Hi, I’m Kashish and I work on Plotlines.

It builds on Chatter, but with a more structured lens. Instead of looking at management commentary from earning concalls in isolation, we track a single theme across companies and over time to connect the dots. The goal is to piece together how narratives evolve, and surface the deeper structural shifts shaping industries.

For today’s episode, we wanted to know how are Indian pharma companies planning to make money off of the GLP-1 trend?

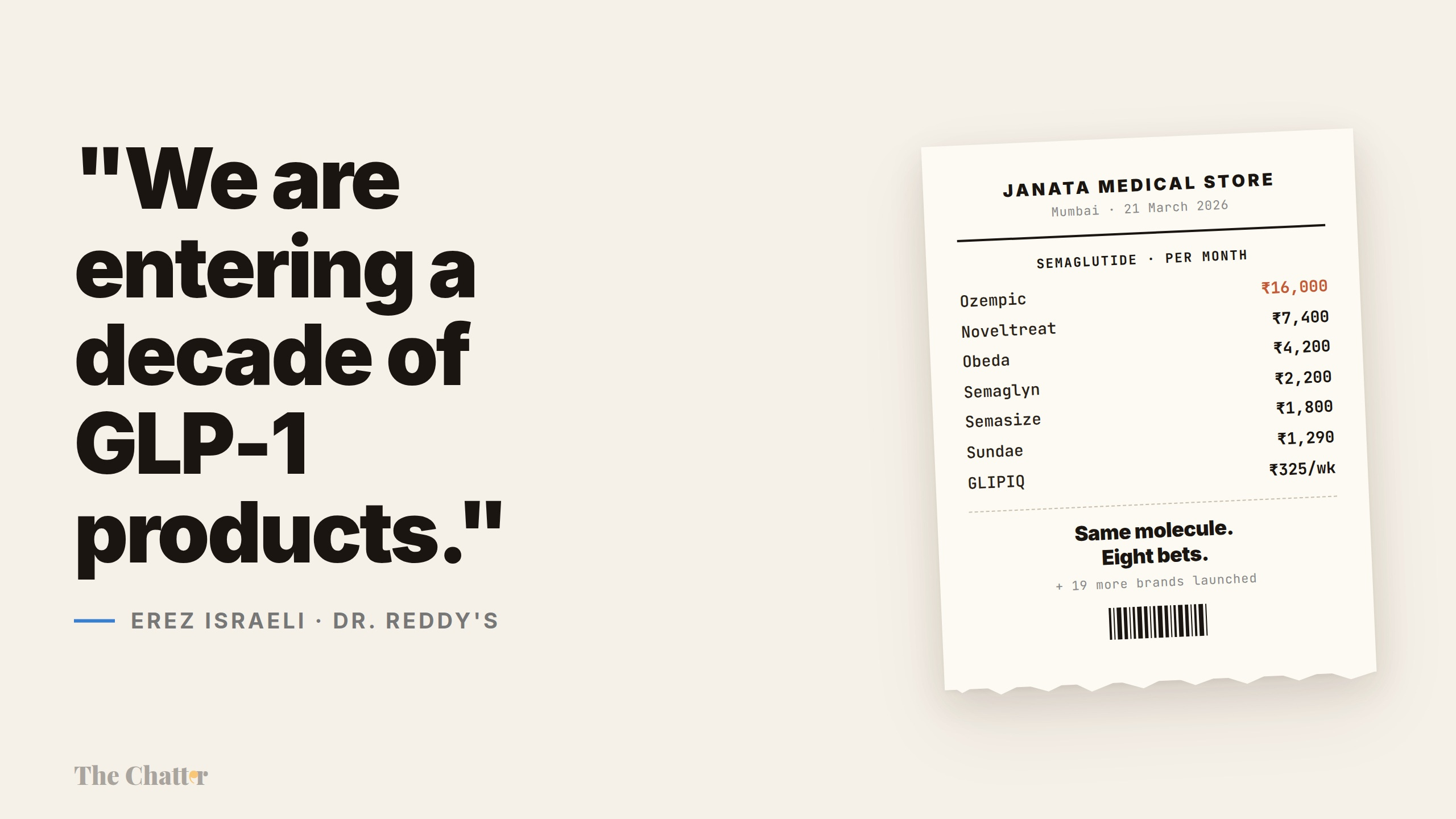

On the evening of 20 March 2026, hours before Novo Nordisk’s Indian patent on semaglutide formally expired, Natco Pharma announced that its generic vial would sell for ₹1,290 a month. The original drug, at innovator pricing, had been going for roughly ₹16,000. By the next morning, six more domestic firms had piled in. By the end of the week, thirteen companies had launched twenty-six brands. Within a month, more than fifty were on the market or in the queue.

