Hi, I’m Kashish and I work on Plotlines.

It builds on Chatter, but with a more structured lens. Instead of looking at management commentary from earning concalls in isolation, we track a single theme across companies and over time to connect the dots. The goal is to piece together how narratives evolve, and surface the deeper structural shifts shaping industries.

Today, we cover the microfinance credit cycle.

From “not expecting any known risks” to “the issues are clearly behind the industry” — eighteen companies, eight quarters, and a credit cycle that rewrote the rules of Indian microfinance, told entirely through the words of the people who lived it.

The Goldilocks Trap

In March 2024, the Indian microfinance industry was in a celebratory mood. Asset quality had recovered from the pandemic. Growth was strong. Guidance was ambitious. The sector had disbursed record volumes and the worst of COVID-era stress was firmly in the rearview.

Satin Creditcare’s HP Singh called FY24 a “momentous chapter” in the company’s 33-year journey. Muthoot Microfin’s CEO saw a clear path to 4.5% ROA. CreditAccess Grameen, the country’s largest pure-play microfinance NBFC, set its sights on numbers that would have seemed outlandish just two years earlier.

“Assuming a stable operating environment, we look forward to achieving loan portfolio growth of 23% to 24% in FY25. We are anticipating credit cost of 2.2% to 2.4%... Overall, we aim to achieve ROA of 5.4% to 5.5% and ROE of 23.0% to 23.5% in FY25.”

— Udaya Kumar Hebbar, Managing Director, CreditAccess Grameen | Q4 FY24

Bandhan Bank, which had spent three painful years cleaning up pandemic-era stress in its microfinance book — the “Emerging Entrepreneurs Business” in Bandhan parlance — declared the legacy behind them. Its SMA-0 pool had halved. Slippages were trending down. The technical write-off of the old book was done.

SMA-0 pool is the set of loan accounts that are overdue by up to 30 days, indicating the earliest stage of repayment stress.

Slippages are loans that move from standard (performing) to NPA status during a period.

“So I think as Rajeev said, we believe that decisively, we are out of the pandemic problem. In fact, all the parameters, as you see, you can clearly see that practically the slippages has come down significantly. Recovery rates have improved. DPD pool has dried down.”

— Ratan Kesh, Executive Director and COO, Bandhan Bank | Q4 FY24

When analysts asked CreditAccess’s managing director what risks he saw on the horizon, his response carried the confidence of a man who had navigated COVID, demonetization, and the Andhra Pradesh crisis — and come out the other side each time.

“We are not expecting any known risks actually. Known risk if you see the last 10 years or 15 years, the risks which have come to this industry are unknown. Whether it is COVID or demonetization, the second COVID, all are unknown. The industry has not lost because of any known risks.”

— Udaya Kumar Hebbar, Managing Director, CreditAccess Grameen | Q4 FY24

It was a reasonable statement grounded in history. Every previous microfinance crisis — Andhra Pradesh in 2010, demonetization in 2016, COVID in 2020 — had been triggered by an external shock that no one could have modelled for. The sector’s risk management frameworks were built around this assumption: the threats come from outside, and when they pass, business returns to normal.

Not everyone agreed. A few voices struck a different note that quarter. Kotak Mahindra Bank’s new CEO Ashok Vaswani looked at the same data and saw a warning sign rather than an all-clear.

“If you look at what is happening in the industry and look at loss rates and stuff like that post the COVID provisions, it has really been a Goldilocks period for the last 2-3 years at least since COVID. Now, all of us know that credits go through cycles. At this point in the cycle, to go out and get aggressive on credit, I don’t think it is a smart thing to do.”

— Ashok Vaswani, MD & CEO, Kotak Mahindra Bank | Q4 FY24

HDFC Bank was quietly building buffers while the sun was shining — creating what it called “countercyclical provisions,” essentially setting money aside during good times for the bad times it expected would eventually come.

“We have, as a part of prudent risk management, created a countercyclical provision, which is a provision in good times.”

— Sashidhar Jagdishan, MD & CEO, HDFC Bank | Q4 FY24

IndusInd Bank, one of the largest MFI lenders through its subsidiary BFIL, was even more specific about where it saw cracks. Its CEO Sumant Kathpalia said the bank had spotted stress building in Punjab eleven months before the rest of the industry acknowledged it.

“We saw Punjab coming 11 months ago. We saw the waves of Punjab coming and even some parts of Odisha and Bihar also coming and some parts of UP also. We started exiting those portfolios at that point.”

— Sumant Kathpalia, MD & CEO, IndusInd Bank | Q4 FY24

Whether the early detection translated into early protection would become one of the more revealing questions of the cycle.

