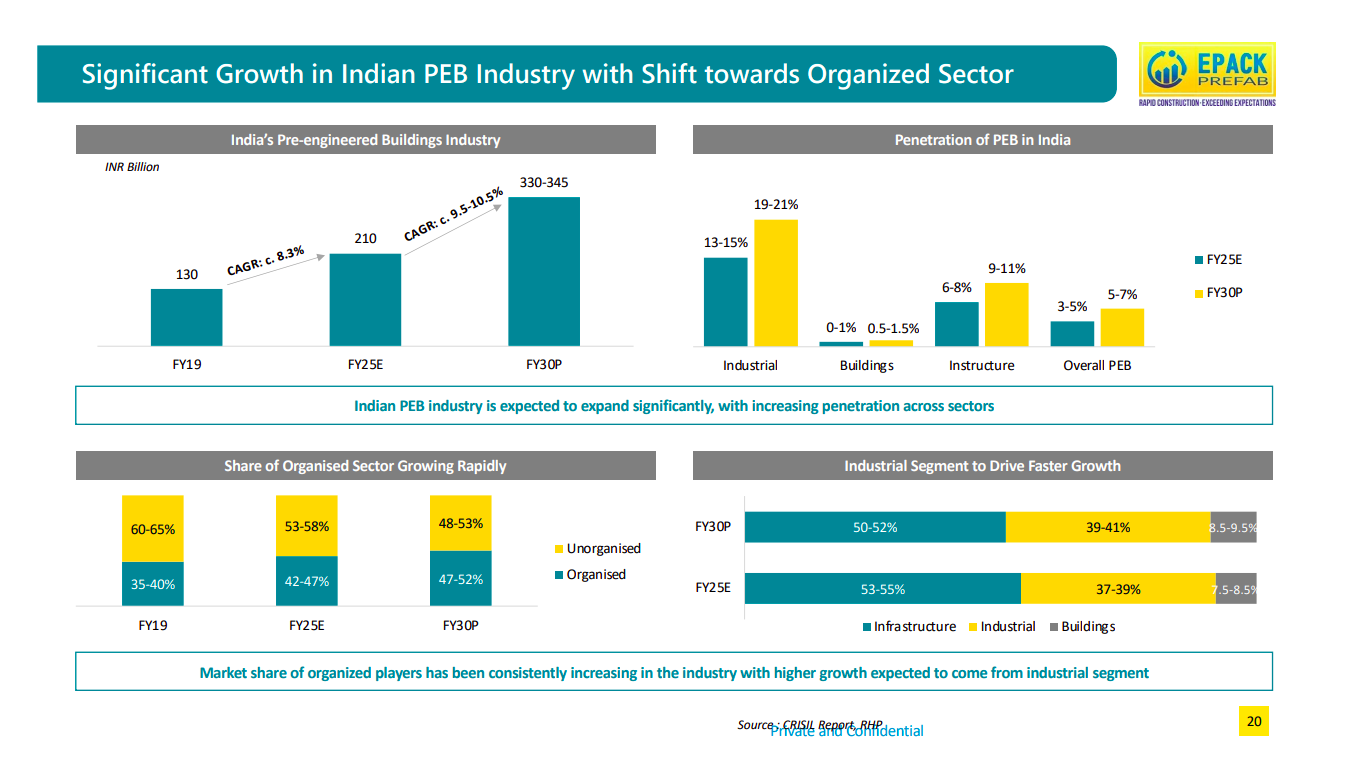

India’s PEB market is set for strong expansion with rising penetration across industrial, infrastructure, and building segments. The shift toward organized players is accelerating, with industrial applications expected to be the key growth driver.

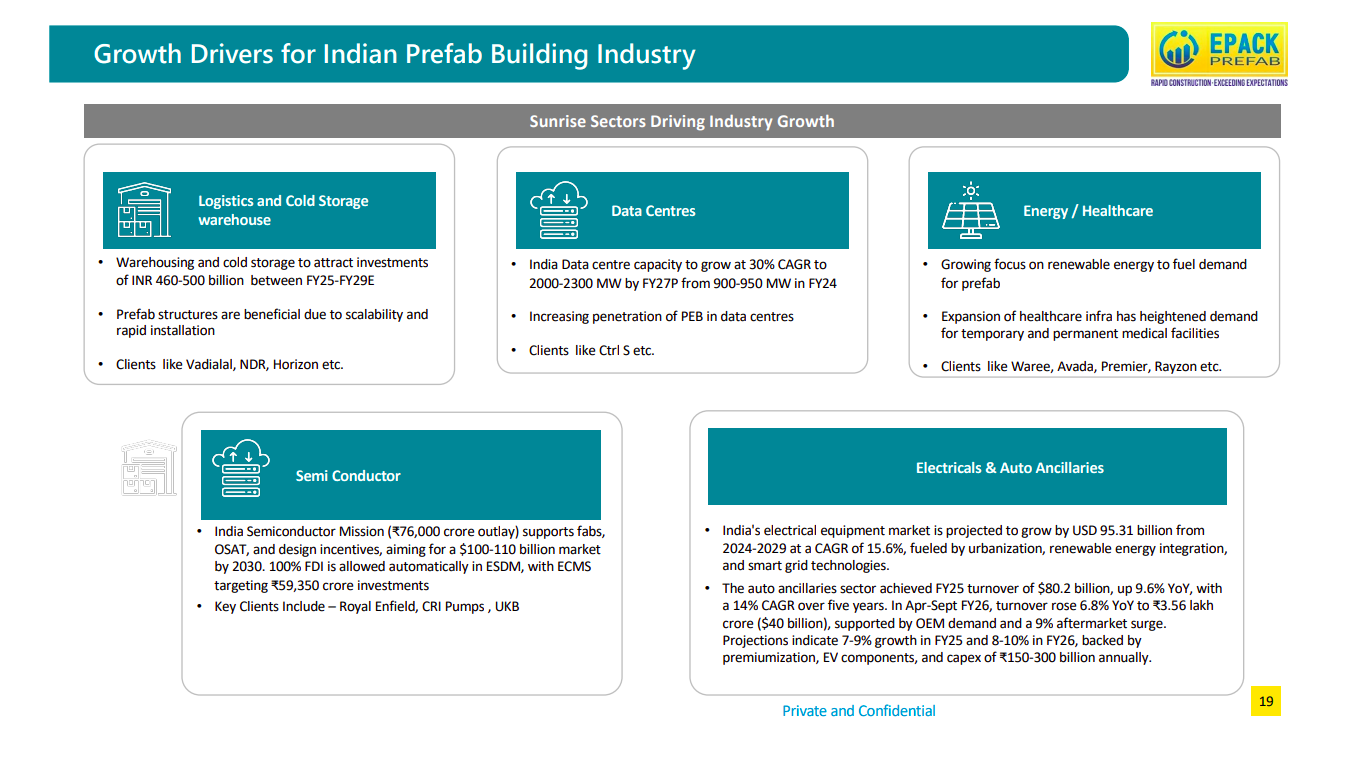

Sunrise sectors like logistics & cold storage, data centres, renewables, healthcare, semiconductors, and auto ancillaries are driving prefab demand. Prefab solutions benefit from faster execution, scalability, and alignment with India’s capex and infrastructure push.

EPack offers a wide range of prefab solutions including PEBs, prefabricated structures, sandwich panels, LGSF, modular units, and EPS packaging. This broad product mix enables it to address varied use cases across industrial, commercial, and infrastructure projects.

