Sometimes, a single slide can explain more than a long report. Points and Figures is our way of breaking down what India’s leading companies are telling their shareholders and analysts. We comb through the decks, pull out the charts and data points that actually matter, and highlight the signals behind the numbers—whether about growth plans, margins, new markets, or risks on the horizon.

This is an extension of The Chatter. While The Chatter focuses on management commentary and earnings call transcripts, Points and Figures dives into investor presentations—and soon, even annual reports—to decode what companies are showing, not just what they’re saying.

We go through every major investor presentation so you don’t have to—bringing you the sharpest takeaways that reveal not just what the company is saying, but what it really means for the business, its sector, and the broader economy.

In this edition, we have covered 15 companies across 11 industries.

Energy

Adani Green Energy

Ellenbarrie Industrial Gases

Building Materials

Ambuja Cement

Metals

Vedanta

SAIL

Engineering & Capital Goods

Thermax

Financial Services

Nippon Life India Asset Management

One Mobikwik Systems

Auto Ancillary

Balkrishna Industries

FMCG

DOMS Industries

Zydus Wellness

Logistics

TCI Express

Media & Entertainment

Saregama India

Diversified

Adani Enterprises

Software Services

eMudhra

Energy

Adani Green Energy | Large cap | Energy

Adani Green Energy, a major player in India’s renewable sector, is committed to providing a cleaner and greener future for the country as part of the Adani Group. Focusing on utility-scale solar and wind projects, the company supplies electricity to government entities and corporations, aligning with the philosophy of ‘Growth with Goodness’.

India represents a colossal growth opportunity, driven by rapid GDP growth (6.5% in FY25, projected at 7.4% in FY26) and the world’s largest consumer base of 1.46 billion people. However, the country faces critical infrastructure gaps—air travel penetration is just 0.1 per capita (2023), and logistics costs account for nearly 50% of direct costs, highlighting the need for scaled road networks and last-mile connectivity. Decarbonization is a key focus, with India consuming just one-third of the global average electricity per capita and aggressively reducing its current account deficit through green hydrogen and renewable energy. The country also boasts a fully developed indigenous digital stack, with 228 billion UPI transactions in 2023 (>49% of global share by 2029), and is emerging as a global AI leader with a $1.2 billion government allocation and a 14x increase in AI-skilled workforce since 2016.

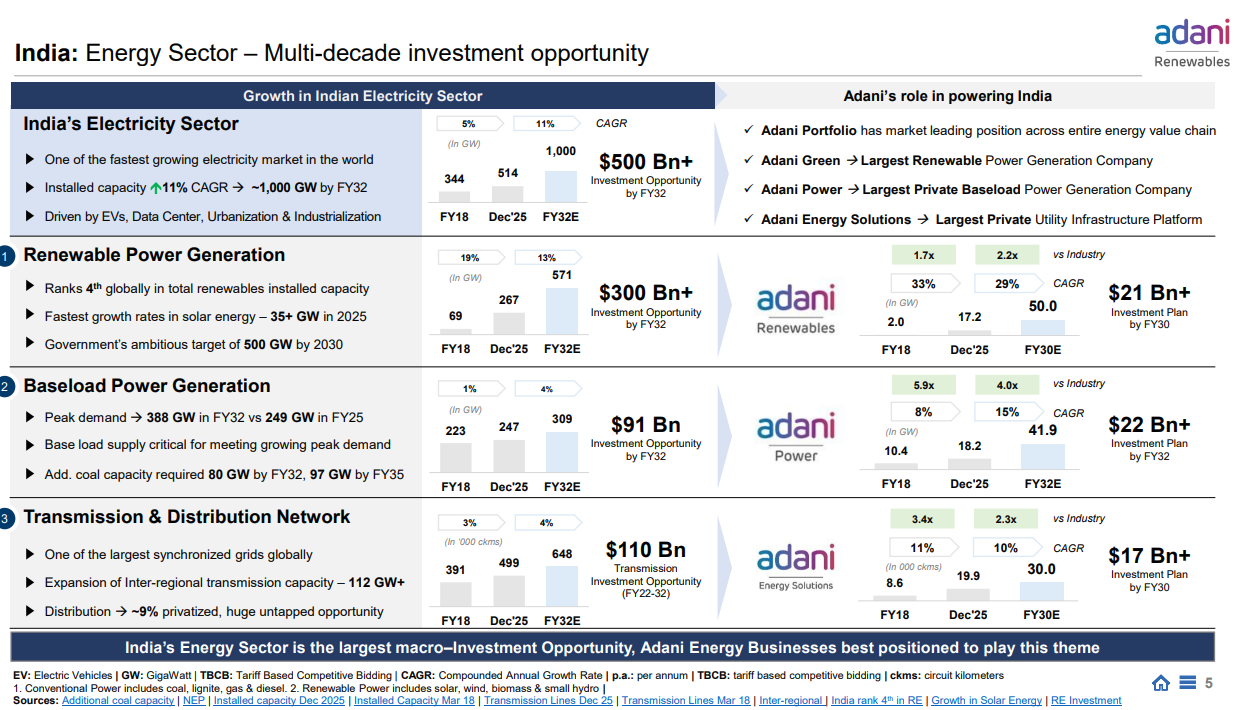

India’s energy sector presents a multi-decade investment opportunity, with total electricity capacity projected to grow from 344 GW in FY18 to over 1,000 GW by FY32, requiring $500 billion+ in investments. Renewable power generation is set to expand from 69 GW in FY18 to 571 GW by FY32E, driven by government targets and $300 billion+ in investment, with India ranking 4th globally in renewables capacity. Baseload power generation will grow from 223 GW to 309 GW by FY32E, requiring an additional 80-97 GW of coal capacity to meet rising peak demand. Transmission and distribution networks, already among the world’s largest synchronized grids, need $110 billion in investments as inter-regional capacity expands to 112 GW+, with distribution remaining 91% privatized, presenting a huge untapped opportunity. Adani’s portfolio is strategically positioned across this value chain, with Adani Green as the largest renewable power company, Adani Power as the largest private baseload power company, and Adani Energy Solutions as the largest private utility infrastructure platform, collectively planning $60 billion+ in investments by FY30.

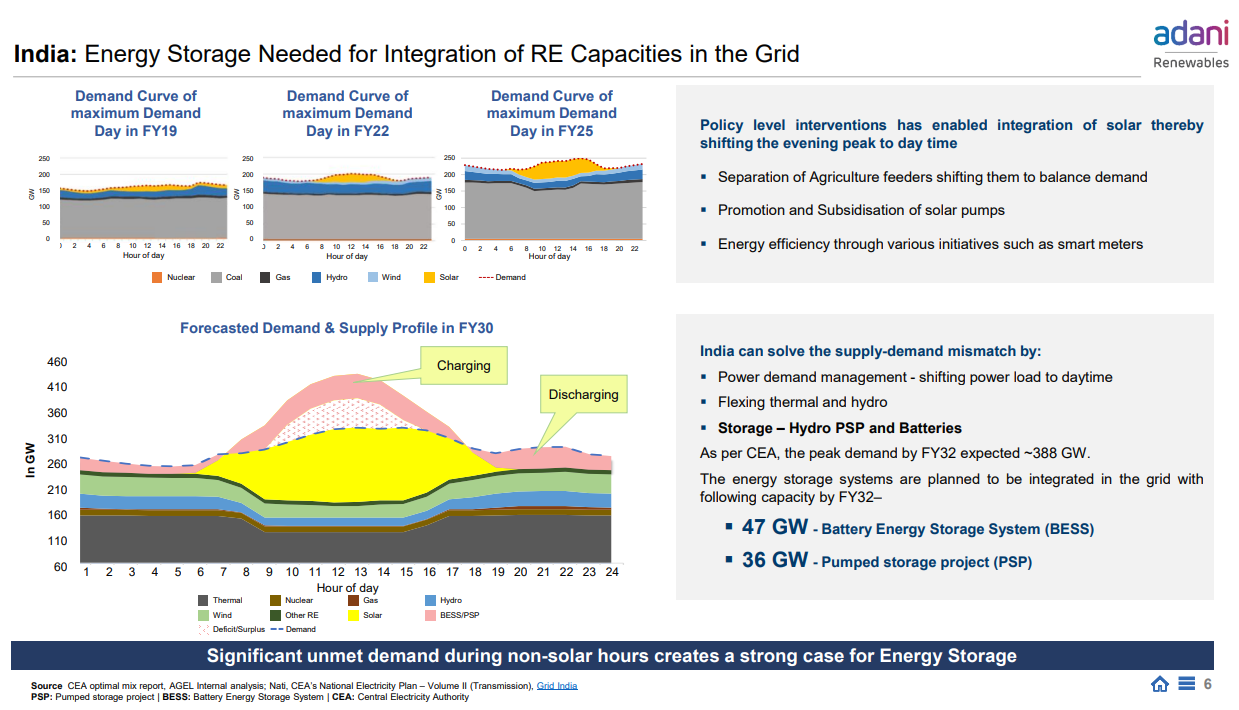

India’s energy grid faces a supply-demand mismatch as solar integration increases, with evening demand peaks shifting to daytime due to policy interventions like agriculture feeder separation, solar pump promotion, and smart meters. By FY30, peak demand is expected to hit around 388 GW, but significant unmet demand during non-solar hours creates a strong case for energy storage. India plans to integrate 47 GW of Battery Energy Storage Systems (BESS) and 36 GW of Pumped Storage Projects (PSP) by FY32 to address this gap. Forecasted demand and supply profiles show charging during solar-rich hours and discharging during evening peaks, with storage, hydro pumping, and thermal/hydro flexibility helping balance the grid. Policy-level interventions have already enabled better solar integration by flattening the evening peak, but energy storage remains critical to managing the grid’s evolving dynamics.

Ellenbarrie Indl. Gas | Small Cap | Energy

Ellenbarrie Industrial Gases specializes in manufacturing and supplying industrial gases for various industries. They provide project engineering services, turnkey solutions for medical gas pipeline systems, and supply medical equipment to healthcare facilities.

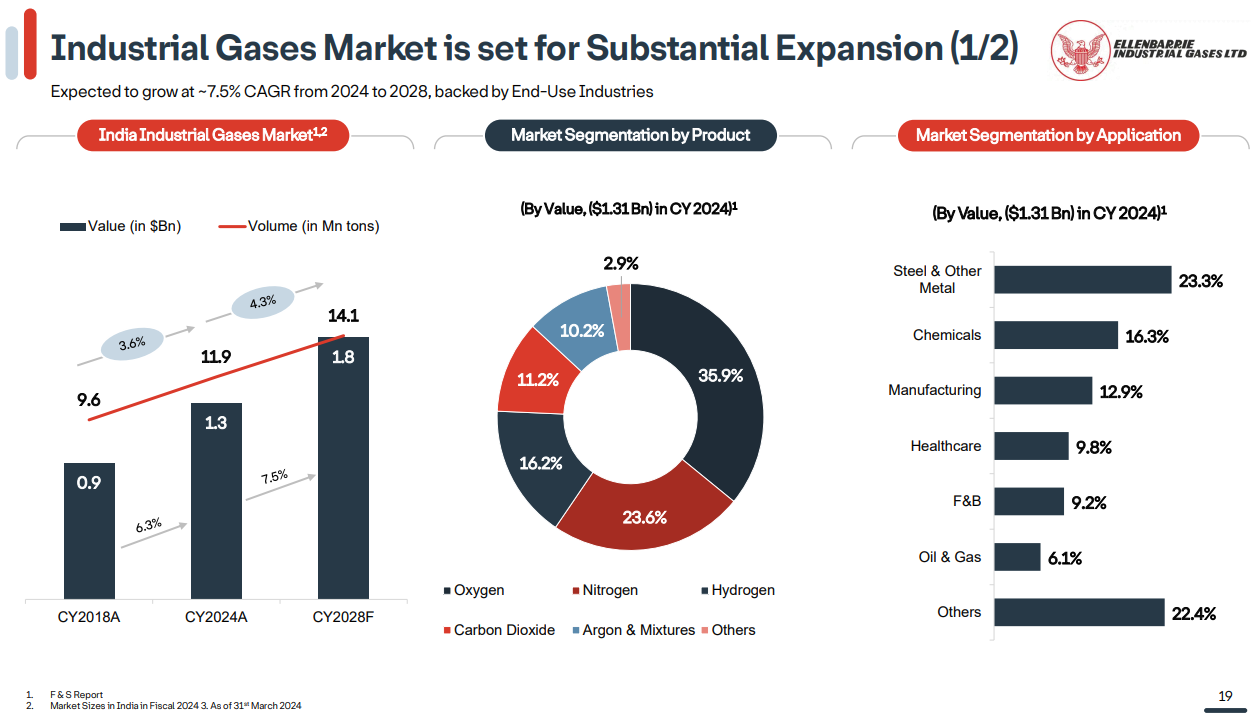

India’s industrial gases market is projected to grow at approximately 7.5% CAGR from 2024 to 2028, driven by strong demand from end-use industries. The market, valued at $1.31 billion in CY 2024, is dominated by oxygen (35.9%), nitrogen (23.6%), and hydrogen (16.2%), with carbon dioxide, argon, and other specialty gases making up the rest. By application, steel and other metals account for 23.3% of demand, followed by chemicals (16.3%), manufacturing (12.9%), and healthcare (9.8%). The market has grown from $0.9 billion in CY 2018 to an expected $1.8 billion by CY 2028, reflecting the increasing industrial activity and infrastructure development across the country.