• • •

Something Breaks

The first tremors arrived in Q1 FY25 — the April-June quarter of 2024. A brutal heatwave across northern India made fieldwork difficult for loan officers accustomed to collecting repayments door-to-door. General elections in April and May disrupted collection schedules — in several states, political activists ran “Karj Mukti Andolans,” loan forgiveness campaigns that encouraged borrowers to stop repaying.

“Majority of that activity has stopped. It was almost linked with the election activity that was going on during that period in Q1. So now we don’t have too much of activism.”

— Sadaf Sayeed, CEO, Muthoot Microfin | Q1 FY25

These were plausible, temporary explanations. Heat waves pass. Elections end. But underneath the seasonal noise, something structural was breaking. At IDFC First Bank, the JLG collection efficiency — the percentage of current-bucket borrowers who pay on time — slipped from 99.7% to 99.2%. Half a percentage point sounds trivial. In microfinance, where the entire model depends on near-perfect repayment discipline, it was a red alert.

“Normally, pre the floods, our credit loss in the JLG book used to be around 1.6%. Now our estimate of credit cost for this year on the joint liability group, because we are 60% concentrated in Tamil Nadu, it is expected around 5% or a little short of it.”

— V. Vaidyanathan, MD & CEO, IDFC First Bank | Q1 FY25

A brief detour is useful here to understand what was actually going wrong. Microfinance in India works primarily through the Joint Liability Group model — small groups of borrowers, typically 5-10 women, who collectively guarantee each other’s loans. The model’s genius is that it replaces traditional collateral with social pressure: if one borrower defaults, the group faces consequences. It works remarkably well in normal times, keeping credit costs at 1.5-2.5% despite lending to some of the most economically vulnerable households in the country.