The interesting question isn’t who launched — almost everyone did. The interesting question is what each company is actually doing: whether they’re making the drug, selling it, both, or simply renting out their distribution to someone who has already done the harder work. The same molecule, the same patent cliff, the same 250-million-strong pool of potential patients — and six very different ways to make money off all of it.

Over the last four quarters, we read through earnings calls from 27 listed Indian pharma companies — more than 140 calls in total — to map what each one is actually up to. Here’s what we found.

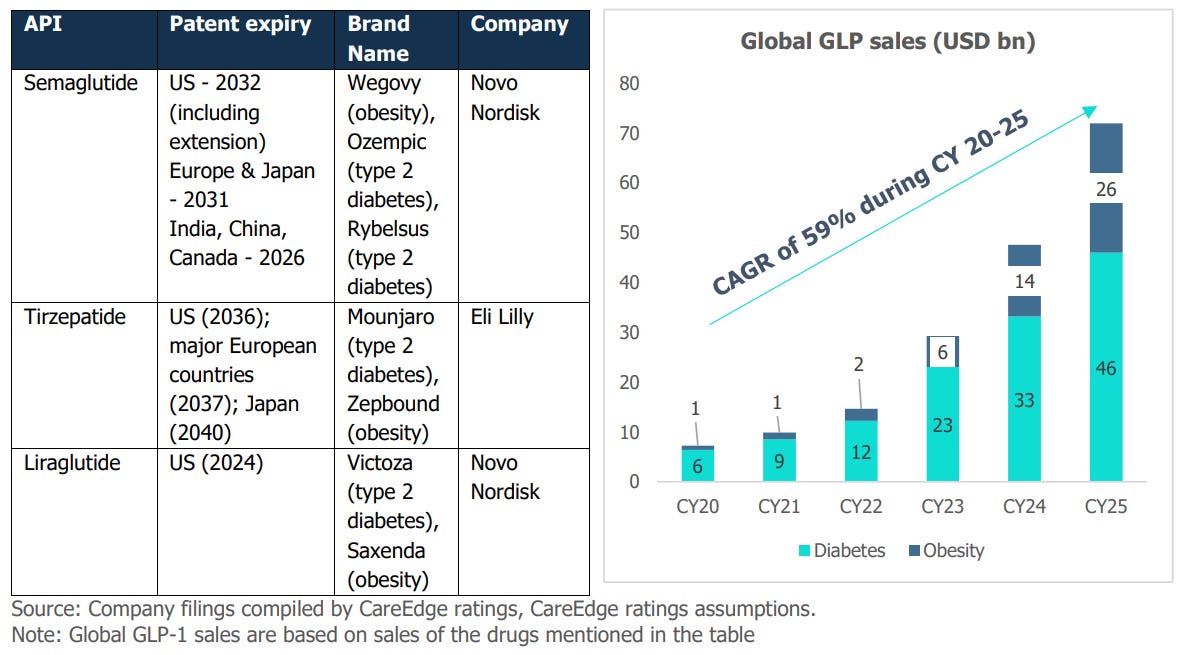

A note on the prize before we get there. India’s GLP-1 market — semaglutide plus Eli Lilly’s tirzepatide — was worth about ₹571 crore in 2024. By February 2026, on a rolling twelve-month basis, it had jumped to ₹1,446 crore, with the anti-obesity slice alone more than doubling. But that figure is the market the innovators built: until 21 March, semaglutide was still on patent, so almost all of it was Novo’s and Lilly’s branded money.

Three estimates of where it goes from here: Systematix sees a ₹5,000-crore incremental opportunity across India, Brazil and Canada combined over the next 12-15 months; CareEdge expects India alone to reach ₹5,000 crore by 2030; and Jefferies, more bullish, sees a market north of $1 billion in India.