The industrial gases market is being driven by burgeoning demand from key end-use sectors. Chemicals lead at $270 billion, fueled by rising demand for plastics, fertilizers, and specialty chemicals. Steel follows at $133 billion, with manufacturers increasingly offloading gas production to specialized players. Healthcare is projected at $105 billion, supported by government policy to boost liquid medical oxygen infrastructure, while pharma stands at $59 billion, driven by increased healthcare spending and innovation in drug development. The industry is dominated by multinational players like Linde, Air Liquide, Inox Air Products, and Air Water, while Ellenbarrie Industrial Gases Ltd. stands out as a large domestic player competing in this space.

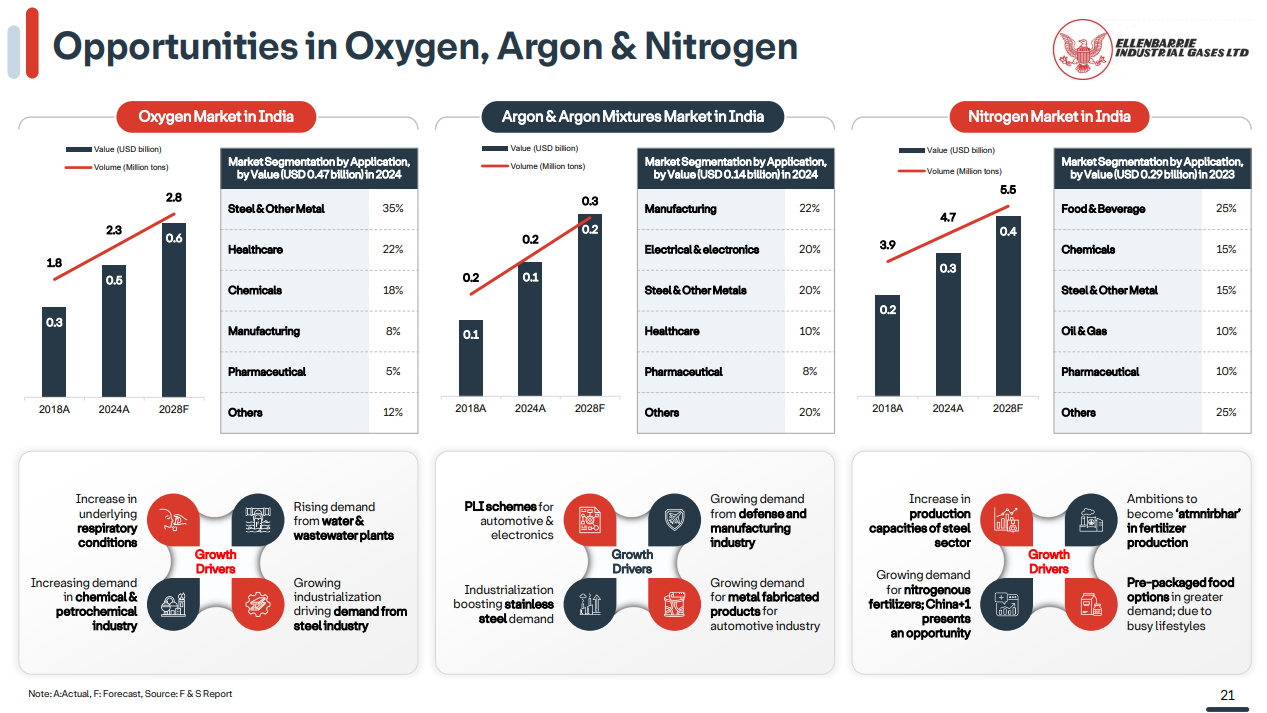

The oxygen market in India is projected to grow from $0.6 billion in 2024 to $0.6 billion by 2028, driven by healthcare (22%), steel and metals (35%), and chemicals (18%). Growth is fueled by increasing demand for underlying respiratory conditions, rising water and wastewater plant demand, and industrialization in the steel sector. The argon market, valued at $0.14 billion in 2024, is set to reach $0.3 billion by 2028, supported by manufacturing (22%), electrical and electronics (20%), and steel (20%), with drivers including PLI schemes for automotive electronics, defense and manufacturing demand, and stainless steel production. The nitrogen market, at $0.29 billion in 2023, is expanding rapidly toward $5.5 billion by 2028, led by food and beverage (25%), chemicals (15%), and oil and gas (10%), with growth coming from production capacity increases, nitrogenous fertilizer demand, and pre-packaged food options catering to busy lifestyles.

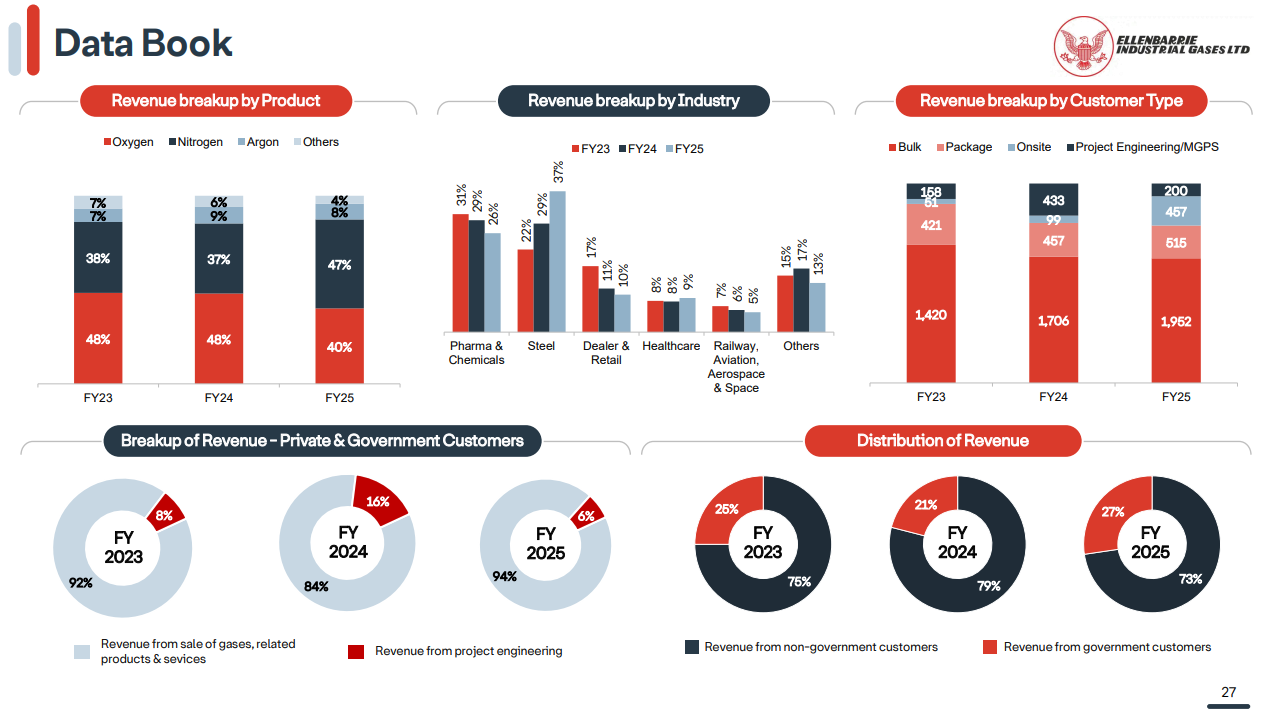

Ellenbarrie’s revenue mix shows oxygen consistently contributing around 48%, nitrogen at 37-38%, and argon at 4-6% across FY23-FY25. By industry, steel has been the largest segment at 37% in FY23, declining to 27% by FY25, while pharma and chemicals remain stable around 22-31%. By customer type, bulk customers account for the largest share at ₹1,962 crore in FY25, followed by package customers at ₹1,706 crore and onsite at ₹433 crore, with project engineering contributing an additional ₹200 crore. Revenue from non-government customers dominates at 73-79%, though government-related revenue (including project engineering) has grown from 21% in FY23 to 27% in FY25, driven by project engineering, which increased from 8% in FY23 to 16% in FY24 and remains at 6% in FY25.

Building Materials

Ambuja Cement | Large Cap | Building Materials

Ambuja Cements Limited, a leading company in the cement industry in India and a member of the Adani Group, focuses on providing sustainable and environment-friendly cement solutions. It operates multiple manufacturing plants and has set industry standards for responsible resource use and conservation, being certified water positive over eight times.

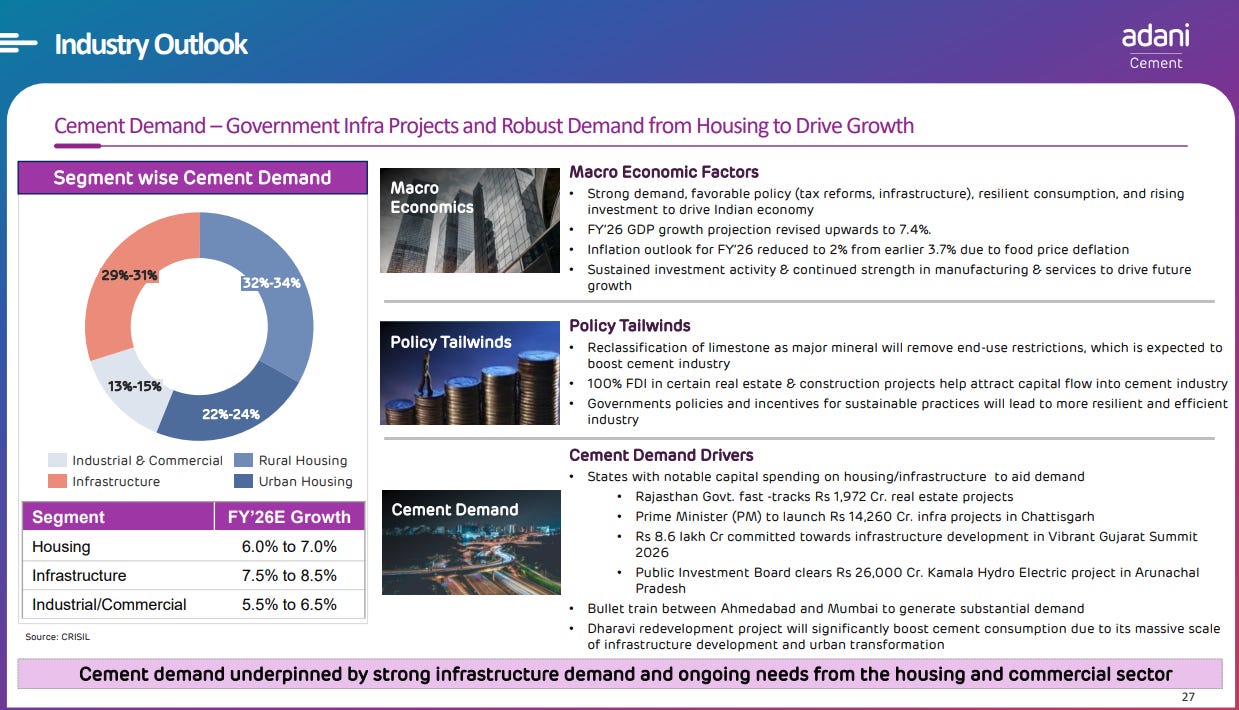

India’s cement demand is expected to grow 6-8.5% in FY26E, driven by government infrastructure projects and robust housing demand. Rural and urban housing account for 54-58% of total cement consumption, while infrastructure makes up 22-24% and industrial/commercial contributes 13-15%. Key growth drivers include GDP growth revised upwards to 7.4%, inflation cooling to 2%, reclassification of limestone as a major mineral, 100% FDI in real estate, and major projects like the ₹14,260 crore Chhattisgarh infra push, ₹8.6 lakh crore Vibrant Gujarat commitments, and ₹26,000 crore Kamala Hydro Electric project. Additionally, the bullet train between Ahmedabad and Mumbai and the Dharavi redevelopment project are expected to generate substantial cement demand, reinforcing strong infrastructure-led growth prospects.

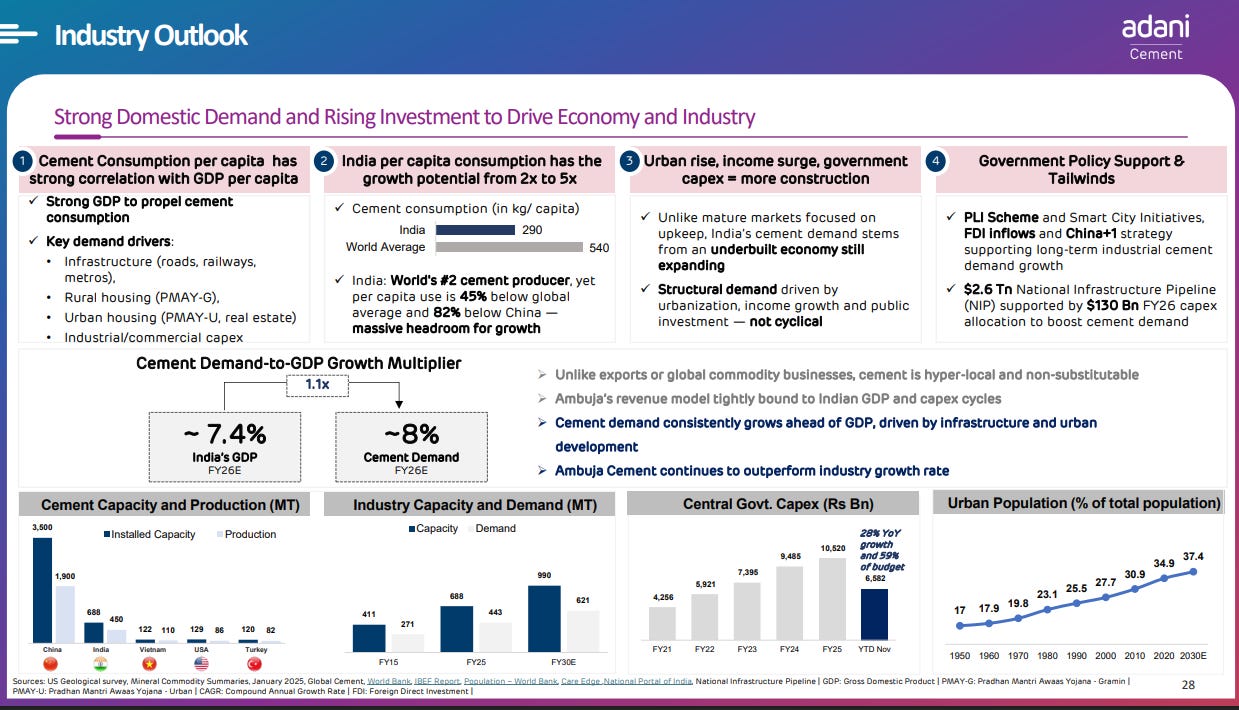

India’s cement demand is tightly linked to GDP growth, with a 7.4% GDP forecast for FY26E translating to an estimated 8% cement demand growth due to a 1.1x multiplier effect. India’s per capita cement consumption is just 290 kg, far below the global average of 540 kg, indicating massive room for growth from 2x to 5x as the economy expands. Key demand drivers include infrastructure projects (roads, railways, metros), rural housing under PMAY-G, urban housing and real estate (PMAY-U), and industrial/commercial capex, all fueled by urbanization, rising incomes, and structural demand that is non-cyclical. Government policy support through PLI schemes, Smart City Initiatives, FDI inflows, and the China+1 strategy are further bolstering long-term industrial cement demand growth. Central government capex has surged from ₹4,256 billion in FY21 to ₹10,520 billion in FY25, with a 29% year-over-year increase in November alone, while urban population is projected to rise from 27.7% in 2000 to 37.4% by 2030E, driving sustained cement demand ahead of GDP growth rates.