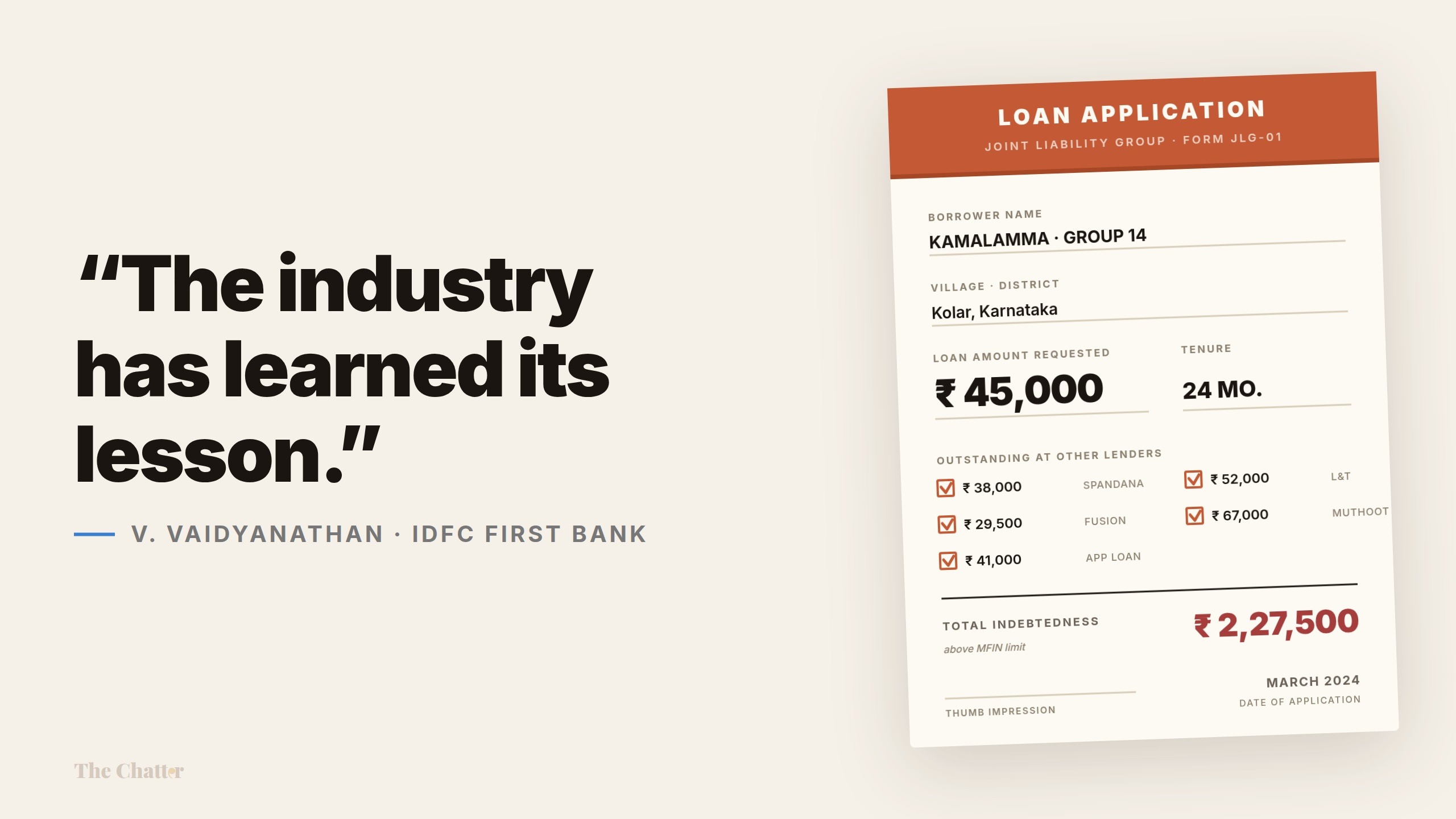

But the model has a critical weakness. It doesn’t control how many groups — or how many lenders — a single borrower joins. And since 2022, something had quietly shifted. Credit bureau data showed that borrowers were taking on loans from more and more institutions simultaneously. Ticket sizes were creeping up. Total indebtedness per borrower was rising fast.

Fusion Finance, a mid-sized NBFC-MFI, laid this out in stark numbers.

“I would like to draw your attention to Slide #8 on our customer leverage. As you can see, our outstanding per customer is mostly below INR 40,000. But 33% of these customers have outstanding greater than 1 lakh across micro finance loans. This increased from 23% in March to 32% March ’24.”

— Devesh Sachdev, MD & CEO, Fusion Finance | Q1 FY25

In twelve months, the share of borrowers carrying more than Rs 1 lakh in microfinance debt had jumped by 10 percentage points. And these were just the loans visible on credit bureaus. Equitas SFB’s veteran founder P.N. Vasudevan — who had been in microfinance for nearly two decades — identified another layer that was harder to track.

“What is not really understood or clear is also there’s some kind of a parallel lending happening to the same set of borrowers by so called app loan companies.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q3 FY25

Spandana Sphoorty’s data quantified the damage from overleveraging: borrowers with five or more lenders were just 12% of the company’s AUM but contributed 21% of its arrear bucket. The more lenders a borrower had, the more likely they were to default — and the industry had spent two years adding lenders to each borrower’s profile.

The most important observation of Q1 came from Vasudevan, who named what nobody else was willing to say clearly: for the first time in living memory, this crisis wasn’t caused by something that happened to microfinance. It was caused by microfinance itself.

“For a change, the crisis or it’s not the word crisis, but at least a stress levels in microfinance for a change is not induced by an external one. This is the first time, I think, in the last 15 years that I know or 17 years that I have been in this business that I’m saying that it’s not an external event trigger, but it’s something inherently coming up from the sector itself.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q1 FY25

Not everyone agreed with this framing. Spandana’s MD Shalabh Saxena pushed back on the idea that overleveraging was systemic.

“I personally do not believe there is a systemic over-leverage issue across the industry. I firmly believe that. There could be a few pockets, a few institutions here and there.”

— Shalabh Saxena, MD & CEO, Spandana Sphoorty | Q1 FY25

Within two quarters, the data would prove him wrong.

• • •

The Guardrails

In July 2024, MFIN — the Microfinance Institutions Network, which functions as the sector’s self-regulatory organization — rolled out what became known as the Guardrails. These were a set of industry-wide lending norms, agreed upon by members representing roughly 87% of the microfinance market, aimed at curbing the overleveraging that was now clearly driving the stress.

The key rules: no borrower should have loans from more than four microfinance lenders. Total unsecured indebtedness, including microfinance, should not exceed Rs 2 lakh. Lenders were required to check bureau data before every disbursement, not just at onboarding.

The guardrails were a significant step, but they were forward-looking — they could prevent new overleveraged loans from being created, but they couldn’t fix the existing book. Borrowers who already had five or six lenders would continue to struggle. The stress already embedded in portfolios would need to be absorbed through provisions, write-offs, and time.

The impact on new business was immediate. At Muthoot Microfin, about 11% of loan applications that would previously have been approved were now being rejected under the new rules. Satin Creditcare reported that at the time the guardrails kicked in, just 1% of their existing clients exceeded the four-lender cap — a sign that some companies had been more disciplined than others.

Fusion stopped disbursements entirely in 104 of its branches. CreditAccess tightened credit filters. Spandana paused new member acquisition in 230 branches and stopped sourcing new-to-credit customers altogether. The industry was simultaneously trying to fix the new pipeline while absorbing damage from the old one.

The CreditAccess team tried to quantify the timeline.

“We however, expect the delinquency trend to stabilise in the coming quarter and credit cost within the guided range of 2.2% to 2.4% for the year.”