Retail

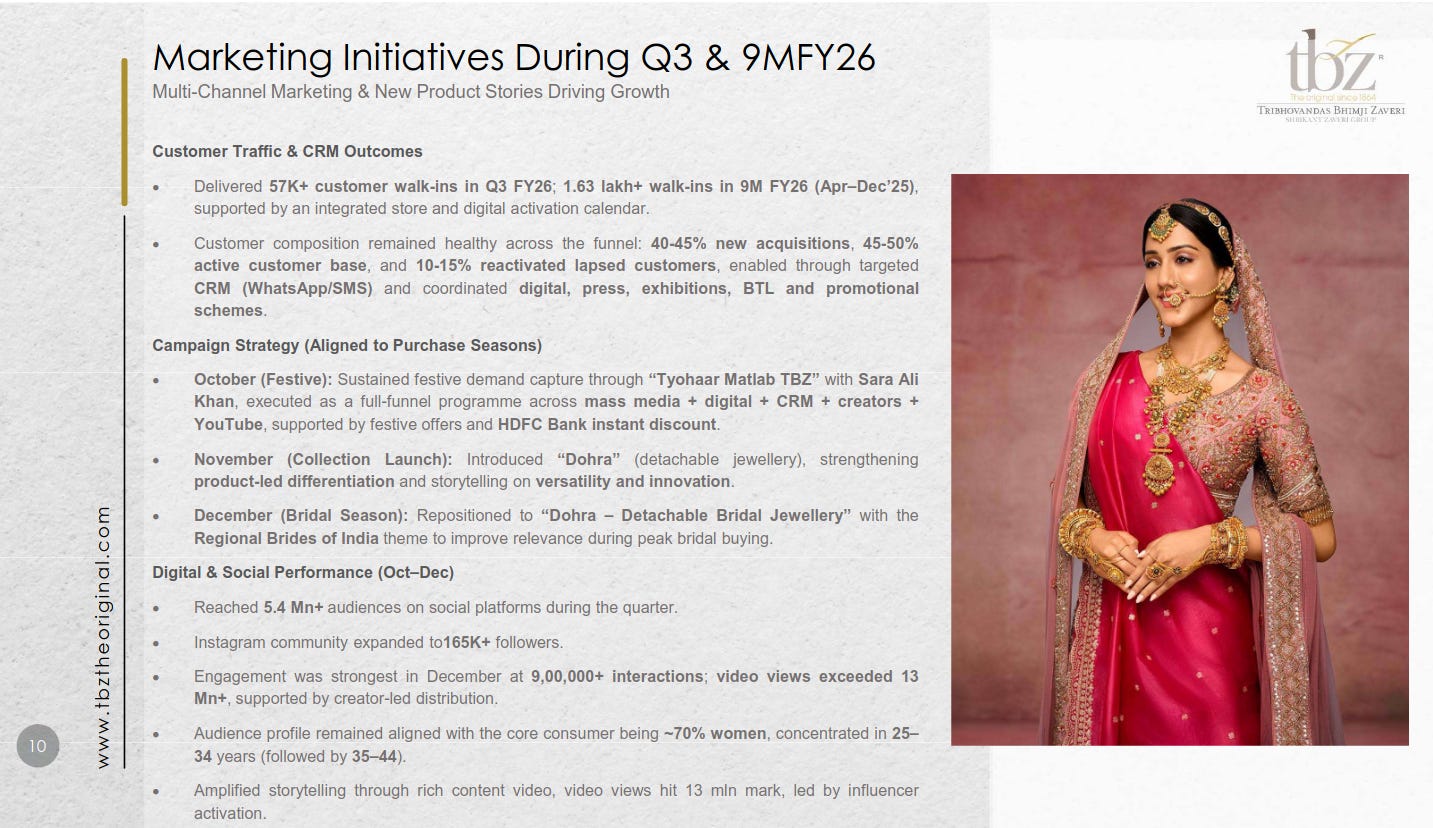

Tribhovandas Bhimji Zaveri Limited (TBZ) | Micro Cap | Retail

Tribhovandas Bhimji Zaveri Limited (TBZ) is one of India’s oldest jewellery houses. With a pan-India presence, TBZ is known for its jewellery for weddings, celebrations, and everyday wear for young India.

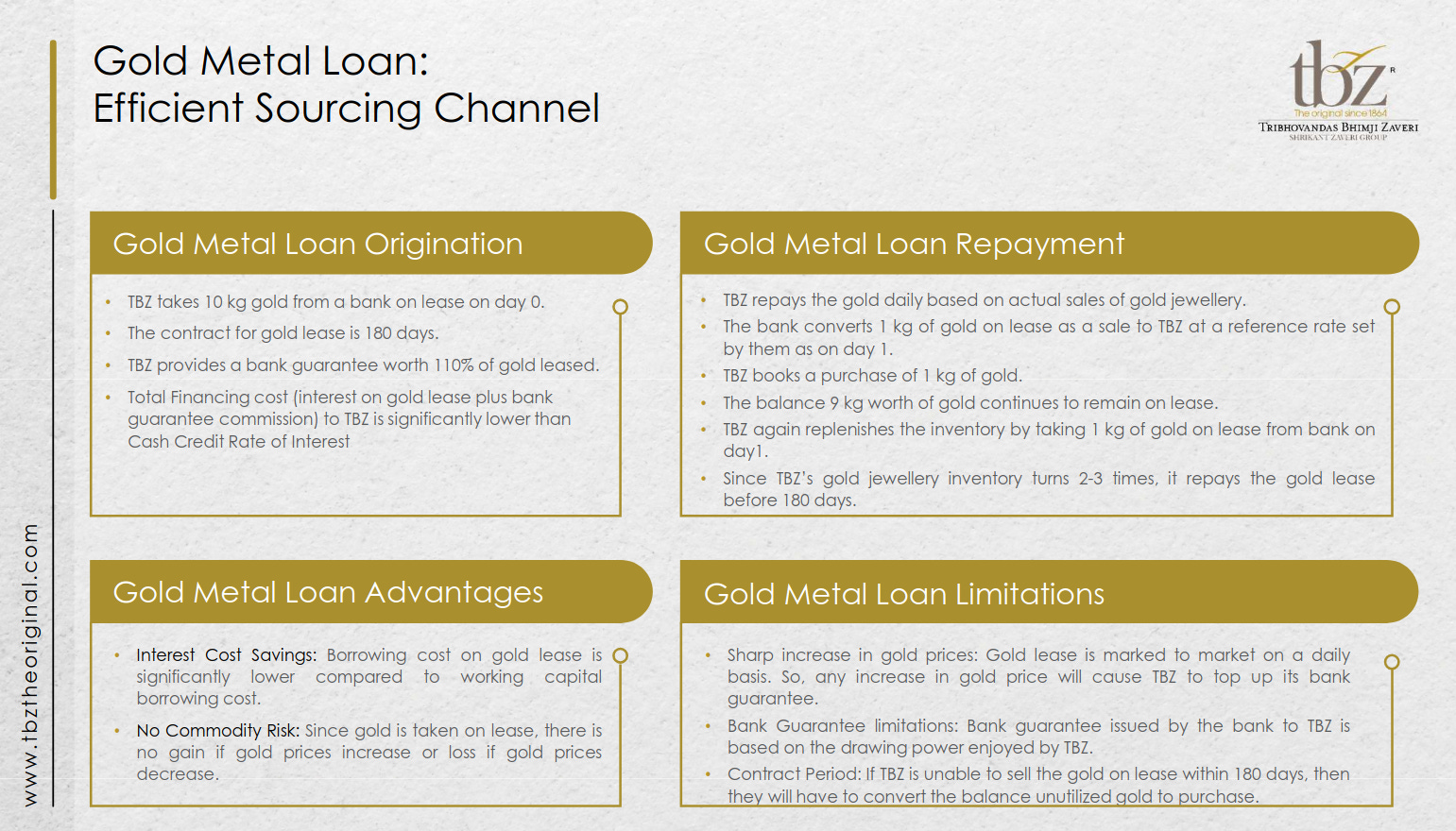

TBZ uses gold metal loans to source inventory at a lower financing cost than cash credit, backed by bank guarantees and short lease cycles. Daily repayment is linked to jewellery sales, allowing faster inventory turns and early lease closure, though sharp gold price moves can increase collateral requirements.