Metals

Vedanta | Large Cap | Metals

Vedanta Ltd is a leading natural resources conglomerate with operations in zinc, lead, iron ore, steel, copper, and more. The company focuses on creating value through strategic capabilities, alliances, and a portfolio of low-cost, profitable assets. It is a global leader in critical minerals and plays a key role in the energy transition by supplying essential materials.

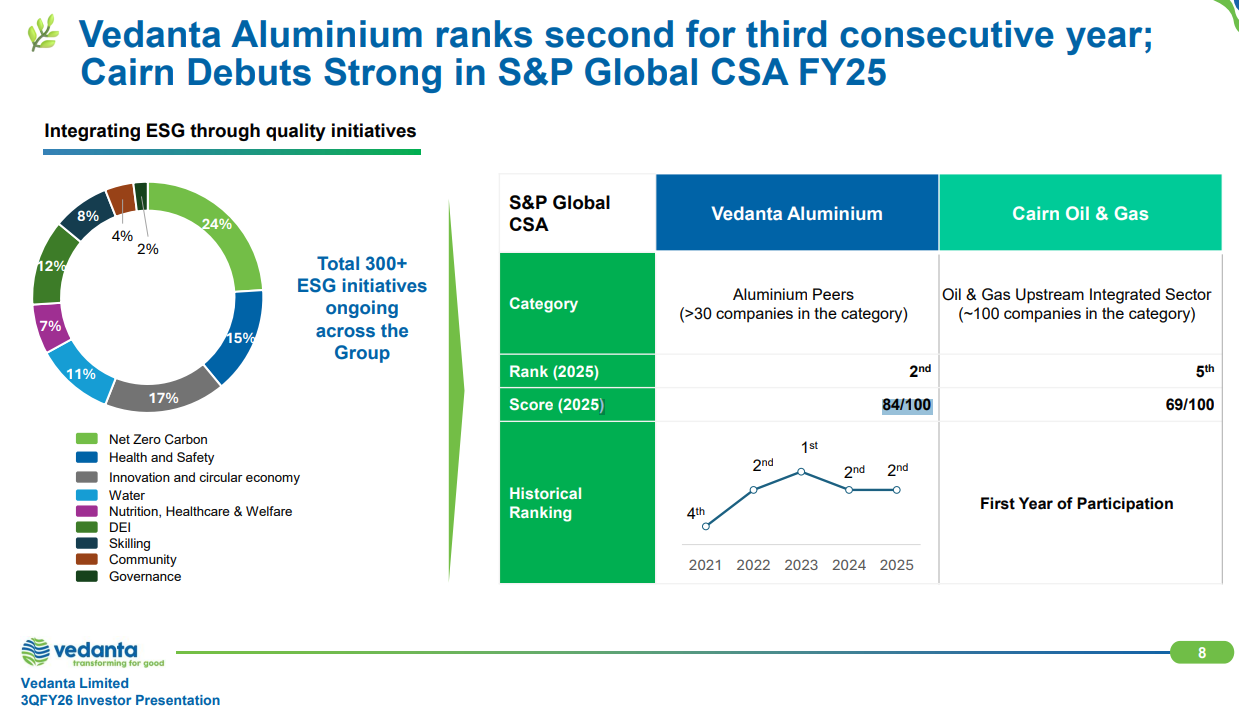

Vedanta Aluminium has secured the 2nd rank in the S&P Global Corporate Sustainability Assessment (CSA) for the third consecutive year, scoring 84/100 among over 30 aluminium peers. The company has steadily improved its ranking from 4th in 2021 to 1st in 2023 and has maintained the 2nd position in 2024 and 2025. Vedanta’s sister concern, Cairn Oil & Gas, debuted strong at 5th rank with a score of 69/100 in the oil and gas upstream integrated sector, marking its first year of participation. The group is driving sustainability through 300+ ESG initiatives across nine focus areas, including net zero carbon (24%), health and safety (15%), innovation and circular economy (17%), and others like water, nutrition, DEI, skilling, community, and governance.

SAIL | Mid Cap | Metals

Steel Authority of India Limited (SAIL) is one of the largest steel-making companies in India and one of the Maharatnas of the country’s Central Public Sector Enterprises. It produces iron and steel at several integrated plants and many special steel plants, located principally in the eastern and central regions of India and situated close to domestic sources of raw materials. It manufactures and sells a broad range of steel products.

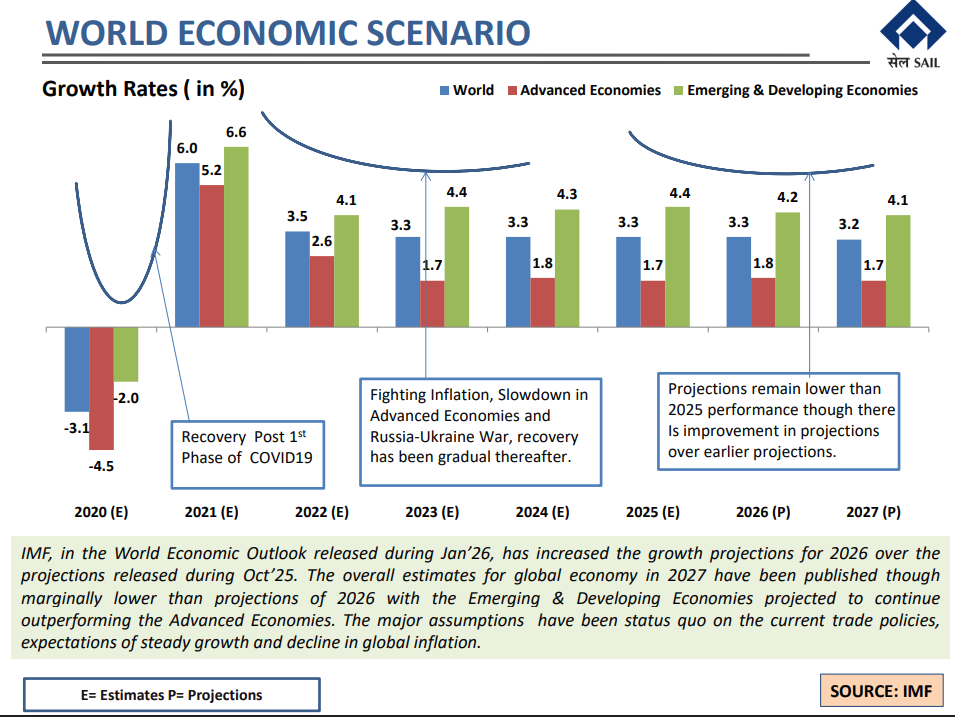

Global economic growth is recovering from the pandemic lows of 2020, but the pace remains subdued. Emerging and developing economies are consistently outpacing advanced economies, growing at around 4% compared to just 1.7-1.8% in developed markets. The IMF has slightly improved its 2026 projections compared to earlier estimates, though overall growth expectations for 2027 remain modest. Recovery has been gradual, weighed down by inflation concerns, geopolitical tensions like the Russia-Ukraine war, and sluggish performance in advanced economies.

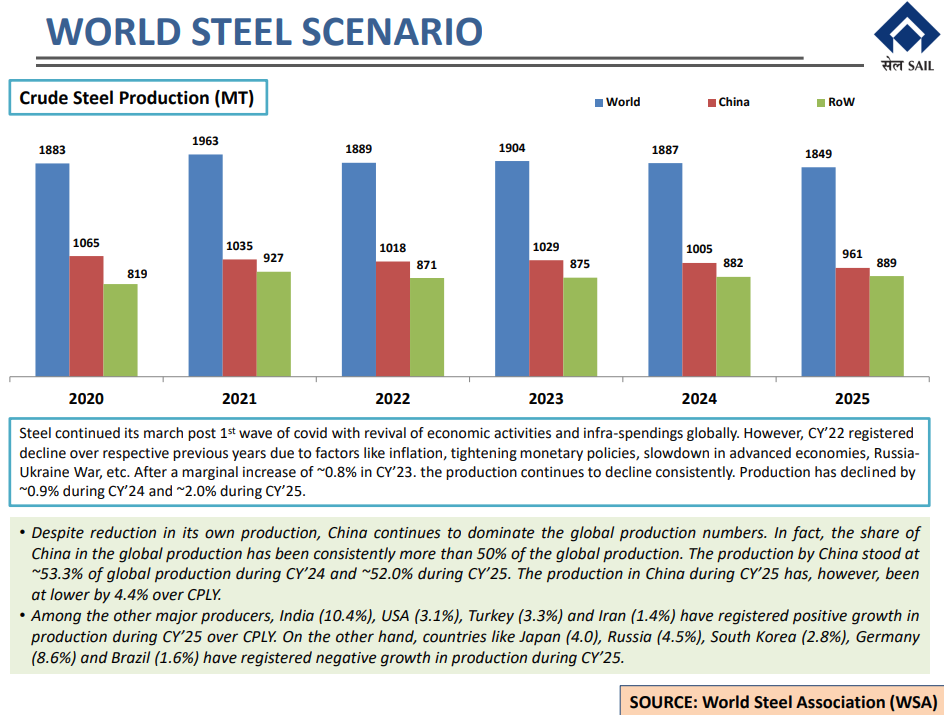

Global crude steel production peaked at 1,963 MT in 2021 during the post-COVID recovery, but has been declining since, dropping to 1,849 MT in 2025. China remains the dominant player, accounting for over 50% of global output, though its production fell 4.4% in 2025 compared to the previous year. The Rest of World has seen mixed performance—India, USA, Turkey, and Iran have grown, while Japan, Russia, South Korea, Germany, and Brazil have recorded declines. Overall, the steel industry is facing headwinds from inflation, monetary tightening, and slower economic activity in advanced markets.

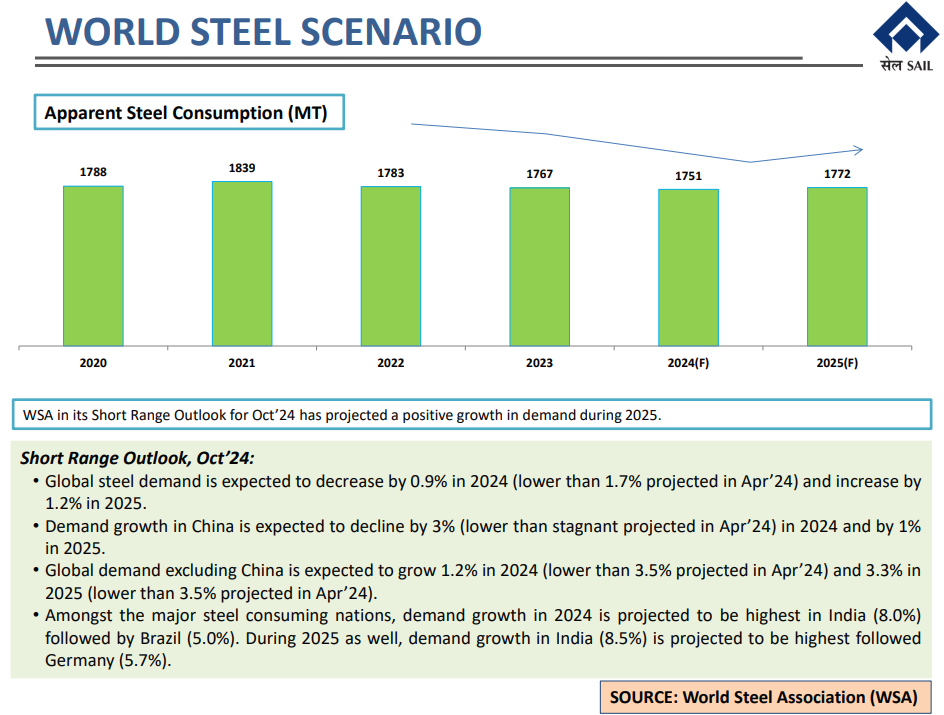

Global steel consumption has been on a downward trend since peaking at 1,839 MT in 2021, falling to 1,751 MT in 2024. However, the World Steel Association expects a modest recovery in 2025, with demand projected to grow 1.2% to 1,772 MT. China’s steel demand is expected to decline by 3% in 2024 and another 1% in 2025, while markets outside China are set to grow stronger—up 1.2% in 2024 and 3.3% in 2025. India stands out as the brightest spot, with demand growth projected at 8% in 2024 and 8.5% in 2025, the highest among major steel-consuming nations.