Set against those projections, what the new entrants have actually booked is almost nil. Cipla’s Yurpeak — itself an innovator launch, Lilly’s tirzepatide sold under a Cipla brand — did ₹14 crore in its first month. Eris’s liraglutide, an older off-patent GLP-1, does about ₹1 crore a month. Every generic semaglutide launched only in the last week of March, so a full quarter of post-launch sales simply doesn’t exist yet. What follows is a description of strategy, not of a profit pool that has already formed.

A primer — what it is, who makes it, how it’s sold

Start with what the drug actually does, because that’s what explains the gold rush.

GLP-1 — glucagon-like peptide-1 — is a hormone your gut releases after you eat. It nudges the pancreas to put out insulin, tells the brain that you’re full, and slows down how quickly the stomach empties. Drugs like semaglutide are engineered copies of that hormone, tuned to last a week in the body instead of a few minutes. Take one injection a week and your appetite quietly shrinks, your blood sugar steadies, and the weight comes off — often 15% of body weight or more.

Sidenote: We discussed about GLP-1 in depth in this podcast.

Now, the cast.

The two innovators. Two foreign drugmakers built the entire global GLP-1 market between them.

Novo Nordisk, a Danish company, makes semaglutide — the molecule everyone is now copying. Novo sells it under three brand names: Ozempic (an injection, for type 2 diabetes), Wegovy (the same molecule at higher doses, for obesity), and Rybelsus (an oral tablet). When people say “Ozempic” colloquially, they usually mean semaglutide in general.

Eli Lilly, an American company, makes tirzepatide — a different molecule that works on the same biological pathway but has shown stronger weight-loss results in trials. Lilly sells it under one global brand, Mounjaro. In India, Lilly has partnered with Cipla to market it under a separate brand, Yurpeak.

What “going off patent” actually means. A patent gives the original drugmaker an exclusive selling window. When it expires — the industry calls this the “loss of exclusivity”, or LOE — other companies can legally make and sell copies, called generics. Semaglutide’s Indian patent expired on 21 March 2026. Tirzepatide’s runs until at least 2030. So semaglutide is now fair game. Tirzepatide is still legally Lilly’s alone.

Pens vs vials — why the device matters. Semaglutide is an injection a patient takes once a week, for years on end. How it’s packaged changes the economics entirely.

A vial is a glass bottle of the liquid drug. To inject, the patient — or a clinic nurse — has to draw the right dose into a separate syringe. Vials are cheap to manufacture but fiddly to use: dosing errors are common, and most patients won’t self-inject from one.

A pen is a pre-loaded injector with a dial. The patient turns the dial to the prescribed dose, presses the pen against the skin, and pushes a button. It costs three to six times more to make than a vial. But it’s dramatically easier to use — and adherence, patients sticking with the therapy long enough for it to actually work, depends almost entirely on the device.

Hold that distinction in your head. It does most of the work in Bets 1 and 6.

Bet 1 — Be there on day one with a generic pen

The default play: show up on 21 March with a branded generic, fight for share through the sales force, and ride the volume.

Almost every Indian pharma company took some version of this bet — Sun, Dr Reddy’s, Lupin, Zydus, Alkem, Natco, Cipla, Glenmark, Torrent, Mankind, Eris. The interesting thing is that nobody priced the same way. Within ten days of launch, the Indian generic semaglutide market had split into three distinct price tiers — and the tier a company chose determined who its patient was.

The cheapest tier was vials. Natco opened at ₹1,290 a month for a vial; Glenmark’s GLIPIQ launched even lower, at ₹325 a week. These prices are roughly a tenth of Novo’s. The trade-off: patients can’t easily self-inject from a vial, so this tier really only works in clinics where staff can manage the dosing — or with the small fraction of patients comfortable handling a syringe.

The middle tier was affordable pens — Alkem, Zydus, Natco’s own pen device — in the ₹1,800-4,500-a-month range. Same molecule as the vial, but in the easy-to-use injector. This is where the mass-market volume will likely settle once price competition has done its work.

The premium tier was high-end pens with patient support wrapped around them — Dr Reddy’s at ₹4,200, Sun at ₹2,960-7,400 depending on dose. These companies are betting that better device design, a branded experience and patient education can justify a premium even after generics have flooded the market.

Same drug, ₹325 a week to ₹7,400 a month. Different patients, different doctors, different settings.

“Sun Pharma plans to be in market on day-one of a generic launch. We have already received the regulators’ approval for both the indication of chronic weight management as well as treatment of type 2 diabetes under the brand name Noveltreat and Sematrinity respectively.”