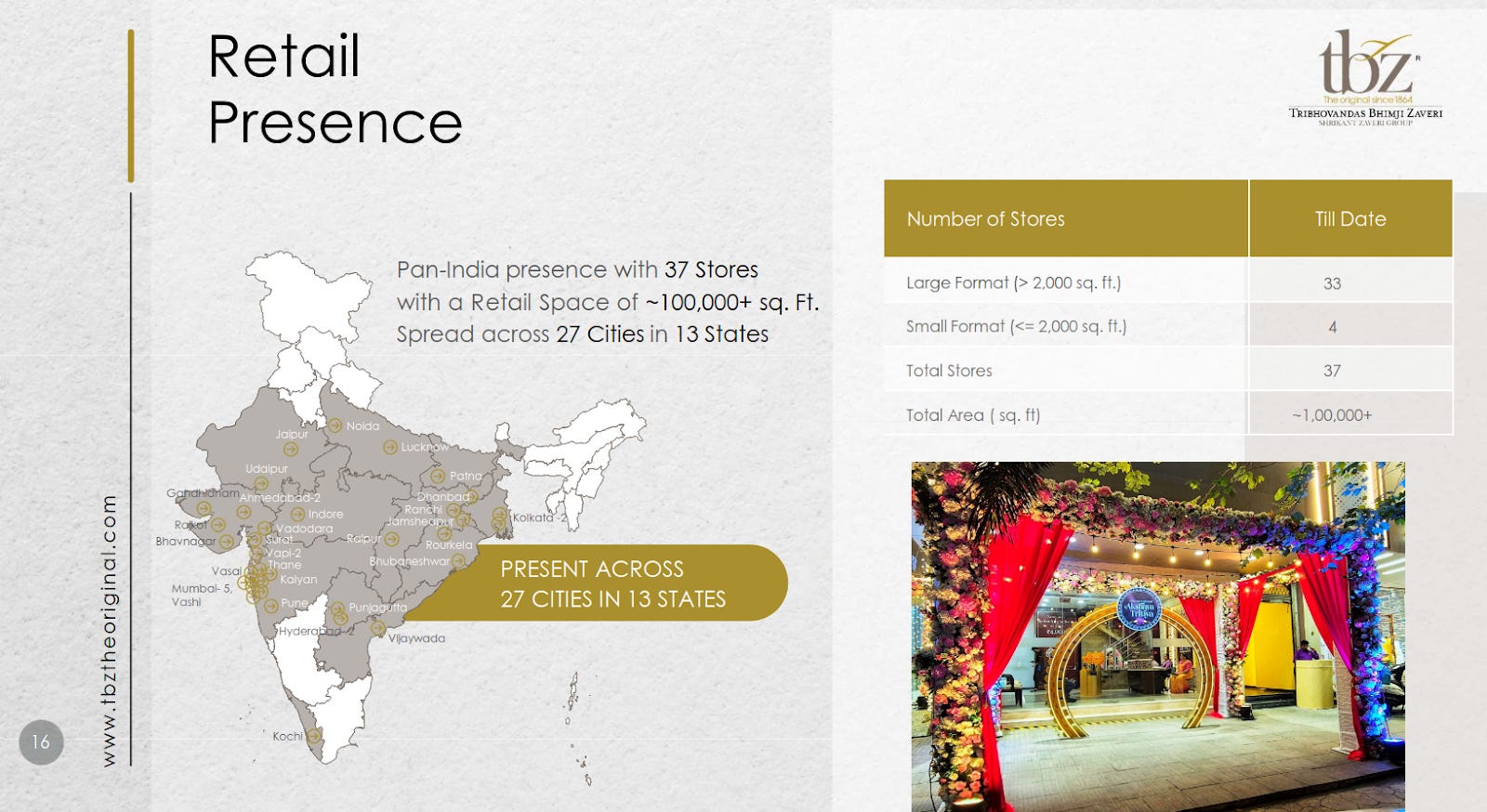

TBZ has a pan-India footprint with 37 stores across 27 cities in 13 states, covering over ~1,00,000 sq. ft. of retail space. The network is largely large-format stores, reinforcing brand visibility and scale in key jewellery markets.

Multi-channel festive and bridal campaigns drove strong footfalls (57K+ in Q3; 1.63 lakh+ in 9M), supported by CRM, digital, and influencer-led storytelling. New product launches and festive branding boosted reach, engagement, and relevance during peak buying seasons.