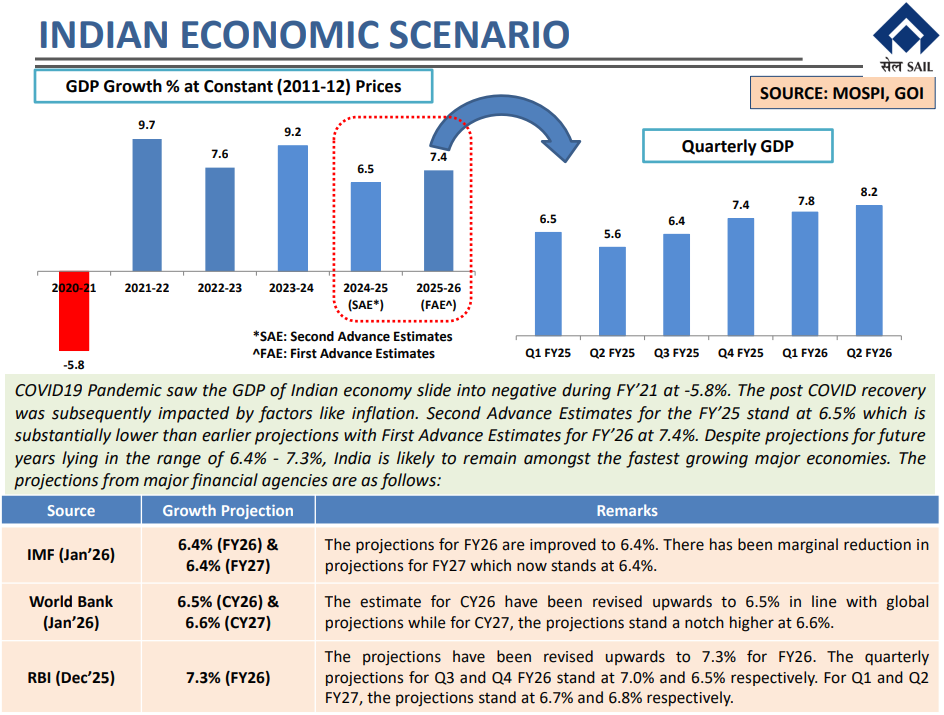

India’s GDP growth bounced back strongly post-COVID, hitting 9.7% in 2020-21, but has since moderated. The latest estimates for FY26 stand at 6.5-7.4%, revised downward from earlier projections of 7.4%. Quarterly data shows growth accelerating from 5.6% in Q2 FY25 to 8.2% in Q2 FY26, reflecting resilience despite global headwinds. Major agencies like the IMF, World Bank, and RBI project India’s growth in the 6.4-7.3% range for FY26-27, keeping it among the fastest-growing major economies globally.

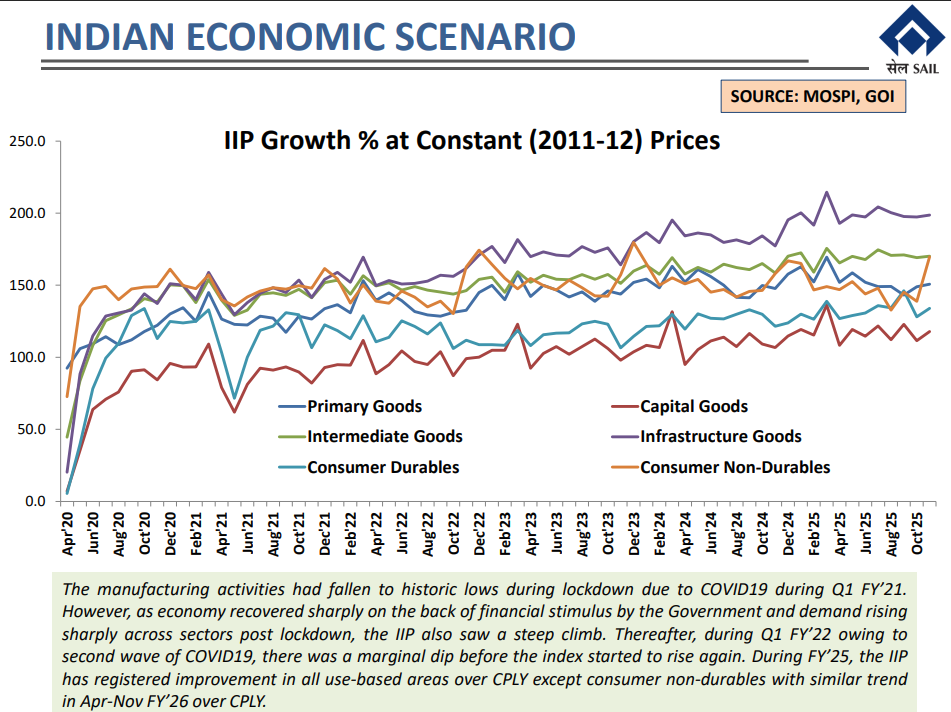

India’s Index of Industrial Production (IIP) crashed during the COVID lockdowns in Q1 FY21 but recovered steadily as the economy reopened and government stimulus kicked in. Infrastructure goods have led the recovery, climbing to over 200 on the index, while capital goods have remained relatively subdued around 120. In FY25, IIP has shown improvement across most categories compared to the previous year, except for consumer non-durables, which continue to lag. The trend suggests manufacturing activity is rebounding, though consumer non-durables remain a weak spot even into FY26.

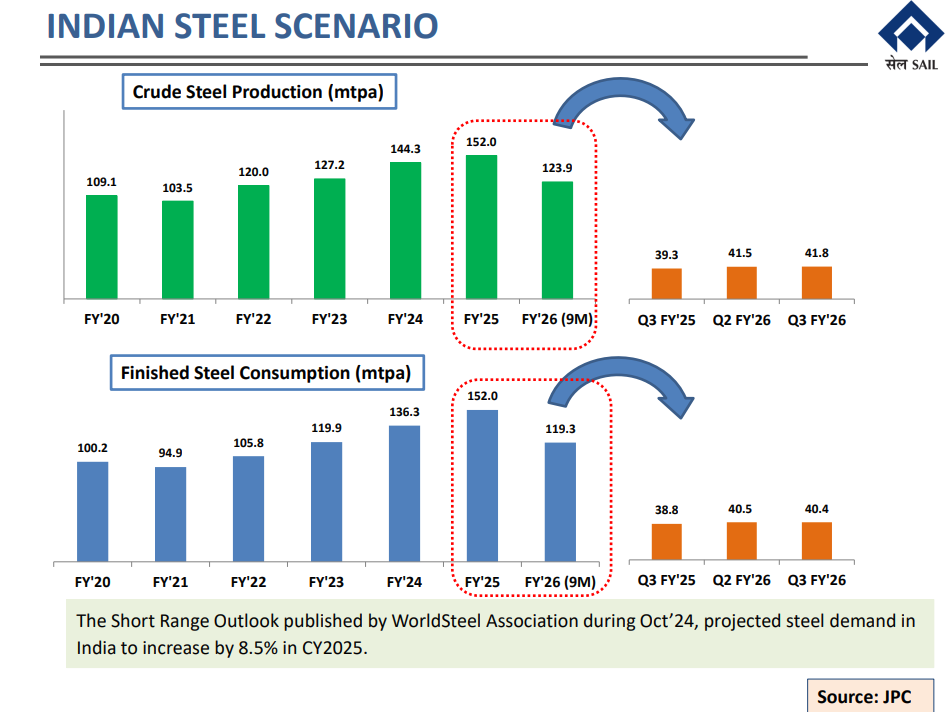

India’s crude steel production peaked at 152 MTPA in FY25 but is projected to decline to 123.9 MTPA in FY26, with quarterly output holding steady around 41-42 MTPA. Finished steel consumption also hit a high of 152 MTPA in FY25 but is expected to drop to 119.3 MTPA in FY26, with quarterly demand remaining flat at around 38-40 MTPA. Despite the projected dip in FY26, the World Steel Association forecasts an 8.5% growth in Indian steel demand for CY2025, signaling optimism for the sector. The mismatch between production and consumption trends suggests adjustments in inventory or export-import dynamics.

Engineering & Capital Goods

Thermax | Mid Cap | Engineering & Capital Goods

Thermax offers a wide range of products and solutions for industrial heating, cooling, water management, and pollution control. They design and build boilers, power plants, wastewater treatment systems, and waste heat recovery solutions. Their technologies help industries improve efficiency and sustainability while reducing environmental impact.

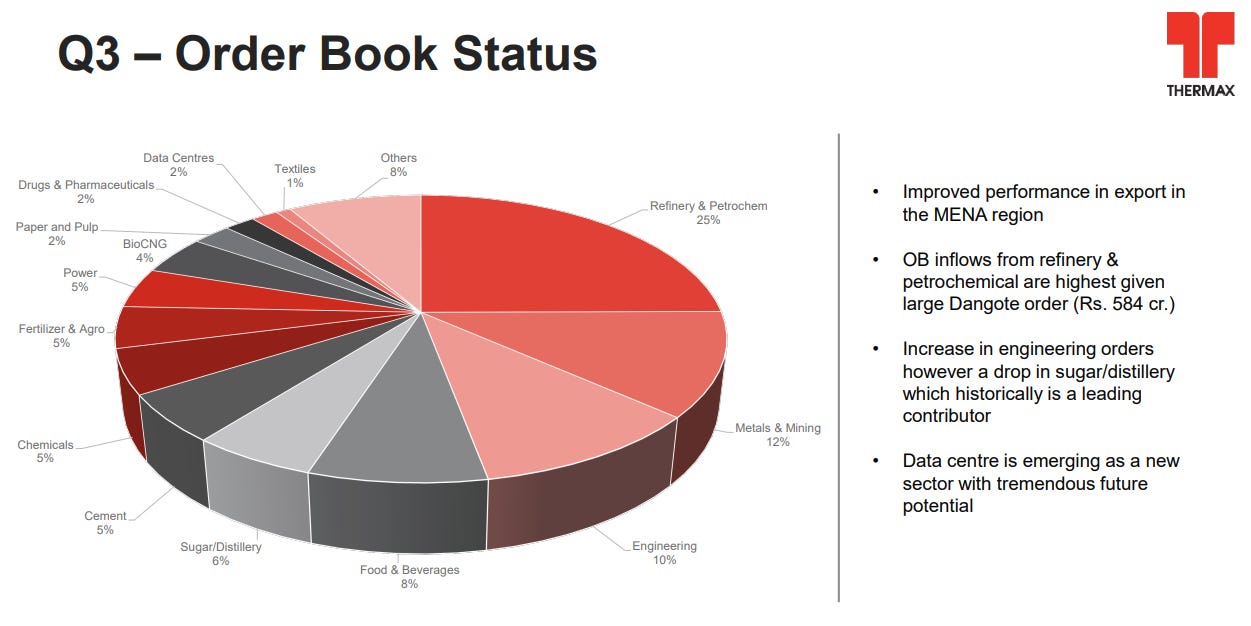

Thermax’s order book for Q3 is dominated by refinery and petrochemical projects at 25%, boosted by a large Rs. 584 crore Dangote order. Engineering orders are picking up at 10%, but sugar and distillery projects have slowed to 6%—a concern since this segment has traditionally been a strong performer. Data centres are emerging as a new opportunity at 2%, hinting at future growth potential in this space.

Financial Services

Nippon Life India Asset Management Ltd. | Mid Cap | Financial Services

Nippon Life India Asset Management Limited (NAM India) is the asset manager of Nippon India Mutual Fund (NIMF). The company’s principal activity is to act as an investment manager to Nippon India Mutual Fund (Formerly Reliance Mutual Fund) (the Fund) and to provide Portfolio Management Services (PMS) and advisory services to clients under Securities and Exchange Board of India (SEBI) Regulations. The Company is registered with SEBI under the SEBI (Mutual Funds) Regulations, 1996.

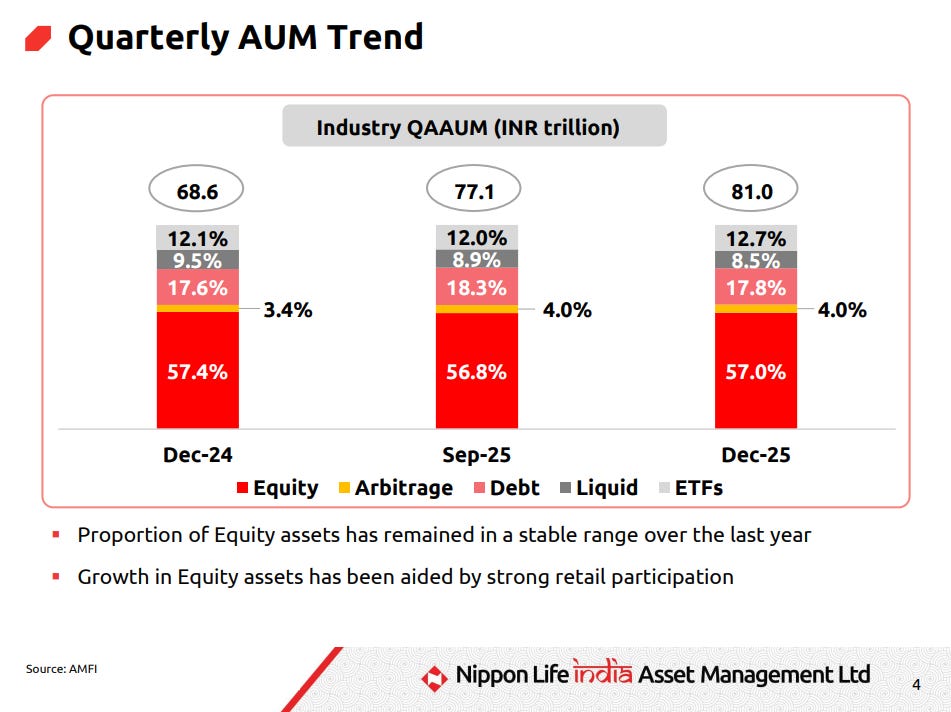

The mutual fund industry’s quarterly average assets under management (QAAUM) has grown from ₹68.6 trillion in December 2024 to ₹81 trillion by December 2025. Equity assets dominate the mix, holding steady at around 57% of total AUM throughout this period. The proportion of debt has increased slightly from 17.6% to 17.8%, while liquid funds and ETFs have seen minor shifts. Strong retail investor participation has been a key driver behind the growth in equity assets over the past year.