— Udaya Kumar Hebbar, Managing Director, CreditAccess Grameen | Q1 FY25

That guidance would not survive the next ninety days.

• • •

Into the Storm

By September 2024, the scale of the problem was undeniable. What had started as “stress in some pockets” was now a full-blown industry credit cycle. The heat waves and elections were months behind, but collection efficiencies were still deteriorating. Equitas’s Vasudevan captured the moment of realization.

“The industry and us included were quite caught by surprise when the collection efficiency dipped further in Q2 for no apparent external reasons. In our case, it dropped from 98.9% of Q1 down to 98.2% in Q2. And when this happened across geographies, it was clear that an important reason for the stress was as much internal as external.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q3 FY25

CreditAccess Grameen, which six months earlier had guided for 23-24% portfolio growth and 5.4% ROA, rewrote its entire outlook.

“In light of the current industry landscape and short-term challenges encountered, we have revised our estimate for FY25 annual performance guidance. We anticipate loan portfolio growth of 8-12%, NIM of 12.8-13.0%, credit cost of 4.5-5.0%, ROA of 3.0-3.5%, and ROE of 12.0-14.0%.”

— Udaya Kumar Hebbar, Managing Director, CreditAccess Grameen | Q2 FY25

Growth guidance halved. ROA guidance cut by nearly 40%. Credit cost guidance doubled. And CreditAccess was among the better-positioned players — it had been conservative relative to its peers, with a diversified geographic footprint and a long track record. For the more concentrated and leveraged players, the numbers were far worse.

Fusion Finance reported a quarterly credit cost of Rs 693 crore — a number large enough to trigger covenant breaches with lenders. This is worth pausing on: Fusion’s borrowing costs and credit lines depended on maintaining certain financial ratios. When its losses blew through those thresholds, its own access to capital came under threat. The stress wasn’t just flowing from MFI borrowers to MFI companies — it was threatening to flow from MFI companies to their lenders, creating a potential second-order shock.

“I would like to mention that post the review of our auditors, our actual credit cost for Q2 FY25 has been determined at Rs. 693 crore. The elevated provisioning has been due to us proactively taking accelerated provisions... Looking at our portfolio performance and challenges faced by the sector, our auditor wants to bring to the attention that there are covenant breaches that will require waivers.”

— Devesh Sachdev, MD & CEO, Fusion Finance | Q2 FY25

IDFC First Bank’s V. Vaidyanathan, who had spent the previous quarter framing the Tamil Nadu floods as a one-off episode, acknowledged the broader reality and took an aggressive provisioning stance.

“Now, what we have done this quarter is because microfinance is an issue and we cannot wish it away because the microfinance portfolio is disturbing in many parts of India. So, what we have done is that in SMA-1 and SMA-2, we have taken provisions and therefore... almost 99% of SMA-1 plus SMA-2 has been provided for by the Bank, fully.”

— V. Vaidyanathan, MD & CEO, IDFC First Bank | Q2 FY25

Ujjivan Small Finance Bank, one of the larger microfinance-focused SFBs with a significant presence in southern states, saw its PAR — the portfolio at risk, measuring any loan that’s even one day overdue — climb sharply.

“On asset quality, as mentioned earlier, we are observing stress in the microfinance segment, due to which our PAR has increased to 5.1% in September 24 vs 4.2% in June 24. PAR 0 for our group loan portfolio has increased to 5.5% in September 24 versus 4.1% in June 24.”

— Sanjeev Nautiyal, MD & CEO, Ujjivan SFB | Q2 FY25

IndusInd Bank’s CEO Sumant Kathpalia — who had claimed to spot the trouble eleven months early — was now projecting confidence that the worst would be over within weeks.

“In my opinion, if everything goes well, within two months we should start seeing the flow rates coming down in this business... I am very bullish on the microfinance segment, and I think you will see the stability coming in very soon.”

— Sumant Kathpalia, MD & CEO, IndusInd Bank | Q2 FY25

That timeline would prove wildly optimistic. Kathpalia himself would not see it through — within months, he would exit the bank amid a governance crisis triggered in the bank’s derivative portfolio.

Vasudevan, characteristically more measured, offered the hardest truth of the quarter.

“This is the first time I’m seeing where an extended period of nearly 9, 10 months, we have been seeing high slippages and it’s by all of us and in many markets. So it’s very difficult to tell you within what time frame we expect it to come back to normalcy.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q1 FY25

• • •

The Darkest Quarter — and the Turn

Q3 FY25 — October through December 2024 — was when the stress peaked for most companies. Bandhan saw microfinance slippages of Rs 1,196 crore in a single quarter. Its collection efficiency outside West Bengal dropped to 96.3%. Satin Creditcare’s PAR-1 rose to 6.8%. RBL Bank described conditions on the ground as being “in a flux.”