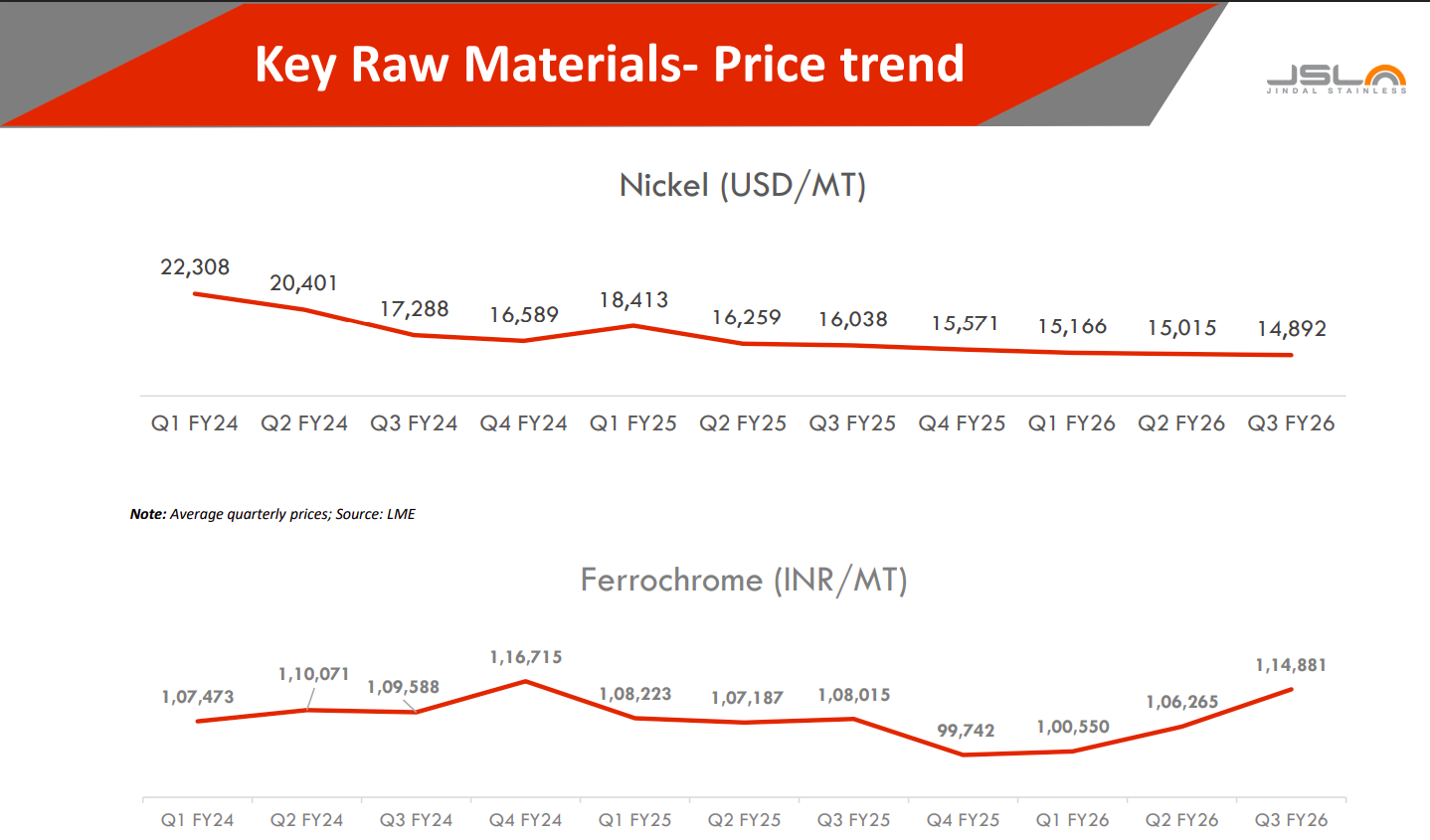

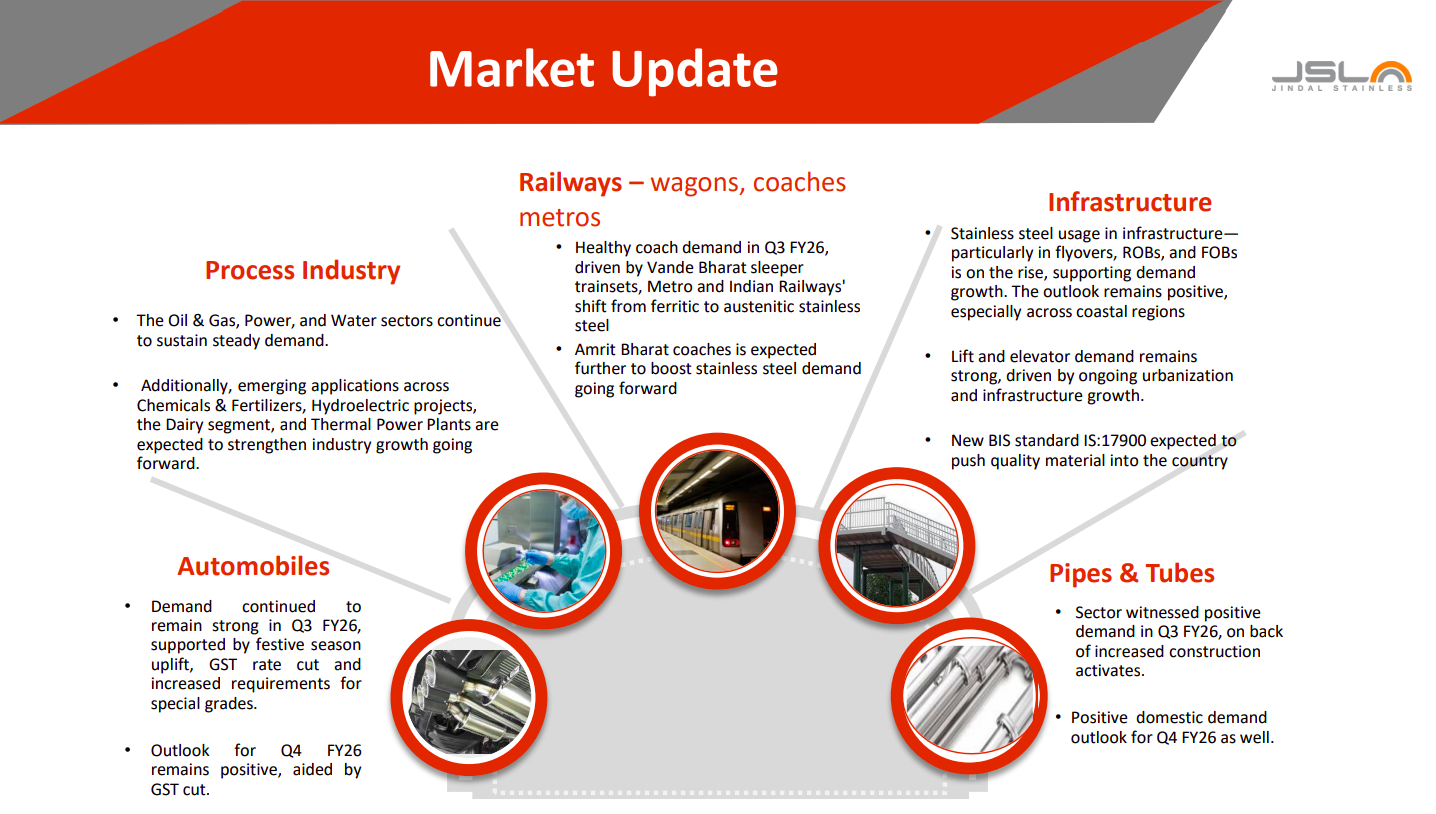

Jindal Stainless | Mid Cap | Metals

Jindal Stainless Limited (JSL) is a major stainless steel conglomerate in India and globally. Established in 1970, it leads in digital transformation in manufacturing through advanced technology solutions. As India’s largest producer of various stainless steel series, it offers a wide range of stainless steel products like coils, plates, sheets, and more.

Nickel prices have trended down steadily from FY24 highs, reflecting global oversupply and softer demand, easing raw material pressure for stainless steel producers. Ferrochrome prices remained volatile, dipping in FY25 before recovering into Q3 FY26, indicating some cost normalization but with recent upward momentum.

Stainless steel demand remained healthy in Q3 FY26 across railways, infrastructure, automobiles, and process industries, supported by government-led capex and urbanization. Railways and infrastructure continue to be key growth drivers, while pipes & tubes and auto segments show a positive near-term outlook into Q4 FY26.

D. P. Abhushan | Small Cap | Retail

DP Abhushan Ltd is in the business activity of Trading Of Jewellery Of Gold,Silver And Other Precious Or Base Metal and Manufacture Of Jewellery Of Gold,Silver And Other Precious Of Base Metal. The company’