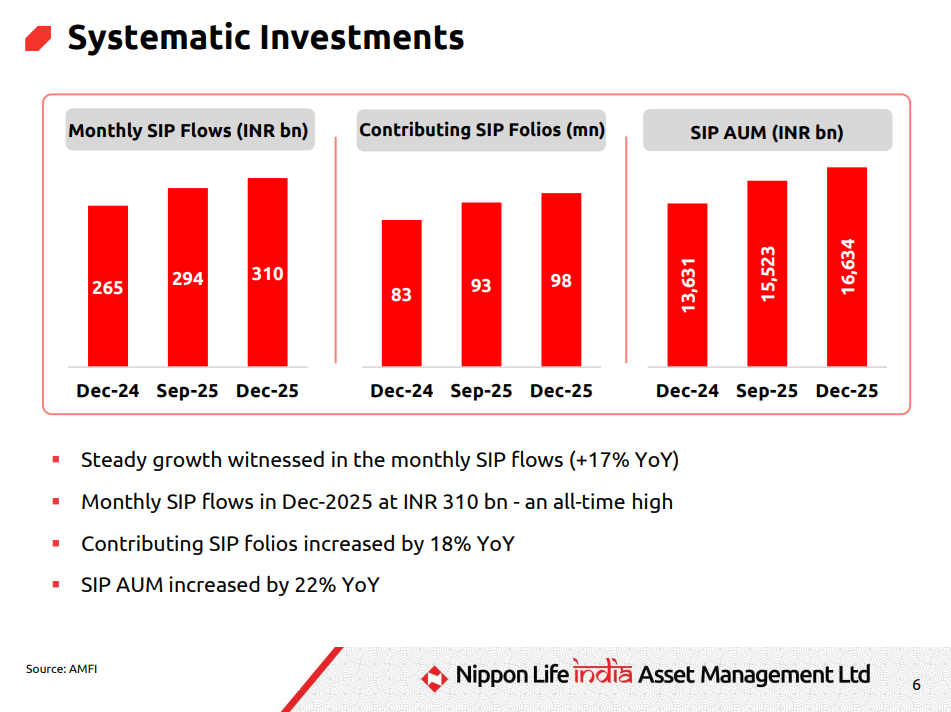

Systematic Investment Plan (SIP) flows have been climbing steadily, reaching an all-time high of ₹310 billion in December 2025, up 17% year-on-year. The number of contributing SIP folios has also grown by 18% YoY to 98 million, indicating broader retail participation. As a result, total SIP AUM has surged 22% YoY to ₹16.6 trillion by December 2025. The consistent growth in SIP inflows and active accounts reflects the increasing popularity of disciplined, long-term investing among Indian retail investors.

One Mobikwik Systems | Small Cap | Financial Services

One Mobikwik Systems is a platform business with a two-sided payments network for consumers and merchants. It offers prepaid payment instruments, payment gateway services, utility bill payments, online shopping, and financial services like loan products in partnership with financing partners.

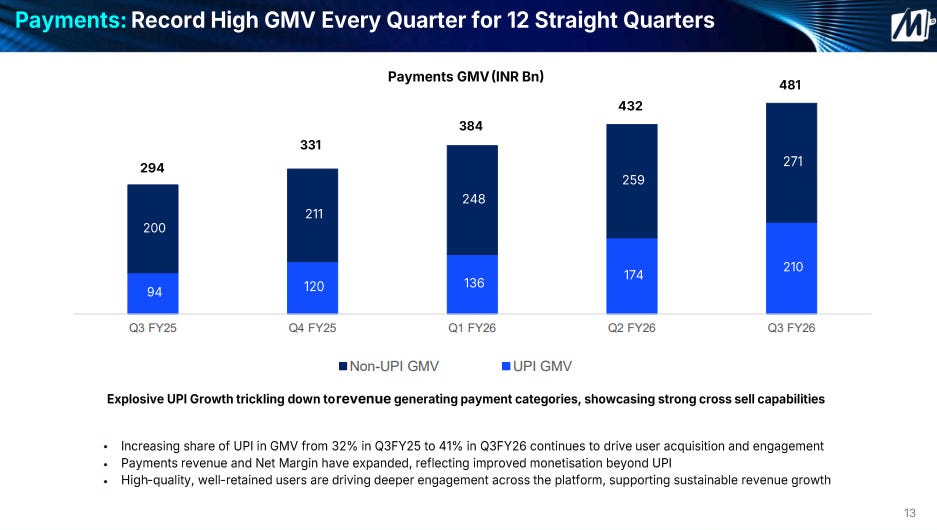

MobiKwik has achieved record-high Gross Merchandise Value (GMV) for 12 consecutive quarters, reaching ₹481 billion in Q3 FY26. UPI now accounts for 41% of total GMV, up from 32% in Q3 FY25, driven by strong user acquisition and engagement. Non-UPI payment categories continue to contribute significantly at ₹271 billion in Q3 FY26, showcasing the platform’s ability to monetize beyond UPI. The company highlights that explosive UPI growth is trickling down to other revenue-generating payment categories, with high-quality, well-retained users driving deeper engagement and sustainable revenue growth across the platform.

Auto Ancillary

Balkrishna Industries Ltd. | Mid Cap | Auto Ancillary

Balkrishna Industries Limited specializes in the Specialty Off-Highway Tire segment, catering to Agriculture, Industrial, Construction, Earthmoving, Mining, Port, Lawn and Garden, and All-Terrain Vehicle Tires markets. The company operates in a highly technical and capital-intensive sector with a wide range of products. While the agricultural sub-segment is non-cyclical, the industrial, construction, and mining sub-segment is cyclical and tied to the global economic outlook. Their products are primarily targeted at markets in Europe, America, Australasia, and India.

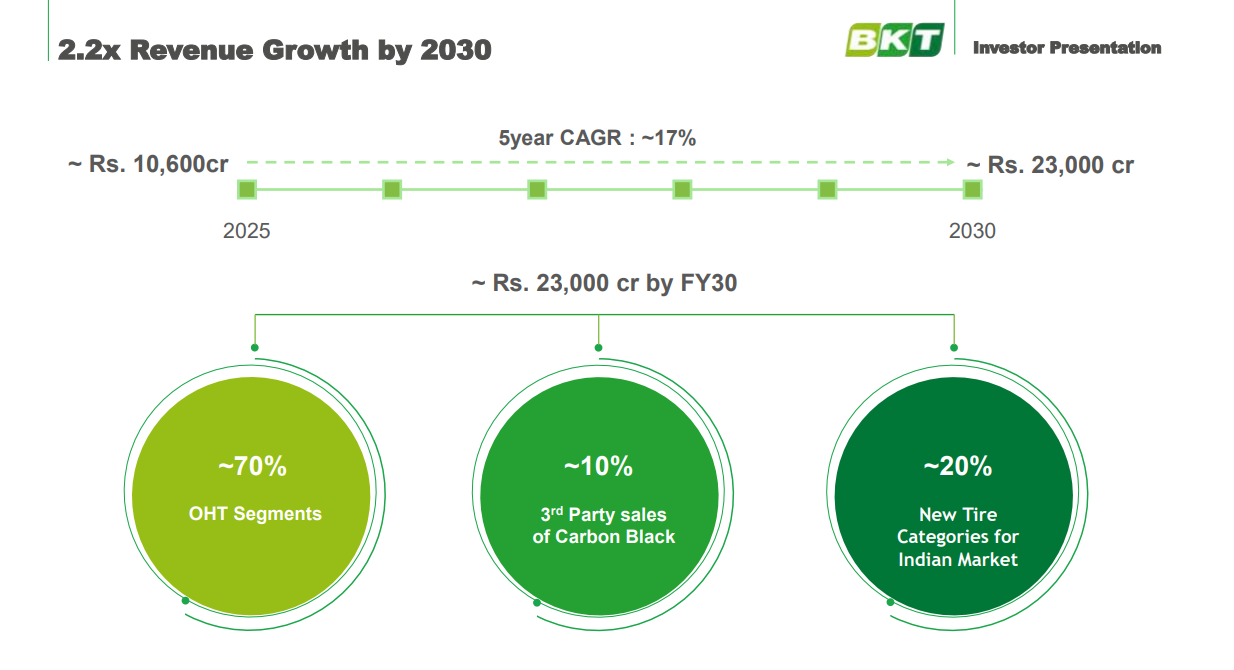

BKT is targeting a revenue of ₹23,000 crore by FY30, more than doubling from ₹10,600 crore in 2025—a compound annual growth rate of around 17%. The growth strategy is built on three pillars: OHT (Off-Highway Tire) segments will contribute roughly 70% of revenues, third-party sales of carbon black will account for about 10%, and new tire categories for the Indian market will make up around 20%. This diversified approach aims to drive sustainable expansion over the next five years.

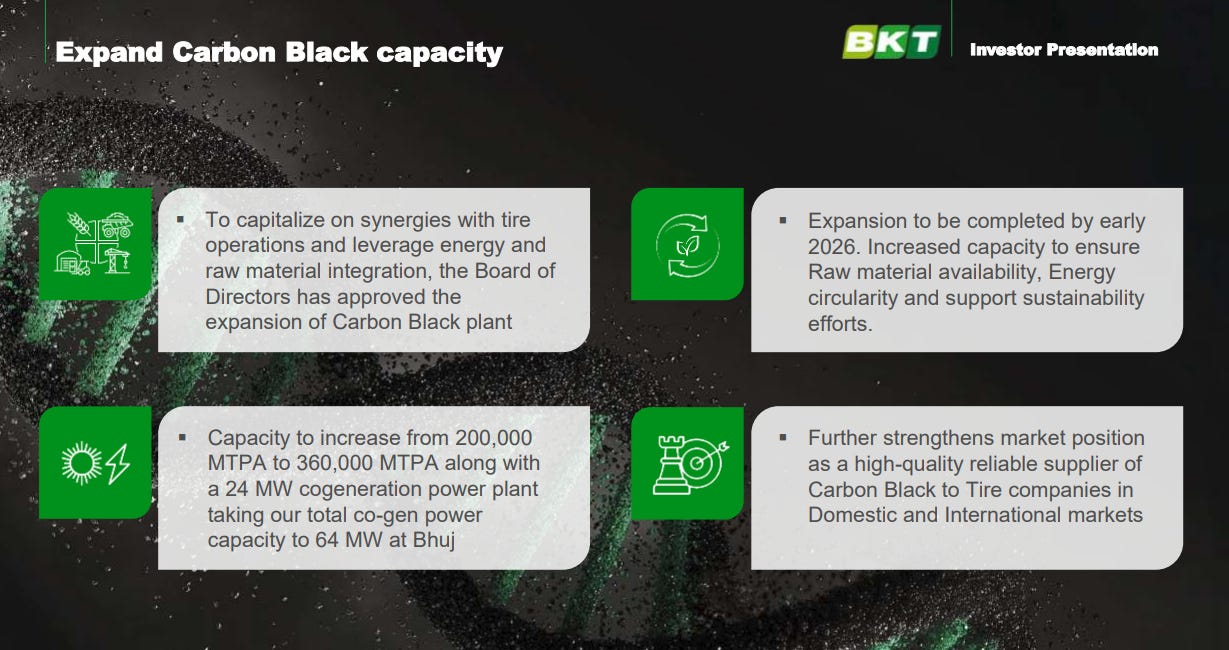

BKT’s Board has approved the expansion of its carbon black plant to capture synergies with tire operations and improve raw material integration. Capacity will increase from 200,000 MTPA to 360,000 MTPA, with a new 24 MW cogeneration power plant boosting total co-gen capacity to 64 MW at Bhuj. The expansion is expected to be completed by early 2026 and will enhance raw material availability, energy circularity, and sustainability efforts. This move also strengthens BKT’s position as a reliable carbon black supplier to tire companies in both domestic and international markets.

BKT is planning a modular entry into new tire verticals for the Indian market, targeting premium passenger car radial tires and commercial vehicle radial tires. The initial focus will be on the Indian replacement market for both categories. The company will pilot CV radial tires starting in Q4 FY26, followed by PCR tires in Q3 FY27, with both segments ramping up gradually. This strategic move aims to diversify BKT’s product portfolio beyond its traditional off-highway tire stronghold.

FMCG

DOMS Industries Ltd. | Small Cap | FMCG

DOMS Industries, formerly Writefine Products, is a company founded in 2006 in Gujarat, India. It specializes in manufacturing, marketing, and distributing school stationery and art materials under the brand names ‘DOMS’ and ‘C3’. With a market presence in India and internationally, DOMS Industries caters to the needs of students and artists.