But this quarter also contained the single most important inflection point of the entire cycle: December 2024.

For months, the data had been uniformly grim. Then, almost simultaneously, company after company reported the same thing — the first material improvement in the current bucket, the pool of borrowers who are not yet overdue. When this pool stops deteriorating, it means fewer borrowers are falling into trouble for the first time. It doesn’t fix the existing NPAs, but it signals that the pipeline of future stress is narrowing.

CreditAccess’s MD, who had initially expected the peak in September, acknowledged the delay but confirmed the reversal.

“Our initial assessment of the current delinquency cycle being transitory in nature has come true as we see the new delinquency addition rate slowing down across various geographies in mid-November 2024... The new delinquency trend reversal was materially visible across various markets beginning mid-November, getting further stronger in December and January.”

— Udaya Kumar Hebbar, Managing Director, CreditAccess Grameen | Q3 FY25

RBL Bank saw the same inflection.

“In the JLG segment, the situation on the ground has been in a flux for most of the past months, but December has seen the first material uptick in collection efficiency and the recoveries of old NPAs.”

— R. Subramaniakumar, MD & CEO, RBL Bank | Q3 FY25

Fusion’s Devesh Sachdev, whose company had been among the hardest hit, was watching a different metric — the new loans disbursed under tighter guardrails since August.

“Even I can tell you one more data, that the new sourcing which we are doing, which we changed in the middle of August. And now when I look it’s a five-month MOB, though it is too early, it’s just a 5 months MOB, but I believe the numbers are infant or early delinquency is clearly showing trends which we have seen in year 2022, ’23.”

— Devesh Sachdev, MD & CEO, Fusion Finance | Q3 FY25

This was quietly one of the most significant data points of the cycle. Loans written under the new guardrails weren’t just marginally better — they were performing like pre-crisis vintage. The guardrails were working.

But Bandhan’s new MD Partha Pratim Sengupta — who had replaced Ratan Kesh in yet another leadership change during the crisis — offered a note of caution that tempered the optimism. The SMA-0 book was improving, but the backlog of loans already deeper in arrears still needed to work through the system.

“So, maybe the level of slippage could not be 1,196 in EEB book, what we have witnessed in Q3, but it will be substantial... But slippages, we are seeing the trend, but at the same time as you are witnessing, you see that our SMA-0 book is improving... But the trend is reversing.”

— Partha Pratim Sengupta, MD & CEO, Bandhan Bank | Q3 FY25

The green shoots were real. But the cleanup was far from over.

• • •

The Reckoning

Q4 FY25 — January through March 2025 — became the quarter of reckoning. The turn in collection efficiencies was confirmed, but the damage from the preceding three quarters had to be absorbed. Companies took massive write-offs to clear the decks. The numbers were staggering.

Equitas SFB revealed the full toll. Its microfinance credit cost went from 2.3% in FY24 to 11.37% in FY25 — a nearly fivefold increase that wiped away Rs 630 crore of profit and dragged the bank’s overall ROA down to 0.32%.

“Last year turned out to be a tough year. We had credit cost in Microfinance portfolio moving up from 2.3% in FY ’24 to 11.37% in FY ’25, wiping away about INR 630 crores of profit of the bank.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q4 FY25

“In response to these headwinds, the bank slowed down its fresh disbursements in Microfinance, leading to a drop in the MFI advances from INR 6,265 crores in March ’24 to just around INR 4,500 crores in March ’25.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q4 FY25

Spandana Sphoorty posted a net loss of Rs 1,035 crore for the full year. CreditAccess wrote off Rs 1,124 crore, including Rs 479 crore in accelerated write-offs of non-paying 180+ DPD accounts. Muthoot Microfin saw its GNPA climb to 4.84% — but its CEO called this the peak.

“So our GNP levels are at 4.84%, which is at an elevated number. But this is the peak of these GNPAs. We feel that in coming quarters, these numbers will only come down because we are seeing better collection efficiency.”

— Sadaf Sayeed, CEO, Muthoot Microfin | Q4 FY25

RBL Bank took perhaps the most aggressive provisioning step of the entire cycle — writing its JLG net NPA to zero in a single quarter.

“In the JLG business, we normally take 25% provisioning each quarter on NPAs, but we have now taken 100% provisioning on the NPA as at March 31, 2025. This means we have a nil net NPA in the JLG business. We have also taken 75% provisioning amounting to INR 283 crores on SMA-0, 1 and 2.”

— R. Subramaniakumar, MD & CEO, RBL Bank | Q4 FY25

And then there was IndusInd Bank. In an industry already reeling from credit stress, IndusInd disclosed something that went beyond a credit cycle — it was a governance failure. An internal review found that microfinance loans at its subsidiary BFIL had been misclassified, concealing Rs 1,885 crore in under-provisioning and unrecognized NPAs.