— Kirti Ganorkar, Managing Director, Sun Pharma | Q3 FY26

The honest part of this bet is that everyone running it knows exactly what it looks like. Crowded. Loud. Margin-thin within a few quarters.

“There’s a mad rush in the market. Every company is launching. And if at this particular time, you launch, you will be lost somewhere.”

— Rajeev Juneja, Vice Chairman & MD, Mankind Pharma | Q4 FY26

“I am not going to tell you that we are going to make a lot of money in India, I will never say that, I actually agree with you, it will be very competitive.”

— Rajeev Nannapaneni, Vice Chairman & CEO, Natco Pharma | Q2 FY26

So why run it anyway? Two reasons. The market is so big that even a thin slice is real money. And being absent on day one means being absent forever — Indian doctors tend to stick with whichever brand they wrote first. That’s why Lupin, Dr Reddy’s and Sun all set internal targets to rank top-three among generics from week one.

“Our goal is very clear to be at Top 3 player in this as generic Semaglutide and I think we’re well on track.”

— Nilesh Gupta, Managing Director, Lupin | Q4 FY26

The early post-launch read suggests Torrent has surprised everyone. The single decision that won it that share was launching the oral version alongside the injectable — something no other generic did at scale.

“Torrent held 38% share among generic players as per the Pharmatrac April data set, with 28% share in the injectable format and 100% share in the oral format.”

— Aman Mehta, Management, Torrent Pharmaceuticals | Q4 FY26

In rupee terms, even Torrent’s standout is small — about ₹17 crore of monthly sales against a quarterly revenue base of roughly ₹3,000 crore. For now, the point of Bet 1 is defensive: don’t let the competitor own the diabetes prescription pad. The money comes later.

Bet 2 — Don’t fight the generics, sell the original

Here’s the counter-bet. If the generic market is going to be a knife fight at ₹1,290 a month, why be in it at all? Instead, partner with the original drugmaker, sell their actual product at a premium, and lean on their global data and their device.

Emcure took this bet hardest. In late 2025, it signed an exclusive deal with Novo Nordisk to launch Poviztra in India. Poviztra is the same drug as Wegovy — Novo’s semaglutide for obesity — just sold under a different brand name in India by Emcure. The molecule is identical. The device is identical (Novo’s own pen). And the data behind it is the same global trial evidence Novo has been collecting for years.

“It was after a fierce competition there were at least 8 or 9 companies who were interested in partnering with Novo Nordisk and they selected Emcure. And we became the only company to launch the innovator drug in the game-changing semaglutide category.”

— Satish Mehta, MD & CEO, Emcure Pharmaceuticals | Q3 FY26

The logic is straightforward. Post-LOE, you have 17 generic semaglutide brands fighting for shelf space, and none of them have Novo’s vast trial record — the evidence on how the drug behaves in patients who also carry other conditions, what the industry calls comorbidities. So Emcure’s pitch to doctors is simple: this is the actual Wegovy, just at a more accessible price than the imported original.

“If you look at the construct of this deal, obviously, post-LOE, we anticipate a very crowded market in India. And so the ability to partner with Novo and launch this brand ahead of the competition and allowing ourselves to shape the market and have brand recall versus being lost in the crowd probably 4, 5 months down the line is something that we feel strongly will allow us to succeed.”

— Vikas Thapar, President, Corporate Development, Emcure | Q2 FY26

Cipla ran a different version of the same bet — and arguably the cleaner one. Rather than partnering with Novo on semaglutide, which is now copyable, Cipla partnered with Eli Lilly on tirzepatide, launching Yurpeak in India in late 2025. Yurpeak is Lilly’s Mounjaro, marketed in India by Cipla under a different name.

The crucial difference is the patent. Tirzepatide’s Indian patent runs until at least 2030, so Cipla isn’t fighting any generic competition at all. It’s selling a still-patented innovator drug, at innovator-adjacent prices, into a country where Mounjaro became the second-largest pharmaceutical retail product within a year of launch. It helps that tirzepatide mimics two gut hormones rather than one — GIP as well as GLP-1 — which is why its trials show even bigger weight loss.

“Tirzepatide is the first and only dual agonist of GIP and GLP-1, which makes it a very unique proposition. And while both products have been launched by the respective innovators, you can see from the uptake that Tirzepatide uptake is far ahead.”