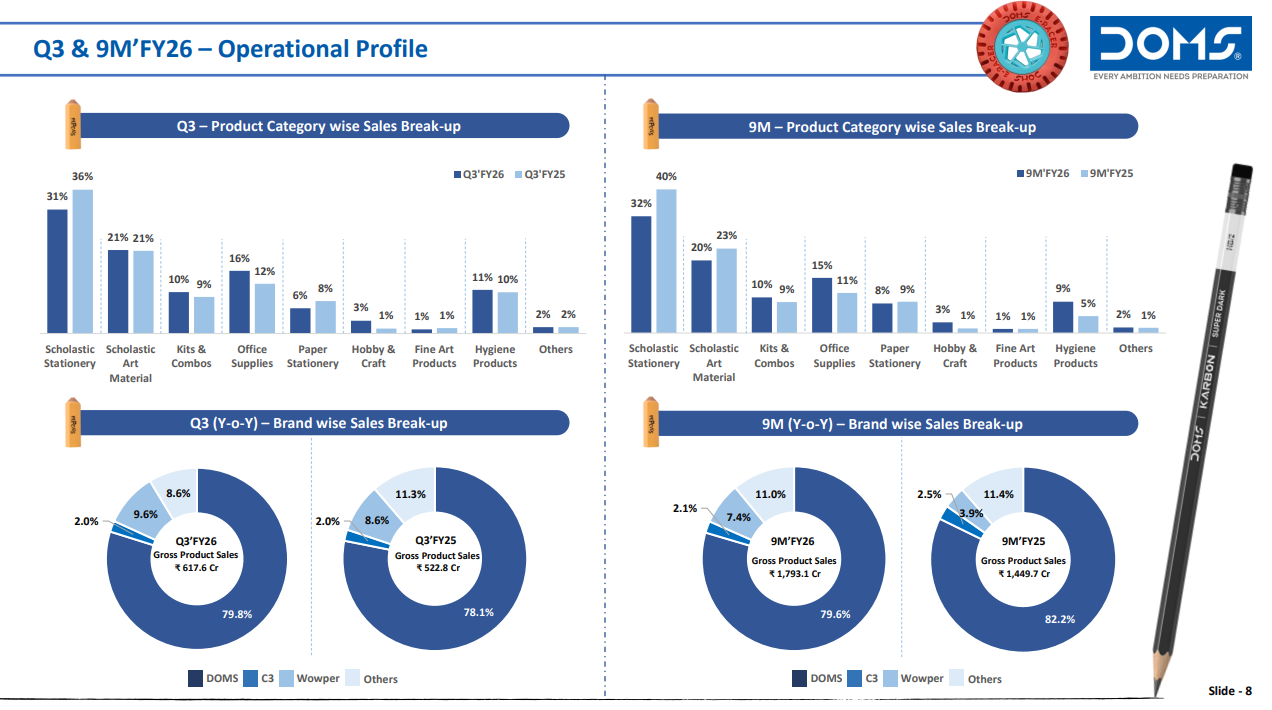

DOMS’ operational profile for Q3 and 9M FY26 shows scholastic stationery as the largest category, contributing 31% and 32% respectively, followed by scholastic art material at 21% and 20%. Brand-wise, DOMS dominates with nearly 80% of sales in both periods, while its sub-brands C3 and Wowper contribute around 8-11% and 2-3% respectively. Gross product sales stood at ₹617.6 crore in Q3 FY26 and ₹1,793.1 crore for 9M FY26, showing consistent performance across categories. The diversified product mix across stationery, art materials, kits, and office supplies reflects DOMS’ strong positioning in multiple segments.

Zydus Wellness | Small Cap | FMCG

Zydus Wellness Limited offers healthcare, nutrition, and cosmeceutical products to promote well-being. They focus on developing and distributing a wide range of health and wellness products under popular brands like Glucon-D, Complan, Sugar Free, Nycil, Everyuth, and Nutralite, aiming to help people achieve integrated well-being.

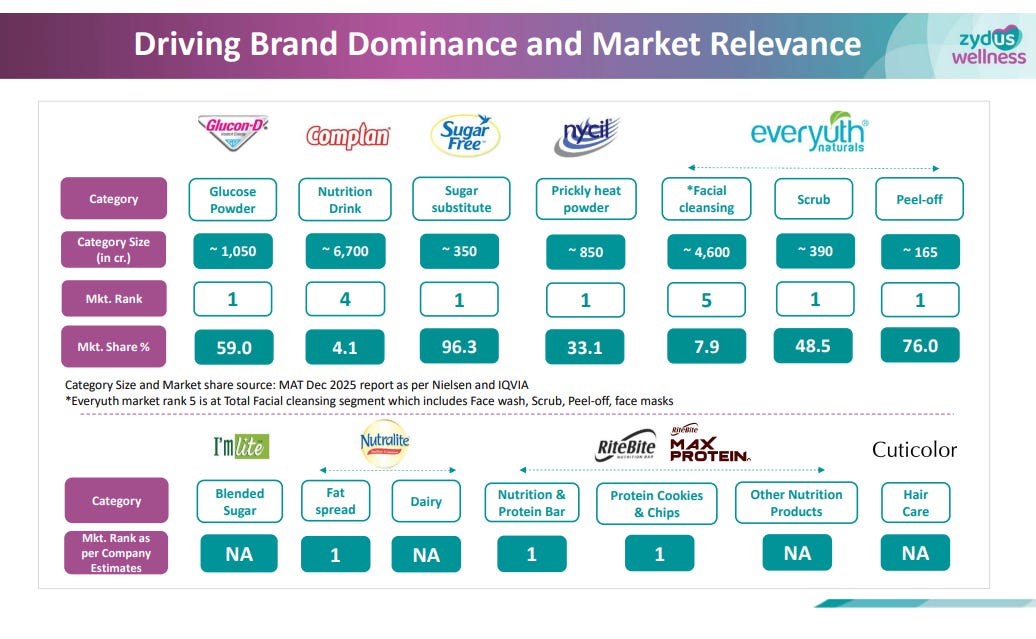

Zydus Wellness has built a portfolio of dominant brands across multiple wellness and nutrition categories. Glucon-D leads the ₹1,050 crore glucose powder market with 59% share, while Sugar Free commands a massive 96.3% of the ₹350 crore sugar substitute segment. Nycil holds 33.1% of the prickly heat powder category (₹850 crore), and Everyuth’s facial cleansing products control 48.5% of the scrub market and 76% of peel-offs. Beyond these, the company also holds the #1 position in fat spreads and nutrition bars through Nutralite and RiteBite, with additional presence in dairy, protein snacks, and hair care via Cuticolor.

Logistics

TCI Express | Small Cap | Logistics

TCI Express Limited offers transport, storage, warehousing, and support services with a focus on express distribution. They provide time-bound solutions across various sectors like automotive, pharmaceutical, textiles, IT, retail, and e-commerce, including domestic and international air express services.

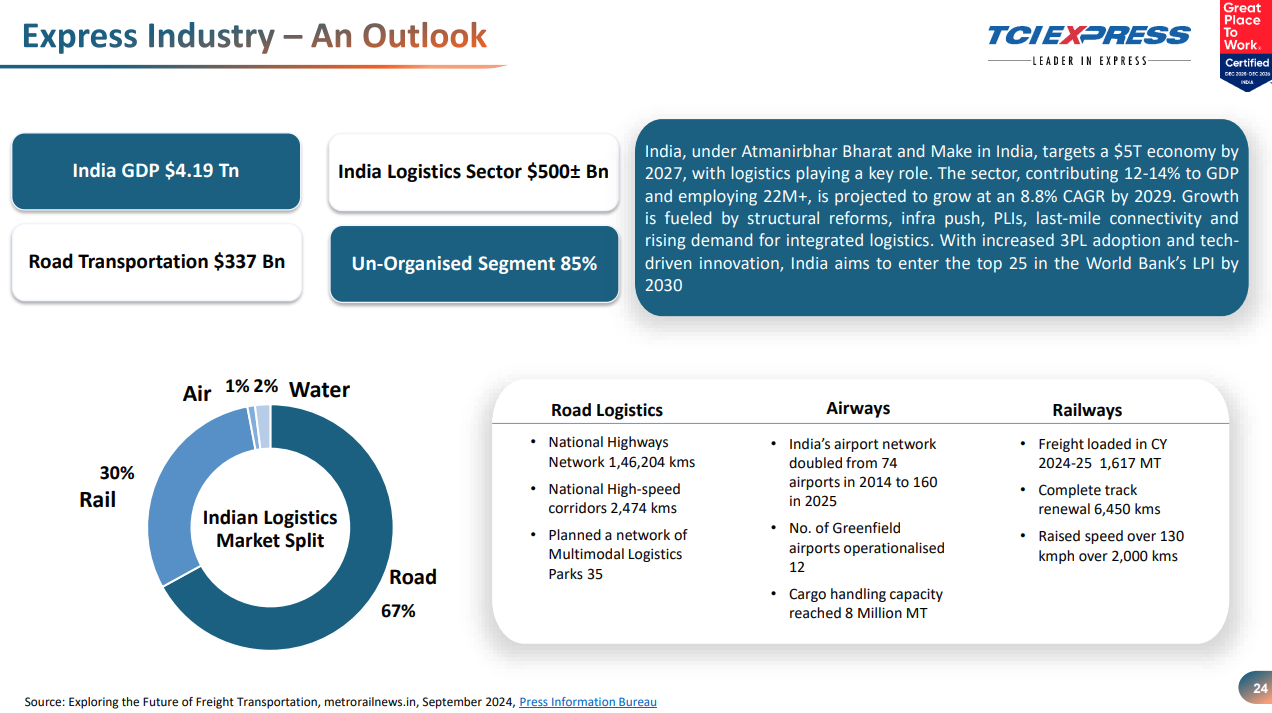

India’s logistics sector is valued at over $500 billion and is expected to grow at 8.8% CAGR through 2029, contributing 12-14% to GDP and employing 22 million people. Road logistics dominates with a 67% market share, supported by a 1.46 lakh km national highways network and 2,474 km of high-speed corridors, though 85% of the segment remains unorganized. Railways account for 30% of the market with ongoing track renewal and speed improvements, while air freight handled 1.6 MT in CY 2024-25, with airport capacity doubling since 2014. The government’s focus on infrastructure, last-mile connectivity, and technology-driven logistics aims to position India among the top 25 in the World Bank’s LPI by 2030.

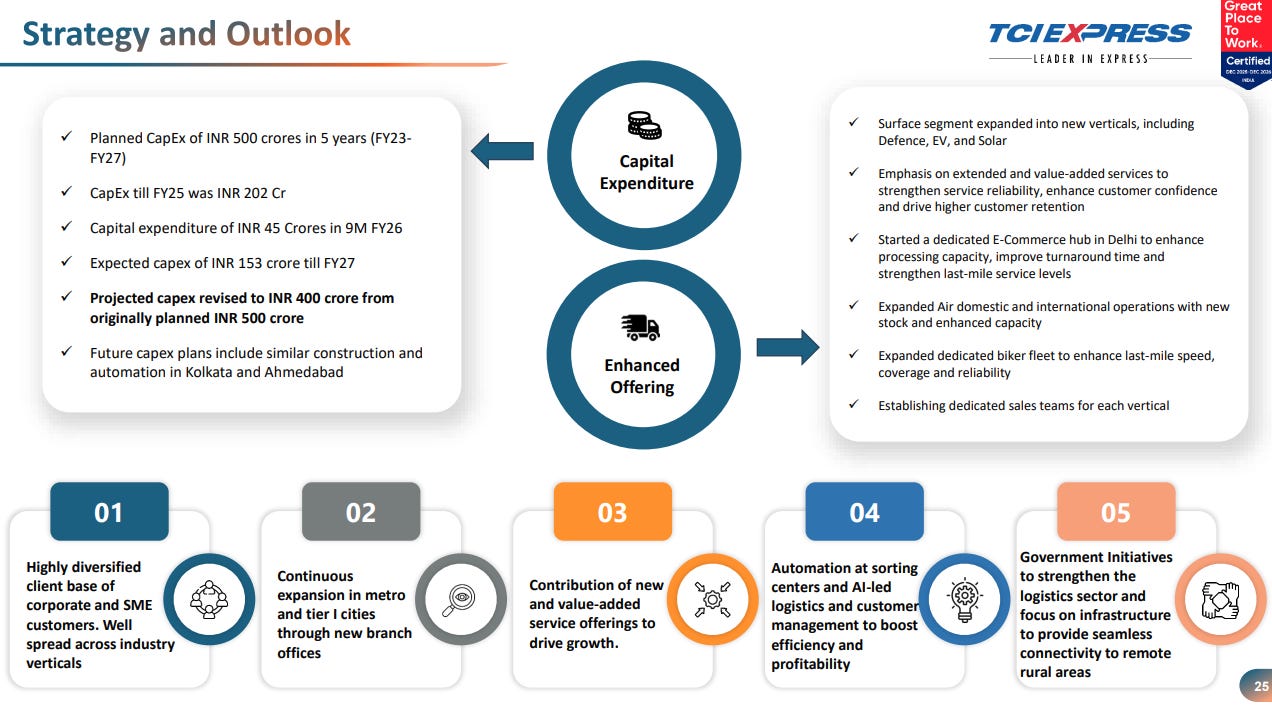

TCI Express is planning a revised capex of ₹400 crore through FY27, down from the original ₹500 crore target, with ₹45 crore already spent in 9M FY26. The investment will focus on expanding infrastructure in Kolkata and Ahmedabad, and enhancing service offerings across defence, EV, solar, and e-commerce verticals. The company is expanding its air freight operations, setting up a dedicated e-commerce hub in Delhi, and increasing its biker fleet for faster last-mile delivery. Additionally, TCI is adopting automation and AI-led logistics at sorting centers to improve efficiency, while leveraging government infrastructure initiatives to strengthen its pan-India presence across metro and tier-1 cities.