“The review has also identified the misclassification of certain microfinance loans has resulted in under-provisioning and non-recognition of NPAs aggregating to Rs 1,885 Crores. The Bank has addressed the underlying cause and is in the process of taking actions for staff accountability.”

— Sunil Mehta, Chairman, IndusInd Bank | Q4 FY25

The disclosure triggered a leadership overhaul. Rajiv Anand replaced Kathpalia as MD & CEO. The microfinance subsidiary’s governance framework was restructured for “greater transparency.” It was a stark reminder that credit cycles don’t just stress balance sheets — they expose operational weaknesses that good times had papered over.

Meanwhile, the industry’s aggregate footprint was shrinking. This is a number that didn’t get much attention in individual earnings calls but told a dramatic story at the sector level.

“The overall loan outstanding at the sector, which was about INR 4.4 lakh crores in March ’24, came down to about INR 3.75 lakhs in March ’25 and further down to INR 3.5 lakh crores in June ’25.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q2 FY26

From Rs 4.4 lakh crore to Rs 3.5 lakh crore in fifteen months — the entire Indian microfinance industry shrank by 20%. That’s roughly Rs 90,000 crore of credit that was withdrawn from some of the poorest households in the country. The human cost of an industry correcting its own excesses.

IDFC First Bank’s Vaidyanathan, whose bank had taken provision hits early and heavily, offered a framing that captured what this quarter was — not the start of a new problem, but the crest of a wave.

“You think of this 2025 as a year that this has happened because of microfinance. You think of it that 2026, we will stage a smart recovery. And FY 27, FY 28, FY 29, we should be back winning ways.”

— V. Vaidyanathan, MD & CEO, IDFC First Bank | Q4 FY25

• • •

The Proof

The first sign that the recovery was real — not just hoped for — came from CreditAccess Grameen’s Q1 FY26 results. The company that had slashed guidance a year earlier now reported its highest-ever first-quarter disbursement.

“Our Q1 FY’26 performance has created a new benchmark, achieving the highest ever 1st Quarter disbursement in our history. This is a testament to our resilience and agility that define us given that we are coming off the back of a challenging credit cycle.”

— Ganesh Narayanan, CEO and MD Designate, CreditAccess Grameen | Q1 FY26

Note the leadership change here too — Ganesh Narayanan had taken over from founding MD Udaya Kumar Hebbar, whose guidance had shaped the company through both the confidence of Q4 FY24 and the crisis that followed. CreditAccess wasn’t alone. Bandhan had moved from Ghosh to Kesh to Sengupta in the span of two years. Spandana’s MD Shalabh Saxena — who had pushed back on the overleveraging thesis — had exited, replaced by Ashish Damani as interim CEO. Fusion brought in Sanjay Garyali. The cycle had churned leadership across the sector.

But the data was now more important than the names on the door. The deleveraging that the MFIN guardrails had set in motion was showing up in every company’s investor presentation with striking consistency. The overleveraged borrower pool that had caused the crisis was being systematically drained.

“GLP of borrowers with greater than 3 pre-lenders stood at 11.1% in June 2025 versus 25.3% in August 2024. GLP of borrowers with greater than 2 lakh unsecured indebtedness stood at 9.5% as of June 2025 compared to 19.1% in August 2024.”

— Ganesh Narayanan, CEO and MD Designate, CreditAccess Grameen | Q1 FY26

Muthoot Microfin saw the same pattern from the industry-level data.

“If you look at the overall industry, the leverage customers were around 20%. They have come down to around 8%, which is more than 4 loans.”

— Sadaf Sayeed, CEO, Muthoot Microfin | Q1 FY26

And the proof that the guardrails were producing a fundamentally better book — not just a smaller one — came from Equitas.

“We had implemented the MFIN Guardrail 2.0 from Jan ’25. Out of the portfolio created between Jan to June of ’25, the X-bucket efficiency is about 99.6%, which is more or less what we used to have before this whole crisis started sometime in the first quarter of last year.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q1 FY26

New loans, written under new rules, were performing at pre-crisis levels. Spandana’s data was even more definitive — its FY26 disbursements were tracking at 99.9% collection efficiency. The problem had been in the origination standards, the guardrails had fixed the origination standards, and the new book was proving it.

Fusion Finance, which less than a year earlier had reported covenant breaches and a Rs 693 crore quarterly credit cost, showed a steady trajectory of decline.

“Credit costs have steadily declined QoQ from Rs. 571 Cr in Q3 FY25 to Rs. 253 Cr in Q4 FY25 and further to Rs. 178 Cr in Q1 of FY26. GNPA improved from 7.92% in Q4 FY25 to 5.43% in this quarter.”