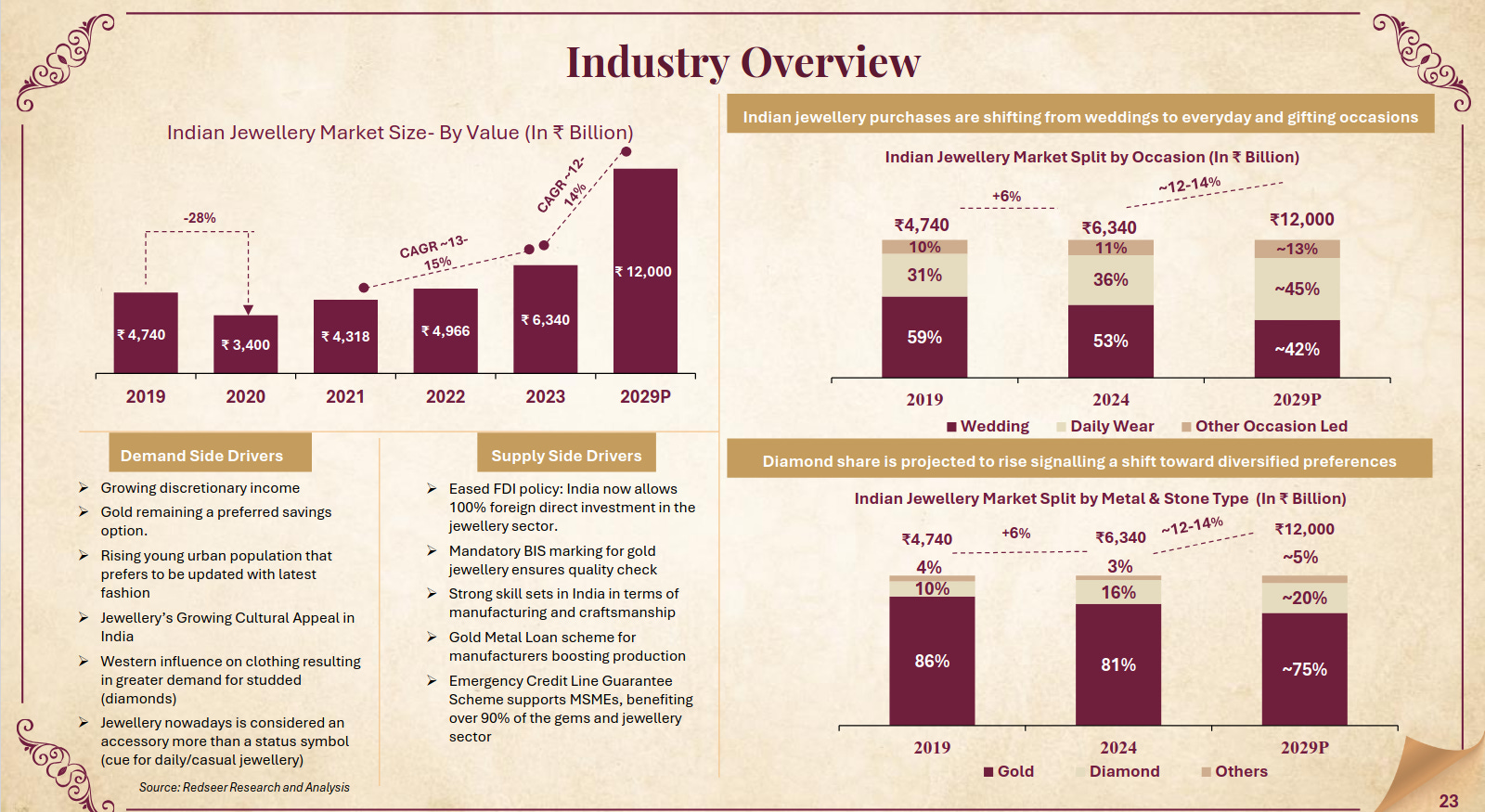

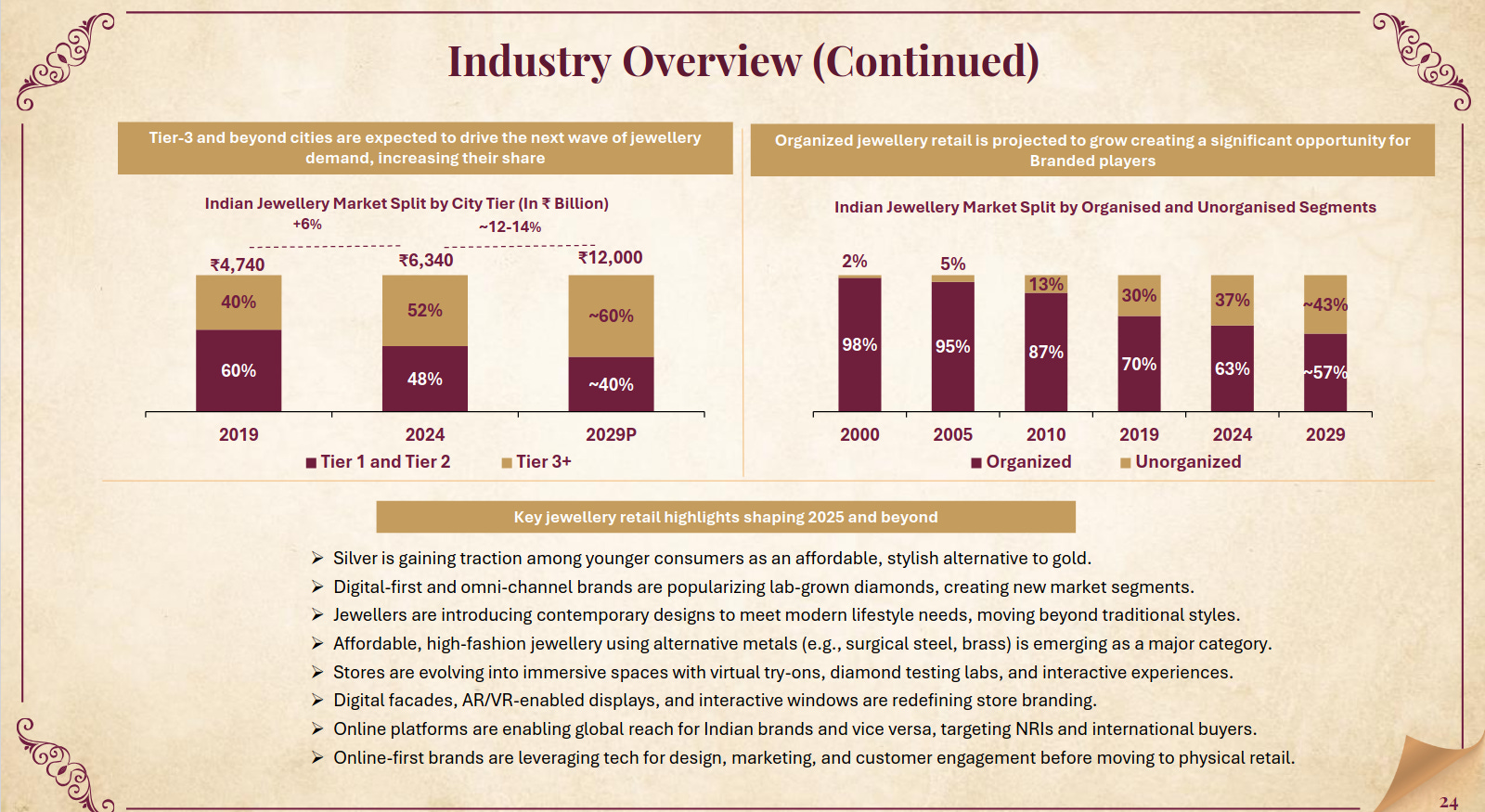

India’s jewellery market is being reshaped by digital channels, lightweight designs, and daily-wear preferences, especially among younger consumers. Policy support through Sovereign Gold Bonds and 100% FDI is further formalising and expanding the sector.

Tier-3 and smaller cities are emerging as the next growth engine, with their share of jewellery demand steadily rising. Organised retail is gaining ground over unorganised players, creating a long runway for branded jewellers as formats, designs, and customer experiences modernise.

The Indian jewellery market is on a strong growth trajectory, rebounding sharply post-2020 and projected to reach ~₹12 trillion by 2029. Demand is shifting from wedding-led purchases toward daily wear and gifting, while diamonds and alternative materials gain share alongside gold.

Services

Gravita India | Small Cap | Services

Gravita India Ltd. is a major global recycling company specializing in the environmentally friendly processing of lead, aluminum, plastics, and rubber, with a growing focus on lithium-ion battery recycling. It operates 13+ eco-conscious facilities, producing refined metals and plastic granules for industries like battery manufacturing.

Gravita focuses on higher-margin, customized products like lead alloys, lead oxide, aluminium alloys, and plastic granules to serve diversified customer needs. The share of value-added products in revenue has steadily increased from ~42% in FY22 to ~50% by FY28E, supporting better realizations.

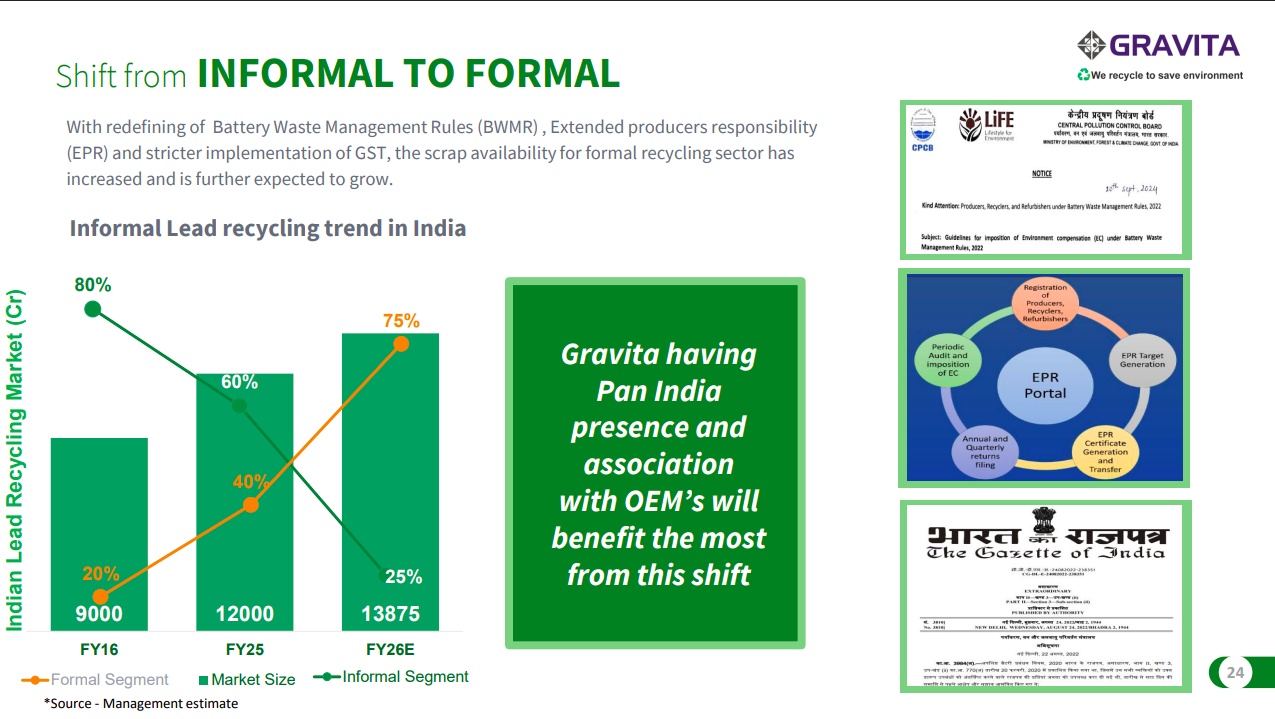

Regulatory tightening through BWMR, EPR norms, and GST is accelerating the shift of lead recycling from the informal to the formal sector. With pan-India presence and strong OEM linkages, Gravita is well positioned to capture a larger share of this expanding formal market.

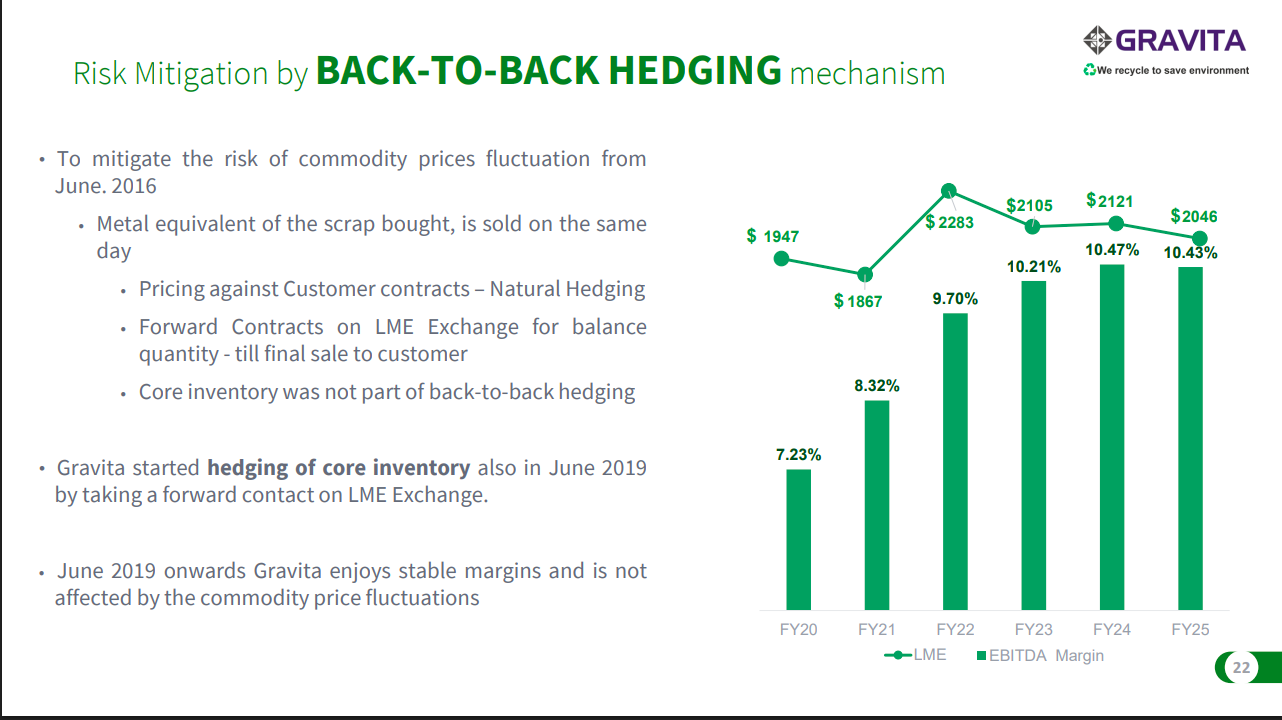

Gravita mitigates commodity price volatility by selling metal equivalents on the same day and using LME forward contracts. Since extending hedging to core inventory in FY19, margins have remained stable despite fluctuations in LME prices.

Gravita works with a wide range of marquee global and Indian partners across batteries, cables, autos, paints, and industrials. These long-standing relationships highlight its credibility, scale, and integration across recycling and materials value chains.