Media & Entertainment

Saregama India | Small Cap | Media & Entertainment

Saregama India Limited, a part of RP Sanjiv Goenka Group, is India’s oldest music label and a leading film studio. It holds the largest collection of Indian music copyrights spanning multiple languages. With over 4000 hours of TV content and innovative initiatives like Saregama Carvaan and Yoodlee Films, the company continues to innovate and evolve in the music and entertainment industry.

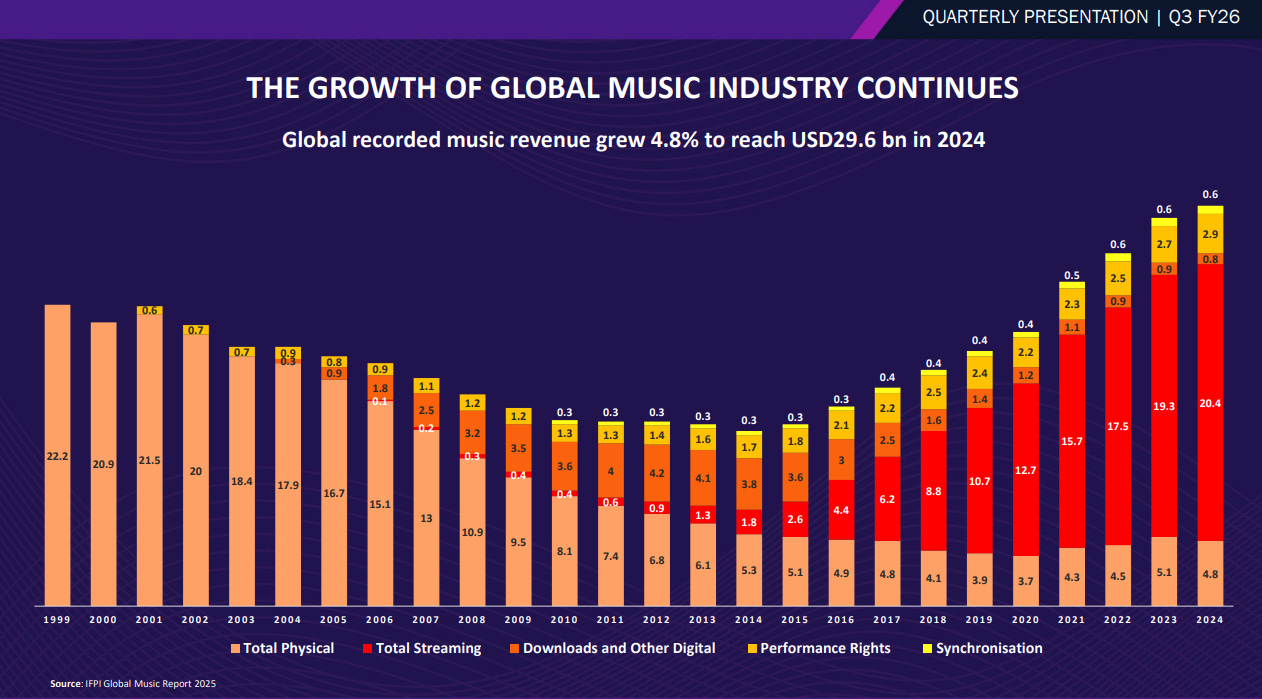

Global recorded music revenue grew 4.8% to reach $29.6 billion in 2024, continuing the industry’s recovery from the digital disruption of the early 2000s. Streaming now dominates the revenue mix at $20.4 billion, overtaking physical sales which have declined sharply from $22.2 billion in 1999 to just $4.8 billion in 2024. Downloads and other digital formats peaked around 2012 but have since faded, while performance rights and synchronization remain steady contributors. The chart shows a clear shift toward streaming-driven growth, reversing the decade-long revenue decline the industry faced between 2000 and 2014.

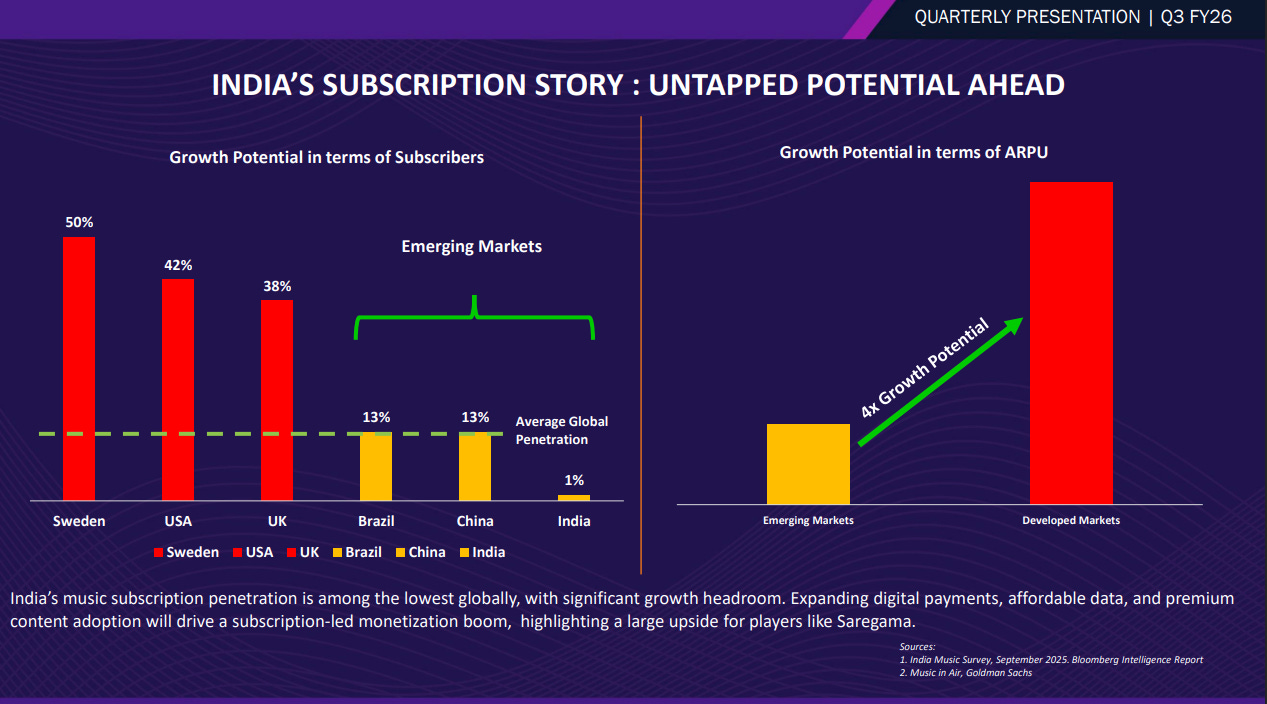

India’s music subscription penetration stands at just 1%, far below developed markets like Sweden (50%), USA (42%), and UK (38%), and even trailing emerging peers like Brazil and China at 13%. This low penetration presents massive growth potential, with ARPU in emerging markets having 4x headroom compared to developed markets. Expanding digital payments, affordable data, and increasing adoption of premium content are expected to drive a subscription-led monetization boom in India, offering significant upside for players like Saregama.

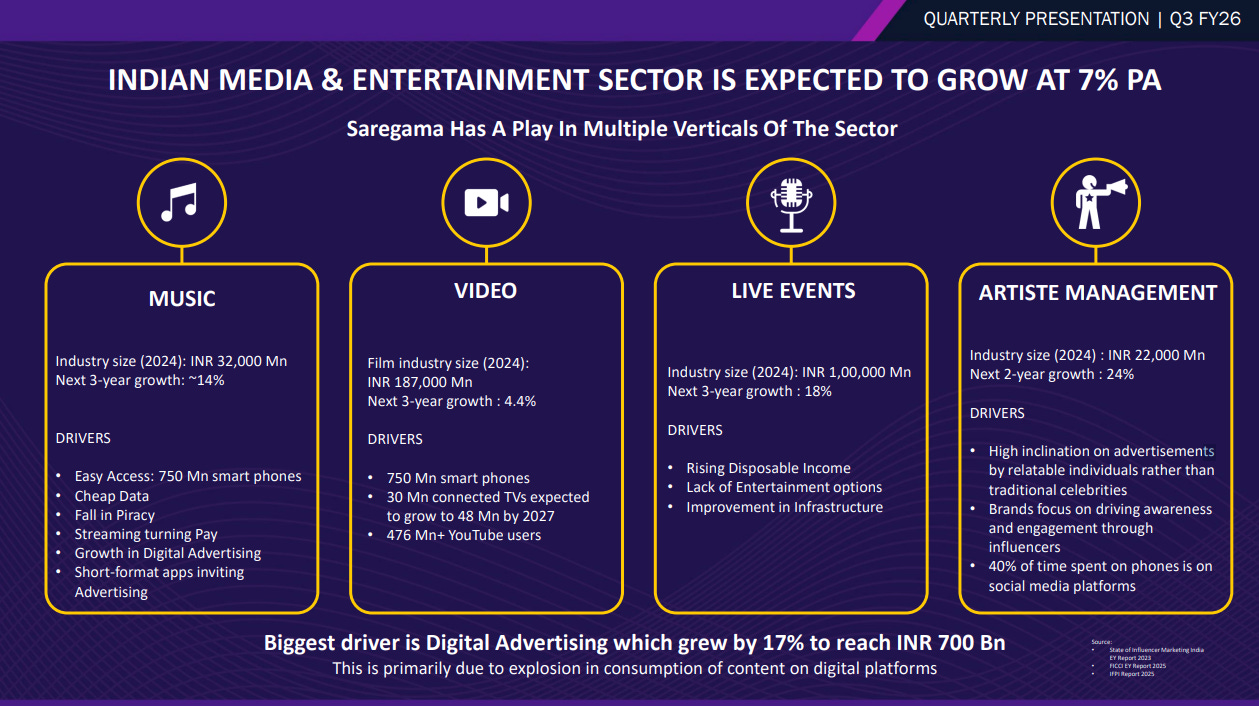

India’s media and entertainment sector is projected to grow at 7% annually, with Saregama positioned across multiple high-growth verticals. The music industry, valued at ₹32,000 million in 2024, is set to grow ~14% over the next three years, driven by 750 million smartphones, cheap data, and the rise of streaming and digital advertising. The video segment, worth ₹187,000 million, is expected to grow 4.4% as connected TV households expand from 30 million to 48 million by 2027. Live events, valued at ₹100,000 million, are projected to grow 18%, fueled by rising disposable incomes and better infrastructure, while artist management (₹22,000 million) is set to grow 24% as brands increasingly leverage relatable influencers and social media engagement. Digital advertising, the biggest growth driver, surged 17% to reach ₹700 billion, reflecting the explosion of content consumption on digital platforms.

Saregama’s total revenue in FY25 stood at ₹11,713 million, with music licensing and artist management contributing 52%, making it the largest segment. The retail business (Carvaan) has declined from ₹2,062 million in FY20 to ₹837 million in FY25, reflecting a shrinking market for physical music devices. The video segment—comprising films, digital series, TV shows, and short-format content—has grown steadily from ₹702 million in FY20 to ₹1,920 million in FY25, now accounting for 16% of total revenue. Live events have surged dramatically from ₹490 million in FY23 to ₹2,852 million in FY25, capturing 24% of revenue and emerging as a major growth driver for the company.

Diversified

Adani Enterprises | Large Cap | Diversified

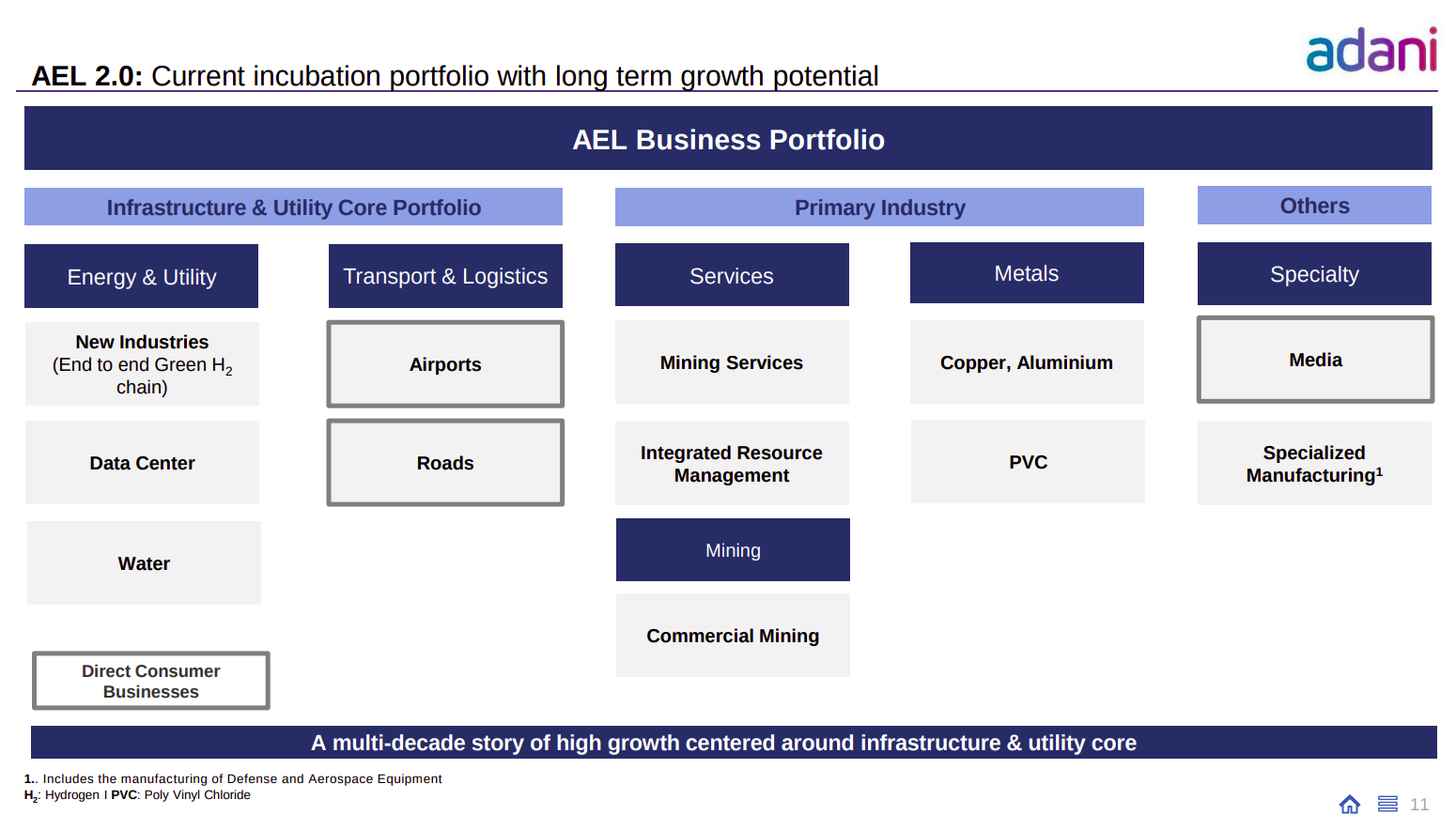

Adani Enterprises is a multifaceted company involved in integrated resources management, mining services, and trading activities. It serves as an incubator for emerging businesses in sectors such as new energy, data centers, airports, roads, copper, and digital space.