— Devesh Sachdev, Managing Director, Fusion Finance | Q1 FY26

Muthoot Microfin, which had posted a loss-making FY25, reported a small but symbolically significant quarterly profit — Rs 6.2 crore. Modest. But the direction mattered more than the magnitude.

“Though it’s a very modest profit, more importantly, it indicates a firm ushering of a turnaround within the operation and the financial performance of the company.”

— Sadaf Sayeed, CEO, Muthoot Microfin | Q1 FY26

• • •

The Industry Exhales

In April 2025, Guardrail 2.0 kicked in — tightening the lender cap from four to three, and further restricting indebtedness limits. Some companies, like Spandana, had already implemented stricter rules from January. The immediate effect was another spike in rejection rates and a temporary pause in the recovery of collection sentiment. Utkarsh Small Finance Bank’s CEO noted the disruption.

“From 1st of April 2025, they changed it to 3 lender caps. Because of that, we saw some more slippages or little elevated credit cost during this quarter. And you must have seen that is more or less industry phenomena.”

— Govind Singh, MD & CEO, Utkarsh SFB | Q1 FY26

But by Q2 FY26, the adjustment was absorbed. And the tone in earnings calls shifted from cautious optimism to something closer to relief. IDFC First’s Vaidyanathan, who had spent five quarters absorbing microfinance losses, said what many were feeling.

“Looking ahead, our own sense is that this microfinance issue is behind us. It’s really taken a lot out of us in the last 5 or 6 quarters. Many of you may have almost begun to lose confidence in us.”

— V. Vaidyanathan, MD & CEO, IDFC First Bank | Q2 FY26

By Q3 FY26 — December 2025 — the normalization was broad-based. Collection efficiencies across the sector had returned to 99.4-99.7%, close to or at pre-crisis levels. Monthly PAR accretion — the rate at which new loans fall overdue — had collapsed. CreditAccess reported the number at 18 basis points in December, down from 47 bps in September.

Fusion Finance returned to profitability — a PAT of Rs 14 crore. Its new CEO described it as an inflection point.

“Q3 represents an important inflection point for Fusion. The business has now entered a phase of controlled stabilization and disciplined execution. I’m pleased to share that we have returned to profitability this quarter.”

— Sanjay Garyali, MD & CEO, Fusion Finance | Q3 FY26

Lenders who had pulled back from the sector during the crisis were returning. Fusion noted that “several banks have freshly opened up” and institutions that were in “wait-and-watch mode” had started actively re-engaging. The wholesale funding squeeze — the second-order effect of the credit cycle — was easing.

RBL Bank’s JLG disbursals had crossed Rs 700 crore monthly, with early bucket collection efficiency at 99.5%.

“The disbursal in the JLG segment is at a run rate of INR 700 crores per month versus INR 550 crores in the previous quarter. The good news is that the early bucket collection efficiency is 99.5%. This is as good as one has got in this segment for a long time.”

— Jaideep Iyer, Head of Strategy, RBL Bank | Q3 FY26

Bandhan declared the de-growth phase in its microfinance book over. Muthoot was back to normalized disbursements of Rs 850 crore a month. Ujjivan SFB reported bucket-X collection efficiency of 99.7% in December — its highest in the current fiscal — with 10 out of 10 states at 99.6% or above.

Satin Creditcare’s HP Singh, who a year earlier had been deploying 1,100 dedicated collection staff to manage overdue buckets, offered a simple verdict.

“The headwinds are practically over. You can see green shoots now coming in. I think overall it bodes well for the industry as well as for us.”

— Dr. HP Singh, CMD, Satin Creditcare | Q3 FY26

And Equitas’s Vasudevan, who had been the first to diagnose this crisis as self-inflicted, delivered the closing line for the cycle.

“As we sign off, I can only reiterate that I think the issues of microfinance is clearly behind not just us but the industry. And going forward, let’s hope for better times for all of us.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q3 FY26

While the MFI players had been fighting for survival, the large diversified banks had watched from a very different vantage point. HDFC Bank’s microfinance exposure was less than 1% of its total book. SBI’s chairman noted their MFI portfolio of Rs 10,000-11,000 crore “does not really add up to anything.” By Q3 FY26, HDFC Bank’s deputy MD was using language that felt like it belonged to a different industry entirely.

“The banking industry right now to borrow a term is going through a Cinderella phase where you’ve got very strong balance sheets... We have the lowest accretion of gross NPAs and net NPAs are at decadal lows.”

— Kaizad Bharucha, Deputy MD, HDFC Bank | Q3 FY26

A Cinderella phase for large banks. A near-death experience for several MFIs. The same economic cycle, experienced at entirely different altitudes depending on how much microfinance a company carried on its books.

• • •

What Changed

The industry that emerged from this cycle was not the one that entered it. The changes were structural, deliberate, and in some cases, permanent.