— Achin Gupta, Global COO, Cipla | Q2 FY26

“As you see from IQVIA data, last month the molecule was clocking upwards of Rs. 130 crores a month. So, our efforts are primarily focused on that.”

— Achin Gupta, MD & Global CEO Designate, Cipla | Q3 FY26

Yurpeak’s ₹14 crore in its first month annualises to about ₹168 crore at the launch run-rate. Small against Cipla’s quarterly revenue — but it’s a healthy margin on a molecule that is still on patent, while the rest of the industry slugs it out at near-cost prices.

Both Emcure and Cipla are making the same wager: don’t try to be the cheapest. Try to be the only one allowed to sell the real thing.

Bet 3 — Differentiate the device

A third group accepted that they’d be launching a generic, but decided to win share through a better pen rather than a lower price.

Zydus went furthest here. The standard semaglutide regimen forces patients to switch devices as the dose climbs — one pen for the first four weeks at the starter dose, another at the next level, another for maintenance. Three different disposable pens over the first few months. Zydus built a single reusable pen with a 15 mg / 3 ml cartridge that handles every dose.

“We have a new formulation where it’s a very significant ease to the patient in terms of use. Also, there is a very meaningful benefit in terms of cost because today, we have in, typically for weight loss, you have to shift from the first four weeks to the next four weeks with a different dose and that means a different pen device. For us, we have a…. and we don’t need to make any changes from the initial dosing to the higher dosing.”

— Dr. Sharvil Patel, Managing Director, Zydus Lifesciences | Q3 FY26

The clever part is what Zydus did next. Instead of trying to take share alone, it licensed the same pen to Lupin and Torrent under semi-exclusive co-marketing deals. Three of the strongest sales forces in India, all pushing the same differentiated device.

“This being a highly competitive product with the multiple launches, we believe that the best strategy would be to launch with more players to create more share of voice and more impact for the new formulation with the customers.”

— Dr. Sharvil Patel, Managing Director, Zydus Lifesciences | Q4 FY26

The arithmetic is striking. Lupin’s, Torrent’s and Zydus’s generic injectable market in April 2026 — 57% of all generic semaglutide sales in India — all flow back to Zydus’s Ahmedabad production lines. The device was the moat and partnerships with others was the distribution.

“The product from Zydus is a unique pen and I think that’s differentiation in the market as well. Our patient support program is pretty solid as well. So, a so good start. I think we’re the number two company as a generic one, the number three as a product itself.”

— Nilesh Gupta, Managing Director, Lupin | Q4 FY26

Sun Pharma’s differentiation was an auto-injector — a pen designed so the needle stays hidden and the injection happens automatically when the patient holds it against the skin. Same molecule, same dose; what changes is the patient’s experience.

“The product has been received very well by the doctor community and one of the differentiating points is our auto-injector as well as the pen system which was appreciated by the doctors and patients equally well.”

— Kirti Ganorkar, Managing Director, Sun Pharma | Q4 FY26

Bet 4 — Sit out the rush

Mankind Pharma did something none of its peers did. It launched a pen, then deliberately refused to compete on price, refused to launch the cheaper vial, and started pointing its energy elsewhere.

“In this competitive market, we have launched our GLP Pen. And we are not in a hurry to launch vials. We are not in a hurry to cut down the prices.”

— Rajeev Juneja, Vice Chairman & MD, Mankind Pharma | Q4 FY26

This is the contrarian bet. The logic: when 50 companies are fighting over the same molecule at falling prices, the better business isn’t winning that fight. It’s selling all the other things patients on GLP-1 also need.

“We are focusing on GLP-1. It’s a long term and a large opportunity for any Indian company to ignore that. But we are also focusing on adjacent and supportive therapies like vitamins and minerals and protein, which is going to grow better in the time to come.”

— Sheetal Arora, CEO, Mankind Pharma | Q4 FY26

The numbers suggest the basket strategy is already working. Mankind’s anti-diabetes portfolio grew 14.4% in Q3 FY26 — about 1.9 times the market, excluding new GLP-1 launches. Chronic-care now contributes 39.3% of its domestic business. The semaglutide pen launched into an existing chronic-care engine, not into a vacuum.

“What we’re doing, we are basically working on the adjacent therapies like vitamins, minerals, protein side because ultimately, a company which would be selling the complete portfolio will be having a better advantage. So our approach is a bit different than the rest of the people actually.”