AEL 2.0 is Adani’s long-duration option pool—a portfolio of incubation bets built around infrastructure and utilities, with exposure to future-facing themes like green hydrogen, data centers, airports, mining services, metals, and water, where capital intensity and regulatory complexity create high entry barriers and long-term compounding potential rather than near-term earnings.

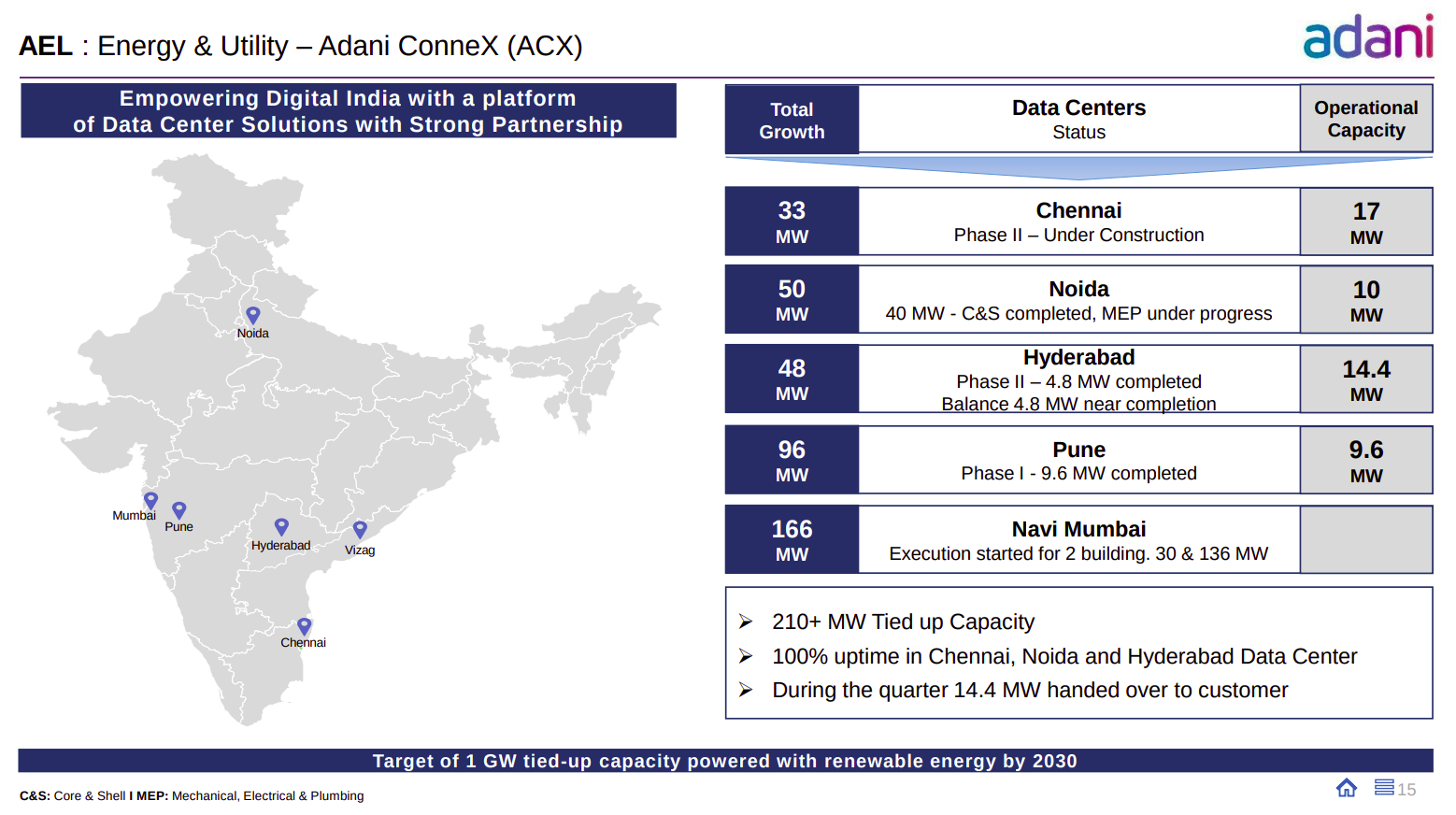

Adani ConneX is Adani’s data-center platform built as a long-term infrastructure play, with capacity already tied up across India’s key digital hubs (Chennai, Noida, Hyderabad, Pune, Navi Mumbai), low initial MW live today but a large pipeline (210+ MW tied-up; 1 GW target by 2030)—signaling a deliberate “build-ahead-of-demand” strategy where execution, uptime, and access to cheap renewable power matter more than near-term utilization.

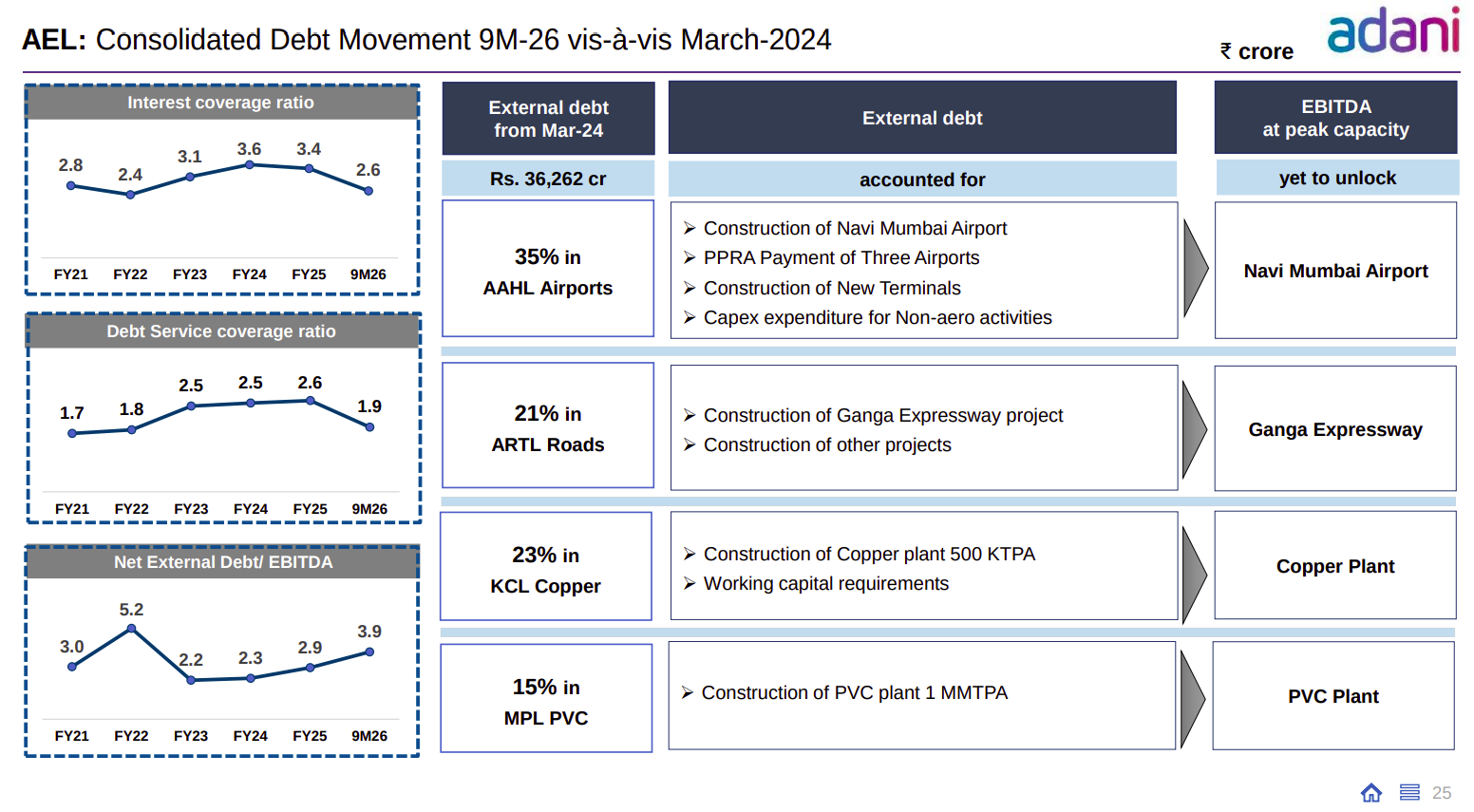

AEL’s debt increase is largely front-loaded capex debt tied to long-gestation infrastructure assets, not stress—~₹36,000 cr of external debt is funding airports, roads, copper and PVC projects that are still under construction, which explains why leverage metrics look optically weaker today but are expected to normalize as EBITDA ramps up once Navi Mumbai Airport, Ganga Expressway, and the copper/PVC plants move to peak utilization.

Software Services

eMudra | Small Cap | Software Services

eMudhra Limited, the largest licensed Certifying Authority in India, offers Digital Trust Services including various types of certificates and Enterprise Solutions to individuals and organizations across different industries. They provide a wide range of services from issuing certificates to offering identity, authentication, and signing solutions, making them a comprehensive player in secure digital transformation.

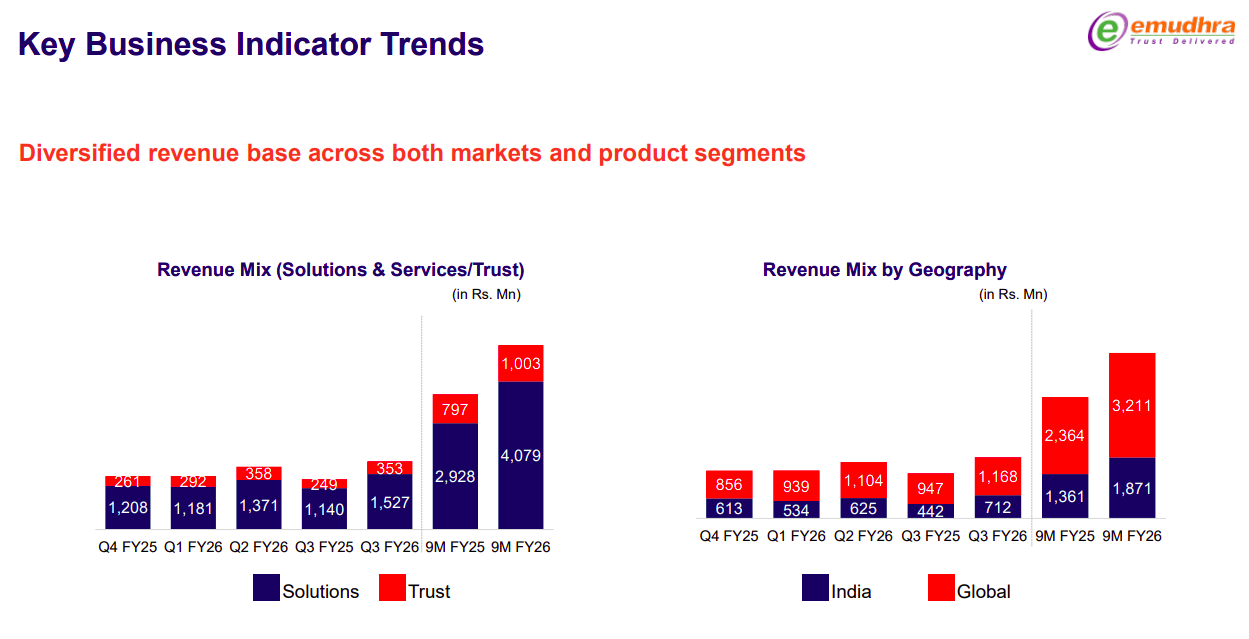

eMudra’s growth is becoming structurally de-risked, with revenue diversification happening on two axes at once—products (Solutions + Trust) and geography (India + Global)—so growth is no longer dependent on a single market or use-case; the sharp step-up in 9M FY26 shows both higher-value Solutions scaling faster and international revenues catching up with India, improving revenue resilience and lowering policy/regulatory concentration risk.

That’s it for now! Your feedback will really help shape how Points and Figures evolves. Drop it down in the comments below!

Quotes in this newsletter were curated by Kashish & Vignesh.

Disclaimer: We’ve used AI tools in filtering and cleaning up the quotes from the images so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Points and Figures is run by the same team that creates The Daily Brief and Aftermarket Report.