Every major player shrank its microfinance portfolio as a share of total assets. Equitas took its MFI mix from 20% to 8.5% and intended to stabilize at 10%. IDFC First expected its microfinance book to bottom at Rs 7,500 crore — half its peak. Bandhan’s non-microfinance book now accounted for 63% of advances, up from 45% two years earlier. RBL shrank its JLG book by 23% and targeted keeping it at 6-7% of advances, down from 9%. The consensus: microfinance at 7-10% of the balance sheet, not 20%+.

Companies were also insuring against the next cycle. CGFMU — the Credit Guarantee Fund for Micro Units — had existed before the crisis but was lightly used. Now it was becoming standard.

“The intent is to take that to 100% and thereby eliminating the tail risk on the microfinance business. So, if you are able to do that and manage the proportionality of the business somewhere between 7% - 8% of the asset side, I do believe that we can build a more predictable and profitable microfinance business going forward.”

— Rajiv Anand, MD & CEO, IndusInd Bank | Q3 FY26

RBL reached 80%+ CGFMU coverage on its standard JLG book. IDFC First had been insuring since January 2024 — one of the earliest movers.

Kotak Mahindra went further than portfolio caps and insurance. It did something more fundamental — it replaced the joint liability group model itself.

“What we have done is that we have replaced the joint liability group model with individual underwriting risk-based models. And therefore, the way we are dispersing and where we are not dispersing has a lot to do with what the model says are the propensity for repayment.”

— Ashok Vaswani, MD & CEO, Kotak Mahindra Bank | Q1 FY26

It was a quiet admission that the JLG model — the foundational innovation of microfinance — had weakened. Social pressure among group members was no longer enough to ensure repayment in an environment where borrowers had loans from five different institutions. Individual credit assessment, powered by bureau data and machine learning, was being layered on top of or replacing the group guarantee.

And the baseline expectations for the business had permanently shifted. The “old normal” of 1.5-2% credit costs was gone. Vasudevan was explicit about what the “new normal” looked like.

“Post corona, we thought around 3% is a normal credit cost for microfinance. Now post this 2024 overleveraging crisis, probably anywhere between 3% to 4% could be a normal credit cost for microfinance.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q1 FY26

Three to four percent, not two. The industry had recovered, but to a worse steady state than before. The premium for lending to this segment had been repriced — not by a regulator, but by experience.

Vasudevan also offered the most honest structural assessment of the sector — one that explained why every company was simultaneously declaring the crisis over while also reducing its exposure to the business that had built them.

“And in spite of that, we have been seeing a series of crisis in the Microfinance sector time and again for various reasons. The reasons change, but the repetitiveness of the crisis doesn’t change.”

— P.N. Vasudevan, MD & CEO, Equitas SFB | Q4 FY25

The industry had survived. The cycle had turned. But the companies that came out the other side were building for a different future — one where microfinance remained in the portfolio but never again dominated it. Smaller books, government guarantees, individual underwriting, tighter guardrails, higher steady-state credit costs. The cycle didn’t just create losses. It created a new architecture.

• • •

What to Watch

• The “new normal” credit cost. Most companies guide for BAU credit costs of 2.5-3.5% going forward, up from the pre-crisis expectation of 1.5-2%. Whether this holds through FY27 will confirm the repricing is real and not just post-crisis caution.

• Karnataka. The last major geography to stabilize. Several companies still flag it as lagging behind the rest of the country. CreditAccess expects Karnataka’s PAR accretion to normalize by end of Q1 FY27.

• CGFMU as industry standard. IndusInd targeting 100%, RBL at 80%+, IDFC First already covered. If credit guarantee becomes universal, the tail risk profile of microfinance changes permanently — but it also adds ~1% to the cost of lending, which has to be passed on somewhere.

• Guardrail 2.0’s growth ceiling. The 3-lender cap is structurally limiting the addressable borrower pool. Several managements now expect industry growth to settle at 10-15% — a far cry from the 25%+ that was standard before the crisis. Whether this is a temporary adjustment or a permanent reset will shape the sector’s economics.

That’s it for now! Your feedback will really help shape how The Chatter evolves. Drop it down in the comments below!

Disclaimer: We’ve used AI tools in filtering and cleaning up these quotes & narratives so there maybe some mistakes. Now, if you are thinking why we are using AI, please remember that we are just a small team of 5 people running everything you see on Zerodha Markets 😬 So, all the good stuff is human and mistakes are AI.

excellent read, thank you.

one thing that could have been to interesting to look at is when the stocks topped and bottomed out at an index level (any microfinance focused index) - just to see if markets were able to capture all of this earlier than the numbers showed up in earnings or were they reactionary

well written , in fact is a chronicler for posterity