— Rajeev Juneja, Vice Chairman & MD, Mankind Pharma | Q4 FY26

There’s a longer game behind it, too. Mankind has a novel molecule, MKP10241 — a small-molecule oral obesity drug — in Phase II trials in Australia. Nothing for FY27 or FY28. But it’s the kind of asset that can turn a defensive GLP-1 launch into an offensive franchise if it works.

Bet 5 — Export the molecule

For companies with international footprints, the Indian market is the appetiser. The main course is everywhere else the innovator is still supply-constrained — Brazil, Canada, the Middle East, parts of Europe.

Dr Reddy’s is the most aggressive here, with 26 GLP-1 products in the pipeline and a plan to launch across 87 countries.

“First of all, I see that as many, many years of opportunity. Actually, we are entering a decade of GLP-1 products. Obviously, it’s going to change and evolve. The full portfolio of GLP-1 for the company is 26 products.”

— Erez Israeli, CEO, Dr. Reddy’s Laboratories | Q1 FY26

Different companies are betting on different geographies. Torrent’s whole international strategy hinges on Brazil — a market whose regulator, ANVISA, is so strict about semaglutide that pharmacies have to keep physical copies of every prescription.

“Each prescription for Semaglutide has to be issued in two copies. And with the indication on the prescription and the pharmacy is required to maintain extensive records, including a copy of each prescription.”

— Sanjay Gupta, Executive Director, International Business, Torrent | Q1 FY26

“Roughly the market is $1 billion for Semaglutide. You can divide it into the injectable at 75% and oral at roughly 25%. Currently, the Ozempic market is declining very fast and Wegovy is growing very fast. There are no generic launches in Brazil as of today.”

— Management, Torrent Pharmaceuticals | Q4 FY26

Biocon is going direct in Europe — selling its own generic liraglutide, an older GLP-1 drug, in the Netherlands rather than through a partner — and out-licensing semaglutide to Ajanta Pharma for 26 countries across Africa, the Middle East and Central Asia.

“We launched generic Liraglutide for diabetes and obesity in the Netherlands as our first ‘direct-to-market’ GLP-1 in the EU. We also signed an out-licensing agreement with Ajanta Pharma to market our vertically integrated drug product, Semaglutide, in 26 countries across Africa, Middle East and Central Asia.”

— Kiran Mazumdar Shaw, Executive Chairperson, Biocon Group | Q3 FY26

Biocon’s cost edge here is structural. The company spent years building fermentation-based capacity to make its peptides — growing them in living cells — rather than taking the more common route of stitching them together through synthetic chemistry. At scale, fermentation brings the cost of the active ingredient down from roughly $200 a gram to between $20 and $50 — a 4-10x advantage rivals can’t easily replicate. In a generic market that will eventually be priced like a commodity, that’s the difference between making money and not. In the September 2025 quarter, Biocon’s generics business grew 24% year-on-year to ₹774 crore, with margins on its biosimilars — near-copies of complex biological drugs — expanding to 28% at the operating-profit (EBITDA) level.

Lupin is leaning on South Africa and Brazil. Emcure picked up Quebec through a Dr Reddy’s partnership. Zydus is taking its differentiated pen to 20-plus markets.

The wrinkle is that this bet has been slower than anyone expected. Canada — meant to be the first big market after the patent expired — stalled for most of the year, with Health Canada clearing no generic GLP-1 at all. Dr Reddy’s, after a Notice of Non-Compliance in October 2025, finally won approval — the first one through. For most of the year, the picture looked like this:

“Of course, the review cycle is long drawn, especially in markets such as Canada, where we have not seen a single generic GLP being approved, including liraglutide, which has not been approved by Health Canada.”

— Siddharth Mittal, CEO & MD, Biocon | Q3 FY26

The export bet has a cleaner economic logic than the domestic one. Innovator pricing abroad is still high, generic competition is thin, and the ₹5,000-crore incremental opportunity Systematix talks about is, in the analysts’ own framing, largely an export number — concentrated in far fewer hands than the domestic chaos suggests.

Bet 6 — Sell the shovels

In any gold rush, some people decide not to dig. They sell the shovels.

In Indian GLP-1, the shovel-sellers split into two distinct camps. One is making the pens for everyone else launching this year. The other is making the chemical raw materials for the next generation of drugs, the ones nobody has launched yet. Both businesses are quietly more profitable than selling the generic itself.