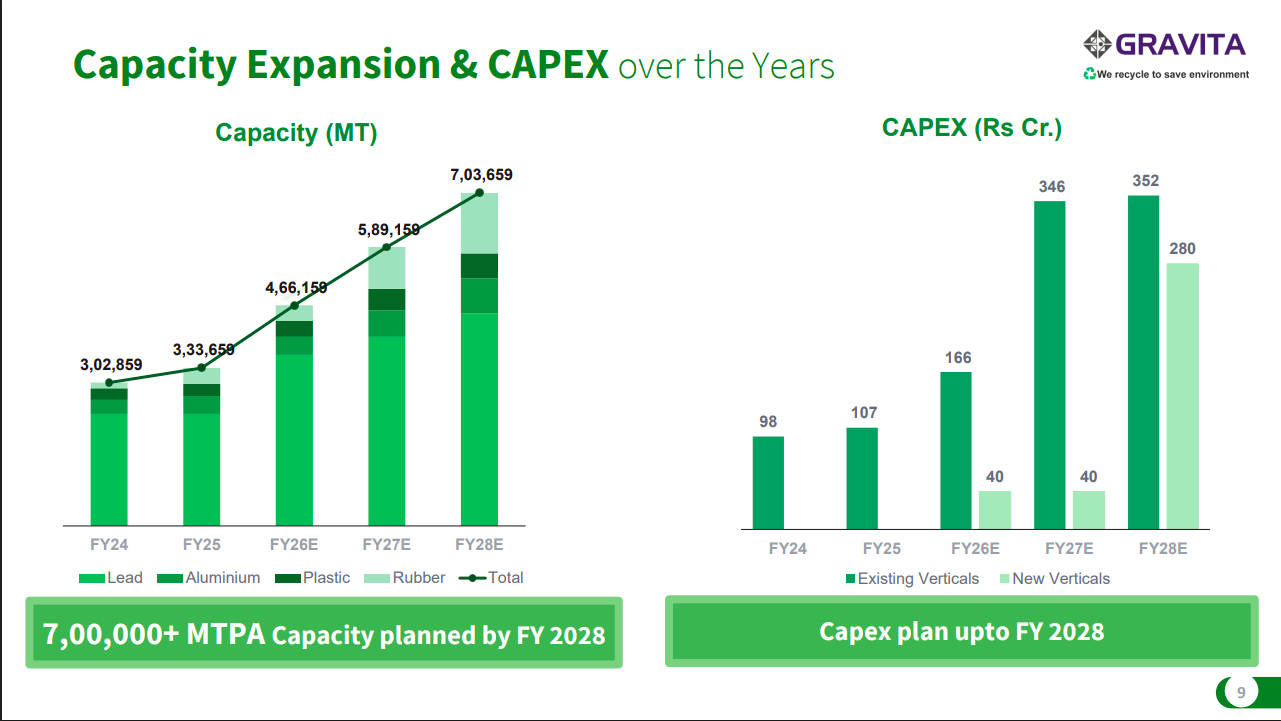

The company plans to scale capacity to over 7,00,000 MTPA by FY28 across lead, aluminium, plastic, and rubber. This growth is backed by a stepped-up capex plan through FY28, with rising investments in both existing and new verticals.

Chemicals

Tatva Chintan Pharma | Small Cap | Chemicals

Tatva Chintan Pharma Chem Limited is a leading specialty chemicals manufacturer in India, producing structure directing agents, phase transfer catalysts, electrolyte salts for super capacitor batteries, and pharmaceutical and agrochemical intermediates. It is the largest manufacturer of SDAs for zeolites in India and holds the second position globally. The company also ranks among the top global producers of PTCs, providing key ingredients for customers’ industrial processes.

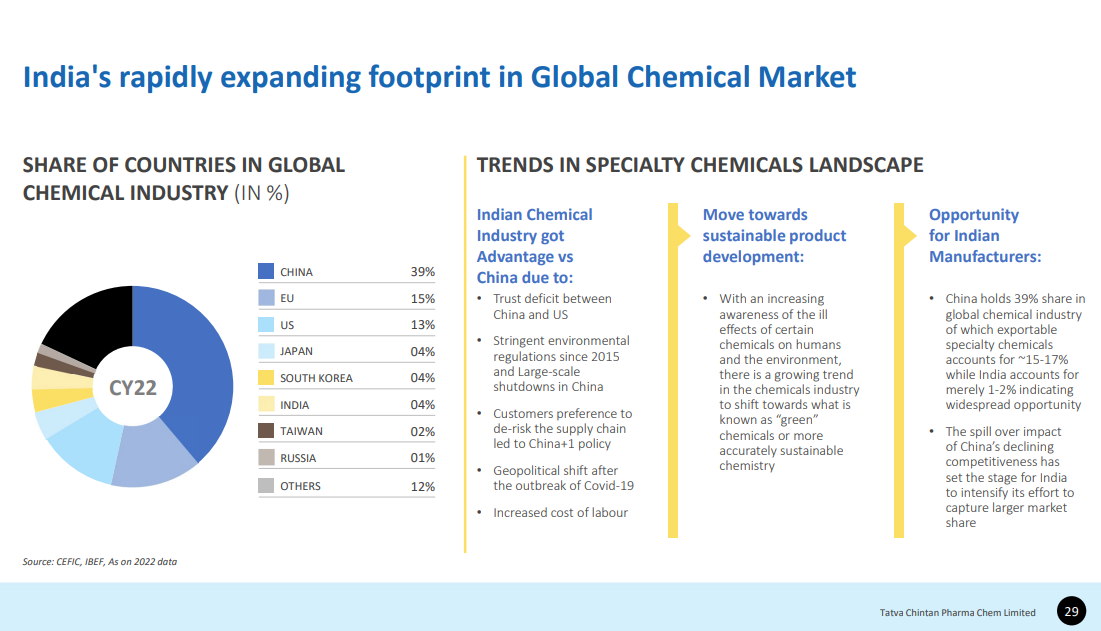

India holds just 4% of the global chemical industry as of CY22, but it’s gaining ground fast. The Indian chemical industry has caught an advantage over China due to the trust deficit between China and the US, stricter environmental regulations in China from 2015, large-scale shutdowns, customer preference to de-risk supply chains, geopolitical shifts after Covid-19, and rising labor costs. There’s a growing global push toward sustainable and “green” chemicals, creating more opportunity for Indian manufacturers. China still dominates with 39% of the global market—of which specialty chemicals account for 15-17%—while India’s share is just 1-2%, leaving plenty of room to grow as China’s competitiveness declines.

The global chemical industry is valued at $5,030 billion in 2022 and is expected to grow to $6,460 billion by 2028, translating to a 4.3% CAGR. It’s divided into three broad categories: commodity chemicals (basic, high-volume chemicals with a market size of $3,700 billion growing at 4% CAGR), specialty chemicals (value-added, low-volume niche chemicals worth $960 billion growing at 7% CAGR), and other chemicals (worth $370 billion growing at 5% CAGR). Within specialty chemicals, key segments include PTC (growing at 5.5% CAGR to reach $1,640 million by 2028), SDA (growing at 5.6% CAGR to $1.65 billion), electrolyte salts (growing at 11% CAGR to $12 million), and intermediates (growing at 5.1% CAGR to $179 billion).

Healthcare

Dr. Reddy’s Lab | Large Cap | Healthcare

Dr. Reddy’s Laboratories is a global pharmaceutical company engaged in the manufacturing and marketing of APIs, generics, biosimilars, and differentiated formulations. It operates in key markets like the USA, India, Russia, CIS countries, China, Brazil, and Europe, focusing on therapeutic areas such as gastrointestinal, cardiovascular, diabetology, oncology, and dermatology.