Sub-part A — Make the pens for everyone else

Semaglutide is a hard drug to manufacture. It’s a 31-amino-acid lipidated peptide — a chemically intricate chain that most Indian small-molecule drugmakers can’t produce consistently at industrial scale. And even the companies that can make the active ingredient often can’t fill it into pens themselves, because cartridge fill-finish — the sterile step of loading the drug into the device — needs specialised, isolator-based sterile lines. There are perhaps three or four such facilities in the whole country.

So a separate set of companies decided not to launch generics at all. They decided to make the pens for everyone who is.

OneSource Specialty Pharma is the dominant player. It’s what the industry calls a CDMO — a contract development and manufacturing organisation, a company that builds a drug end-to-end for others to sell under their own labels. And the pitch is exactly that end-to-end-ness: develop the formulation, fill the cartridge, assemble the pen, serialise the box.

“Our biggest value proposition to our customers is end-to-end we supply. Not only we do development for them, we will do commercial manufacturing for fill finish for cartridge, pack it, put it in the box, serialize it. So the box which a patient opens at home is the box coming out of one source site.”

— Neeraj Sharma, CEO & MD, OneSource Specialty Pharma | Q2 FY26

The scale is real. OneSource has signed up more than twenty customers — and has stopped taking new ones. Capacity is being scaled from 40 million units in FY26 to 220 million in FY27. Its customer base holds roughly two-thirds of the Indian generic semaglutide market by value. Several customers have paid capacity-reservation fees up front; others are on take-or-pay contracts, which means they owe OneSource for the reserved capacity whether or not they actually take the product.

“And today as we speak, our customer base total as on end of April holds almost two-thirds of the Indian market share by value of the generic market… We are the first and the only CDMO partner for the first three generic Semaglutide approvals in all the highly regulated markets, US and Canada.”

— Neeraj Sharma, CEO & MD, OneSource Specialty Pharma | Q4 FY26

Gland Pharma is running the same play with cartridges — capacity expanded from 40 million to 140 million units a year, eight GLP-1 contracts signed, six or seven more in the pipeline.

“In the GLP-1 space, we have made significant progress with eight contracts already signed and an additional 6-7 expected to be signed soon. Our current cartridge capacity now stands at 140 million units. Our approach remains disciplined and value-focused, positioning this as a strong mid-to-long-term opportunity with meaningful upside.”

— Srinivas Sadu, Executive Chairman, Gland Pharma | Q4 FY26

The neat thing about this bet is that these companies don’t care who wins the Indian launch war. Whoever ends up selling the pen — they made it.

Sub-part B — Make the building blocks for the next wave

Go one layer deeper. The fill-finish CDMOs need cartridges, the cartridges need an active ingredient, and that active ingredient is a peptide that has to be synthesised from raw chemical pieces. That’s where the second group of shovel-sellers sits.

A quick definition. A peptide is a chain of amino acids — essentially a small protein. Semaglutide itself is a 31-amino-acid peptide. To make a peptide drug, you take individual amino acids, chemically “protect” them so they don’t react in the wrong places, link them together in the right order, and then strip the protections off at the right time. The whole thing get assembled like Lego into the final drug.

Divi’s Laboratories made the most interesting choice here. It flatly refused to make generic GLP-1s. Instead, it sells the Lego pieces — fragments and amino acids — to the original innovators like Novo Nordisk and Eli Lilly, who use them to build their own peptide drugs.

“Divi has strategically decided that we will not look at generic part of peptide synthesis. We are right now fully occupied with the amount of CS projects we have. So, we do not want to venture into that mode.”

— Dr. Kiran S. Divi, Whole-Time Director & CEO, Divi’s Laboratories | Q2 FY26

The economics are very different from Sub-part A. Divi’s makes its own protected amino acids in-house — dull to describe, but it gives the company a grip on cost and on impurity that pure peptide assemblers don’t have. It has earmarked roughly ₹700-800 crore per project for three new dedicated peptide units. Custom synthesis — what it calls its innovator-facing business — already accounts for 56% of Divi’s revenue, and that segment grew 23% year-on-year in Q2 FY26.

“The one unique thing about Divi’s is, we manufacture our own protected amino acids, which gives us both in natural and unnatural, which gives us an edge over everyone, because we control our quantities, we control our cost, we control our impurity profile.”