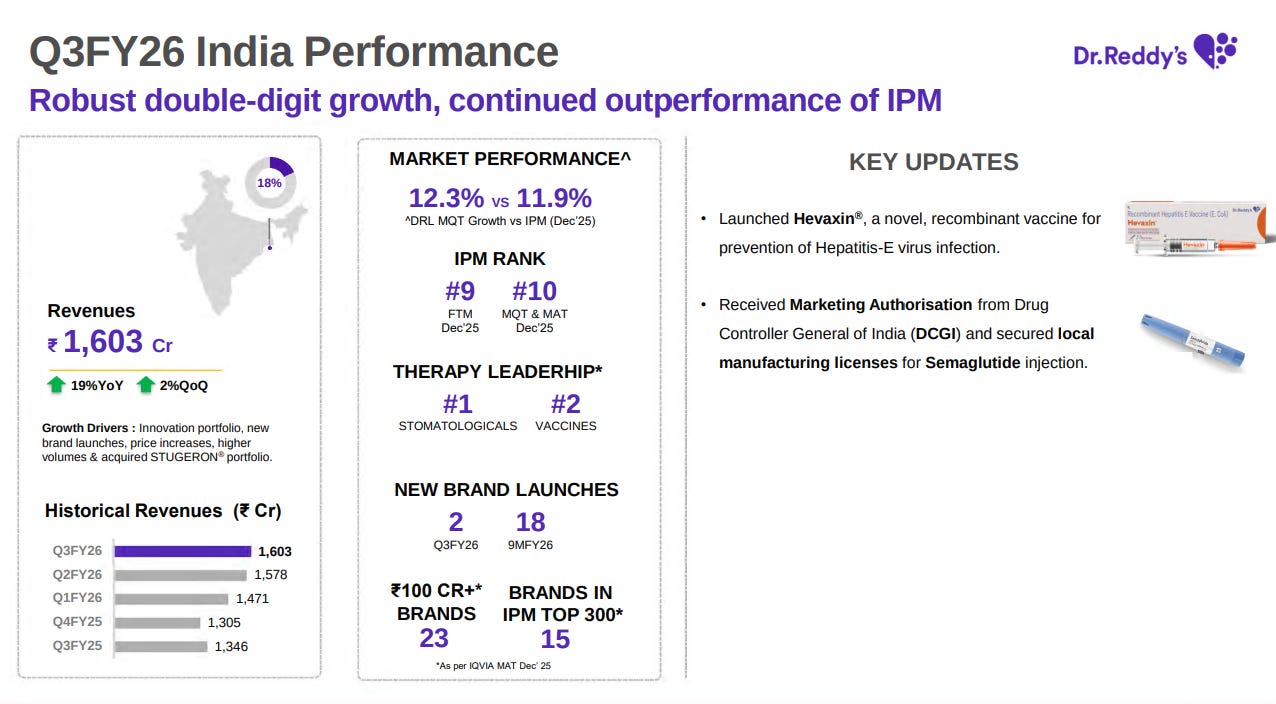

Dr. Reddy’s India business posted revenues of ₹1,603 crore in Q3FY26, up 19% year-on-year and 2% quarter-on-quarter, driven by innovation, new launches, price increases, higher volumes, and the acquired Stugeron portfolio. The company outperformed the Indian Pharmaceutical Market (IPM), which grew at 11.9%, with Dr. Reddy’s clocking 12.3% growth. It ranks #9 in the overall market, #10 in Moving Annual Total (MAT), and holds #1 position in stomatologicals and #2 in vaccines. The quarter saw two new brand launches, taking the nine-month tally to 18, with 23 brands now crossing ₹100 crore and 15 brands in the IPM top 300—plus the launch of Hevaxin, a novel hepatitis-E vaccine, and marketing authorization for Semaglutide injection with local manufacturing licenses secured.

Software Services

Mphasis | Mid Cap | Software Services

Mphasis is a global service provider offering technology-driven solutions for multiple industries, with a focus on Service Transformation to deliver scalable digital operations. They emphasize a holistic approach to AI, aiming to make it practical and beneficial for all stakeholders, positioning themselves as a leader in enabling future-ready, digital enterprise solutions.

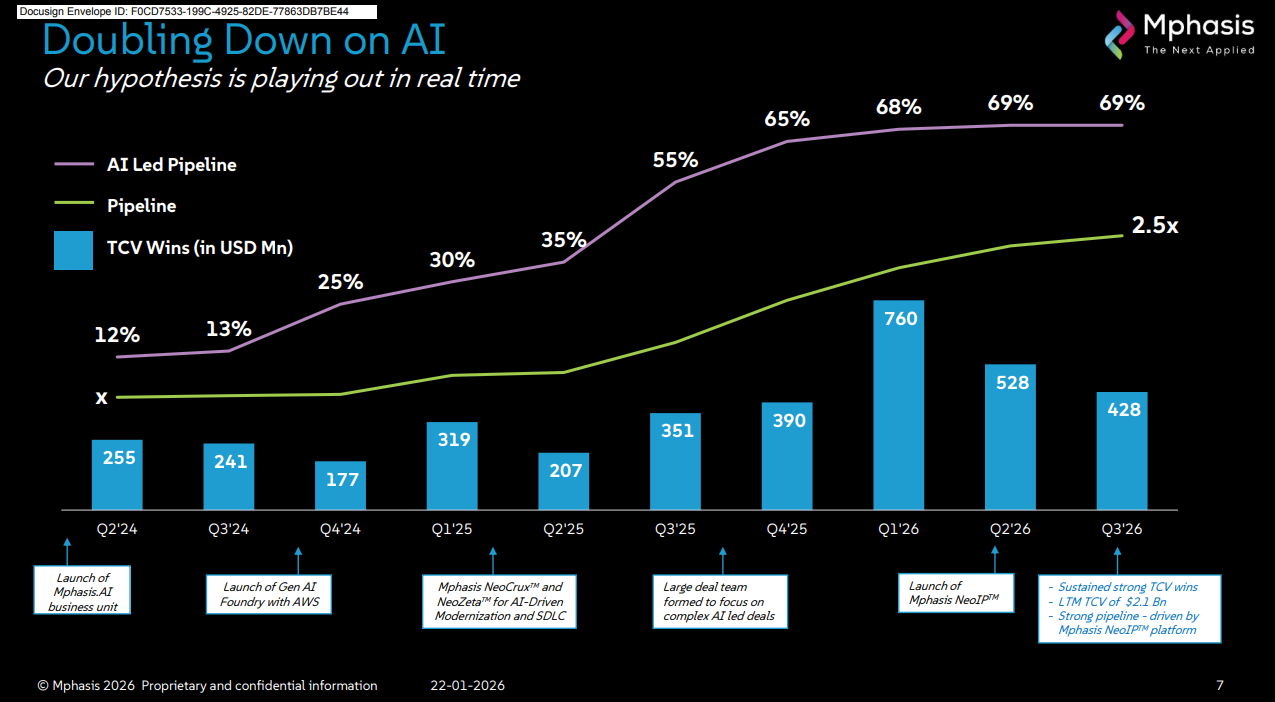

Mphasis has been betting big on AI, and the numbers show it’s paying off. The share of AI-led deals in their pipeline has jumped from just 12% in Q2’24 to 69% by Q3’26, while total contract value (TCV) wins have nearly doubled from a baseline of ‘x’ to 2.5x over the same period. Key milestones include launching the Mphasis-AI business unit in Q2’24, Gen AI Foundry with AWS in Q3’24, NeoCreux and NeoZeta platforms in Q1’25, and Mphasis NeoTP in Q1’26. Total TCV wins hit $760 million in Q1’26 and remained strong at $428 million in Q3’26, driven by sustained momentum from their AI platforms and a large deal team focused on complex AI-led engagements.

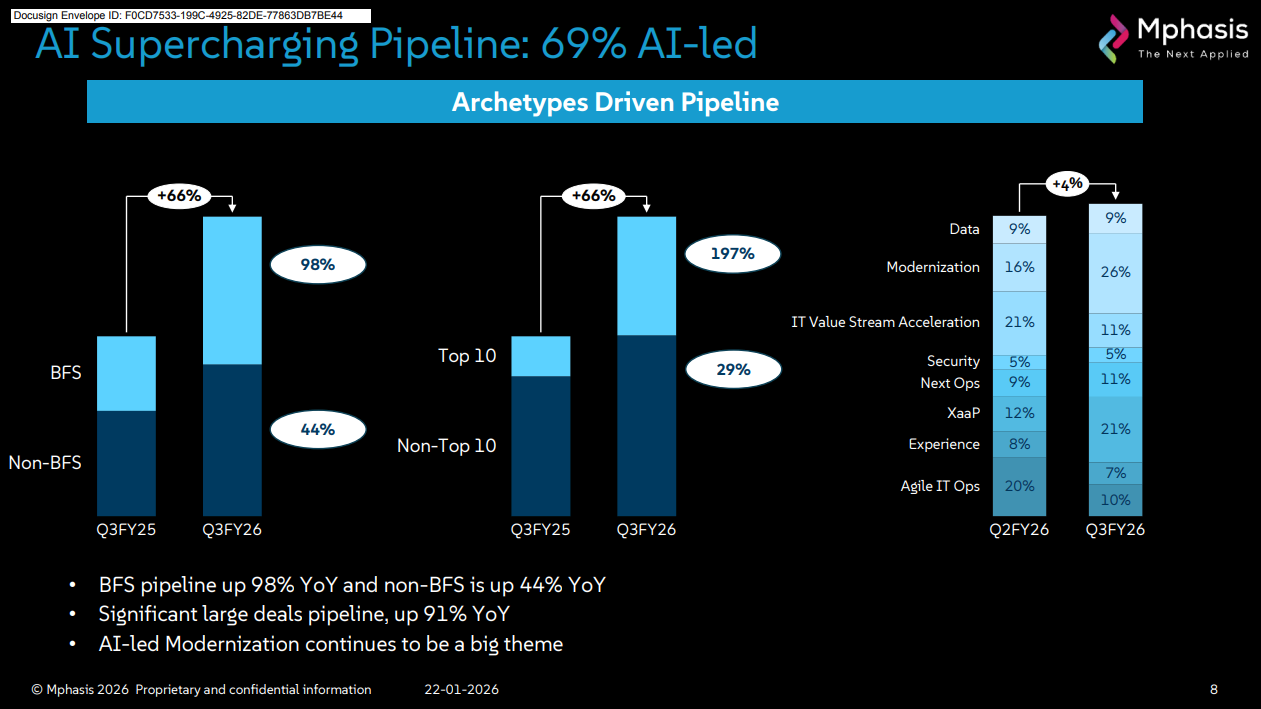

Mphasis’ pipeline is now heavily AI-driven, with 69% of deals being AI-led. The BFS (Banking and Financial Services) pipeline surged 98% year-on-year, while non-BFS grew 44%, resulting in an overall 66% increase in both top 10 and non-top 10 client pipelines. Within the top 10 clients, the pipeline jumped 197% year-on-year, with AI-led modernization now making up 26% of deals (up from 16% in Q2FY26), IT value stream acceleration at 11%, and Agile IT Ops at 10%. The significant large deals pipeline is up 91% year-on-year, and AI-led modernization continues to be a dominant theme across all client segments.