— Dr. Kiran S. Divi, Whole-Time Director & CEO, Divi’s Laboratories | Q2 FY26

The trade-off is clean. The branded generics are scrapping over a fragmented Indian retail market. Divi’s is selling shovels to the prospectors who still own the gold mine.

Neuland is running a similar bet, but framing it bigger. The global peptide CDMO market, in its telling, has gone from a $1-1.5 billion category to $5-6 billion in just a few years — and most of that explosion is downstream of GLP-1’s success, which has made innovators want to develop the next generation of peptide drugs.

“What used to be a $1 or $1.5 billion market space is now a $5 or $6 billion market space and it is growing very rapidly because more and more drugs are coming out into the market, which are peptides.”

— Saharsh Davuluri, Vice-Chairman & MD, Neuland Laboratories | Q1 FY26

“It’s not just about the weight loss drugs that have been commercialized, but it’s also about the next gens, not just from the large companies, but other companies as well. So there is a plethora of development candidates, which are peptides.”

— Saharsh Davuluri, MD & CEO, Neuland Laboratories | Q4 FY26

Laurus Labs, Syngene, Piramal Pharma and Shilpa Medicare are all running variations of this bet. Different scales, different positioning, but the same thesis: don’t bet on which generic semaglutide wins in India — bet on the entire peptide modality, globally, over the next decade.

A coda — the diagnostics tag-along

There’s one more bet, and it isn’t pharma at all. If millions of new patients go on a powerful weekly injection, somebody has to test their bloodwork. Diagnostic labs see the GLP-1 boom as a downstream opportunity.

Metropolis Healthcare is the most explicit about it:

“On the GLP-1 front, the receptor agonist market in India is currently valued at USD 110 million in 2024 and is projected to grow to USD 500 million by 2030. This shift is likely to drive higher demand for regular monitoring of glucose, lipids, liver, kidney, and cardiac parameters.”

— Ameera Shah, Chairperson, Metropolis Healthcare | Q1 FY26

Dr Lal PathLabs is less convinced — at least so far:

“Patient volume growth is partly a factor of the improved collection and lab network we have put in place. It is definitely not driven by GLP-1.”

— Shankha Banerjee, CEO, Dr Lal PathLabs | Q4 FY26

A bet that’s real but small. The kind of thing that shows up in the numbers two or three years from now, not next quarter.

A footnote on what’s not a bet — the next-generation Indian molecules

Beneath the semaglutide land grab, three Indian companies are quietly building their own proprietary metabolic drugs — ones that could end up mattering more than any generic launch.

Sun Pharma has GL0034 (also called Utreglutide), an in-house GLP-1 molecule now in global Phase II trials for both Type 2 diabetes and MASH, a form of fatty liver disease. Mankind has MKP10241, a small-molecule oral obesity drug, in Phase II in Australia. Lupin is developing its own oral semaglutide in-house and has partnered with China’s Gan & Lee on Bofanglutide, a novel fortnightly GLP-1 agonist.

None of these reach the market for two to four years. None move FY27 earnings. But they’re the only assets in the listed Indian pharma universe that could turn GLP-1 from a defensive franchise into an offensive one.

TL;DR

Semaglutide came off patent in India on 21 March 2026, and within a week thirteen companies had launched twenty-six generic brands. But the synchronised launch hides six different answers to the same question — how do you actually make money off this molecule? Most went for the generic pen and split into price tiers; Eris reframed it as a metabolic drug for “thin-fat” India; Emcure and Cipla skipped the generic fight and sold the innovators’ own products; Zydus won by licensing a better pen to its rivals; Mankind sat out the price war; Dr Reddy’s, Torrent and Biocon chased exports; and OneSource, Gland, Divi’s and Neuland sold the shovels. The point isn’t that everyone launched — it’s that almost no one chose to compete head-on with the company next door. Combined listed-player revenue is still just ₹100-130 crore a month. The real money is two years out, and most of it will be made outside India.

That’s it for now! Your feedback will really help shape how The Chatter evolves. Drop it down in the comments below!

Disclaimer: We’ve used AI tools in filtering and cleaning up these quotes & narratives so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

Actually a good article explaining the current dynamics in indian pharna

Good overview and classification of the landscape. You have however missed out on Shaily Engineering which makes pens