Persistent Systems | Mid Cap | Software Services

Persistent Systems Limited is a global company specializing in software products, services and technology innovation. It designs, develops and maintains software systems across various industries such as telecommunications and life sciences, offering complete product life cycle services to enhance customer software products.

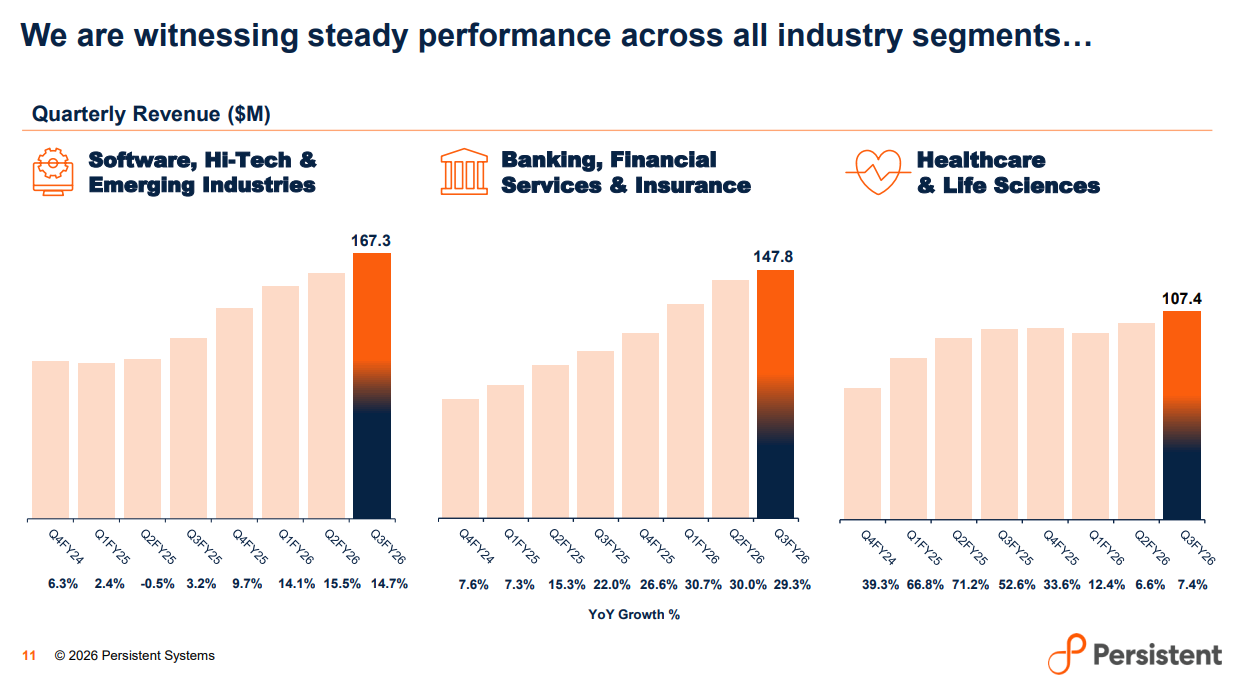

Persistent Systems is seeing consistent growth across its three main verticals. Software, Hi-Tech & Emerging Industries posted quarterly revenue of $167.3 million in Q3FY26, growing 14.7% year-on-year after peaking at 15.5% in Q2FY26. Banking, Financial Services & Insurance reached $147.8 million with a strong 29.3% year-on-year growth, accelerating from 30% in the previous quarter. Healthcare & Life Sciences generated $107.4 million in revenue with 7.4% year-on-year growth, down from double-digit growth rates seen in earlier quarters but showing steady sequential momentum.

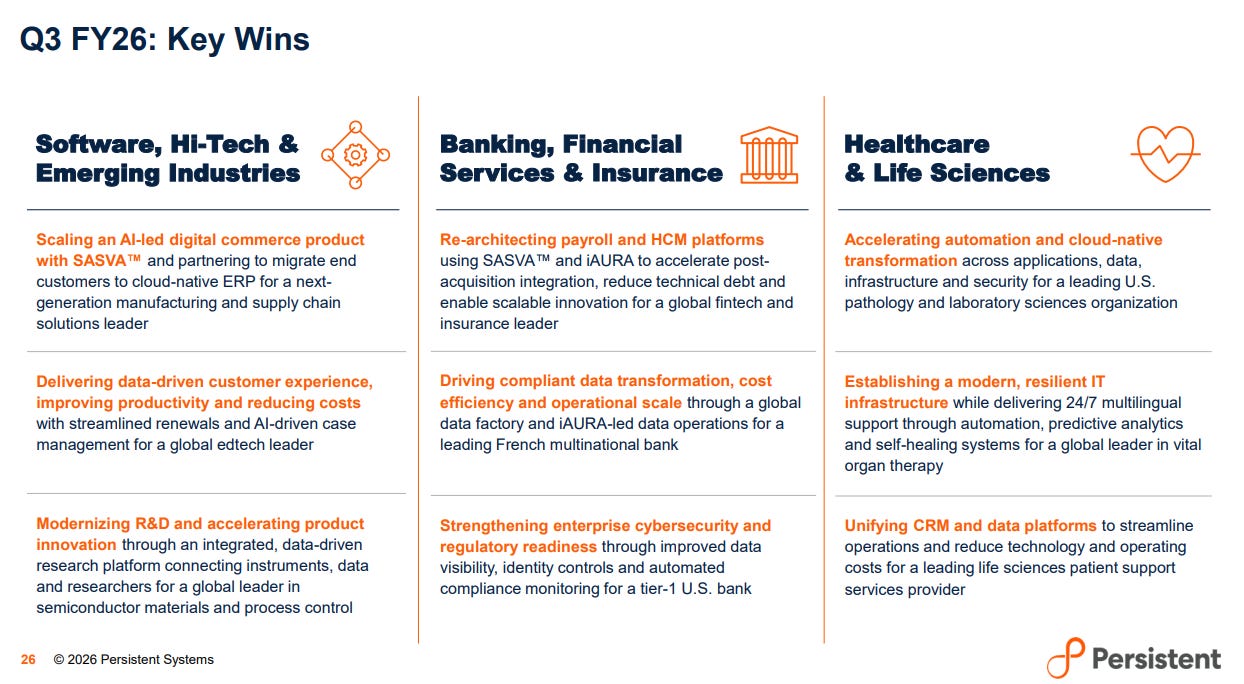

Persistent Systems secured notable client wins across all three verticals in Q3 FY26. In Software, Hi-Tech & Emerging Industries, they’re scaling an AI-led digital commerce product with SASVA, migrating customers to cloud-native ERP for a supply chain leader, delivering data-driven customer experience for a global edtech leader, and modernizing R&D through an integrated research platform for a semiconductor materials leader. In Banking, Financial Services & Insurance, they’re re-architecting payroll and HCM platforms using SASVA and iAURA for a fintech and insurance leader, driving compliant data transformation for a French multinational bank, and strengthening cybersecurity and regulatory readiness for a tier-1 U.S. bank. In Healthcare & Life Sciences, they’re accelerating automation and cloud-native transformation for a U.S. pathology and lab sciences organization, establishing a modern IT infrastructure with 24/7 multilingual support for a vital organ therapy leader, and unifying CRM and data platforms for a life sciences patient support services provider.

That’s it for now! Your feedback will really help shape how Points and Figures evolves. Drop it down in the comments below!

Quotes in this newsletter were curated by Meher & Vignesh.

Disclaimer: We’ve used AI tools in filtering and cleaning up the quotes from the images so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Points and Figures is run by the same team that creates The Daily Brief and Aftermarket Report.

Thank you for very useful summaries. Your efforts are commendable